Embed Size (px)

Citation preview

www.elsamconsult.com 1

EMAC

AUDIT COMMITTEE TRAINING

By: Sako Mayrick

Dar Es Salaam

ELSAM MANAGEMENT CONSULTANTS

www.elsamconsult.com 2

EMAC

Who are we? Elsam Management Consultants

(EMAC) is a pool of professional consultants in management disciplines established as a limited liability company since 2006

Core Functions are: Recruitment, Training and Consultancies

More details: www.elsamconsult.com

Welcoming Remarks

www.elsamconsult.com 3

EMAC

Introduction of facilitators Self introduction to others on your team Recap- Share something on personal

experience in Risk Management and high level expectations of this training

Pick 1-Identify a risk-discuss it as both a threat and an opportunity

Report to the a large group pick a spokesperson

Welcoming Remarks

EMAC

AUDIT COMMITTEES ROLE AND

RESPONSIBILITIES

EMAC

Contents

1. Introduction 2. Audit Committee Issues3. Financial Management4. Operations Management5. External and Internal Audit6. Other Considerations and

Reporting

EMAC

Part I

Introduction & Overview

EMAC

Introduction Audit Committee is a part of governance

of entity Governance is the system by which

organizations are directed and controlled. It includes rules and procedures for

making decision on corporate affairs to ensure success while maintaining the right balance with stakeholder’s interest.

Audit Committee is one of the major pillars of governance system in public companies

EMAC

Entity Governance Structure

What is the entity Governance?

Discussions

EMAC

Role of Audit Committee General

Oversight of financial reporting Risk management Internal control Compliance Ethics Management Internal audit

Management, the board and the audit committee all play critical roles in entity’s tone at the top

