Embed Size (px)

Citation preview

Digging deeper

Prepared for:

Global Iron Ore & Steel ConferenceMarch 2016

Adrian DoyleSenior Consultant – Iron Ore Costs

2

• Recap of 2014 & 2015

• Key changes in 2015: macro factors, productivity and marketing

• What does the outlook for iron ore costs look like

• Conclusions

Agenda

The key themes from 2014 and 2015

A large amount of production was required to exit to

balance the market in 2014 and 2015

4

Additional supply, demand changes and displacement requirements for 2014 and 2015, Mt

195

3513

217

0

50

100

150

200

250

Supply from estabished producers Demand changes Displacement requirements

Australia

Data: CRU

Brazil

The majority of this displacement was fulfilled from non-

traditional exporters, China and other markets

31 Mt15 Mt

10 Mt

20 Mt

2 Mt

100 Mt

2014 and 2015 supply exits, Mt

23 Mt

15 Mt

5

Cost reductions in 2015:

macro vs productivity

7

The majors all posted strong cost reductions in 2015…

Indexed FOB cash costs, $/t (dry), 2014=100

40

60

80

100

120

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015

FMG Rio Tinto BHP Billiton Vale

Data: CRU, Company reports

-38%

-23%

-31%

-35%

8

…but in each case these were eclipsed by the decline in the

iron ore priceIndexed 62% fines price, $/t (dry), 2014=100

40

60

80

100

120

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015

Data: CRU, Company reports

-43%

Lower oil prices have provided assistance to these cost

reductions

9

Oil price scenario analysis, index $100/bbl oil = 100, Australian mines

45 41

2320

22

13

10

11

0

10

20

30

40

50

60

70

80

90

100

$100/bbl $30/bbl

Other Freight Transportation Mining

Data: CRU Iron Ore Cost Model

0

10

20

30

40

50

60

70

2014 Q4 2015 Q3 2015 Q4

Other costs Freight costs Cash costs, FOB

Data: Vale Day London 2015

56.5 32.4 31.2

10

Vale achieved a staggering 45% y/y reduction in delivered

costs...Vale's cash cost landed China, $/t dry

0

10

20

30

40

50

60

70

2014 Q4 2015 Q3 2015 Q4

Other costs Freight costs Cash costs, FOB

Data: Vale Day London 2015

21.7

16.4 14.3

11

…although macroeconomic factors helped. Freight costs

to China fell 35%, or by over $7 /tVale's cash cost landed China, $/t dry

0

10

20

30

40

50

60

70

2014 Q4 2015 Q3 2015 Q4

Data: Vale Day London 2015

48.0 36.3 34.1

12

… while FOB cash costs in local currency fell by 29%,

indicating that this wasn’t purely driven by macro factorsVale's FOB cash cost, adjusted for quality, BRL/t dry

0

10

20

30

40

50

60

70

80

2014 2014 2014 2014 2015 2015 2015 2015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Cash costs, FOB, USD

Cash costs, FOB, AUD

Data: FMG company reports, CRU estimatesData: FMG company reports, CRU estimates

FMG’s results paint a similar picture of cost reductions,

with the AUD assisting pure productivity gains

13

-37%

-51%

FMG's FOB cash cost, $/t dry

14

0

10

20

30

40

50

60

70

80

2014 2014 2014 2014 2015 2015 2015 2015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Normalisation to 62% price

Cash costs + freight + royalty + admin

Cash costs, FOB

Data: FMG company reports, CRU estimates

FMG's FOB cash costs, CFR costs and breakeven cost, $/t dry

FMG’s results paint a similar picture of cost reductions,

with the AUD assisting pure productivity gains

The Australian juniors have also continued to lower costs

into the last quarterBenchmark breakeven price, Australian mid-tiers, CFR China, $/dry t.

Left estimate: 2015 Q3. Right estimate: 2015 Q4

15

0

10

20

30

40

50

60

70

80

Arrium Atlas Iron Cliffs Gindalbie Grange Resources

Mineral Resources

Mount Gibson

+1% -18%-15%-8%-9%-7%-6%

Data: CRU estimate, including sustaining capital, royalties and corporate costs

Looking ahead: market dynamics

-88

-129

-46 -47

-12-16

-8

2014 2015 2016 2017 2018 2019 2020

Displacement requirements, while below the levels in 2014

& 2015, are still significant

17

Data: CRU.

