Embed Size (px)

Citation preview

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc.

Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in

any form or manner without the prior written permission of Experian. Experian Public.

Attracting and retaining commercial and small-business clients with powerful segmentation strategies

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 2

Joanne Pollitt CEB TowerGroup

Mike Horrocks Experian

Introducing:

@ExperianVision | #vision2015

Follow us on Twitter:

3 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

What is happening in your markets?

What is at risk?

What is the segment within the segment?

What are the commercial borrowers wanting?

Case study

Call to action

Agenda

4 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Discover

Learn

Hear

React

Solidify

Commercial clients are unique So why do we treat them the same?

5 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Capturing the growth opportunity requires deep understanding of target segments, channel choices and products / services

1

3 2

Target segments What are the needs of our market’s

segments?

For which segment(s) should we build a value proposition to attract new businesses and those willing to switch

Product / service portfolio What are the products and

services that resonate with our target segments?

What is the most efficient go-to-market model?

Channel choices

What channels do our target segments prefer / primarily use?

What sales/ service delivery model best aligns to their preferences and needs

6 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

There may be more than one target

Competitive rates

Access to credit

Knowledgeable banker

Credit seekers

Values my business

Passive customers

Common and distinct needs

Problem resolution

Financially stable

Trust

Delivers solutions

Common needs

Common needs vs. distinct needs Credit seekers vs. passive customers

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 7

What is happening

in your markets?

8 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

What is happening in your markets? Continued pressure for growth and cost controls

Expectations of higher revenue growth and cost pressure Percentage of FS Executives, Q1 2012 to Q3 2014

n = 3,825.

Source: CEB Q1 2012–Q3 2014 Business Barometer Survey.

50%

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

70%

90%

72% Revenue growth

64% Cost pressure

9 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

What is happening in your markets? Continued pressure for growth and cost controls

n = 374.

Source: CEB Q3 2014 Business Barometer Survey.

Note: Totals do not equal 100% due to rounding

© 2014 CEB. All rights reserved. RBLC1072214SYN

17% 14%

10% 23%

72% 64%

0%

25%

50%

75%

100%

Revenue growth Cost pressure

Higher

No change

Lower

Expectations of revenue growth and cost pressure Percentage of FS Executives, Q1 2012 to Q3 2014

10 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Growth driven by sales to current customers

0%

Q4 2013 Q1 2014 Q2 2014 Q3 2014

50%

100%

n = 195.

Source: CEB Q4 2013–Q3 2014 Business Barometer Survey.

Expectations of sales to existing customers Percentage of FS Executives, Q1 2012 to Q3 2014

70% Higher

19%

No change

11%

Lower

11 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

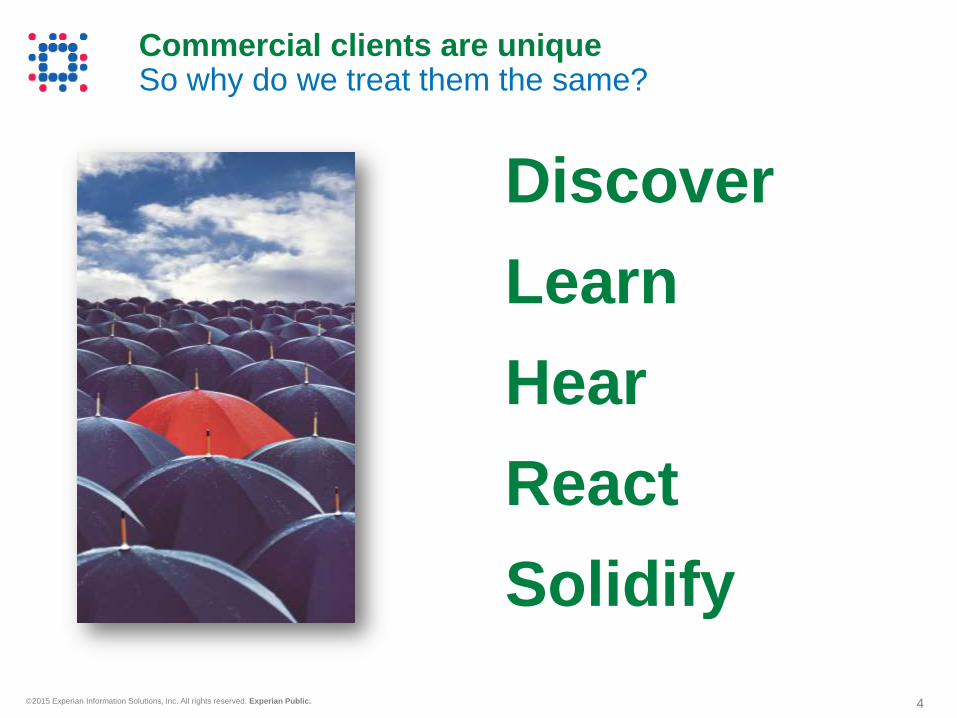

Decreased revenue growth driven by lower sales to new customers

0%

Q4 2013 Q1 2014 Q2 2014 Q3 2014

50%

100%

n = 195.