Role of Audit Committee

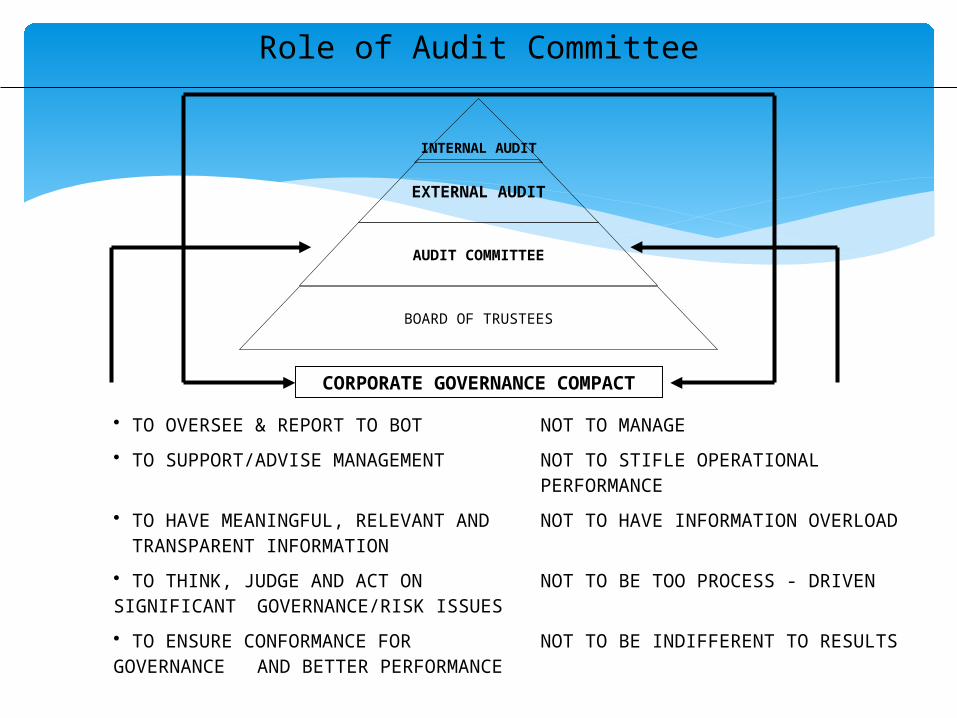

• TO OVERSEE & REPORT TO BOT NOT TO MANAGE

• TO SUPPORT/ADVISE MANAGEMENT NOT TO STIFLE OPERATIONAL PERFORMANCE

• TO HAVE MEANINGFUL, RELEVANT AND TRANSPARENT INFORMATION

NOT TO HAVE INFORMATION OVERLOAD

• TO THINK, JUDGE AND ACT ON SIGNIFICANT GOVERNANCE/RISK ISSUES

NOT TO BE TOO PROCESS - DRIVEN

• TO ENSURE CONFORMANCE FOR GOVERNANCE AND BETTER PERFORMANCE

NOT TO BE INDIFFERENT TO RESULTS

CORPORATE GOVERNANCE COMPACT

INTERNAL AUDIT

EXTERNAL AUDIT

AUDIT COMMITTEE

BOARD OF TRUSTEES

Corporate Governance Model

EffectiveGovernance

EMAC

What is an audit committee?

It is established with aim of enhancing confidence in the integrity of entity process and procedure relating to internal controls and corporate reporting including financial reporting

It provides an independent re-assurance to the board through its monitoring and oversight roles

EMAC

Case Study I

Video Presentation on audit committees

EMAC

Responsibilities of Audit Committees

Monitor integrity of financial statements of entity Review the Entity’s internal control system and Risk

Management Systems Unless a separate Committee exists

Monitor and review of entity’s internal audit function Recommend to the board in relations to the

appointment of external auditor Approves remuneration Approves terms of engagement

Monitoring the effectiveness of the external auditor’s performance and their independence and objectivity

Develop and implement policy on the engagement of the external auditor to supply non-audit services

EMAC

Responsibilities of AC … It is not a replacement for the Board It is a committee of the board and

therefore subordinate to the Board It must be given written terms of

reference for audit committee. The Terms of Reference must be

reviewed annually The Board must review annually the

effectiveness of audit committee

Sako Mayrick Apt Financial Consultants

EMAC

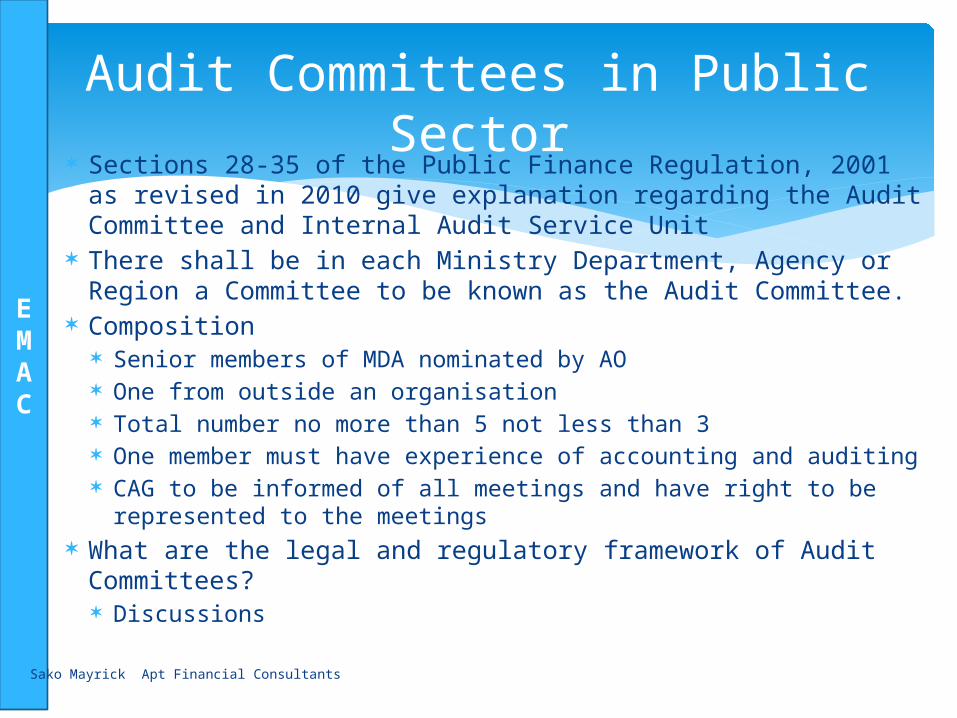

Audit Committees in Public Sector Sections 28-35 of the Public Finance Regulation, 2001 as

