Embed Size (px)

Citation preview

Presentation for

| May 30, 2013

May 30, 2013

MODULE 1: What is C&I Lending?

May 30, 2013

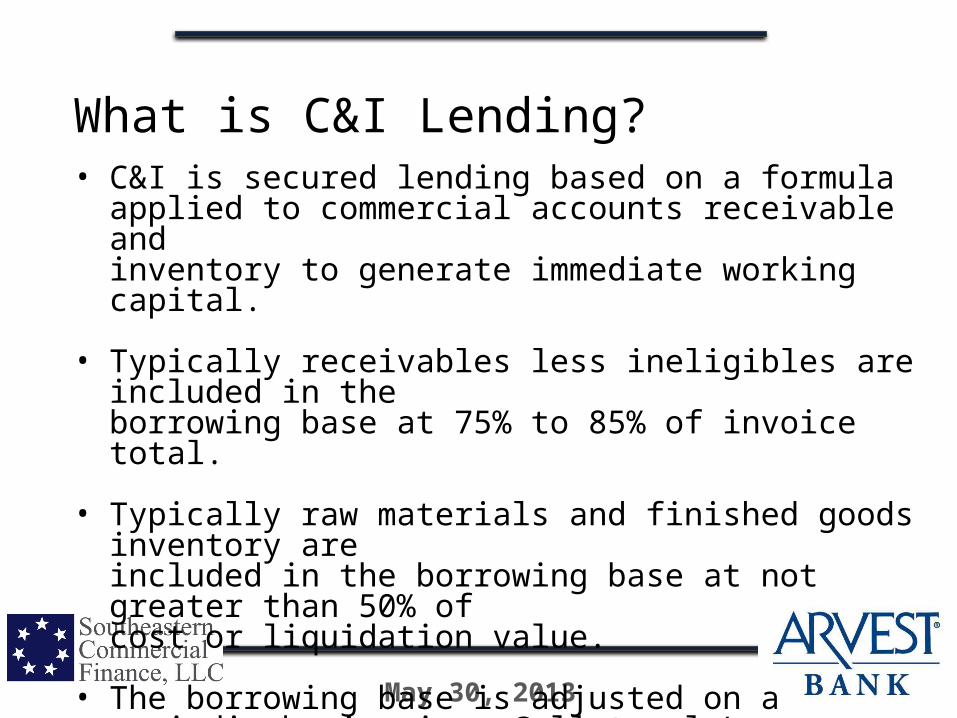

What is C&I Lending?• C&I is secured lending based on a formula

applied to commercial accounts receivable and inventory to generate immediate working capital.

• Typically receivables less ineligibles are included in the borrowing base at 75% to 85% of invoice total.

• Typically raw materials and finished goods inventory are included in the borrowing base at not greater than 50% of cost or liquidation value.

• The borrowing base is adjusted on a periodic basis via a Collateral Loan Report.

May 30, 2013

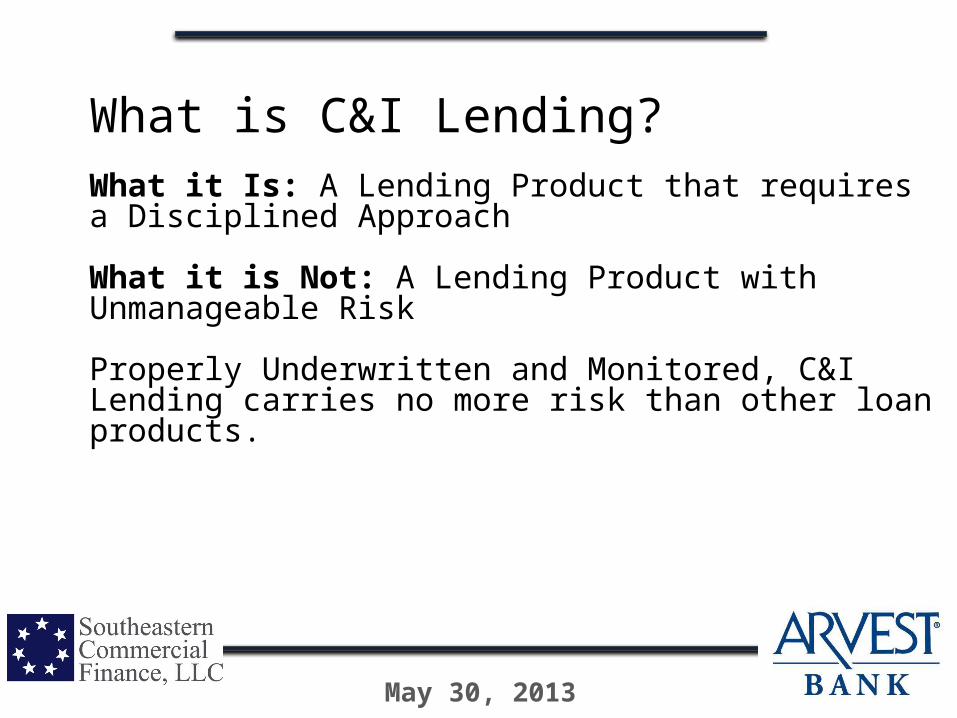

What is C&I Lending?What it Is: A Lending Product that requires a Disciplined Approach

What it is Not: A Lending Product with Unmanageable Risk

Properly Underwritten and Monitored, C&I Lending carries no more risk than other loan products.

May 30, 2013

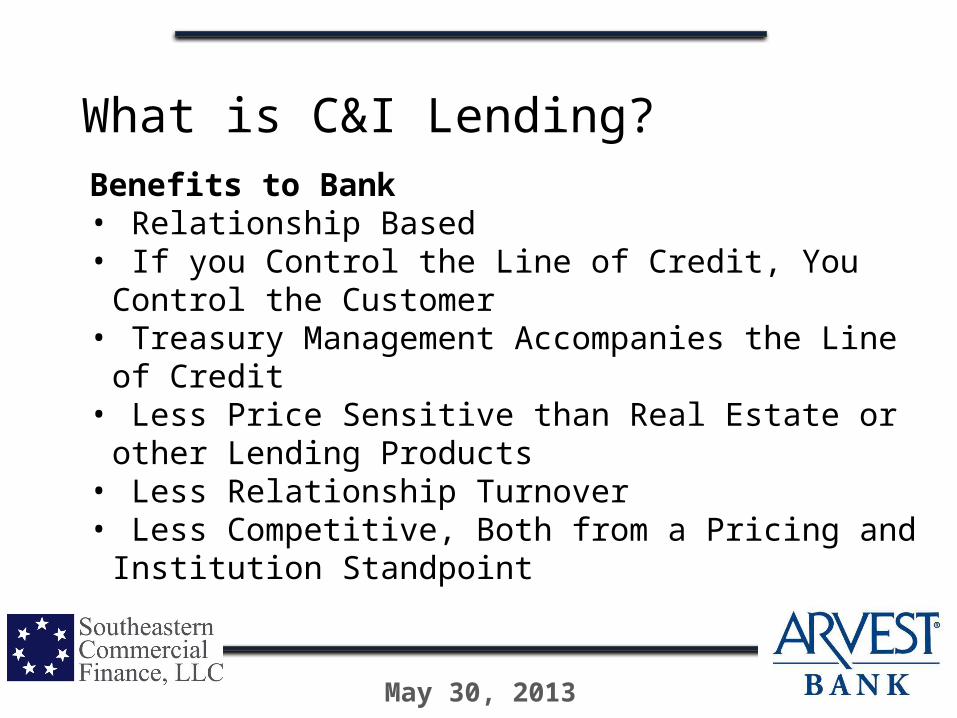

What is C&I Lending?Benefits to Bank• Relationship Based• If you Control the Line of Credit, You Control the

Customer• Treasury Management Accompanies the Line of

Credit• Less Price Sensitive than Real Estate or other

Lending Products• Less Relationship Turnover• Less Competitive, Both from a Pricing and

Institution Standpoint

May 30, 2013

What is C&I Lending?

Key Differences Between C&I and Other Lending Products • Relationship Based v. Transaction Based• Consultive and Advising v. Price Base Sales

Process• Establishing Creditability with Management is Key• Business Analysis, Credit and Underwriting Skills

are Imperative

May 30, 2013

Cash Flow Cycles of C&I are determined by the relationships between A/R Turns, Inventory Turns, & A/P Turns.

May 30, 2013

MODULE 2: Evaluation of and Lending on Accounts

Receivable

May 30, 2013

Tools for General Evaluation of Accounts Receivable:• Who is the Receivable from?• What are the terms?• Is the sale complete?• Is there the possibility of dispute of the

receivable?• How long is the collection cycle (A/R

turnover)?

