Embed Size (px)

Citation preview

Business Future: AMLCD and AMOLED TV

An update to my SID Jubilee (2012) view on the potential for OLED TV substitution of LCD TV

—David Barnes, BizWitz LLC, Feb 2014

2012: it was “time for more pixels to constrain AMOLED”This chart summarizes by view shared three years ago.Some listeners were surprised by the idea that AMLCD could and would move into most of the TV market spaces targeted by OLED marketers.That is what happened and we even saw some panel makers stop pretending OLED TV will be competitive any time soon.Technical and financial trends remained active drivers of TV improvements based on LCD.Producers and retailers gave consumers more for less and trained us all to wait for sales.What’s next?

20 Jan 2015 Business Future 2

Potential TV Space Served: the next three years*

* As presented at the Jubilee in Sep ’12except 8K was labeled UHD and 4K was labeled QHD

40”59”

60”79”

80”99”

8K

4K

HD

LCD2016

LCD2014

LCD2013

LCD2013

OLED2013

LCD2012

Size

Format

100”109”

LCD2016

LCD2012

LCD2014

LCD2014

OLED2016

2015: it is “time for more of the same”

n Updated quantitative analysis will be presented at the SID Biz Con. Some of my recent charts are placed in an appendix for your consideration.

n Here, I will present key qualitative thoughts on the business future of FPD in general and of flat panel TV in particular through five maxims.n Pixels are freen Materials mattern Policy drives economyn Cannibals should eat outn Value evaporates

20 Jan 2015 Business Future 3

Past

n Improvements in photolithography and process yield enabled greater spatial resolution for TFT backplanes.

n Consumers appreciated higher-ppipanels or larger panels with high-ppidespite often clumsy marketing.

n AMLCD makers pushed CRT and PDP from the TV field.

n Technologies perfected to serve the market for mobile applications were adapted to serve the LCD TV market.

n Rivalries hindered development of LCD alternatives without roadmaps.

Future

20 Jan 2015 Business Future 4

Pixels are free… ppi will increase because it can.

n Improvements in photolithography and process yield will continue to enable 8K (FUHD?) TFT backplanes.

n Consumers will appreciate improving visual value from 4K UHD TV despite marketing and streaming confusion.

n AMLCD makers will push OLED TV into niche markets for several years.

n Technologies will diverge more between small and large because of personal versus social viewing needs.

n Rivalries will slow AMOLED process evolution, especially for OLED TV.

Past

n Purchasing materials accounts for 2/3 of panel makers’ manufacturing cost.

n Changing post-fab material was a simple and inexpensive way to reduce cost or to increase product value.

n Suppliers offered improved materials to sustain rents and impede supplier substitution or rearward integration.

n Reducing purchased materials with AMOLED processes was a key driver for panel makers seeking hegemony.

Future

20 Jan 2015 Business Future 5

Materials matter… because they drive panel costs and values.

n Purchasing materials will remain the main AMLCD cost/value driver.

n Selecting materials will remain a key means of product differentiation such as recent QD or glass LGP offerings.

n Adding QD or glass LGP to LCD BLU will create new value propositions for suppliers and consumers, not makers.

n Realizing AMOLED hegemony will remain difficult for any single maker, so commodity may evolve instead.

Past

n US corporations declined the AMLCD fab investment opportunity.

n Japan guided development of LCD infrastructure and led the market to economic exhaustion circa 1996.

n Korea encouraged chaebol entry and export expansion until LCD economic exhaustion circa 2008.

n Taiwan over-stimulated investment until industry exhaustion circa 2006.

n China restructured AMLCD circa 2006 and increased stimulus through policies to the present.

Future

20 Jan 2015 Business Future 6

Policy drives economy… so China will over-stimulate as others did.

n US and EU corporations will still make better returns from materials.

n Japanese tool and material suppliers will retain premium positions and profit more than panel makers did.

n Korean panel makers will restructure or create value through some vertical integration and brand differentiation.

n Taiwanese panel makers will move into former Japanese niche markets.

n China will drive panel prices and economic losses along historical trend lines for the rest of this decade.

Past

n Attempts to substitute LTPS for a-Si and thereby create new hegemony made sense for leaders with few alternatives and few assets to impair.

n Rivalries impeded LTPS development and its capacity peaked at 5% share.

n Innovations such as iPhone absorbed under-used LTPS capacity.

n Conversions from a-Si to p-Si or toa-MO were constrained by roadmaps and opportunity costs.

n Promotions of AMOLED undercut the value of existing AMLCD assets.

Future

20 Jan 2015 Business Future 7

Cannibals should eat out… because eating at home is dangerous.

n Attempts to develop novel capabilities for large LTPS or a-MO backplanes will slow and informal cooperation will lead to commoditization.

n Rivalries impede AMOLED backplane and frontplane development, still.

n Innovations such as Galaxy will drive interest in mobile LTPS and a-MO.

n Conversions will infrequent and most AMOLED growth will depend on green-field investments.

n Fight Club dynamics persist as makers try not to hurt themselves…too much.