revised in 2010 give explanation regarding the Audit Committee and Internal Audit Service Unit

There shall be in each Ministry Department, Agency or Region a Committee to be known as the Audit Committee.

Composition Senior members of MDA nominated by AO One from outside an organisation Total number no more than 5 not less than 3 One member must have experience of accounting and auditing CAG to be informed of all meetings and have right to be

represented to the meetings What are the legal and regulatory framework of Audit

Committees? Discussions

EMAC

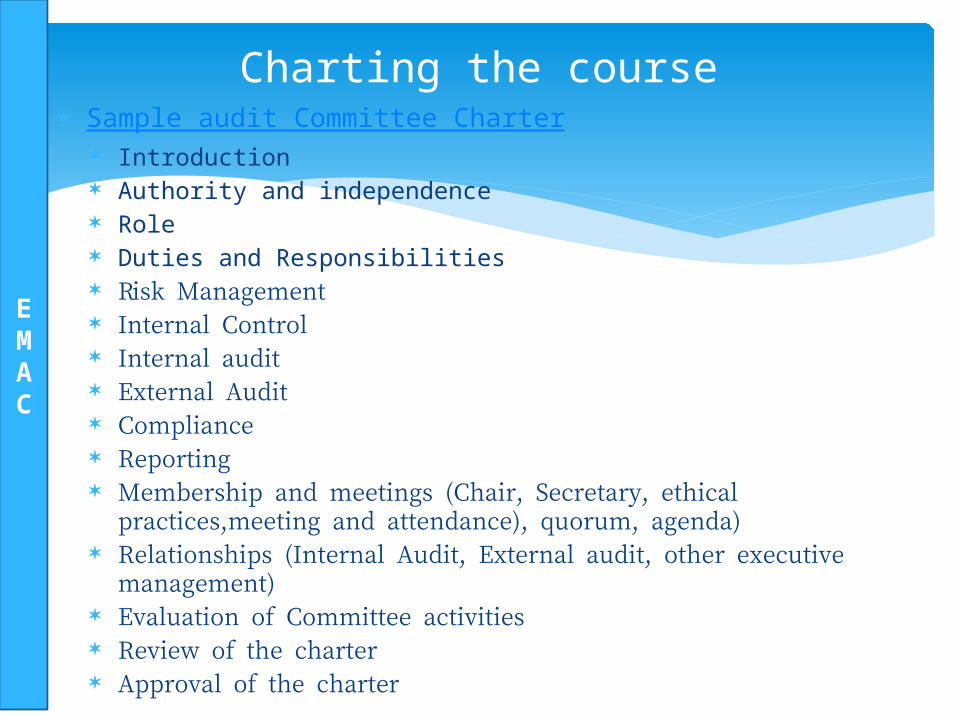

Charting the courseAn audit committee charter is a blueprint for its operation and should address:

Processes Procedures Responsibilities

EMAC

Charting the course Sample audit Committee Charter

Introduction Authority and independence Role Duties and Responsibilities Risk Management Internal Control Internal audit External Audit Compliance Reporting Membership and meetings (Chair, Secretary, ethical

practices,meeting and attendance), quorum, agenda) Relationships (Internal Audit, External audit, other executive

management) Evaluation of Committee activities Review of the charter Approval of the charter

EMAC

Case study 2

Roles and Responsibilities Audit Committees

a. What do you think to be the critical role of Audit Committee at Entity

b. Do you think there is a gap?c. What should be done?