Displacement needed to balance market, Mt

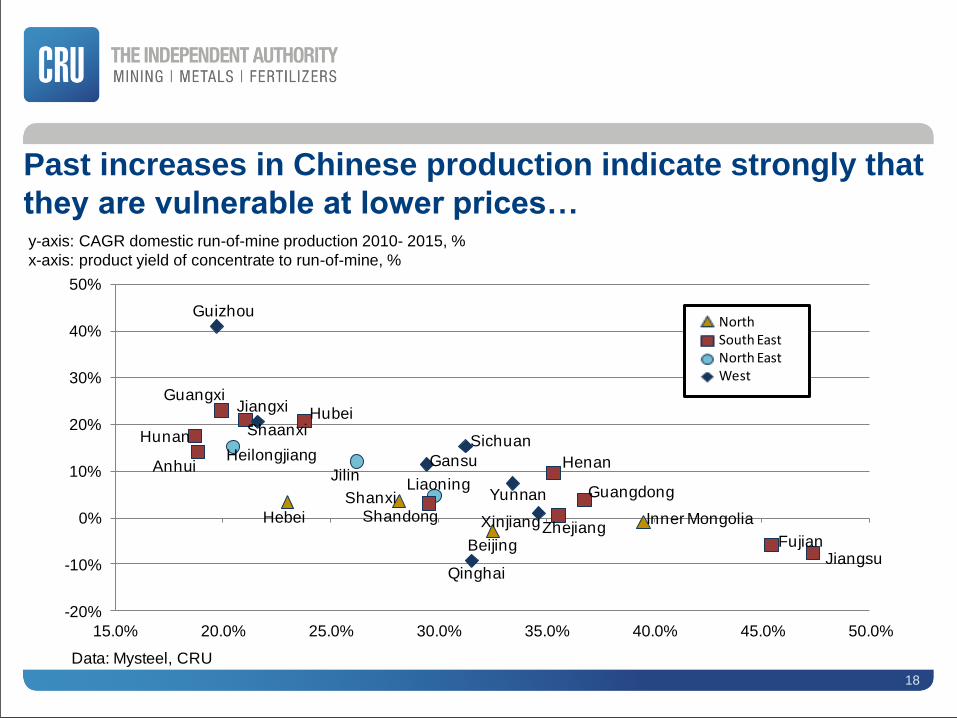

18

Beijing

Hebei Inner Mongolia

Shanxi

Heilongjiang

JilinLiaoning

Anhui

Fujian

Guangdong

Guangxi

Henan

Hubei

Hunan

Jiangsu

Jiangxi

ShandongZhejiang

Gansu

Guizhou

Qinghai

ShaanxiSichuan

Xinjiang

Yunnan

-20%

-10%

0%

10%

20%

30%

40%

50%

15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0%

NorthSouth EastNorth EastWest

Data: Mysteel, CRU

Past increases in Chinese production indicate strongly that

they are vulnerable at lower prices…y-axis: CAGR domestic run-of-mine production 2010- 2015, %

x-axis: product yield of concentrate to run-of-mine, %

…with large amounts of high-cost ore being situated in

range of low-cost imports

0. 0

20. 0

40. 0

60. 0

80. 0

100. 0

120. 0

140. 0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2014 2015 2016

GansuSha’anxi

Guizhou

Guangxi

HunanJiangxi

AnhuiHubei

HEBEI

Jilin

Heilongjiang

19

20

We expect further reductions. However, a solid core of

production will remainy-axis: Supply of iron ore to Chinese steel market, 2017, Mt

x-axis: 62% fines price, CFR China, $/t

0

200

400

600

800

1000

1200

20253035404550556065707580

Imported ore Domestic - Southeast Domestic - Northeast Domestic - North Domestic - West

Data: CRU

How will macroeconomic factors

change looking ahead

22

After a volatile 2015, we expect major commodity currencies to

begin to level off from this yearSelected currencies against US dollar, index 2014=100

0

20

40

60

80

100

120

140

160

180

200

2013 2014 2015 2016 2017 2018 2019 2020

AUD BRL CNY EUR RUB UAH

Data: CRU

23

Oil and freight will provide start to stretch the cost curve

LHS: Brent oil price, $/bbl

RHS: Capesize time charter rate, $’000/day

Modelled freight differential, Australia to

China & Brazil to China, $/t

0

10

20

30

40

50

60

0

20

40

60

80

100

120

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Brent oil Capesize charter rate

Data: CRU

0

2

4

6

8

10

12

14

16

18

20

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Data: CRU

The road ahead

24

Effect on costs/prices

Factor 2014-2015 2016-2020 Long-term

Supply additions FMG,AA,RTIO Roy Hill, S11D Uncertain

Oil Fall below $50/bbl $80/bbl by 2020 Recovery to $100/bbl

Freight Collapse in freight

rates

Sharp recovery Further steady

recovery

FOREX Widespread

depreciation

Stabilisation in most

currencies

Stabilisation in most

currencies

Demand Demand correction

in China

Demand stabilisation Long-term demand

story remains

Productivity Price falls drive

gains

Price pressure to

drive further increases

Price pressure to

unwind

Steel profitability Collapse in Chinese

steelmakers’ profit

Increasing from low

base

Continuing increase

Negative No change Positive

25

• 2014 & 2015 saw large displacement requirements mostly met through a

combination of exits from China, non-traditional exporters and existing

producers.

• Cost reductions were impressive throughout 2015 across the cost curve, driven

by productivity improvements and macroeconomic factors. The majority of

these cuts are sustainable. These led to a lower and flatter cost curve.

• We require further displacement from a much more resilient set of producers in

2016 and 2017. Market dynamics are ugly for these years.

• However, macroeconomic factors and an anticipated improvement in steel

industry conditions will raise and stretch the cost curve, leading to increased

profitability.

Adrian Doyle

Senior Consultant, Iron Ore Costs

T: +61 2 8412 2807

CRU International (Australia) Pty

71 Walker Street

North Sydney, 2060

NSW

Please address any questions or comments relating to this

presentation to:

Philip Sewell

Business Development Manager

T: +61 2 9387 8842

Alex Tonks

Managing Consultant, CRU Consulting

T: +61 2 8412 2801