Source: CEB Q4 2013–Q3 2014 Business Barometer Survey.

Expectations of sales to new customers Percentage of FS Executives, Q1 2012 to Q3 2014

75% Higher

15%

Lower

9%

No change

12 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

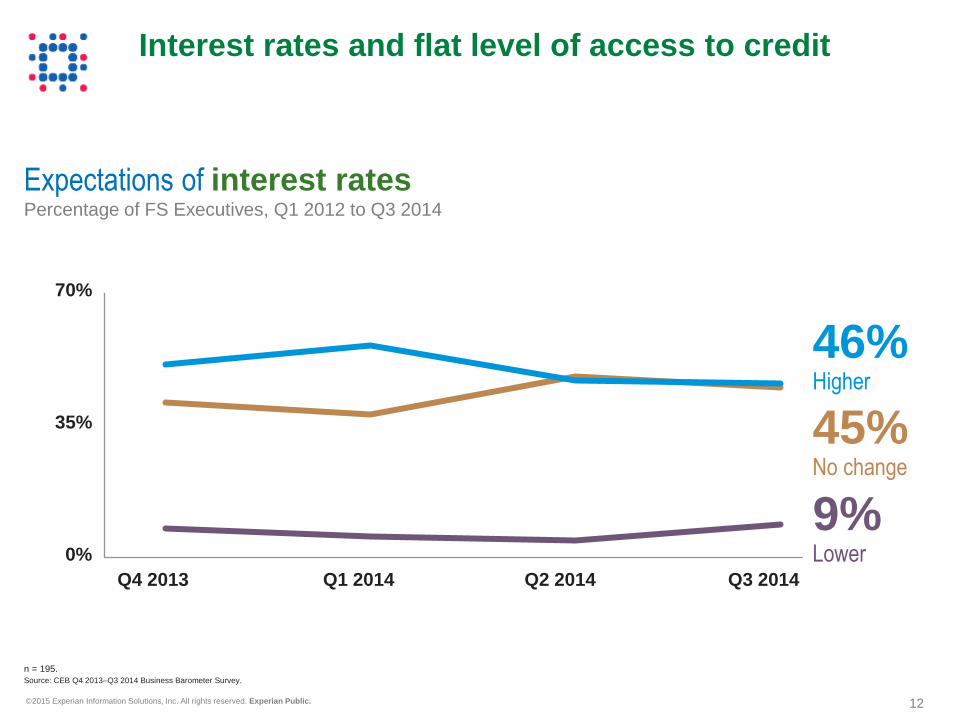

Interest rates and flat level of access to credit

0%

Q4 2013 Q1 2014 Q2 2014 Q3 2014

35%

70%

n = 195.

Source: CEB Q4 2013–Q3 2014 Business Barometer Survey.