EMAC

Part II

Audit Committee Issues

EMAC

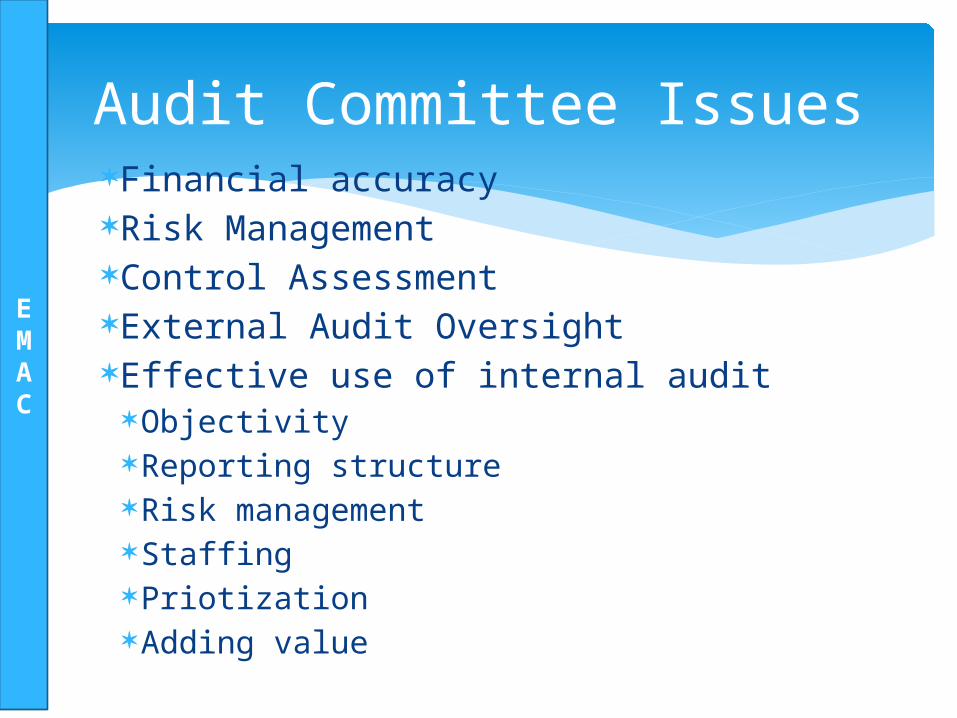

Audit Committee Issues Financial accuracy Risk Management Control Assessment External Audit Oversight Effective use of internal audit

Objectivity Reporting structure Risk management Staffing Priotization Adding value

EMAC

Best Practices in AC Should comprise of Independent non-

executive directors Chairman of the company should not be an

audit committee member But may attend the committee meeting as

invited guest At least one member of the AC should have

significant, recent and relevant financial experience at senior level

Members should have experience in corporate financial matters

EMAC

Best Practices in AC Should at least annually meet the external and internal auditors,

without management, to discuss issues arising from the audit Sufficient internal should be allowed between audit committee

meetings and main board meetings to allow any work arising from AC meeting to be carried out and reported to the board

Should have sufficient resources to undertake its duties New committee members should be given an induction program

Role of audit committee, ToR, Overview of company’s business Identifying the main business and financial dynamics and risks Meeting some company staff

Regular training should be given to all members of audit committee Understanding the financial reporting and financial statements Company law or entity memorandum Formal courses Internal Agency talks and seminars Briefing by external advisers

EMAC

Best Practices in AC AC should review financial reporting issues on

financial statements, interim reports and related statements Judgments Clarity Completeness of disclosure

AC should monitor the integrity of internal financial controls

AC should assess the scope and effectiveness of the systems established by management to identify, assess, manager and monitor Risks ( unless there is a separate committee on risks

EMAC

Best Practices for Audit Committee Annually the AC should consider

whether there is a need for internal audit function and make recommendation to the board

AC should review the complementing effect of internal and external audit

AC should approve the appointment or termination of appointment of CAE

AC should review and monitor internal audit activities

EMAC

Best Practices for AC AC should ensure that

CAE has direct access to the board chairman and audit committee and is accountable to audit committee

AC should review and assess annual internal audit work plan

AC should receive a report on the result of the internal auditors’ work on a periodic basis

Review and monitor management responsiveness to the Internal auditor findings and recommendations

Meet with the head of Internal audit at least once a year without the presence of management

Monitor and assess the role and effectiveness of internal audit function in overall company context of risk management.

