Embed Size (px)

Citation preview

Michael GilmartinManager, Solution ConsultingBlackLine Systems

Gina DeBernardiExecutive Director – Client ServicesMGM Resorts International

Automating Account Reconciliation to Mitigate Compliance Risk

© 2014 Proformative

2

Are Your Reconciliations in Good Shape?

• Are all reconciliations completed in a timely manner?

• Do you have old reconciling items?

• Do you have any material write-offs?

• Can you easily provide documentation?

• Do you have standard procedures?

• Are there manual steps in the process that could be automated?

• Do you have to reconcile multiple standards?

© 2014 Proformative

Agenda

• Current Regulatory Environment/Impact on Finance Organization

• Importance of Account Recs/What to look for in an Automated Solution

• Client Case Study – TBD

• Q&A

3

© 2014 Proformative

CURRENT REGULATORY SITUATION

• Accounting standard setters, including the European Financial Reporting Advisory Group (EFRAG), the FASB in the United States and the IASB (its international counterpart), are enforcing multiple standards that companies must adhere to

• Accounting rule makers also are mandating international alignment on reporting rules and requirements

• Restatement of corporate earnings worldwide more common than ever due to new and changing rules, tax credits, etc.

• Convergence of standards and guidelines causing confusion among CFOs/CEOs about what is required and how to comply

4

© 2014 Proformative

ACCOUNTING-SPECIFIC CHANGES

• Several projects underway to align U.S. and international standards on revenue recognition, leasing, financial instruments and insurance

• SEC setting new policies for how U.S. companies will adopt International Financial Reporting Standards (IFRS)

• COSO Framework revamped in 2013, adding more stringent mandates on internal controls for large corporations

• Regulators in the United States and Europe are considering a rule requiring public companies to switch their auditing firms every several years

5

© 2014 Proformative

WHAT DOES ALL THIS MEAN FOR THE CORPORATE FINANCE DEPT?

• CEOs/CFOs have to be more meticulous than ever in enforcing company reporting policies and procedures; more training will be required

• Number of reconciliations, tasks, journals, etc., is multiplied for each set of books maintained

• Maintaining multiple sets of accounting standards, including IFRS, GAAP, and Statutory accounts, will create significant resource constraints and challenges for companies when closing the books each month

• By leveraging technology, a company can automate its reconciliation process and link accounts across different standards to minimize the amount of manual labor required for each financial close

• Just as account reconciliation is a key control in producing accurate financial statements, proper IFRS reconciliation will be key, as well – a process must be put in place to ensure this is done effectively

6

© 2014 Proformative

NEW RULES CAUSING CONFUSION, WEAKNESSES IN THE CLOSE PROCESS

• Lack of visibility

• Little/no standardization of reconciliations

• Too many manual processes

• Unclear ownership of tasks

• Too much room for human error

7

© 2014 Proformative

© 2014 Proformative

Common Close

© 2014 Proformative

Agenda

• Current Regulatory Environment/Impact on Finance Organization

• Importance of Account Recs/What to look for in an Automated Solution

• Client Case Study – TBD

• Q&A

10

© 2014 Proformative

11

© 2014 Proformative

EXISTING METHODS FOR HANDLING ACCOUNT RECONCILIATIONS

• Doing manually

• Excel/spreadsheets

• Internally developed tool/system

• Automated technology/software tool

• Others?