May 30, 2013

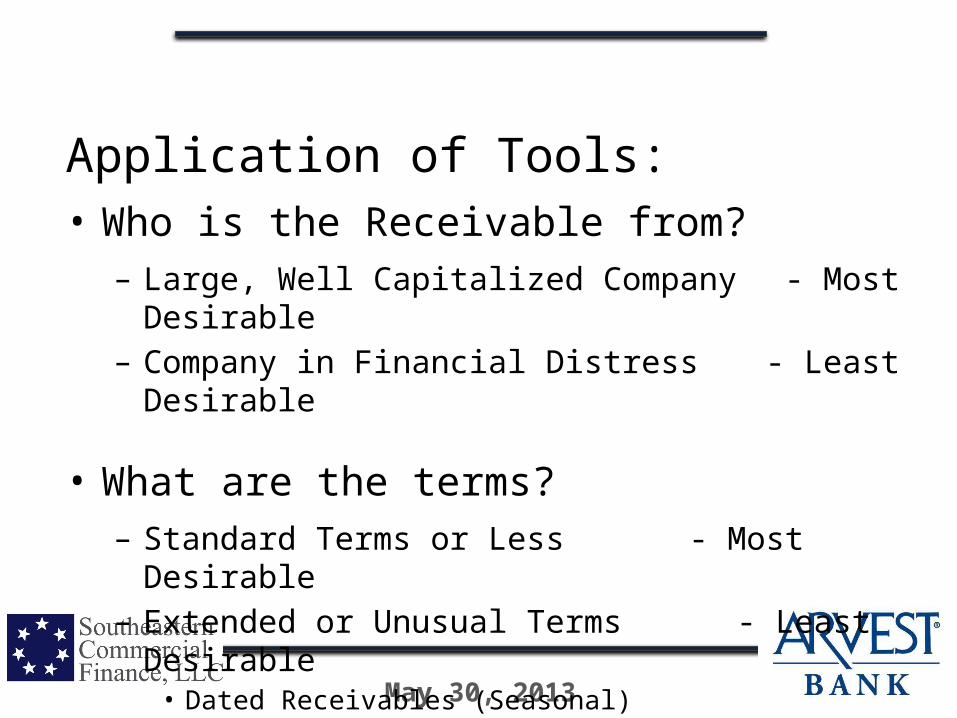

Application of Tools:• Who is the Receivable from?– Large, Well Capitalized Company - Most

Desirable– Company in Financial Distress -

Least Desirable

• What are the terms?– Standard Terms or Less -

Most Desirable– Extended or Unusual Terms - Least

Desirable• Dated Receivables (Seasonal)• Consignment / Guaranteed Sale

May 30, 2013

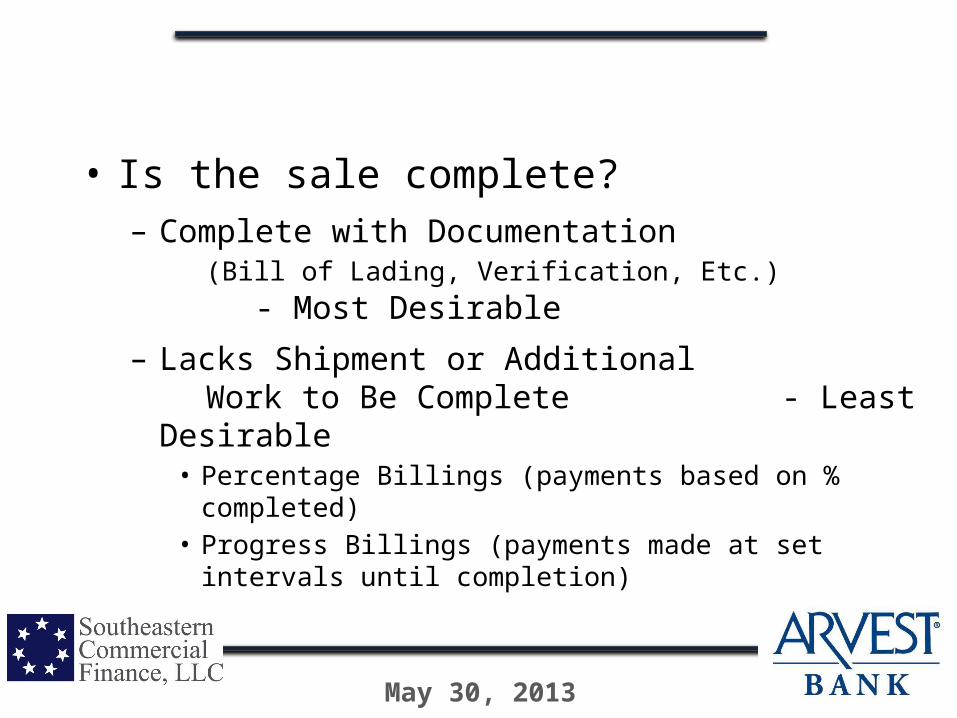

• Is the sale complete?– Complete with Documentation (Bill of Lading, Verification, Etc.) -

Most Desirable

– Lacks Shipment or Additional Work to Be Complete - Least

Desirable• Percentage Billings (payments based on %

completed)• Progress Billings (payments made at set intervals

until completion)

May 30, 2013

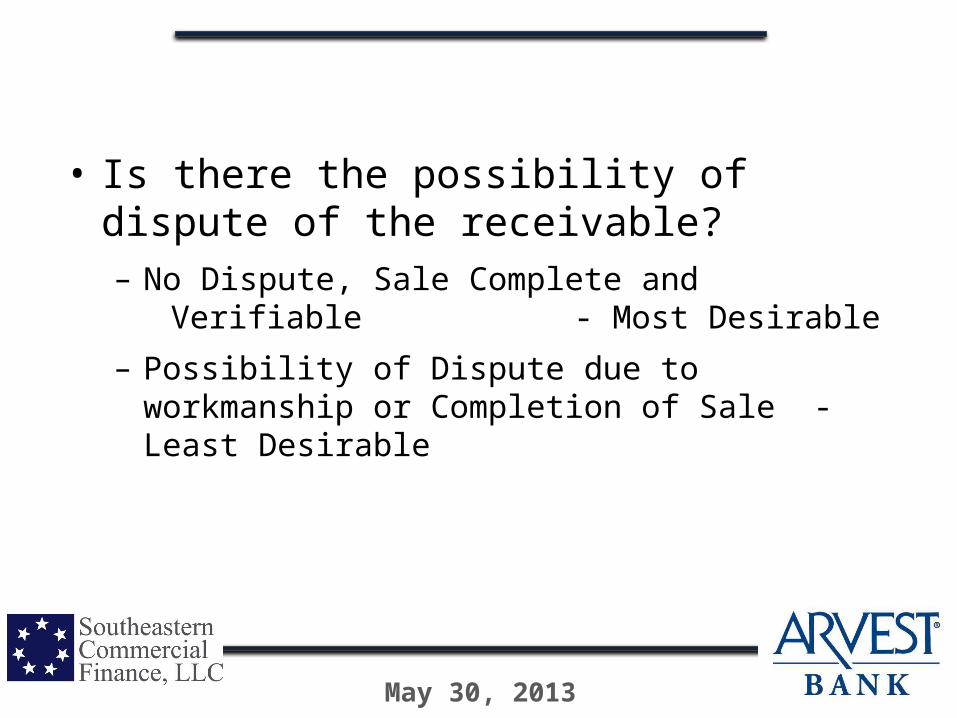

• Is there the possibility of dispute of the receivable?– No Dispute, Sale Complete and Verifiable - Most

Desirable

– Possibility of Dispute due to workmanship or Completion of Sale - Least Desirable

May 30, 2013

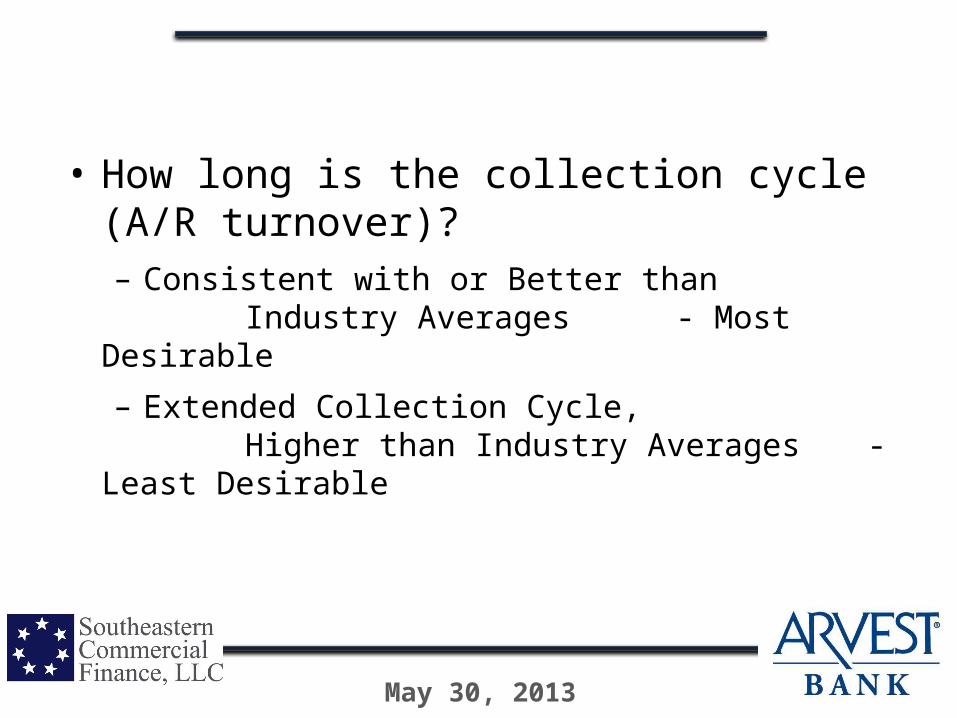

• How long is the collection cycle (A/R turnover)?– Consistent with or Better than

