Embed Size (px)

Citation preview

© 2016 IHS

ihs.com

IHS ENERGY

Argentine natural gas markets at regional

inflection point: what’s ahead?

IHS 2016 Argentina Energy Symposium

Buenos Aires, 26 July 2016

Roberto Ferreira da Cunha

Associate Director

IHS Energy

© 2016 IHS 2

Presentation outline

What is the outlook

for Argentine natural

gas supplies from

Vaca Muerta?

What is the price

outlook for LNG over

the coming future?

Will it compete with

Vaca Muerta?

How much gas can

Bolivia export to

Argentina and at

what price?

What is the outlook for

Argentina’s natural gas

demand over the next

20 years?

© 2016 IHS 3

1 - Natural gas demand is set to grow.

What is the outlook for

Argentina’s natural gas

demand over the next

20 years?

© 2016 IHS. ALL RIGHTS RESERVED.

End-user natural gas prices have been regulated at

subsidized levels since the 2000s.

4

-

1

2

3

4

5

6

0

2

4

6

8

10

12

14

16

18

Jan-0

0

Jun-0

0

No

v-0

0

Apr-

01

Sep-0

1

Feb

-02

Jul-0

2

De

c-0

2

Ma

y-0

3

Oct-

03

Ma

r-0

4

Aug-0

4

Jan-0

5

Jun-0

5

No

v-0

5

Apr-

06

Sep-0

6

Feb

-07

Jul-0

7

De

c-0

7

Ma

y-0

8

Oct-

08

Ma

r-0

9

Aug-0

9

Jan-1

0

Jun-1

0

No

v-1

0

Apr-

11

Sep-1

1

Feb

-12

Jul-1

2

De

c-1

2

Ma

y-1

3

Oct-

13

Ma

r-1

4

Aug-1

4

Jan-1

5

Jun-1

5

No

v-1

5

Domestic Supplies Bolivian imports LNG imports Old contracts price Bolivian import price LNG imports price

Historical natural gas supplies and prices

© 2016 IHS

US

$/M

MB

tu

Notes: Old contracts price refer to the legacy contracts prior to the subsidy programs implemented by the Argentine governmentSource: IHS Energy, Ministerio de Energía y Mineria (Argentina)

Bc

f/d

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

As a result, demand has been grown strong. Going

forward, demand would grow 1.7% CAGR over 2016-40.

5

0

20

40

60

80

100

120

2010 2015 2020 2025 2030 2035 2040

Metrogas Camuzzi Gas Pampeana Centro Cuyana Gasnor Ban Camuzzi Gas Del Sur Litoral Gasnea

End-user natural gas demand outlook

Source: IHS Energy, Enargas © 2016 IHS

MM

cm

/d

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Power sector would grow twice as fast at 2.8% CAGR

between 2016-40, mainly led by residential sector.

6

-3%

-2%

0%

2%

3%

5%

6%

8%

9%

11%

12%

14%

15%

0

50

100

150

200

250

300

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037 2039

Industrial Residential Commercial Agricultural Transport Demand growth (%)

Argentina annual power demand by sector

© 2016 IHS

Te

raw

att

-ho

urs

Source: IHS Energy

Dem

an

d g

row

th (

%)

CAGR (%) 2005-15 2015-25 2025-40

Total sales 3.8% 2.3% 2.9%

Industrial 2.2% 1.9% 2.5%

Residential 6.8% 2.8% 3.2%

Commercial 3.0% 2.3% 3.1%

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Additional LNG import capacity to support winter-time

demand peaks will depend on Vaca Muerta build-up.

7

0

20

40

60

80

100

120

140

160

2013 2014 2015 2016 2017 2018 2019 2020 2021

Resid./Comm./Public OtherPower generation(from gas) Power generation(from diesel)

Argentina's seasonal natural gas demand outlook

© 2016 IHS

MM

cm

/d

Source: IHS

0

20

40

60

80

100

120

140

160

2013 2014 2015 2016 2017 2018 2019 2020 2021

Total Supply - low case Total Supply - base case

Potential Demand

Argentina’s seasonal gas supply outlook

© 2016 IHS

MM

cm

/d

Source: IHS

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

2 - Changing landscape for Bolivian gas supplies.

How much gas can

Bolivia export to

Argentina and at

what price?