Past

n Panel makers cycle from experiment to discouragement to excitement to disappointment and back around.

n Leaders capture value during the initial stage of market excitement.

n Followers compete for scraps of value and fight to remain relevant.

n Periods of profit lead to periods of reinvestment and subsequent loss.

n Price wars fail to chase any significant competitor from the market and panel prices fall faster than costs.

Future

20 Jan 2015 Business Future 8

Value evaporates… time and pressure makes it disappear.

n Panel makers will commoditize QD, UHD, SPR, lightfield and AMOLED innovations to reach consumer prices.

n Leaders have already captured 4K value and must move on to 8K.

n Followers will make a lot of money for suppliers as they buy market share.

n Surges of LTPS capacity will lead to value declines in mobile, 2015–2016.

n Price declines in mobile will lead makers to allocate more capacity for TV and to discount large 4K panels.

In summary, historical forces remain in play and OLED TV can only “win” as a commodity.n Hopes for a Korean hegemony in AMOLED has been disappointed.n Uncertainties that I presented in 2012 have decreased.

n Samsung has pivoted away from OLED TV and now sells mobile OLED to other product assemblers. I anticipate more restructuring.

n LG remains committed in a limited way but has placed its OLED operations into a division for possible separation or disposition.

n Scenarios for continued value destruction by AMLCD panel makers have become more likely outcomes.n Chinese expansion of Gen 7 to 10 capacity will grow at historical

AMLCD rates of 40% or more over the mid term.n Chinese policy supports domestic supply of key tools and materials.n Chinese export policy supports price reductions for poorer markets.

n Suppliers with proprietary positions (e.g. Corning) will still prosper, but operating margins may fall commensurate with market maturation.

20 Jan 2015 Business Future 9

But hey, what about all those great bargains?n I remain bullish about consumers’ ability to get more for

less.n 100” LCD TV with REC. 2020 color at 88 ppi here we come!n In the meantime, BizWitz can help you with…

20 Jan 2015 Business Future 10

Growth

§ Market entry§ Business structure§ Phase gates, R&D

Technologies

§ Market sensing§ Market & IP value§ Consortia synergy

Alliances

§ M&A candidates§ Partnerships, JVs§ Integration plans

Plans

§ Strategic audits § Investor insights§ Business valuation

Materials

§ Pricing policies§ Market strategies§ Licenses, royalties

Performance

§ Price position§ Cost reduction§ Portfolio balance

CapEx

§ Factory plans§ Tool selections§ Plant conversions

Sourcing

§ Make/buy§ Value chains§ Supplier selection

Appendix—Where have we been?n 1960–1984: US companies develop FPD technology but become

distracted by silicon and discouraged by capex.n 1984–1994: Japan’s MITI coordinates LCD industrial development that

remains the basis of production materials and tools today.n 1994–2014: Korean chaebol apply political, capital and feudal resources

to FPD and dominate the market and destroy industrial coordination.n 1998–2008: Taiwanese trade capacity for technology from Japan and

add LCD to their PC supply chain with excessive ministerial stimulus.n 2004–2014: China fails (mainly) to leverage Japanese FPD technology

and restructures its industry around Korean technology.n 2008–2014: Taiwanese policy changes and macroeconomics halts FPD

reinvestment and forces restructure.

20 Jan 2015 Business Future 11

Capacity development by substrate octaves shows concentration in the Gen 7–8 regime