Industry Averages - Most Desirable

– Extended Collection Cycle, Higher than Industry Averages -

Least Desirable

May 30, 2013

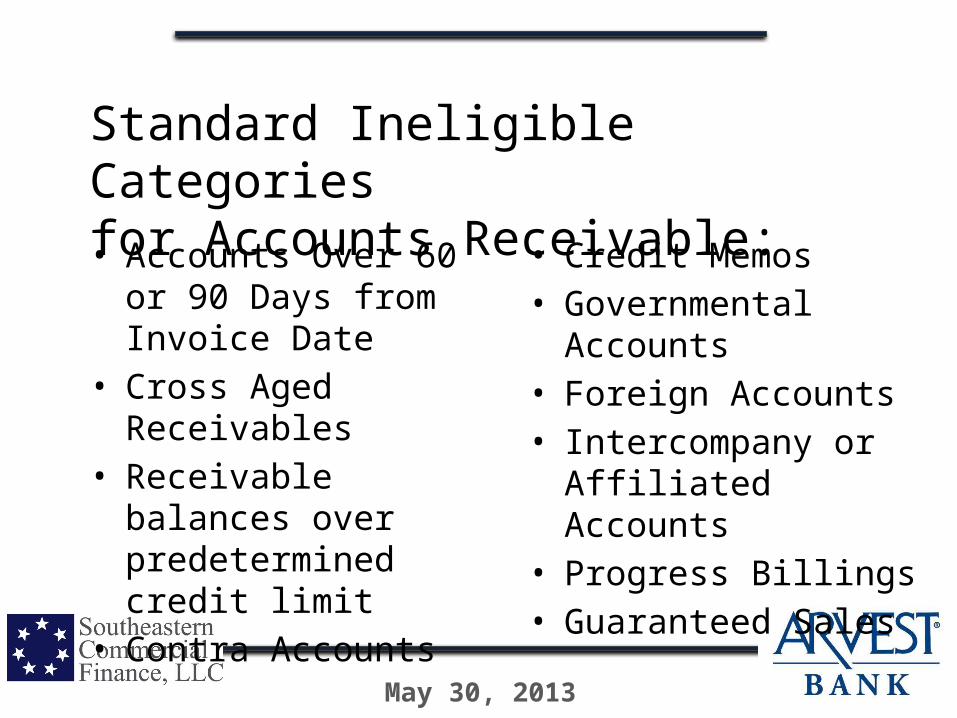

Standard Ineligible Categories for Accounts Receivable:• Accounts Over 60 or

90 Days from Invoice Date

• Cross Aged Receivables

• Receivable balances over predetermined credit limit

• Contra Accounts

• Credit Memos• Governmental

Accounts• Foreign Accounts• Intercompany or

Affiliated Accounts• Progress Billings• Guaranteed Sales

May 30, 2013

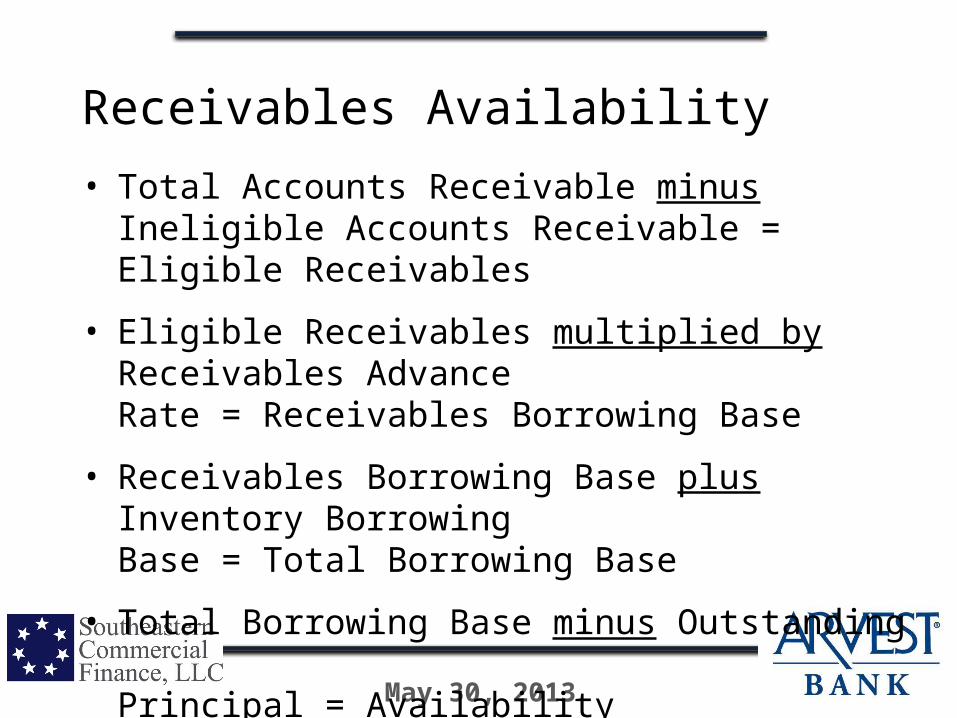

Receivables Availability

• Total Accounts Receivable minus Ineligible Accounts Receivable = Eligible Receivables

• Eligible Receivables multiplied by Receivables Advance Rate = Receivables Borrowing Base

• Receivables Borrowing Base plus Inventory Borrowing Base = Total Borrowing Base

• Total Borrowing Base minus Outstanding Principal = Availability

May 30, 2013

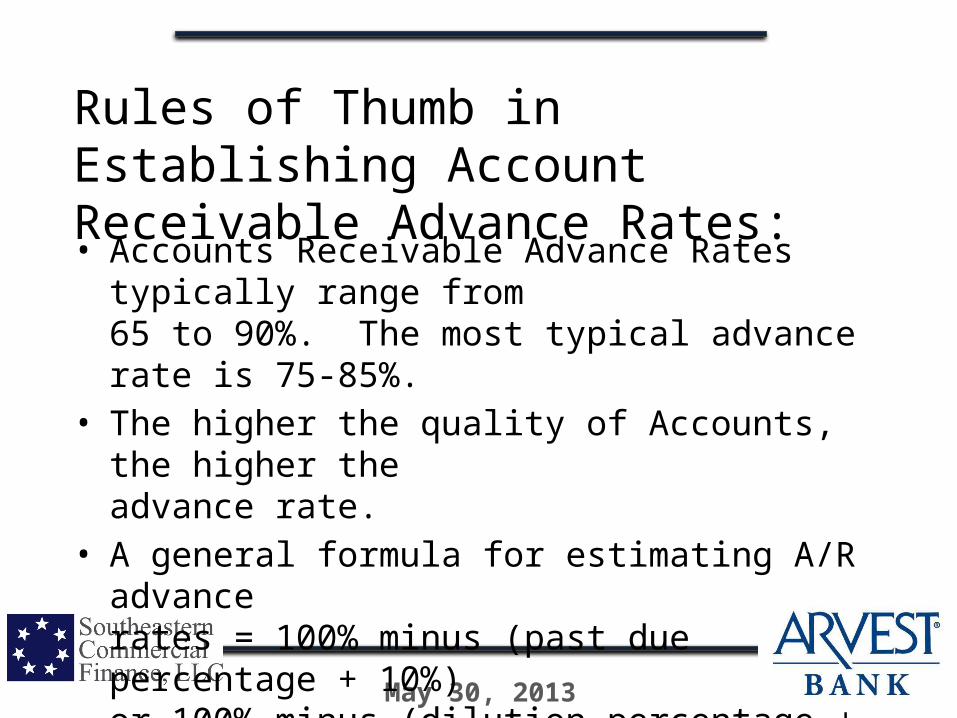

Rules of Thumb in Establishing Account Receivable Advance Rates:• Accounts Receivable Advance Rates typically

range from 65 to 90%. The most typical advance rate is 75-85%.

• The higher the quality of Accounts, the higher the advance rate.