Expectations of interest rates Percentage of FS Executives, Q1 2012 to Q3 2014

46% Higher

45%

No change

9%

Lower

13 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

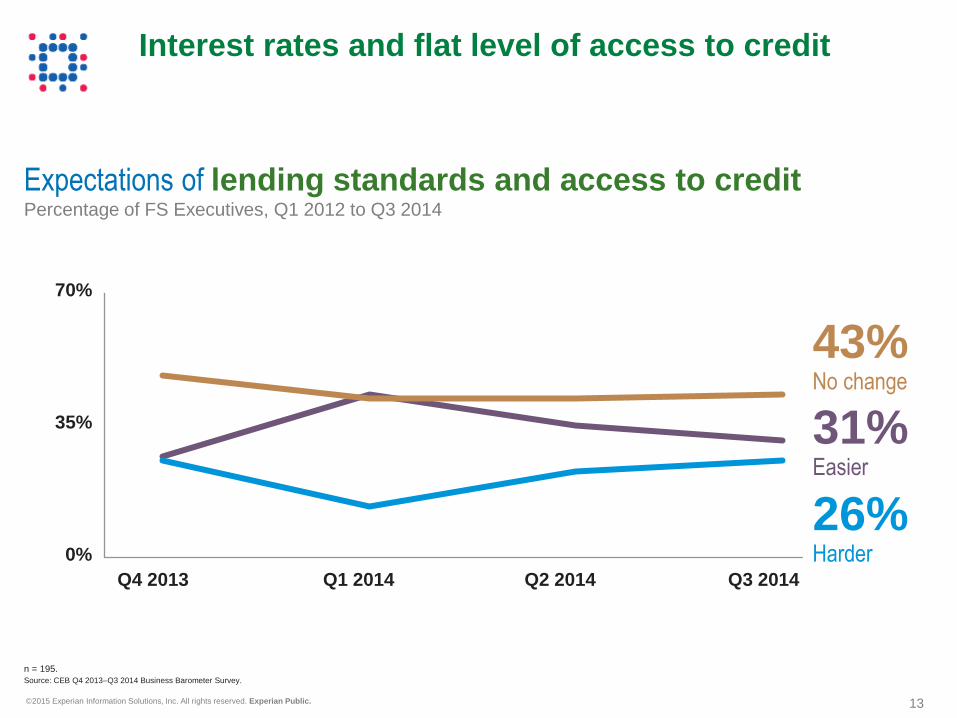

Interest rates and flat level of access to credit

0%

Q4 2013 Q1 2014 Q2 2014 Q3 2014

35%

70%

n = 195.

Source: CEB Q4 2013–Q3 2014 Business Barometer Survey.

Expectations of lending standards and access to credit Percentage of FS Executives, Q1 2012 to Q3 2014

43% No change

31%

Easier

26%

Harder

14 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

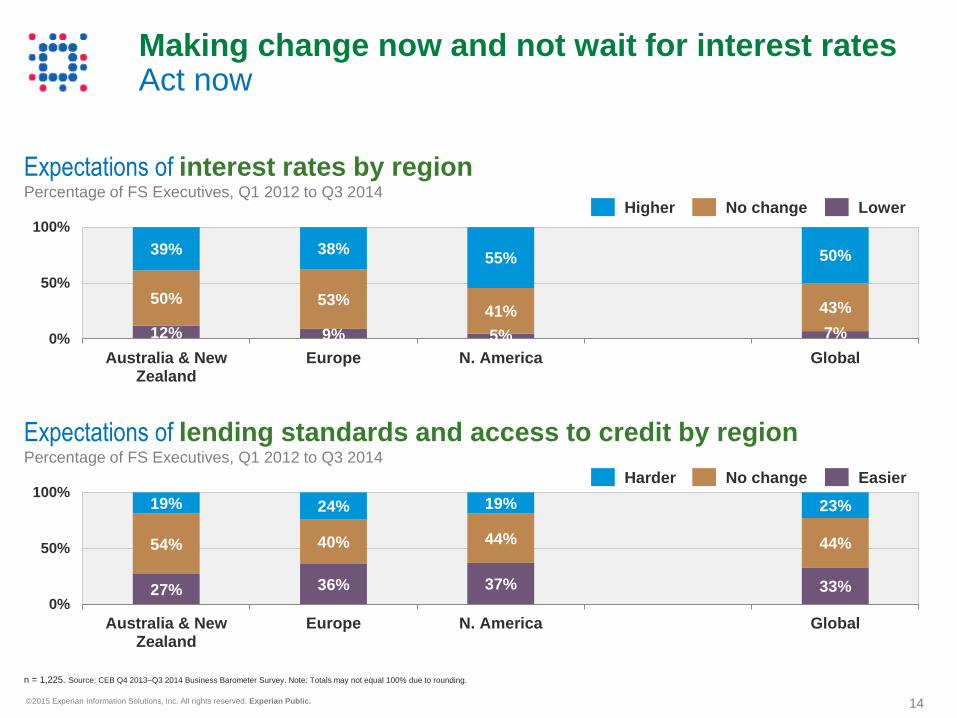

Expectations of interest rates by region Percentage of FS Executives, Q1 2012 to Q3 2014

12% 9% 5% 7%

50% 53% 41% 43%

39% 38% 55% 50%

0%

50%

100%

Australia & NewZealand

Europe N. America Global

Higher No change Lower

Making change now and not wait for interest rates Act now

n = 1,225. Source: CEB Q4 2013–Q3 2014 Business Barometer Survey. Note: Totals may not equal 100% due to rounding.

Expectations of lending standards and access to credit by region Percentage of FS Executives, Q1 2012 to Q3 2014

27% 36% 37% 33%

54% 40% 44% 44%

19% 24% 19% 23%

0%

50%

100%

Australia & NewZealand

Europe N. America Global

Harder No change Easier

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 15

What is at risk?