12

© 2014 Proformative

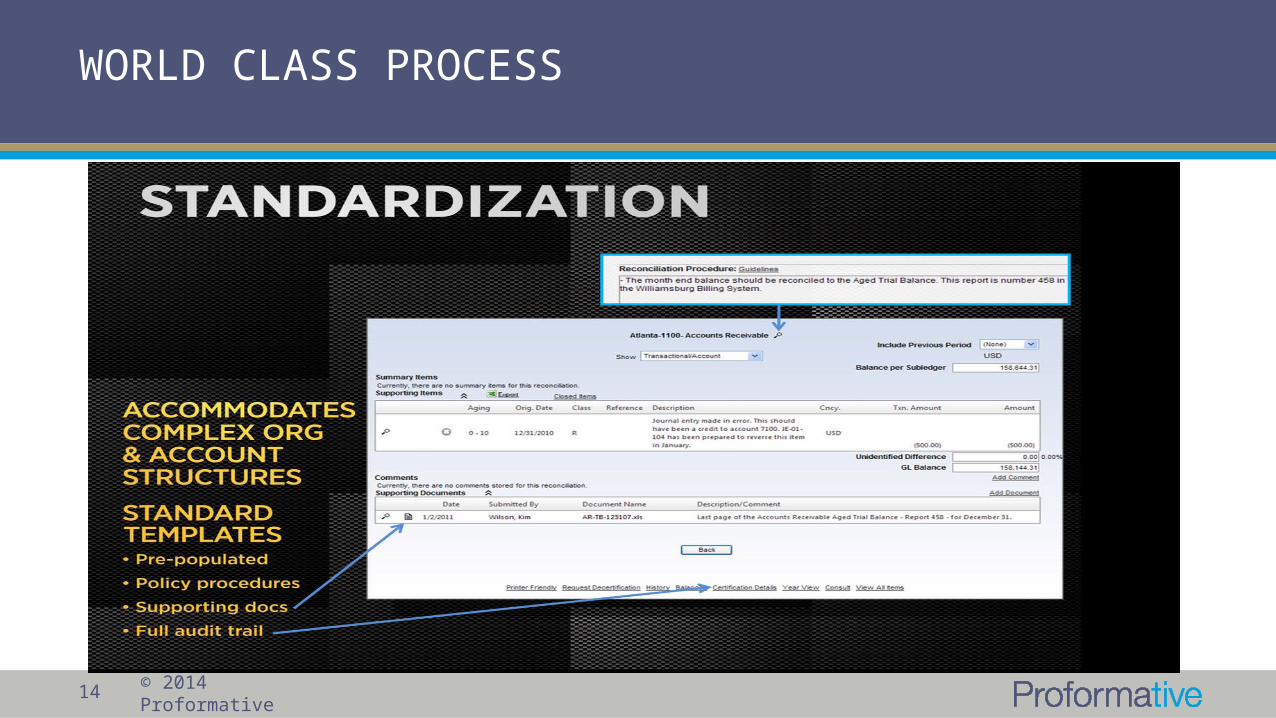

WORLD-CLASS PROCESS

• POLICIES AND PROCEDURES

• STANDARDIZATION

• CONTROL

• TRAINING

• AVAILABILITY

• ?

13

© 2014 Proformative

14

WORLD CLASS PROCESS

© 2014 Proformative

15

WORLD CLASS PROCESS

© 2014 Proformative

16

Data Consistency & Integrity

Automated Interfacing between Data Sources and Software Functionality, Modules

© 2014 Proformative

SPECIFIC FUNCTIONALITY TO LOOK FOR SURROUNDING ACCOUNT RECS

• System that can be used for entire balance sheet: pre-paids, accruals, bank, subledger, debt, equity, etc.

• Auto-certification of low risk reconciliations

• Templates-based process for standardization and quality

• Supporting documents – can be saved/accessed from within the system

• Approval workflow – multiple levels with flexible scheduling

• Automated e-mail alerts for proactive notification/monitoring

• Reporting for real-time status updates

• Centralized, global access – anywhere, anytime

• Easy integration with existing ERP, GL systems

17

© 2014 Proformative

SHOULD WE MAINTAIN IN-HOUSE OR HOST “IN THE CLOUD”?

BENEFITS OF GOING WITH A CLOUD/SaaS SERVICE PROVIDER:

• No hardware or software to purchase, install, or maintain

• Lower upfront costs/minimal capital outlay at onset

• Pay as you go, only for the users who need access

• Reallocation of internal IT resources to more strategic projects

• Quick implementation, even for multiple locations

• When using world-class hosting partner (such as Verizon/Terremark):

• Higher level of uptime guaranteed

• Hot disaster recovery built-in

• Security is No. 1 priority

• 24/7 access to superior customer service/support team

• Anytime access from anywhere with an Internet connection

18

© 2014 Proformative

OTHER CONSIDERATIONS/QUESTIONS TO ASK

• Who is the hosting provider?

• What specific security, back-up processes and technologies do they have in place?

• Will the solution (whether in-house or hosted) integrate easily with my existing ERP, GL systems?

• Does the solution offer an SAP Connector?

• What security standards reports has the provider AND hosting partner completed to ensure the security of my data?

• Do they have an SSAE 16 and/or ISAE 3402 under their belt?

19

© 2014 Proformative

IMPORTANCE OF SSAE 16/ISAE 3402

• Internationally recognized auditing standards developed by the AICPA and IAASB on control effectiveness for service organizations

• The AICPA’s SSAE 16 effectively replaces the prior Statement on Auditing Standards No. 70 (SAS 70) as the authoritative guideline

• Completion of the ISAE 3402 audit shows that the company also has the proper controls and processes in place to meet international audit and accounting reporting standards as set forth by the IAASB

• Important that both the application and data center/hosting company have gone through successful SSAE 16/ISAE 3402 audits

20

“Adherence to guidelines set forth by worldwide regulatory organizations such as the AICPA and IAASB is becoming increasingly important as more companies move to SaaS where sensitive corporate data is hostedby third parties.” Chris Kradjan, partner, Moss Adams LLP

© 2014 Proformative

Agenda

• Current Regulatory Environment/Impact on Finance Organization

• Importance of Account Recs/What to look for in an Automated Solution

• Client Case Study – TBD

• Q&A

21

© 2014 Proformative

Agenda

Client Case Study – MGM Resorts International• Company Overview:• Expansion and Growth