• A general formula for estimating A/R advance

rates = 100% minus (past due percentage + 10%) or 100% minus (dilution percentage + 10%)

May 30, 2013

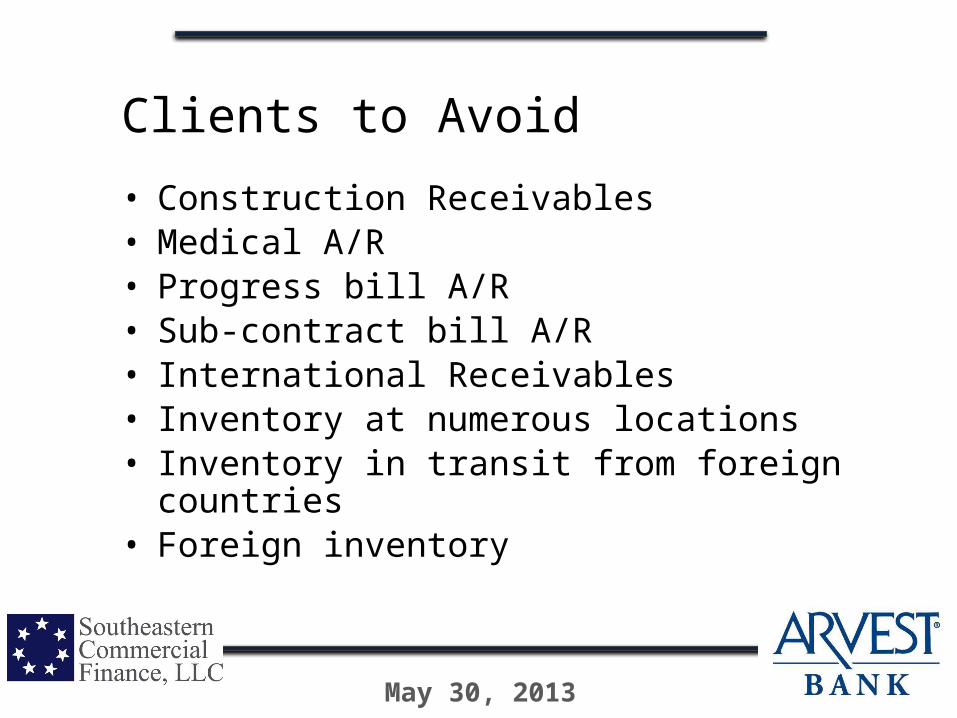

Clients to Avoid

• Construction Receivables• Medical A/R• Progress bill A/R• Sub-contract bill A/R• International Receivables• Inventory at numerous locations• Inventory in transit from foreign

countries• Foreign inventory

May 30, 2013

MODULE 3: Evaluation of and Lending on Inventory

May 30, 2013

Editorial Comment: “Underwriting Accounts Receivable is a Science. Underwriting Inventory is Witchcraft.”

May 30, 2013

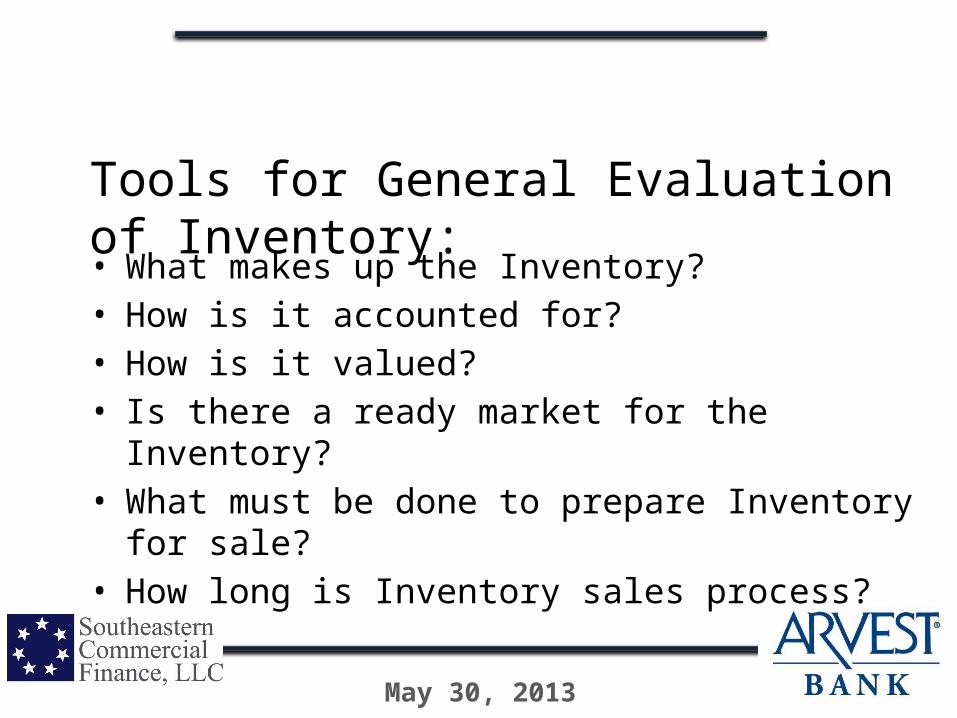

Tools for General Evaluation of Inventory:• What makes up the Inventory?• How is it accounted for?• How is it valued?• Is there a ready market for the Inventory?• What must be done to prepare Inventory for

sale?• How long is Inventory sales process?

May 30, 2013

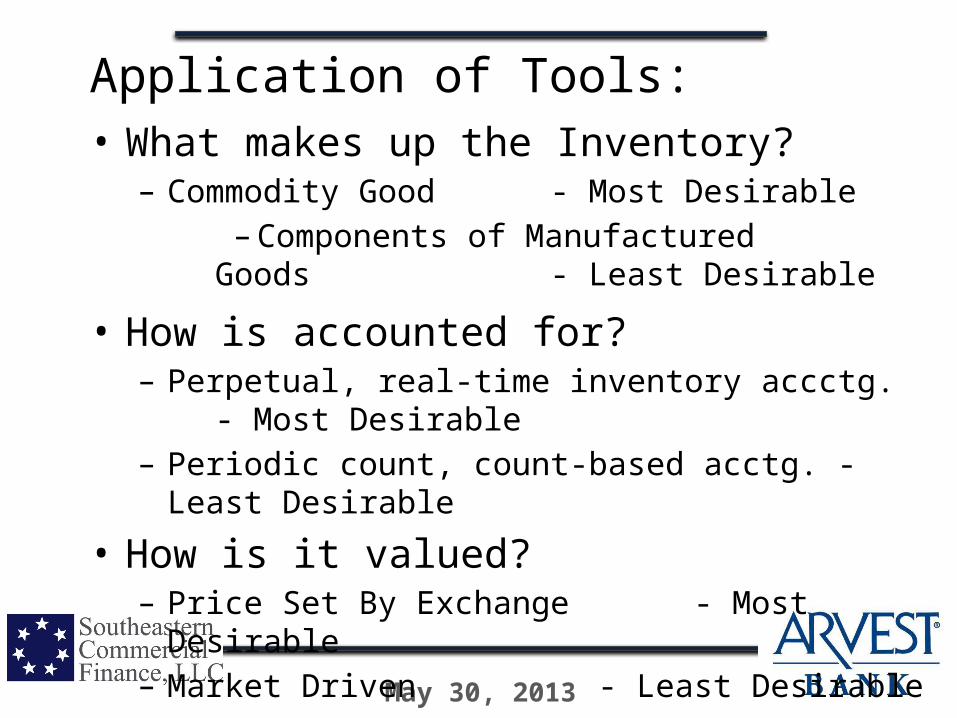

Application of Tools:• What makes up the Inventory?– Commodity Good - Most Desirable

–Components of Manufactured Goods -

Least Desirable

• How is accounted for?– Perpetual, real-time inventory accctg. -

Most Desirable– Periodic count, count-based acctg. - Least

Desirable

• How is it valued?– Price Set By Exchange - Most

Desirable– Market Driven - Least

Desirable

May 30, 2013

• Is there a ready market for the Inventory?– Large Number of Potential Buyers - Most

Desirable– Limited Number of Industry Competitors -

Least Desirable

• What must be done to prepare Inventory for sale?– Completed and Ready for Shipment -

Most Desirable– Assembly Required - Least

Desirable

May 30, 2013

• How long is Inventory sales process?– Immediate Buyers Available - Most

Desirable– Extended Sales Process -

Least Desirable

May 30, 2013

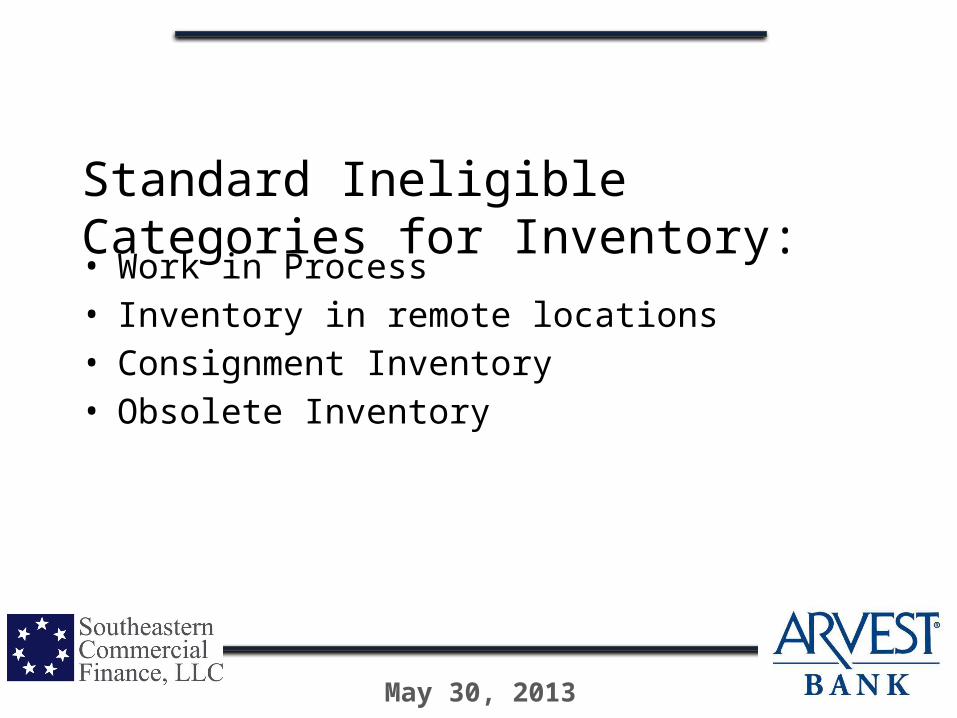

Standard Ineligible Categories for Inventory:• Work in Process • Inventory in remote locations• Consignment Inventory• Obsolete Inventory