16 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

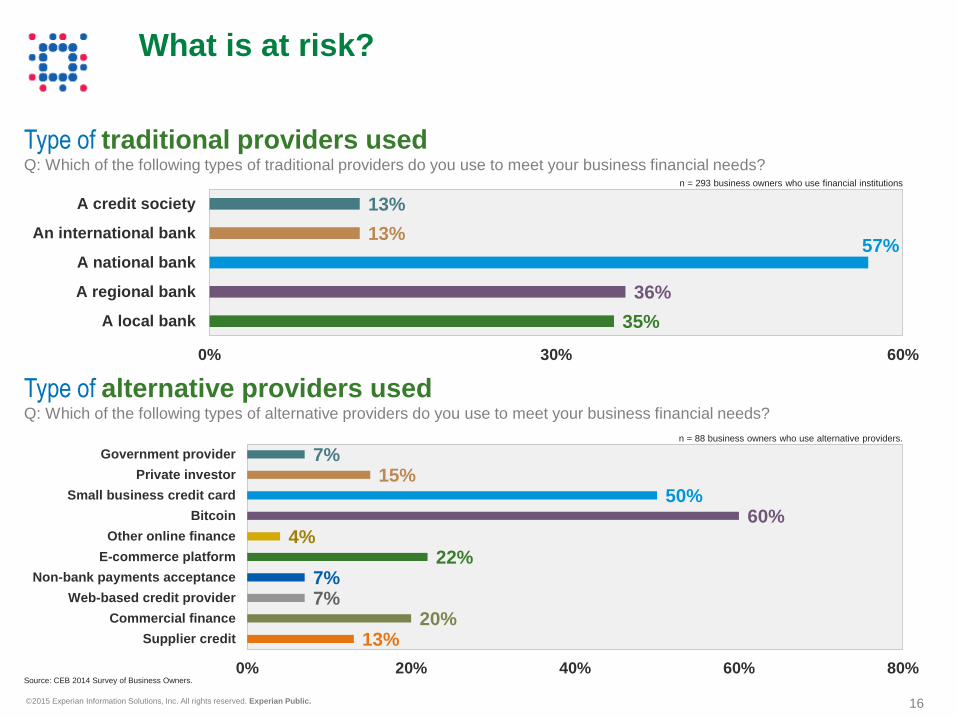

What is at risk?

n = 293 business owners who use financial institutions

35%

36%

57% 13%

13%

0% 30% 60%

A local bank

A regional bank

A national bank

An international bank

A credit society

Source: CEB 2014 Survey of Business Owners.

Type of alternative providers used Q: Which of the following types of alternative providers do you use to meet your business financial needs?

n = 88 business owners who use alternative providers.

13% 20%

7% 7%

22% 4%

60% 50%

15% 7%

0% 20% 40% 60% 80%

Supplier credit

Commercial finance

Web-based credit provider

Non-bank payments acceptance

E-commerce platform

Other online finance

Bitcoin

Small business credit card

Private investor

Government provider

Type of traditional providers used Q: Which of the following types of traditional providers do you use to meet your business financial needs?

17 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

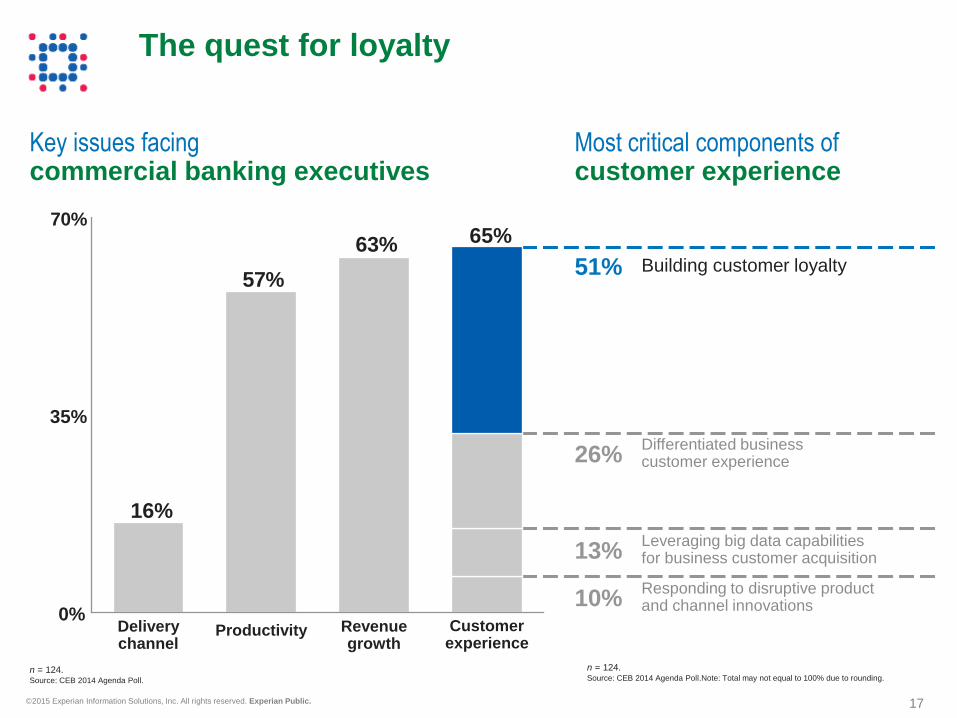

The quest for loyalty

n = 124. Source: CEB 2014 Agenda Poll.

n = 124. Source: CEB 2014 Agenda Poll.Note: Total may not equal to 100% due to rounding.