EMAC

Best Practices of AC

AC should ensure independence and objectivity of the external auditor annually

At start of audit cycle, the AC should ensure that appropriate plans are in place for the audit

AC should review with the external auditors, the finding of their work

At end of audit work the AC should assess the effectiveness of external audit process

EMAC

Audit Committee Issue

The duties of care and loyalty, and the expectation that directors will act in good faith.

These are the primary source of Trustee liability.

EMAC

Audit Committee Issues(cont.)Board members who wish to become empowered guardians and builders of corporate value must:

Learn and follow best practices, avoid conflicts of interest, pay strict attention to board matters, drawing on appropriate expertise,

including their own. AC members should be “eyes on”

“hands off” The lines of authority for AC and management

should be clear and understood AC members must communicate openly with

management as appropriate

EMAC

Audit Committee Issues Financial accuracy Risk Management Control Assessment External Audit Oversight Effective use of internal audit

Objectivity Reporting structure Risk management Staffing Priotization Adding value

EMAC

Challenges of Audit Committees

Understanding the organization The few hours they meet is a challenge. So?

Never be afraid to ask questions even if stupid Insisting heads of functions to attend the meeting so as to

understand their roles, perspectives and control Responding to change

Corporates a changing so fast. So what to do? Ensure annual confirmation by directors and staff of compliance

of key regulations and policies Overseeing Risk and Control

Apply root course analysis Improving continuously Communicating with stakeholders Organization failures Financial literacy and changing accounting rules

EMAC

Current issues in AC Development of laws and regulations

Significant government and regulatory interferences

We need to be more balanced and refocus our attention back on the business

International Professional Practice Framework (IPPF)

Risk Management Effectiveness of Audit Committees Financial statements errors and fraud

investigations

EMAC

Part III

Financial Management

EMAC

Financial Reporting and Controls

The central role of Audit Committee is to oversee the integrity of entity’s financial statements and related controls

AC receives a great deal of financial information and it is the key to explain the company performance

The Audit committee must properly understand the operations of the company

EMAC

Financial Reporting Understand the basic financial Reports

Statement of financial performance Statement of financial position Statement of cash flows Statement of changes in equity

Understanding the organization Review the business discussions of last year Visit company operations, zones and facilities Meet the business unit leaders to grasp the operational details Meet the finance management, internal audit, and the external

auditors Review the analyst reports about the company Review the competitors financial statements and non financial

information Understand the major business transactions and changes during

the period Understanding the company’s regulators Meet the finance, taxation, and treasury personnel to understand

capital structure, tax structure and investment strategies

EMAC

Financial Reporting The other areas of financial reporting

Complex, difficult and risker areas Materiality Accounting policies Accounting estimates Significant changes during the reporting

period Related party transactions Interim financial statements Timing issues

EMAC

Case study 4

Issues in Financial Reporting and

Controls

EMAC

Internal Controls and Risk Assessment

Internal Controls It Is an essential tool to help mitigate risks to

an acceptable level The best framework is the COSO internal

Control Framework, defines Internal Control as Process that provides reasonable assurance

a company will be able to achieve its objectives for Effectives and efficiency operations Reliability of financial reporting Compliance with applicable laws and regulations

EMAC

Case study 5

COSO Internal Control Framework

EMAC

Role of AC on Internal Controls

Meet with individuals who are primarily responsible for internal control over financial reporting