May 30, 2013

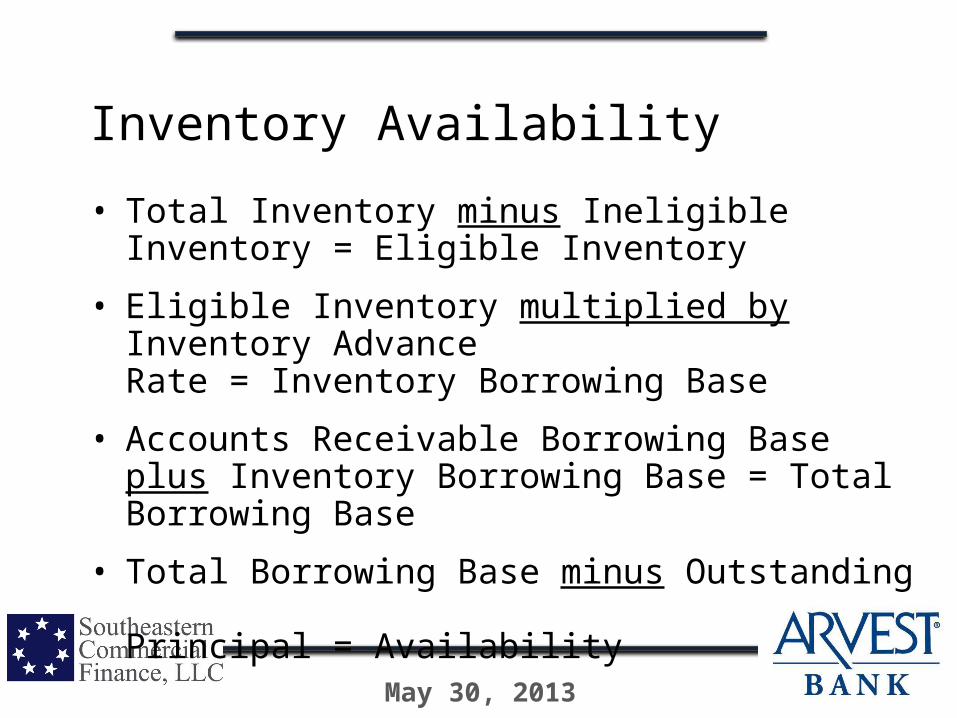

Inventory Availability

• Total Inventory minus Ineligible Inventory = Eligible Inventory

• Eligible Inventory multiplied by Inventory Advance Rate = Inventory Borrowing Base

• Accounts Receivable Borrowing Base plus Inventory Borrowing Base = Total Borrowing Base

• Total Borrowing Base minus Outstanding Principal = Availability

May 30, 2013

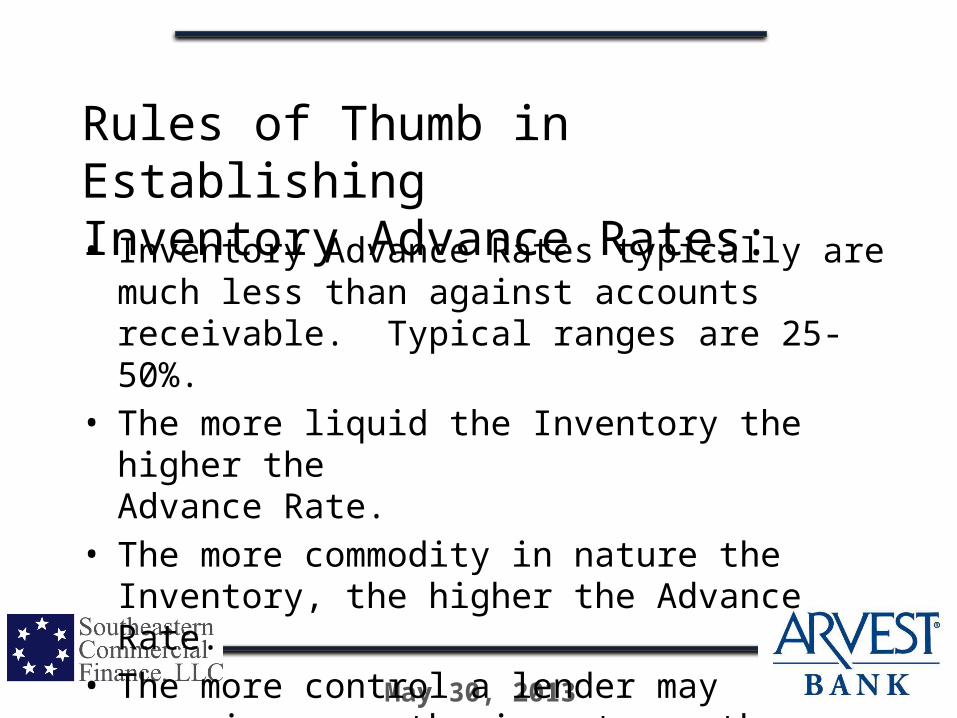

Rules of Thumb in Establishing Inventory Advance Rates:• Inventory Advance Rates typically are much

less than against accounts receivable. Typical ranges are 25-50%.

• The more liquid the Inventory the higher the Advance Rate.

• The more commodity in nature the Inventory, the higher the Advance Rate.

• The more control a lender may exercise over the inventory, the higher the Advance Rate.

May 30, 2013

MODULE 4: Structuring a Working Capital Line of Credit

May 30, 2013

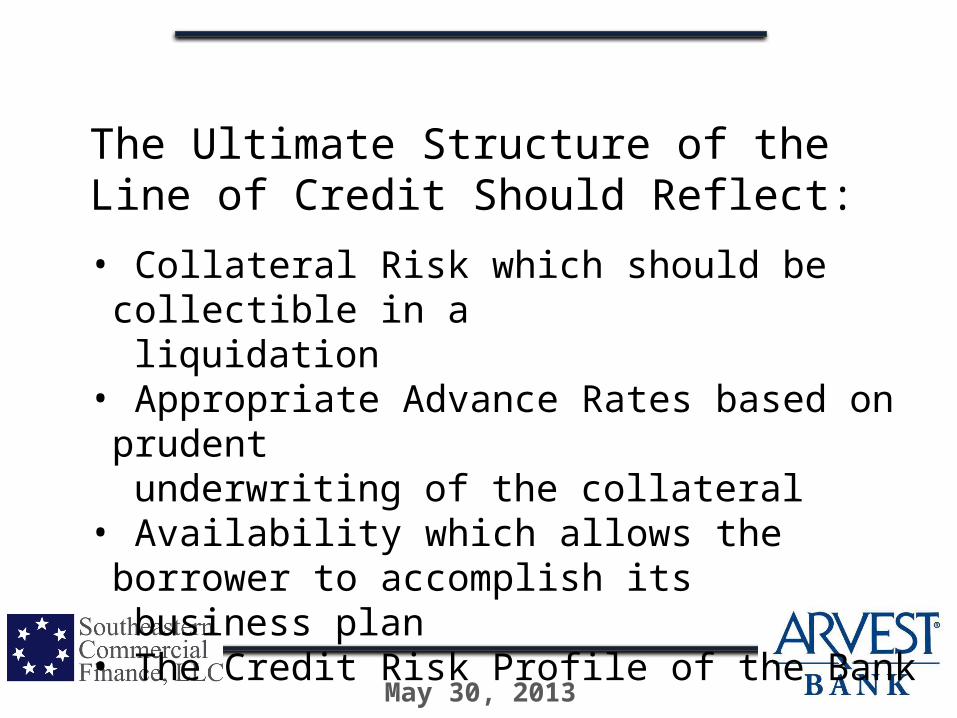

The Ultimate Structure of the Line of Credit Should Reflect:

• Collateral Risk which should be collectible in a

liquidation• Appropriate Advance Rates based on prudent

underwriting of the collateral• Availability which allows the borrower to accomplish its

business plan• The Credit Risk Profile of the Bank

May 30, 2013

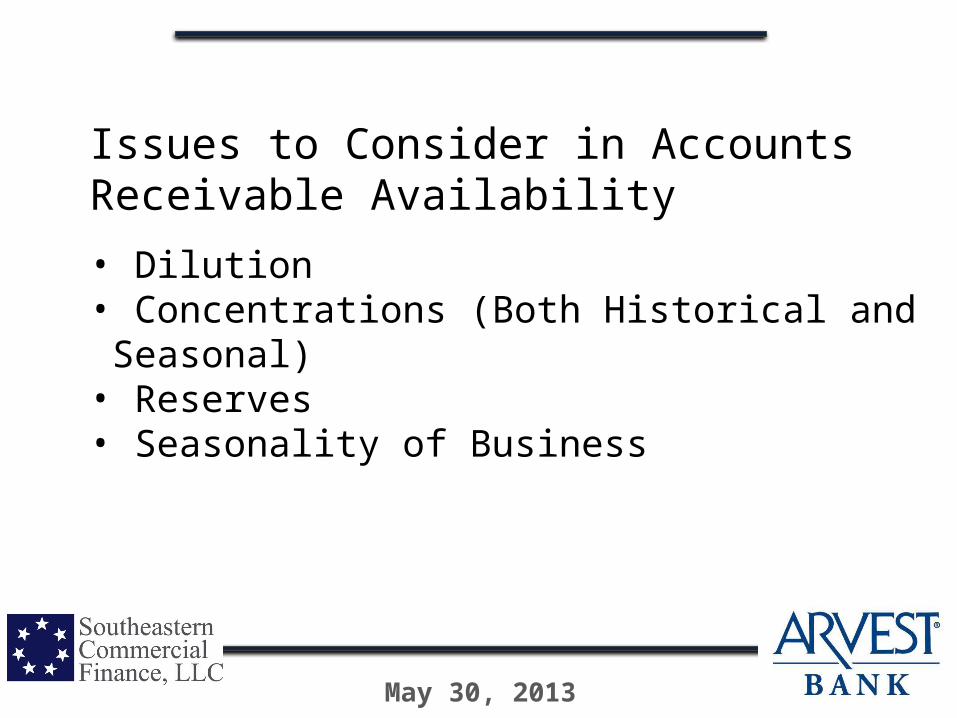

Issues to Consider in Accounts Receivable Availability

• Dilution• Concentrations (Both Historical and Seasonal)• Reserves • Seasonality of Business

May 30, 2013

Issues to Consider in Inventory Availability

• Seasonality• Maximum Exposure (both seasonal and non seasonal)• Limits on Inventory Advances

‐ Hard Dollar‐ Percentage of A/R Availability• Seasonal needs

May 30, 2013

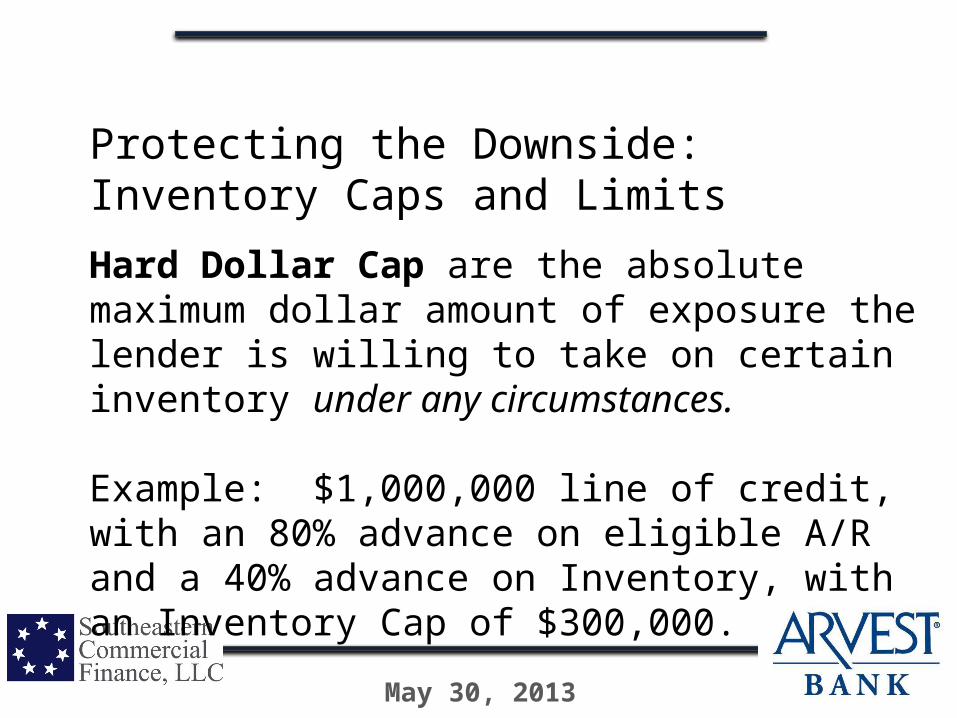

Protecting the Downside: Inventory Caps and Limits

Hard Dollar Cap are the absolute maximum dollar amount of exposure the lender is willing to take on certain inventory under any circumstances. Example: $1,000,000 line of credit, with an 80% advance on eligible A/R and a 40% advance on Inventory, with an Inventory Cap of $300,000.

May 30, 2013

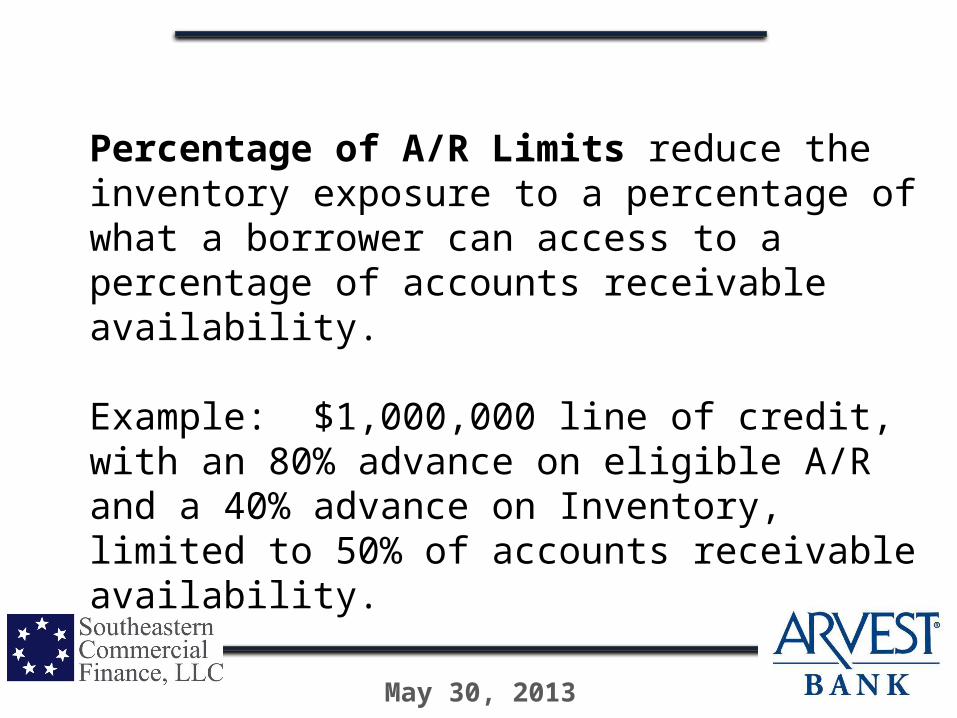

Percentage of A/R Limits reduce the inventory exposure to a percentage of what a borrower can access to a percentage of accounts receivable availability. Example: $1,000,000 line of credit, with an 80% advance on eligible A/R and a 40% advance on Inventory, limited to 50% of accounts receivable availability.