Most critical components of customer experience

26% Differentiated business customer experience

51% Building customer loyalty

13% Leveraging big data capabilities for business customer acquisition

10% Responding to disruptive product and channel innovations

Key issues facing commercial banking executives

Delivery channel

Productivity Revenue growth

Customer experience

0%

35%

70%

16%

57%

63% 65%

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 18

What is the segment

within the segment?

19 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

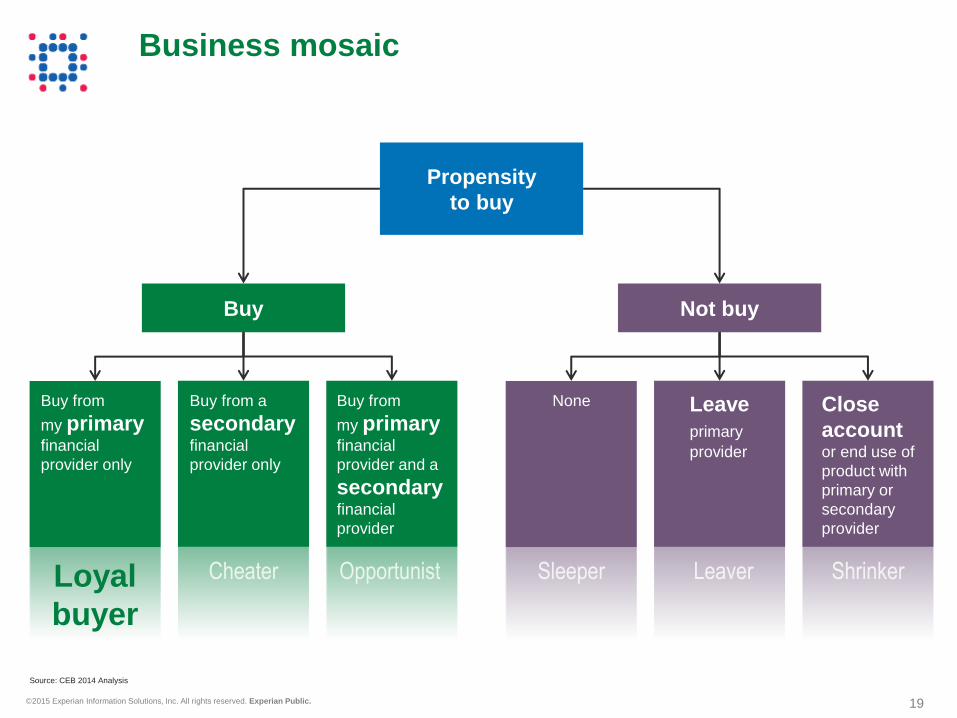

Business mosaic

Buy Not buy

Propensity

to buy

Buy from

my primary financial

provider and a

secondary financial

provider

Buy from a

secondary financial

provider only

Buy from

my primary financial

provider only

Leave

primary provider

None Close

account or end use of

product with

primary or

secondary

provider

Opportunist Cheater Sleeper Leaver Shrinker Loyal

buyer

Source: CEB 2014 Analysis

20 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Half of revenue opportunity is going to competitors

Source: CEB 2014

Business Owners Survey

21%

11% 8%

48%

8% 5%

17% 12%

6%

53%

8% 4%

0%

30%

60%

Loyal buyer Cheater Opportunist Sleeper Leaver Shrinker

Past Future

Typology distribution n = 1,493 (Past); 1,475 (Future)

Past purchases Future purchases

61%

Loyal buyer 28%

Cheater

21%

Opportunist

47%

Loyal buyer 35%

Cheater

18%

Opportunist

n = 572 n = 633

21 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Loyal buyer basics

9% 10%

53% 37%

31% 46%

7% 7%

0%

50%

100%

Loyal Buyers All Respondents

67 & above

47 to 67

30 to 46

Less than 30

Age of business owner Percentage of Loyal Buyers vs. All Respondents

n = 289 (Loyal Buyers); 1,485 (All Respondents) Source: CEB 2014 Business Owners Survey

22 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Loyal buyer basics

Age of business Percentage of Loyal Buyers vs. All Respondents

24%

28%

17%

25%

7%

0%

28%

29%

18%

17%

6%

2%

0% 20% 40%

> 20 years

11-20 years

7-10 years

4-6 years

1-3 years

< 1 year

All Respondents

Loyal Buyer

n = 263 (Loyal Buyers); 1,310 (All Respondents) Source: CEB 2014 Business Owners Survey