Understanding and help set a tone at the top Discuss with management on controls in place to mitigate

key financial reporting risks including fraud risks Focus discussions on areas of greatest potential risk Understand management plans to assess the internal

control and what role internal audit and other related resources will play

Understand the external auditor’s scope and plan to test the controls

Meeting regularly with management, internal audit and external auditors to discuss significant deficiencies and material weakness and management’s action plan to respond

EMAC

Role of AC on Internal Controls

Areas of potential risk for internal controls Management override controls Outside services provider Information technology Restructuring of organsiation

EMAC

Risk Assessment

AC should oversee how management addresses risk for financial reporting

The risk assessment should be linked to company strategy and risk appetite

The AC should report to the Board on the results of committee’s review of risk management and internal control system

EMAC

Case Study 6

Risk Assessment Framework

EMAC

Role of AC in Risk Assessment The AC have responsibility of overseeing the risk

management process How management identifies events that could put the

company at risk and how it assess the likelhood and impact of identified risks

How management has tailored the process to meet the company specific needs

Whether the process of risk management is continuous If individuals are assigned primary responsibility for

risk management and has appropriate expertise, statute within the company and available time

Ensure that all key risks are subject to the Board-level oversight

Understand the internal auditor role in risk management and the extent of its audit plan covers the key risks

EMAC

Part IV

Operations Management

EMAC

Process Owners A process owner is a person who

has ultimate responsibility for the performance of the process in realizing its objectives measured by key process indicators and has the authority and ability to make necessary changes

The focus of audit committee operations management should be on period end process owners

EMAC

Anti-Fraud programs

Fraud prevention and detection makes good business sense and can provide cost savings to entity

The following are main anti-fraud programs Performing Fraud Risk Assessments Creating a control environment Designing antifraud control activities Sharing information and communication Monitoring activities

EMAC

Fraud Risk The CFE Report in 2010 identified

Assets misappropriation (where employees steal or misuse an organization's resource) are the most common forms of fraud

Corruption ranked the second ( where an employee gains a personal benefit by violating his or her duty to the company including, bribery, extortion, and conflicts of interests)

Financial Statement fraud ranked the last but has greater impact

Weakness in internal control can make a company more susceptible to fraud

EMAC

Fraud Risk There are many company’s fraud, but the

Audit Committee is more concerned with financial reporting fraud

Financial reporting fraud is a deliberate misrepresentation of a company financial position, stemming from intentional misstatements or omissions in the financial statements

Many company’s have admitted to fraudulent financial reporting

EMAC

Motivators for financial reporting fraud

To meet political expectations Personal gain, including maximizing bonuses

and compensation Conceal bad news, such as company’s

deteriorating financial conditions Increase company value Others

Audit querries Procurement failures

EMAC

Role of AC in Fraud Risk When the motivators for fraud are present audit

committee should Review the internal control Maintaining skepticism Overseeing the company strategy on financial

reporting Assess management integrity regularly Review and understand the results of complaints to

the whistle blower hotline Fully understanding the third party transactions and

significant non routine transactions Have management periodically report on the control

environment and fraud prevention program.

EMAC

Role of AC in Fraud Risk

Assessing the tone at the top

Overseeing company compliance programs

Review the whistleblower programs

EMAC

Whistleblower process owner

Whistleblower have become another source of information for Audit Committees

They are used to identify inappropriate behavior on part of company personnel involving issues such as sexual harassment or violation of anti-bribery programs

Many experts believe that providing mechanism to allow employees to report concerns anonymously is core to compliance programs

Best practices requires audit committees to establish procedures for the receipt, retention, and resolution of any complain regarding Accounting Internal accounting controls Auditing matters

But other organizations have put in place regulations to prohibit whistle blowing procedures that encourage anonymous reporting.

The organizations using whistleblowing believe that it will decrease the likelhood that managers who engage on wrong doing will be able to suppress staff concerns over the long term

EMAC

Role of AC in Whistleblowing The whistleblowing must be reported periodically to the audit committee.