May 30, 2013

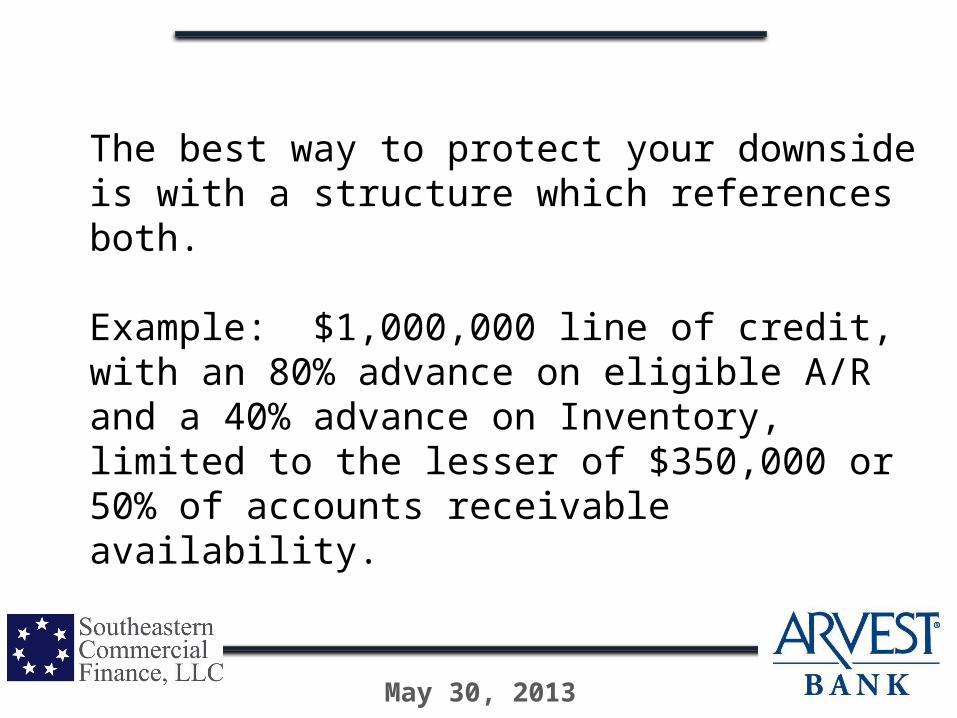

The best way to protect your downside is with a structure which references both. Example: $1,000,000 line of credit, with an 80% advance on eligible A/R and a 40% advance on Inventory, limited to the lesser of $350,000 or 50% of accounts receivable availability.

May 30, 2013

Special Situations• Seasonal Inventory Build Periods‐ May waive or modify Inventory Caps or Limits for a period of time. Always limit to specific amounts and time frames. Do not make the exception the structure.

• Seasonal Extended A/R Terms (Datings, etc)

‐ May waive or modify A/R eligibility for a period of time. Always limit to specific amounts and time frames. Do not make the exception the structure.

May 30, 2013

MODULE 5: Administration of Lines of Credit

May 30, 2013

The Collateral Loan Report is the primary document used to monitor a C&I or ABL Loan.

The quality of information provided in the Collateral Loan Report is critical to the collectability of the loan.

May 30, 2013

The Collateral Loan Report is a reconciliation of all changes to the

Collateral Base; that brings Borrower and Lender up to the present.

May 30, 2013

The Collateral Loan Report Should Reflect:

A) The collateral underlying the Loan at a point in time and

B)What changes have occurred in the collateral base since the last report.

May 30, 2013

The Collateral Loan Report is meaningless without appropriate supporting documentation. The Report should always be supported by the following:

May 30, 2013

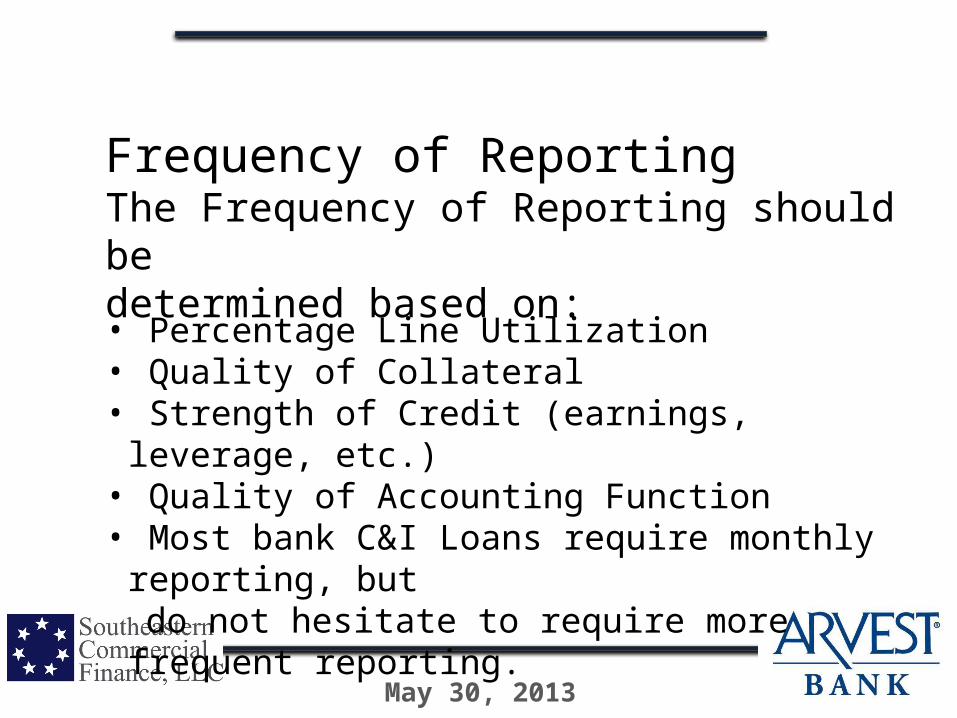

Frequency of ReportingThe Frequency of Reporting should be determined based on:

• Percentage Line Utilization• Quality of Collateral• Strength of Credit (earnings, leverage,

etc.)• Quality of Accounting Function• Most bank C&I Loans require monthly

reporting, but do not hesitate to require more frequent

reporting.

May 30, 2013

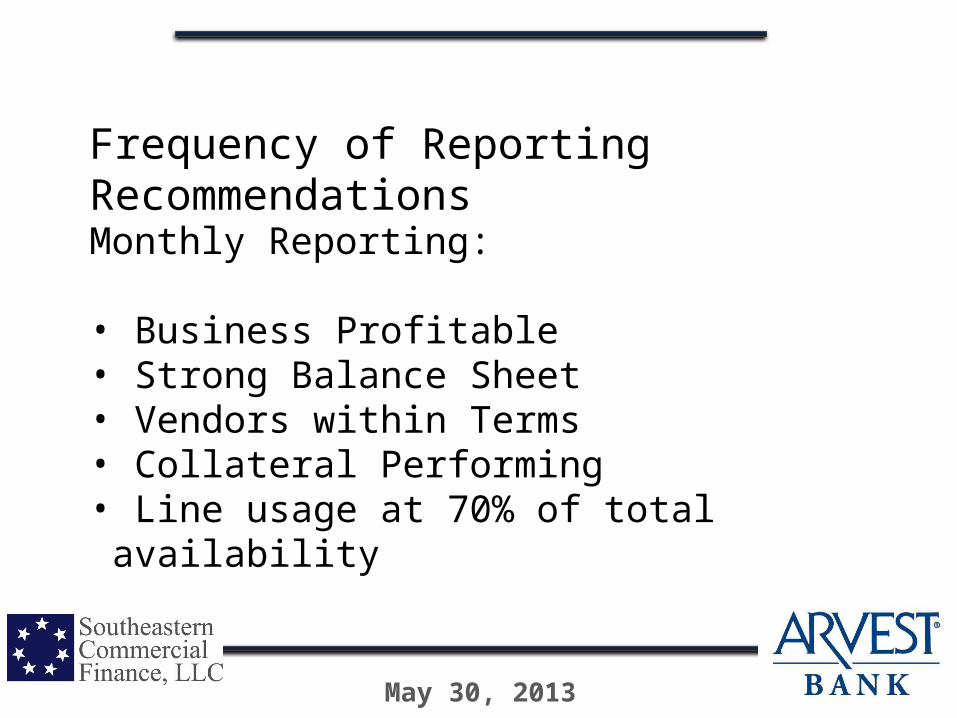

Frequency of Reporting RecommendationsMonthly Reporting: • Business Profitable• Strong Balance Sheet• Vendors within Terms• Collateral Performing• Line usage at 70% of total availability

May 30, 2013

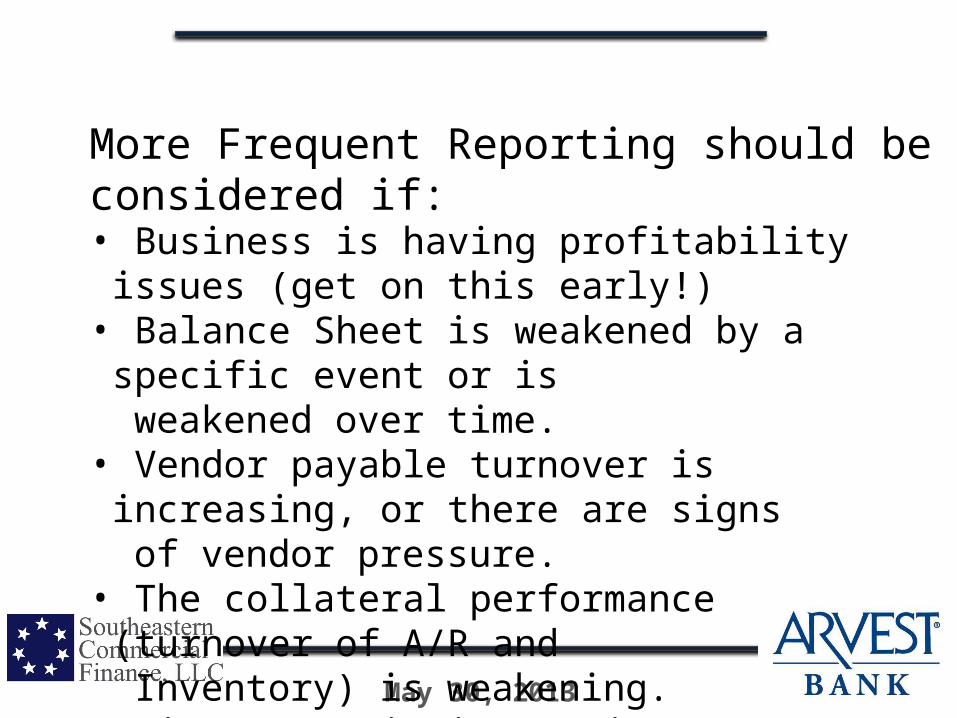

More Frequent Reporting should be considered if:• Business is having profitability issues (get on this early!)• Balance Sheet is weakened by a specific event or is

weakened over time.• Vendor payable turnover is increasing, or there are signs

of vendor pressure.• The collateral performance (turnover of A/R and

Inventory) is weakening.• Line usage is increasing .