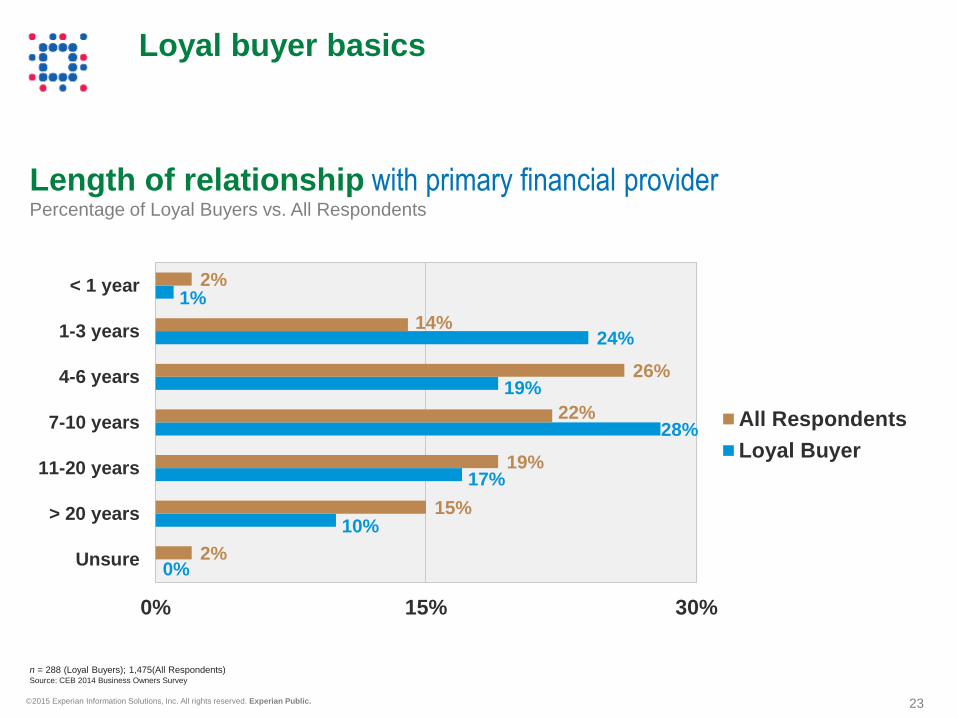

23 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Loyal buyer basics

Length of relationship with primary financial provider Percentage of Loyal Buyers vs. All Respondents

0%

10%

17%

28%

19%

24%

1%

2%

15%

19%

22%

26%

14%

2%

0% 15% 30%

Unsure

> 20 years

11-20 years

7-10 years

4-6 years

1-3 years

< 1 year

All Respondents

Loyal Buyer

n = 288 (Loyal Buyers); 1,475(All Respondents) Source: CEB 2014 Business Owners Survey

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 24

What are

commercial

borrowers

wanting?

25 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

What is the buyer wanting and who does the buyer want to work with?

N = 336 United State; n = 1,544 Multi-national

Source: CEB 2014 Survey of Business Owners.

Type of contact at primary business provider

32% 37%

26%

33%

10%

10% 4%

6% 28%

14%

0%

50%

100%

United States Multi-national

No primary contact

Non-bank representative

Other bank representative

Bank branch manager

Bank regional manager

26 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

n = 312 business owners.

Source: CEB 2014 Survey of Business Owners.

Face-to-face channels dominate purchasing

Current channel use for specific banking activities

38%

25%

36% 34%

47% 39%

18%

12%

13%

16% 17%

19%

17%

7%

39%

49% 20% 20%

21%

28%

18%

2% 5%

5% 5%

6% 3%

6%

1%

9% 7%

22% 21%

7% 12%

49%

2% 1% 1% 1%

0%

50%

100%

Resolvingproblems aboutmy transactions

Resolvingproblems about

my credit

Learning abouttransactionproducts

Learning aboutcredit products

Purchase newtransaction

products

Purchasing newcredit products

Using financialservices

Social media

Mobile app

Online bankWebsite

ATM

Automated phonecenter contact

Personal phonecontact

Face-to-face withreg mgr

Branch face-to-face

27 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

What loyal buyers purchase Loyal buyers purchased primarily business lines of credit and online services in the past year

n = 310 (Loyal Buyer; n = 168 (Cheater); n = 128 (Opportunist)

Source: CEB 2014

12%

24%

12%

21%

24%

11%

16%

10%

22%

21%

15%

16%

19%

25%

34%

0% 10% 20% 30% 40%

Owner occupied real estate loans

Mobile business banking

General payment & collection services

Checking accounts

Business lines of credit

Loyal Buyer

Cheater

Opportunist

28 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Engaging loyal buyers

Source: CEB 2014 Business Owners Survey.

Reason for purchase Loyal Buyers vs. All Respondents

4%

29%

41%

25%

2% 6%

26%

36% 31%

2% 0%

25%

50%

Dissatisfed withanother product

Business need for anew product

Learned of businessneed for product

Responded toproduct offering

Other

n = 288 (Loyal Buyers); n = 685 (All Respondents)

Source of learned need Loyal Buyers vs. All Respondents

57%

18% 9% 8% 7% 3%

47% 19%

7% 10% 10% 8%

0%

30%

60%

Guidance fromfinancial provider

Advertisements Social media Friends / family Guidance fromnon-financial

provider

News / media

n = 117 (Loyal Buyers); n = 208 (All Respondents)

Loyal Buyers All Respondents

29 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Source: CEB analysis.