• Finance Consolidation

• Compliance Weaknesses – pre-automation

• Compliance – post Blackline implementation

22

© 2014 Proformative

Company Overview – Expansion and Growth

Expansion and Growth:• Mandalay Resort Group Merger – 2004

• CityCenter – 2009

• Rapid expansion expected 2014-2016

Resulting in:• 234 company numbers

• 10,882 account reconciliations

• 24,000 average journal entries per month

• 3,000 monthly control tasks

• 15 million matched transactions daily

23

© 2014 Proformative

Company Overview – Consolidation

24

12/31/03 12/31/04 12/31/05 12/31/06 12/31/07 12/31/08 12/31/09 12/31/10

Accounts Payable

Payroll

Non-gaming Acct. and Audit

General Accounting

Accounts Receivable

Casino Acct. and Audit

Financial Planning and Analysis

Systems "Infrastructure"

MANDALAY MERGER TI SALECITYCENTER OPEN

Implement LV Strip BRMandalay resorts

Detroit Corp Vendor portal

"Hub" structure Consolidate Standardize/ Kronos rollout

DesignStandardizeF&B Audits

Implement LV Strip

Design Implement LV Strip

Chart standardization

Design

"Hub" structure

Design

MandalayInfinium

Fixed assets conversion

FDR developmentCognos Reporting

Cognos Ent. Planning Cognos 8 and Cubes

TO BE DETERMINED

© 2014 Proformative

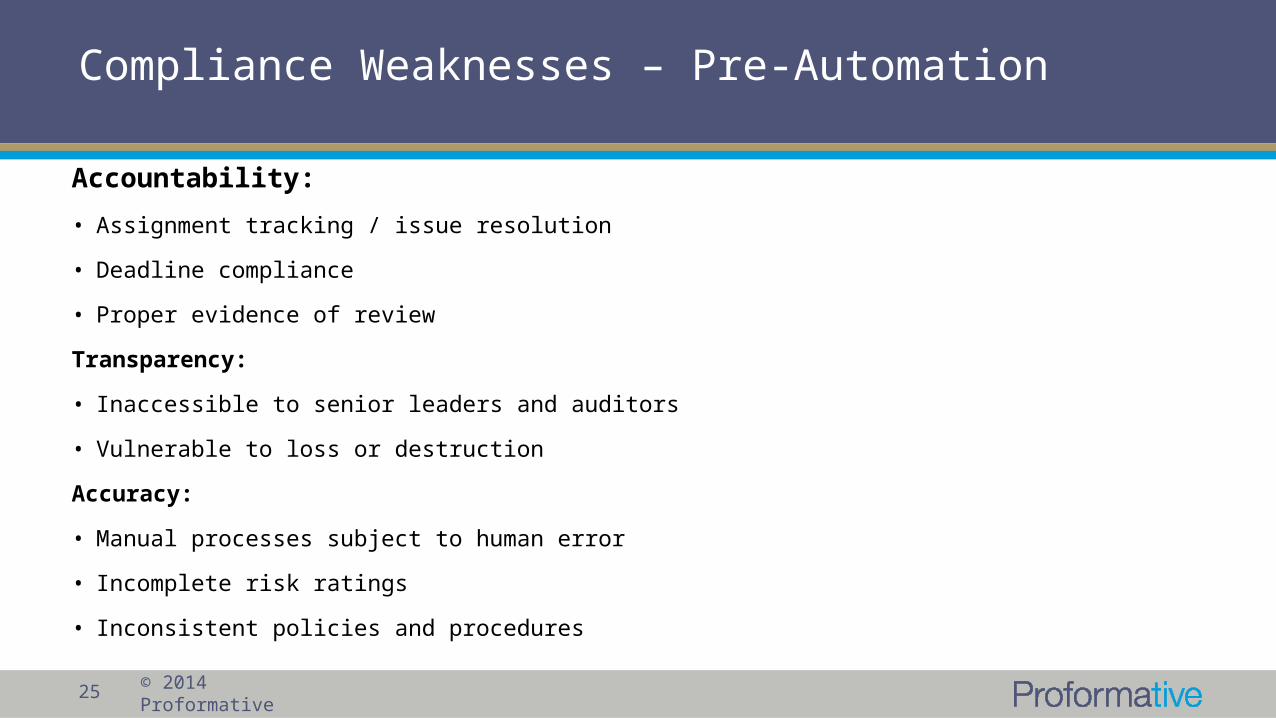

Compliance Weaknesses – Pre-Automation

Accountability:

• Assignment tracking / issue resolution

• Deadline compliance

• Proper evidence of review

Transparency:

• Inaccessible to senior leaders and auditors

• Vulnerable to loss or destruction

Accuracy:

• Manual processes subject to human error

• Incomplete risk ratings

• Inconsistent policies and procedures

25

© 2014 Proformative

Compliance – Post Blackline Implementation

Reconciliation Metrics:

• 99% deadline compliance rate on average

• 98% required adjustments corrected within policy

• 100% reviewed in accordance with policy

Transparency increased:

• Accessible to senior leaders and internal/ external auditors

• Electronic signature capture

Accuracy increased:

• Consistent policies and procedures

• Risk ratings drive frequency and effort

• Templates populate with automated data

26

© 2014 Proformative

27

Q&A

Automating Account Reconciliation to Mitigate Compliance Risk

Thank You For Attending

Michael GilmartinBlackLine [email protected]