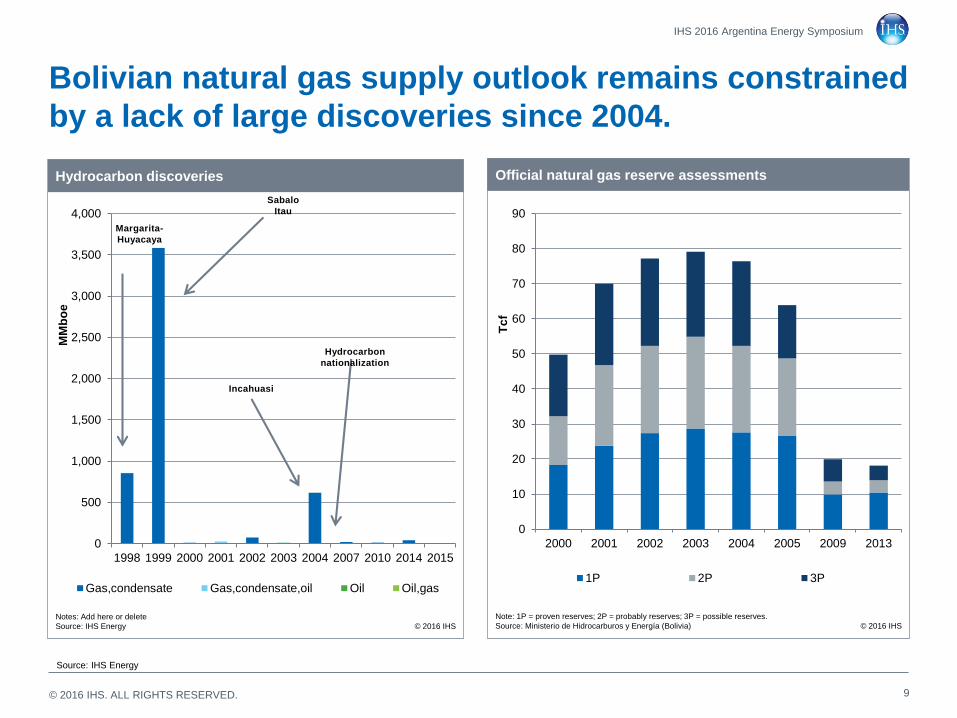

© 2016 IHS. ALL RIGHTS RESERVED. 9

Bolivian natural gas supply outlook remains constrained

by a lack of large discoveries since 2004.

Source: IHS Energy

0

10

20

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2009 2013

1P 2P 3P

Official natural gas reserve assessments

Note: 1P = proven reserves; 2P = probably reserves; 3P = possible reserves.

Source: Ministerio de Hidrocarburos y Energía (Bolivia) © 2016 IHS

Tc

f

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1998 1999 2000 2001 2002 2003 2004 2007 2010 2014 2015

Gas,condensate Gas,condensate,oil Oil Oil,gas

Hydrocarbon discoveries

Notes: Add here or delete

Source: IHS Energy © 2016 IHS

MM

bo

e

Hydrocarbon

nationalization

Sabalo

Itau

Margarita-

Huyacaya

Incahuasi

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED. 10

0

20

40

2000 2003 2006 2009 2012 2015Chapare High and Cambrian Basin Chaco Foothill Belt (Chaco Basin)

Beni Sub-Andean Zone (Beni Basin) Beni Foothill Belt (Beni Basin)

Chaco Sub-basin (Chaco Basin) Chaco Sub-Andean Zone (Chaco Basin)

Number of drilled exploratory wells

Source: IHS Energy, EDIN © 2016 IHS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

NFW sucess rate

© 2016 IHS

Note: Include oil, gas and condensate discoveries

Source: IHS

0

100

200

300

400

500

600

700

800

0 5 10 15 20

Gas recoverable reserve discovery (2P)

© 2016 IHS

MM

Bo

e

Notes: Add here or delete

Source: IHS

7,200 MMBoe per

discovery

10 new exploratory

wells per year

38% success rate

0

2

4

6

8

10

12

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 20262P YTF

9-pt - IHS line chart - 2016

© 2016 IHS

Tcf

Source: IHS Energy

Natural gas reserve outlook (2P)

Central question about Bolivian natural gas supply

outlook remains its “Yet-to-Find” supply outlook.

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED. 11

Bolivian online supplies are likely to peak in 2018,

leaving declining volumes available for exports.

0

10

20

30

40

50

60

70

2010 2015 2020 2025 2030 2035 2040

Total supply (excl. YTF)Domestic demandArgentina SoP+Domestic demandBrazil SoP+Argentina SoP+Domestic demand

Natural gas supply capacity vs existing SoP commitments

© 2016 IHS

MM

cm

/d

Notes: Contractual terms regarding existing long term contracts

Source: IHS Energy, YPFB

Domestic

Demand

Uncontracted

Brazilian

Contract

Argentine

Contract

Uncontracted

0

10

20

30

40

50

60

70

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040

San Alberto Sabalo Margarita-Huacaya Others

Yapacani Vuelta Grande Bulo Bulo Incahuasi

Incahuasi - phase II Rio Grande

Bolivian gross natural gas supply outlook by field (without YTF)

© 2016 IHS

MM

cm

/d

Source: IHS Energy, YPFB

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED. 12

Petrobras could reduce its Bolivian imports, potentially

freeing volumes for increased exports to Argentina.