As “good” as it gets

Q: Which one word best describes your relationship with your primary financial provider?

30 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

n = 338 business owners (U.S.); n = 1,553 business owners (Multi-national)

Source: CEB 2014 Survey of Business Owners.

“Nobody” is the most recommended

Recommendations

15%

10% 8%

15% 11%

21%

56%

25%

10%

15%

20%

10%

20%

37%

0%

30%

60%

Businessprimaryfinancialprovider

Businessnon-primary

financialprovider

Businessbank

relationshipmanager

Businessbank branch

manager

Businessnon-bankadvisor

Otherprofessional

advisor

None

United States

Multi-national

31 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

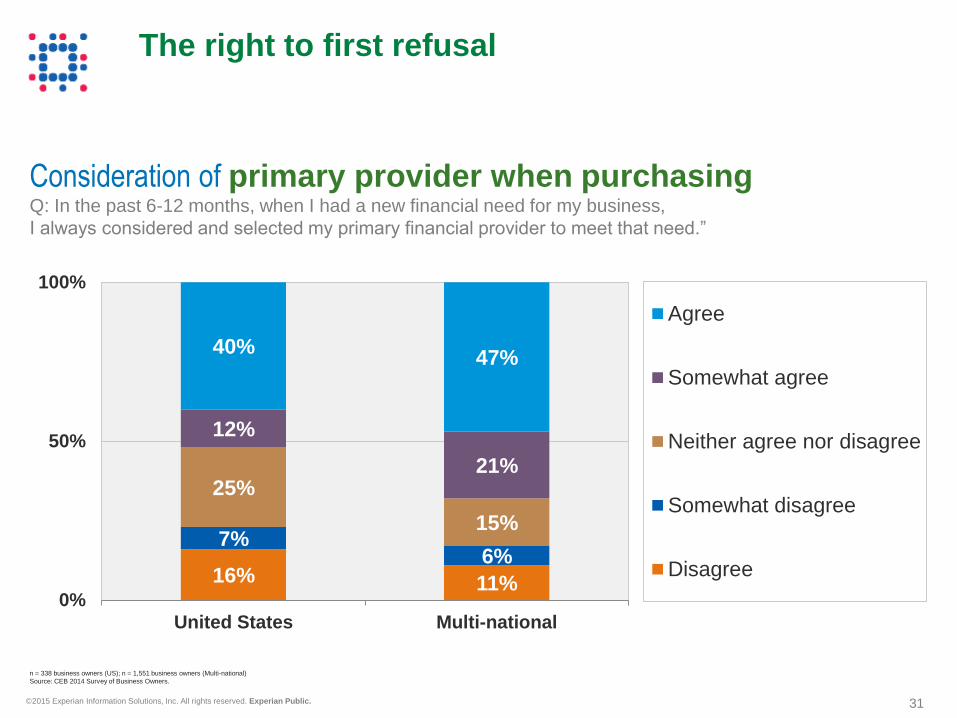

n = 338 business owners (US); n = 1,551 business owners (Multi-national)

Source: CEB 2014 Survey of Business Owners.

The right to first refusal

Consideration of primary provider when purchasing Q: In the past 6-12 months, when I had a new financial need for my business,

I always considered and selected my primary financial provider to meet that need.”

16% 11%

7% 6%

25%

15%

12%

21%

40% 47%

0%

50%

100%

United States Multi-national

Agree

Somewhat agree

Neither agree nor disagree

Somewhat disagree

Disagree

32 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Source: CEB 2014 Survey of Business Owners.

Well-connected to business owners

83% of business owners in the U.S. have a smartphone or tablet

Owners in the U.S. are slightly less likely to use social media than internal business owners

37% of U.S. business owners do not use social media, compared with 25% internationally

0%

50%

100%

United States Multi-national

Have smartphone & tablet

Have tablet, no smartphone

Have smartphone, no tablet

No smart phone or tablet

Prevalence of personal smartphone

or tablet ownership n = 337 business owners (US); n = 1,546 business owners (Multi-national)

0%

50%

100%

United States Multi-national

Actively read and contribute

Often read, occasionallycontribute

Often read, do not contribute

Sometimes read, do notcontribute

Do not use

Use of social media n = 337 business owners (US); n = 1,546 business owners (Multi-national)