It is important to get a summary of all complaints received at least annually.

Audit committees should determine how often they wish to receive information

EMAC

Case study 7

Fraud Risk ManagementFraud Risk Management

EMAC

Operations Management Management has deep insight into

company and its challenges, and therefore is best positioned to recommend what information the audit committee needs

The audit committee can add value for management

AC should work with management to add value by bringing an objective perspective on financial reporting decisions and counseling on how to handle difficult issues

EMAC

Operations Management Audit committee should have positive,

trusting relationship with management , they need to maintain their skepticism an be ready to question management on uncomfortable topic including Fraud risk Appropriateness of judgments

Management should expect rigorous questioning from audit committee

Failure of management to provide clear responses or overly defensive that should raise red flag for the committee

EMAC

Operations Management The degree of interactions and involvement

between the committee and management shifts with changes in The business environment Changes in company circumstances Capabilities of individuals in the finance function

When the company is running in a steady state, the committee continues to review information carefully and challenge management when necessary, but properly relies on management to resolve everyday issues

EMAC

Operations Management The knowledge and technical competence of the

finance team is vital to an audit committee faith in the financial reports it reviews

There should be discussions with the CFO on how he/she ensures the finance team is qualified

Assessment of performance of the finance personnel based on witnesses at committee meetings and responses to queries

Reviewing confidential feedback from internal and external auditors

The AC should also monitor succession plan for the CFO position

EMAC

Operations Management The AC should ensure that there are formal and

informal meetings with management for a strong relationship

Management’s participation should focus on engaging in meaningful dialogue with the committee, answering questions and providing additional insights

The following members could attend the meeting; the CFO, CA and controller, treasurer, head of PMU and chief information officer

AC should hold private sessions with internal audit head and external auditors

EMAC

Case Study 9

AC Operations Management

EMAC

Part 6

External and Internal Audit

EMAC

Pre-auditPhysical auditPost auditAudit follow-up

63

Basic Audit Activities

EMAC

Pre-Audit

Scope & DepthTeam Selection

Budget

DocumentsPreps

Team Meeting

Audit

Entry MeetingPhysical Insp..

Functional AreasFindings

Daily Meetings

Post-Audit

Company De-briefAudit Report

Wrap-up Activities

Follow-Up

Start Finish64

Corrective Action Follow Up

Basic Audit Activities

EMAC

AC and Internal Auditor Internal auditing is an independent,

objective assurance and consulting activity designed to add value and improve organization's operations. It helps an organization o accomplish it objectives by bringing systematic, disciplined approach to evaluate and improve effectiveness of risk management, control and governance process

They are day to day tools for audit committees

EMAC

AC and Internal Auditor The internal auditors deals with issues

that are fundamentally important to the survival of an organisation.

Unlike external auditors, they look beyond financial risks and statements to consider wider issues such as organisation’s reputation, growth, its impact on environment and the way it treats its employees.

They help organizations to succeed by combination of assurance and consulting

EMAC

Evaluating External Auditors Audit Committee should evaluate

external auditors based on its own experience and ask management and internal audit to provide their own assessment

EMAC

Evaluating External Auditors Areas of evaluation

Caliber of external audit firm (cases, reputation and resources)

Quality process ( approach, control, personnel and risk) Audit Team (competence, knowledge, resources, scope,

team member) Audit Scope (agreement, regulations, understanding, areas

covered) Audit Fees (comparison with other, variation between actual

and estimated fee, service) Audit Communication (inform AC on risk, governance,

controls, access with AC, feedback of service) Audit governance and independence ( does the AC or

management control relationship with external auditors?, communication of internal control weaknesses

EMAC

Evaluating of internal auditors

The following are main areas for evaluation Understanding Charter and Structure Skills and experience Communication Performance Planning Skills and experience Work program Overall performance

EMAC

Assessment of audit committee

In addition to reviewing its ToR, the AC members should review the effectiveness of audit committee annually