20 Jan 2015 Business Future 12

0

50

100

150

200

250

2000 2005 2010 2015

8–16 m²4–8 m²2–4 m²1–2 m²0–1 m²

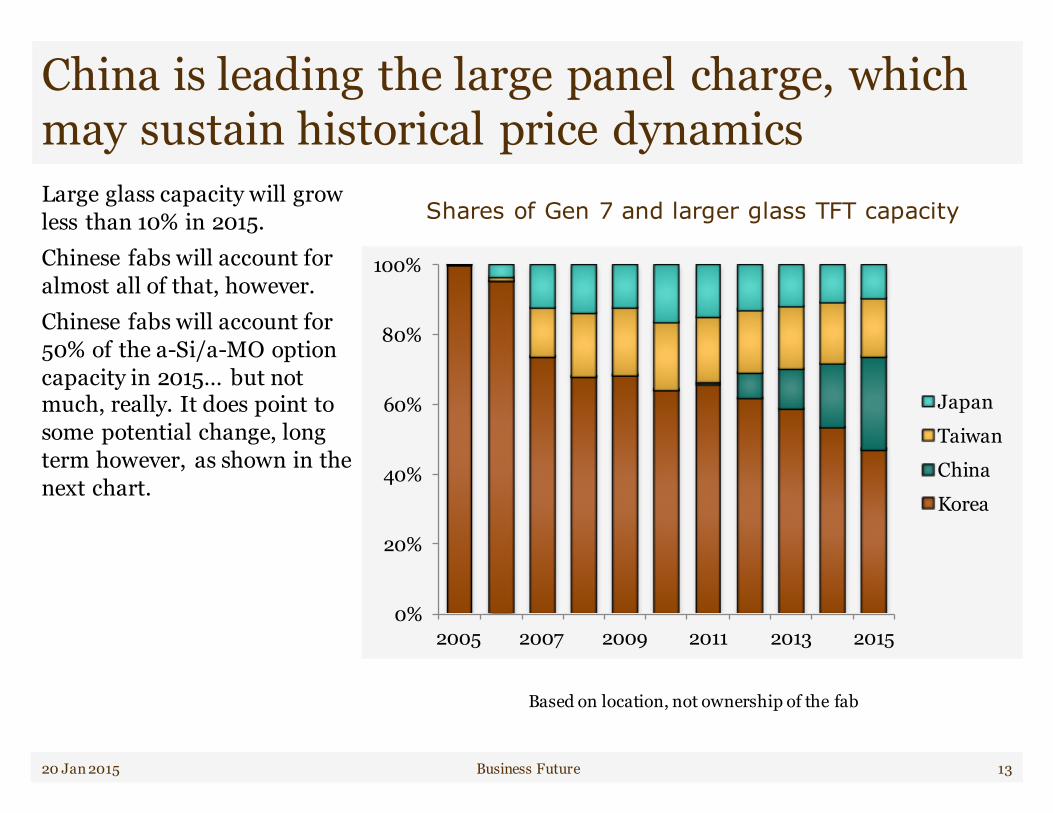

China is leading the large panel charge, which may sustain historical price dynamicsLarge glass capacity will grow less than 10% in 2015.Chinese fabs will account for almost all of that, however.Chinese fabs will account for 50% of the a-Si/a-MO option capacity in 2015… but not much, really. It does point to some potential change, long term however, as shown in the next chart.

20 Jan 2015 Business Future 13

Shares of Gen 7 and larger glass TFT capacity

Based on location, not ownership of the fab

0%

20%

40%

60%

80%

100%

2005 2007 2009 2011 2013 2015

JapanTaiwanChinaKorea

We will see the effect of options to increase a-MO capacity in new fabs, later this decade.High-mobility TFT capacity for TV-class production is just now appearing.Conventional a-Si capacity may retain an 80% share for the remainder of this decade.Thus, the potential market for OLED TV will be constrained by capacity, despite Chinese aspirations.I am not sure how much real capacity will go into a-MO over the mid-term… it can be thought of as a real option for some Chinese producers.

20 Jan 2015 Business Future 14

Gen-7 and larger TFT Glass Capacity by Technology

Based on expressed options for a mix of a-Si and a-MO in new fabs

0%

20%

40%

60%

80%

100%

2005 2007 2009 2011 2013 2015

p-Si (LTPS)a-MOa-Si/a-MOa-Si

Cumulative view of panel size allocation and average area price distribution in Q2’14

20 Jan 2015 Business Future 15

$0

$700

$1,400

$2,100

$2,800

$3,500

$4,200

0

25

50

75

100

125

150

Sq meters millions

USD millions

Price (USD on right)

Cumulative as diagonal inches increase

The attractive market segments (Phone and TV) see falling prices but not the PC segmentThe size categories of 0–10”, 50–60” and 60–70” saw 13% annual price decline while PC sized panel prices rose 2% per annum.This recovery in PC panel pricing indicates two things.Panel makers reallocated capacity to other applications and resisted buying business.Panel makers pushed more expensive TV-class panels into the monitor market as growth slowed for tablets and such.I therefore expect panel makers to target industrial display applications such as automotive.

20 Jan 2015 Business Future 16

Panel Area Price Development (USD/m²)

Source: BizWitz analysis

$500

$600

$700

$800

$900

$1,000

2011 2012 2013 2014

10"–30"

Phone+TV

All Sizes

Appendix—Where are we going? n Panel makers are pivoting away from the mobile market and are

allocating more capacity to TV applications as 4K (now) and 8K (soon) offer temporary price premiums.

n Chinese panel makers and the brands they support are preparing to enter developed markets with high-spec, low-price products.n Brands like Apple will see unit share decline as they preserve margin.n New brands and value propositions will appear experimental but will

be supported by internet interests.n Balkanization of the internet will foster local/regional champions.

n Brazil no longer presents a threat to China, so we may have seen the last national wave of investment in AMLCD (though it is not over, yet).

n The two known unknowns:n Will panel makers learn how to integrate and differentiate?n Will near-eye display become important, and when?

20 Jan 2015 Business Future 17