May 30, 2013

MODULE 6: Documentation of Lines of Credit: What’s Important/What’s Not

May 30, 2013

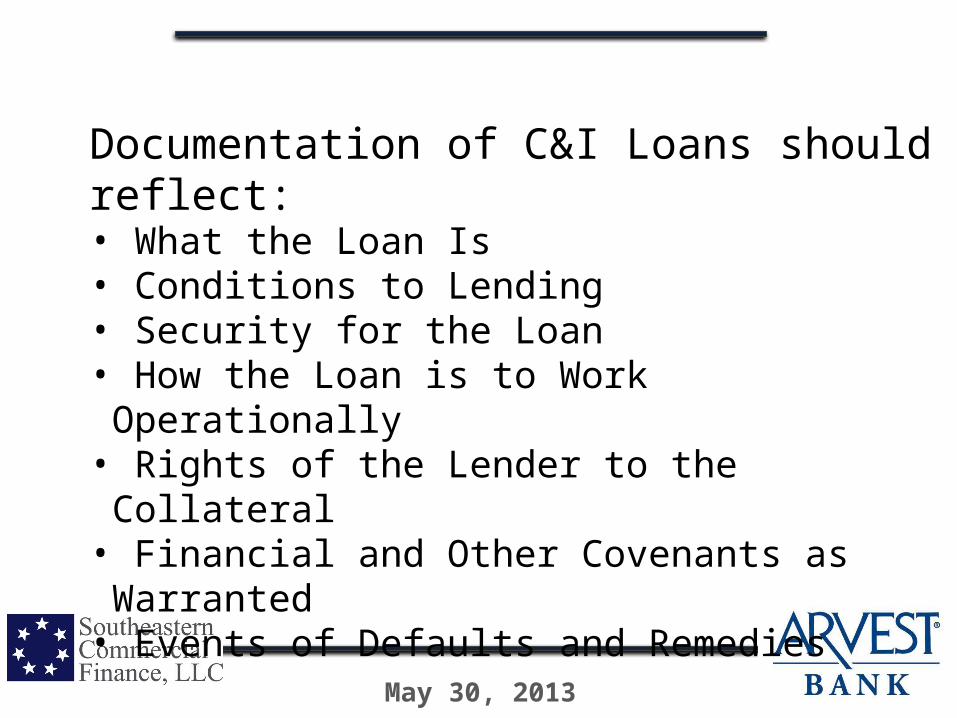

Documentation of C&I Loans should reflect:• What the Loan Is• Conditions to Lending • Security for the Loan• How the Loan is to Work Operationally• Rights of the Lender to the Collateral• Financial and Other Covenants as Warranted• Events of Defaults and Remedies

May 30, 2013

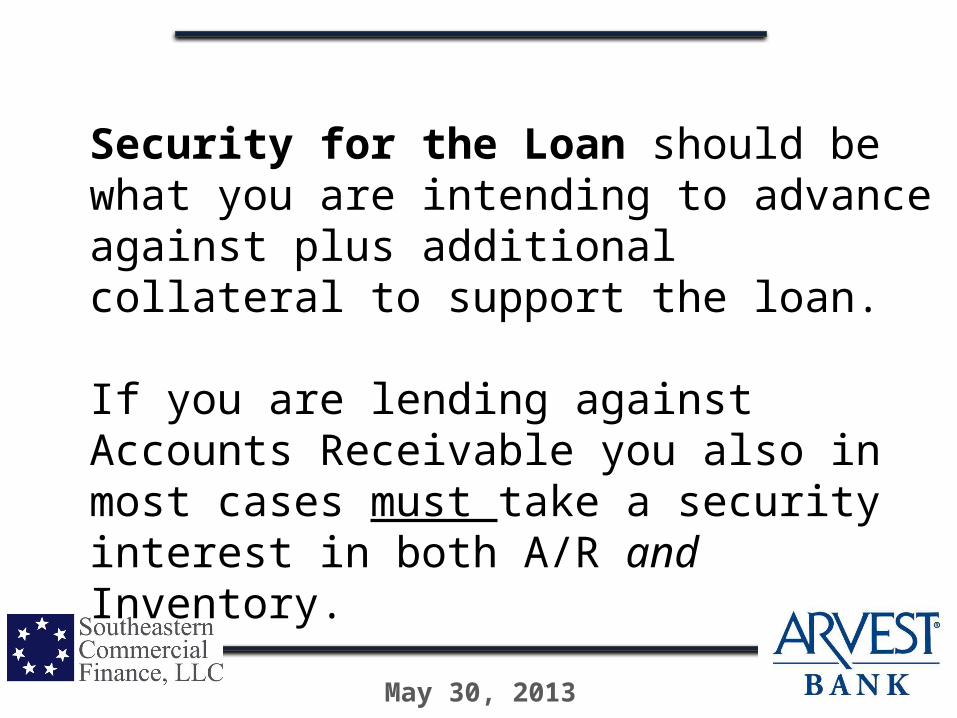

Security for the Loan should be what you are intending to advance against plus additional collateral to support the loan. If you are lending against Accounts Receivable you also in most cases must take a security interest in both A/R and Inventory.

May 30, 2013

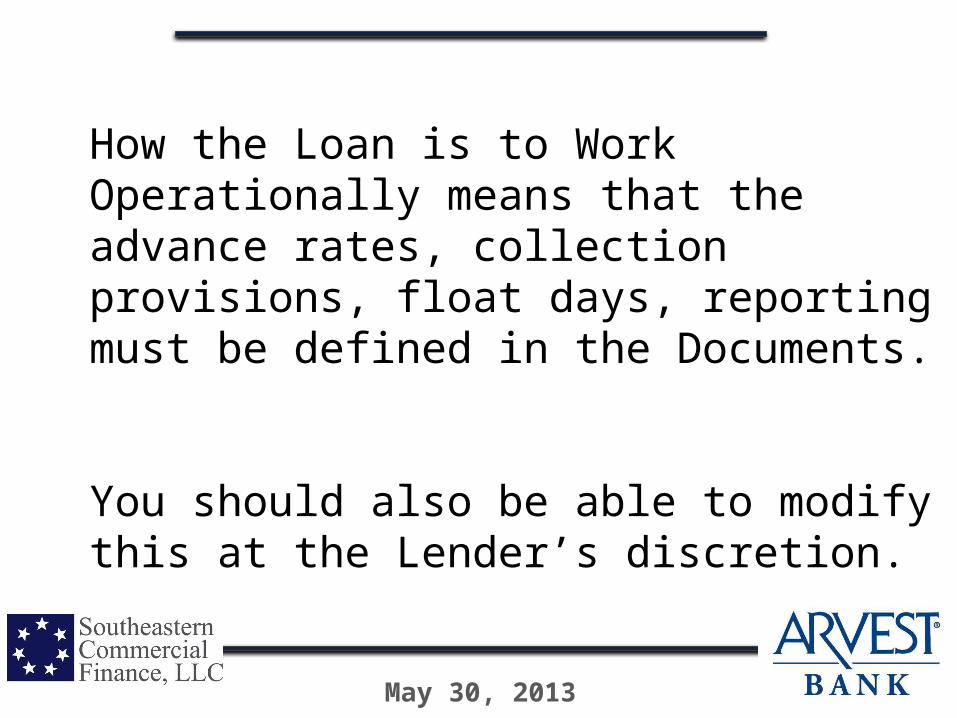

How the Loan is to Work Operationally means that the advance rates, collection provisions, float days, reporting must be defined in the Documents. You should also be able to modify this at the Lender’s discretion.

May 30, 2013

Rights of the Lender to the Collateral – due to the nature of the Collateral for the Loan, the Lender needs rights to inspect, verify, and possess collateral in the event of Lender’s insecurity.

May 30, 2013

Standard Financial Covenants in C&I Lending• Debt to Worth• Fixed Charge Coverage• Limits on additional debt

May 30, 2013

Other Documentation Issues

• Personal Guaranty’s• Validity Guaranty’s• UCC Security Interest Documentation• Treasury Management Documentation• Landlord Lien Waivers