0

10

20

30

40

50

60

70

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Domestic demand Argentina SoP Brazil SoP Brazil SoP - renewal Net supply

Natural gas supply capacity vs existing SoP commitments

© 2016 IHS

MM

cm

/d

Notes: Contractual terms regarding existing long term contracts

Source: IHS Energy, YPFB

Natural gas supply capacity vs existing SoP commitments (without YTF)

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

3 - Global LNG supply abundance keep spot prices low.

What is the price

outlook for LNG over

the coming future?

© 2016 IHS. ALL RIGHTS RESERVED.

The global LNG market is currently over-supplied due to

new liquefaction capacity and slower demand growth.

14

Key regional trends shaping the LNG market

© 2016 IHS

China slowdown;

strong coal

competition

‘Residual market’

for LNG

Ongoing cost

reductions

LNG imports

for power

Growing LNG

dependenceSupply surge;

CBM uncertainty

Nuclear policy

uncertainty;

solar uptick

East Africa

remains on

starting blocks

Growing gas surplus

capacity Canadian LNG

remains on starting

blocks

Gas Long

Gas Short

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Australia and US set to increase liquefaction capacity by

almost 50%, despite lagging LNG demand growth.

15

-10

0

10

20

30

40

2015 2016 2017 2018 2019 2020 2021

US Australia Other Pacific

Other Atlantic Middle East Southeast Asia

Africa

Incremental liquefaction capacity additions

Note: MMt = Million metric tons of LNG

Source: IHS © 2016 IHS

MM

t

-15

-10

-5

0

5

10

15

20

25

30

35

40

2015 2016 2017 2018 2019 2020 2021

Other Other Asia MENA

South America North America Europe

JKT

Incremental LNG demand

Note: MMt = Million metric tons of LNG

Source: IHS © 2016 IHS

MM

t

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Excess capacity will pressure LNG spot prices over the

next 5 years, favoring LNG imports in Argentina.

16

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

ARA Brent Asia spot price Japan LNG term average Henry Hub NBP

Global energy and LNG prices

Note: MMBtu = Million British thermal units. ARA coal price has been heat-rate adjusted to gas plant efficiency equivalence.

Source: IHS © 2016 IHS

$/M

MB

tu

Asian-European spot

price differential to

erode as LNG trade

optimizes

Asia contract prices to

rebound with modest

oil price recovery

NBP will face

pressure as Europe

becomes LNG market

of last resort; but coal

provides a floor

Low-cost resource

base to hold down

Henry Hub

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

On the long term, a recovery of the UK’s NBP prices

would keep prices to Argentina above US$10/MMBtu.

17

IHS 2016 Argentina Energy Symposium

0

5

10

15

20

25

Jan-08 Jan-11 Jan-14 Jan-17 Jan-20 Jan-23 Jan-26 Jan-29 Jan-32 Jan-35 Jan-38

NBP Netback Shipping Regas Historical Cargoes Quintero terminal(Chile)

LNG spot prices have a floor given by NBP netback estimates

© 2016 IHS

Real (2

016)

US

$/M

Mb

tu

Notes: Shipping estimates take Trinidad & Tobago as reference point.

Source: IHS Energy with data from Aliceweb

© 2016 IHS. ALL RIGHTS RESERVED.

4 – Pricing policies are key sign-post for Vaca Muerta.

What is the outlook

for Argentine natural

gas supplies from

Vaca Muerta?

© 2016 IHS. ALL RIGHTS RESERVED.

Macri’s election improves the long term investment

potential of Vaca Muerta, but how much?

19

0

50

100

150

200

250

2000 2005 2010 2015 2020 2025 2030 2035 2040

Incremental - High case Incremental - Base case Unconventional supplies - Low caseConventional + Tight Reference Demand

Argentina - Illustrative natural gas deficit scenarios under Argentina supply cases

Source: IHS EnergyNotes: Demand outlook assuming all flexible generation from oil derived fuels takes place with natural gas.

© 2016 IHS

MM

cm

/d

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Gas pricing policies are the key sign-post to investment

attractiveness, but political challenges remain.

20

0

2

4

6

8

10

12

14

16

18

20

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Jan-1

2

Ap

r-1

2

Ju

l-1

2

Oct-

12

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oct-

13

Ja

n-1

4

Ap

r-1

4

Jul-1

4

Oct-

14

Ja

n-1

5

Ap

r-1

5

Ju

l-1

5

Oct-

15

Old contracts price Bolivian import price LNG imports price Gas Plus Program price

Gas Plus program in place since 2008

© 2016 IHS

US

$/M

MB

tu

Source: IHS Energy, Ministerio de Energía y Mineria (Argentina)

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Vaca Muerta wellhead price is likely to remain cheaper

than LNG and more expensive than Bolivian imports.