This is done using AC self Assessment Areas includes

Creating an effective audit committee Running an effective Audit Committee Professional development Overseeing financial reporting Overseeing risk management and internal control Overseeing external audit Overseeing internal audit

EMAC

WHAT MAKES AUDIT COMMITTEE EFFECTIVE

Member experience/educational qualifications Inquiry Diligence Decision making Integrity Independence Leadership Communication Ability to work with othersNo two audit committees are equalThe only way to know and factor this is at annual evaluation

EMAC

Qualities of an effective audit committee

Strong interpersonal and communication skills Disciplined and focused Conversant with the current issues of the industry In-Depth knowledge of Strategic Plans Technical Financial Expertise Industry regulation knowledge Understand Audit Review findings Monitor quality of internal audit Help build right team Meet regularly with internal auditors Resource allocation

EMAC

Qualities of an effectives committee member

Has appropriate and requisite experience Has appropriate and requisite technical knowledge

about accounting, auditing, tax, internal control and other necessary subject areas

Satisfies requisite independence requirements Is interested and committed to the company Is knowledgeable about the company, and its industry Has a willingness to learn about matters relating to the

audit committee function Has a thorough understanding of his or her legal

responsibilities Demonstrates leadership and tone at the top Has sufficient time availability

EMAC

Qualities of an effectives committee member Has sufficient time availability

Has integrity; doing the right thin attitude After due consideration is comfortable (i.e.,

satisfied) that the committee has complied with the laws, regulations, rules , and charter provisions that govern and related to audit committee activities

Reviews and is comfortable of financial statements related documents, securities filings and corporate communications to the extent required by laws, regulations, rules, and audit committee Charter provisions

Reviews and is comfortable with the accuracy of all documents and statements signed by or attributed to the committee members, or the committee

EMAC

Qualities of an effectives committee member Is comfortable with other audit committee

members, CEO, CFO, inside auditor, outside auditor, board, counsel and others

What is more: individual self-confidence, humility and conviction

Meetings are conducted in a collaborative, participatory, interactive and organised manner

The services of the outside auditor, and the outside auditor selection process are evaluated annually, and more often as necessary

There is an appropriate and effective anonymous whistle blower and complaint, inquiry and investigation processes.

EMAC

Other attributes of Audit Committee

The ease and demeanor of communications between committee members are appropriate

The ease and demeanor of communication with other people outside of the committee are appropriate, including the CEO, CFO, Controller, outside auditor, inside auditor, board, legal counsel and others

The committee has appropriate accessibility to information and resources paid for by the company

The committee has appropriate accessibility to continuing education about core areas, new developments, and hot topics, paid for by the company

The committee has a accessibility to independent legal counsel and consultants, paid for by the company

EMAC

Other attributes of Audit Committee

There is an audit committee charter. There are prudent process for the documentation

of committee activities The activities and performance of audit

committee are evaluated annually; or more often as necessary

There is prudent procedures for the timing, calendaring, and organization of committee activities

There is effective meeting agenda and dissemination process

EMAC

Annual Assessment Audit Committee Chairperson should continuously

monitor the effectiveness of the Audit Committee Areas of assessment includes

Audit Committee Charter Audit Committee composition Audit Committee independence Meetings and Attendance Risk Management Assignments Code of Conduct – Supplier relationship management Reporting of fraud and illegal Acts – Whistleblower function Financial Expert Oversight Oversight of External Auditor Oversight of internal auditor Oversight of self assessment

EMAC

Sample evaluation forms Evaluation of external auditors Evaluation of internal audit Audit committee self Assessment Checklist for oversight of internal auditors Checklist for oversight of external auditors

EMAC

Case Study 10

Assessment of Audit Committee and useful

template(see a separate guide)

EMAC

Conclusion

Audit Committee

![Comprehensive CSS MOrley Audit Report_25MAR2010[1]](https://img.pdfslide.us/doc/110x75/577cc56f1a28aba7119c60f2/comprehensive-css-morley-audit-report25mar20101.jpg)