33 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

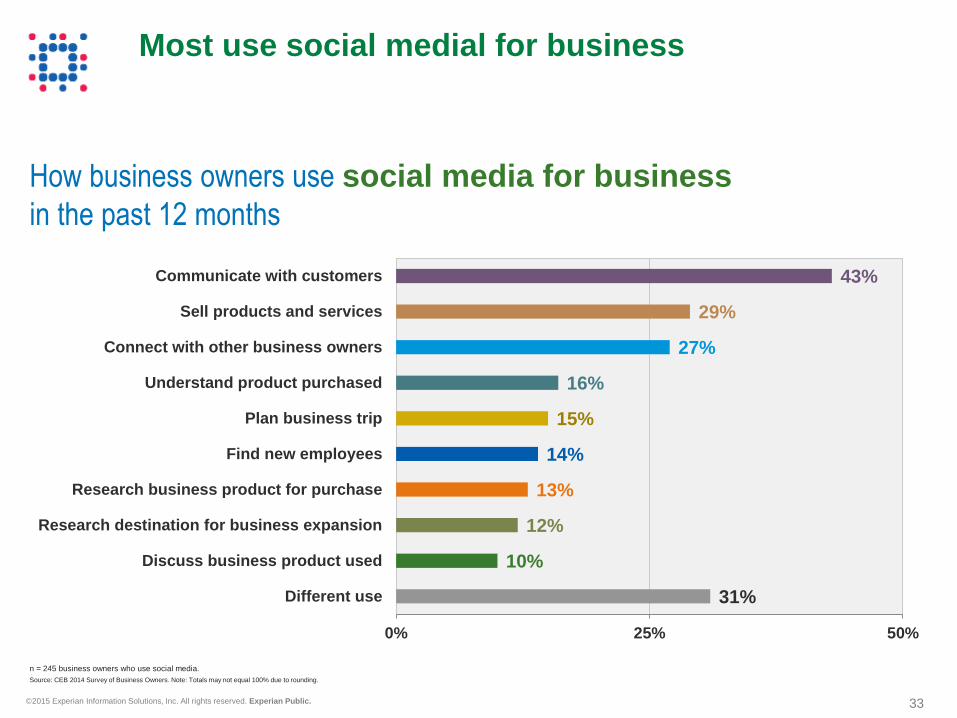

n = 245 business owners who use social media.

Source: CEB 2014 Survey of Business Owners. Note: Totals may not equal 100% due to rounding.

Most use social medial for business

How business owners use social media for business

in the past 12 months

31%

10%

12%

13%

14%

15%

16%

27%

29%

43%

0% 25% 50%

Different use

Discuss business product used

Research destination for business expansion

Research business product for purchase

Find new employees

Plan business trip

Understand product purchased

Connect with other business owners

Sell products and services

Communicate with customers

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 34

Case study

35 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Develop an accessible and quantitative method for defining an prioritizing specialization areas

Imperative: Identify quality businesses Segment selection process

Define Prioritize Understand

Syndicated data

Customer data

Primary research Employee

size

Industry types

Priority: Market size (50%) + Penetration (15%) +

Profitability per business (35%)

Identify high-risk segments

Customer profitability

Market penetration

Market opportunity

Product needs

All businesses

Five groups

36 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Use existing customer data to better understand and build best-fit strategies for segments

Imperative: Identify quality businesses

Bank

Segmentation

Report

An analysis of segment

needs, demand, and

profitability in existing

customer base

Bank existing

customer base

Segmentation Report

37 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Use existing customer data to better understand and build best-fit strategies for segments

Imperative: Identify quality businesses

Industry profitability

by size Illustrative

Number of employees

1-3 4-9 10-24 25-50

Pro

fita

bilit

y p

er

em

plo

ye

e

Product propensity for industry

by size Illustrative

Number of employees

Deposits Loans Cash management

Merchant services

More likely to own

Indifferent

Less likely to own

1-3 4-9 10-24 25-50

38 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Express review

Faster, with a focus on serving an immediate need

Needs-driven outreach

CM may contact priority client with a targeted offer, such as a rewards credit card that fits his or her spending habits

Event-driven outreach

CM may contact priority client in response to certain triggers, such as a term deposit reaching maturity

Full A-to-Z needs-based discussion

20-30 minutes

In-depth detailed assessment of the whole client relationship

Imperative: Help customers plan Annual priority client relationship cycle

Q1 Q2

Q3 Q4

39 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Imperative: Help customers plan Characteristics and benefits of the A-Z needs-based discussion

Clients are receptive to periodic, in-depth discussions because they value the time saved by the service

Previously, their needs were underserved

Discussion format is flexible, meaning CMs talk broadly about clients’ situations and conversations feel focused on goals rather than sales

Information allows CMs to build a pipeline of life events and also proactively reach out with offers based on what they learn from the discussions

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 40

@mikehorrocks

For additional information,

please contact:

@ExperianVision | #vision2015

Follow us on Twitter:

41 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Share your thoughts about Vision 2015!

Please take the time now to give us your feedback about this session. You can complete the survey in the mobile app or request a paper survey.

Select the breakout

session you attended

Select the Survey

button and complete 1 2

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.