21

0

2

4

6

8

10

12

14

16

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

Escob

ar

Ch

ile H

H Q

T

GS

A B

O-B

R

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Wellhead price US LNG NBP netback - Escobar Shipping Regas Transportation Premium

Natural gas import parity price (Real US$ 2015)

Note: Assumes premium of US$ 4/MMBtu; Assumes Escobar LNG spot imports from Trinidad and Tobago.

Source: IHS © 2016 IHS

MM

cm

/d

IHS 2016 Argentina Energy Symposium

© 2016 IHS. ALL RIGHTS RESERVED.

Base case would reduce deficit to 0.95 Bcfd by 2030 and

0.46 Bcfd by 2040, limiting demand for imports.

22

IHS 2016 Argentina Energy Symposium

0

50

100

150

200

250

2000 2005 2010 2015 2020 2025 2030 2035 2040

Post 2027 Supply Deficit LNG Bolivian Contract (DCQ)Unconventional - Base Case Conventional + Tight Reference Demand*

Argentina - Illustrative natural gas deficit scenario under Base Case

Source: IHS EnergyNotes: Demand outlook assuming all diesel-gas flexible generation takes place with natural gas.

© 2016 IHS

MM

cm

/d

© 2016 IHS. ALL RIGHTS RESERVED.

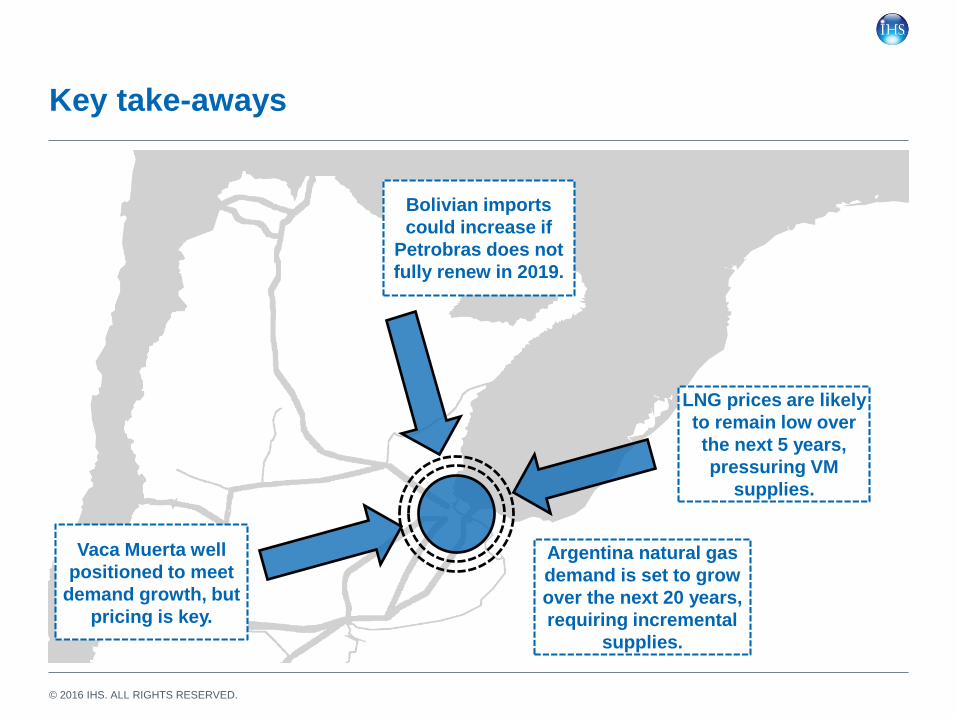

Key take-aways

Vaca Muerta well

positioned to meet

demand growth, but

pricing is key.

LNG prices are likely

to remain low over

the next 5 years,

pressuring VM

supplies.

Bolivian imports

could increase if

Petrobras does not

fully renew in 2019.

Argentina natural gas

demand is set to grow

over the next 20 years,

requiring incremental

supplies.

IHSTM ENERGY

COPYRIGHT NOTICE AND DISCLAIMER © 2016 IHS. For internal use of IHS clients only.

No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content

reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the

opinions and analyses that are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular,

please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events

and results may differ materially from forecasts and statements of belief noted herein. This report is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at client’s own risk. IHS and the

IHS logo are trademarks of IHS.

IHS Customer Care:

Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected]

Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected]

Asia and the Pacific Rim: +604 291 3600; [email protected]