Embed Size (px)

Citation preview

MARKET UPDATE – Singapore July 30th, 2015

Offshore Iron ore Derivatives Volumes Hit Key Milestone

Singapore Exchange (SGX) and the CME Group together cleared over 118 million tonnes of iron ore

swaps, options and futures by the 29th of July. SGX had cleared over 105 million tonnes, making it

the highest trading volume month on record for the Asia-based bourse. This record volume was

recorded in a month which saw significant price volatility for this key steelmaking raw material (see

recent notes on the topic here).

Iron ore derivatives were introduced by the Singapore Exchange in April 2009 and the contracts

have seen rapid uptake and continual growth in annual volumes traded during every calendar year.

It was only by January of this year that Open Interest at the Singapore Exchange breached the 100

million tonne mark for the first time.

By July 29th, SGX had cleared over 105.7 million tonnes, whilst CME had cleared 12.8 million tonnes

of swaps, options and futures. Their combined volume (exceeding 118.5 million tonnes) is

significant as it annualizes to a figure in excess of 1.4 billion tonnes, which is the approximate size of

the physical global seaborne iron ore market. Many commodities markets see traded derivatives

volumes many multiples of the size of the physical market, reflecting the number of times that

material changes hands, as well as downstream or adjacent market exposure to the commodity

being traded.

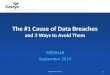

Open interest at SGX on the 29th was over 172 million tonnes, though this typically wanes towards

month-end as positions close out.

0

20

40

60

80

100

120

140

160

180

0

10

20

30

40

50

60

70

80

90

100

110

120

Options

Futures

Swaps

SGX Open Interest (RHS)**

* Total volume cleared by SGX, CME Group, LCH.Clearnet, NASDAQ OMX and ICE; Open interest for SGX only; Jul-15 values preliminary (MTD)

Iron Ore Futures and OTC Derivatives Contracts - Volume Cleared and Open Interest* (million tonnes)

**End of month, except Jul-15 (MTD)

Option futures stand out as the fastest growing part of SGX’s total volumes, having more than

doubled since January (they were only introduced in August 2014). 12 months after launch,

volumes are already rivalling those of swaps – the original instrument launched in 2009.

The exchange, which uses The Steel Index (TSI) price benchmark for 62% Fe iron ore fines shipped

to China for cash settlement of its iron ore contracts, serves as the leading venue for price risk

management for the global iron ore market. Since launch in 2009, the volume of derivatives traded

on SGX and other offshore exchanges entering the market in later years, including the CME Group,

has more than doubled annually. In 2014, almost 600 million tonnes of swaps, options and futures

were cleared globally, equivalent to almost half of all seaborne physical trade worldwide, and two-

thirds of Chinese imports.

“The growing utility of iron ore derivative contracts is a boon to physical actor’s ability to hedge

against price volatility for traded cargoes, stock inventory and guard against price erosion for

finished steel products” says Tim Hard, TSI Director in Singapore. “However, for the larger ferrous

industry to benefit across-the-board, it is crucial that both coking coal and finished steel derivative

markets grow in tandem with those of iron ore. Liquid markets for these products will provide the

flexibility for steelmakers to properly hedge margins as the global steel industry is entering an

uncertain period of shake-out, restructuring and consolidation”.

Miners and hedging

During July’s torrid price movements, one Australian iron ore miner explicitly revealed their ongoing

options hedging strategy in an investor note. During the commodity supercycle of recent years,

miners have maintained a corporate position of being ‘unhedged’, in order to provide shareholders

with direct exposure to commodity price movements. But with prices now falling amid oversupply,

bringing spot prices closer to breakeven levels for some miners, and hedging strategies are now

increasingly important – not just for the producers, but also banks financing them.

With derivatives volumes rising so that the physical market can be hedged tonne for tonne, it will

be interesting to see whether hedging moves beyond a strategy primarily employed by traders and

end-users. If it does, there is an opportunity for basis risk to be negated along the supply-chain.

International traders and Chinese steel mills have been increasingly vocal in asking for TSI-linked

physical supply contracts in recent months.

Ends

For further information

Please contact: Tim Hard (Singapore) [email protected]

Oscar Tarneberg (Shanghai) [email protected]

Note to Editors:

The Steel Index (TSI) is a leading specialist source of impartial steel, scrap, iron ore and coking coal price information based on

spot market transactions.

Transaction price data is submitted confidentially to TSI on-line by companies buying and selling a range of relevant steel, iron

ore, scrap, coking coal products. TSI’s index reference prices are then calculated using transparent and verifiable procedures

which are fully aligned with IOSCO principles.

TSI’s iron ore price indices are published daily at 19:00 Singapore/Shanghai time (11:00 GMT) and coking coal price indices daily

at 18:30 Singapore/Shanghai time (10:30 GMT). Steel prices for Northern Europe, Southern Europe and US HRC are published

daily at 14:00 UK time and for ASEAN HRC imports daily at 18:30 Singapore time. Scrap prices for Turkish imports are published

daily at 13:30 UK time. Weekly steel and scrap price indices are published every Monday and Friday respectively, with each price

representing the average transaction price for the previous calendar week.

TSI’s indices are widely used by steel mills, miners, traders, distributors and manufacturing companies worldwide as the basis for

their physical pricing arrangements. TSI’s indices are also used as the industry standard in the settlement of ferrous financ ial

contracts.

Singapore Exchange (SGX), LCH.Clearnet (London), CME Group (Chicago), NASDAQ OMX Clearing (Oslo) and Intercontinental

Exchange (ICE) all use TSI’s iron ore index for settling their monthly cleared iron ore financial contracts. SGX also uses TSI’s

coking coal indices and hot rolled coil index for ASEAN imports to settle its coking coal and Asian HRC steel futures and swap

contracts respectively. In addition, TSI’s prices are used for the settlement of European hot rolled coil steel contracts on

LCH.Clearnet and CME Clearing Europe and for the settlement of Turkish scrap imports contracts on LCH.Clearnet, CME Europe

and Borsa Istanbul. In all cases, settlement prices are the average of TSI’s reference prices published in the expiring month.

TSI is a Platts business, part of McGraw Hill Financial. Further information on TSI, including a free trial of the service, is available

at http://www.thesteelindex.com.

Platts, founded in 1909, is a leading global provider of energy, petrochemicals, metals and agriculture information and a premier

source of benchmark prices for the physical and futures markets. Platts' news, pricing, analytics, commentary

and conferences help customers make better-informed trading and business decisions and help the markets operate with greater

transparency and efficiency. Customers in more than 150 countries benefit from Platts’ coverage of the biofuels, carbon

emissions, coal, electricity, oil, natural gas, metals, nuclear power, petrochemical, shipping and sugar markets. A division of

McGraw Hill Financial (NYSE: MHFI), Platts is based in London with more than 1000 employees in more than 15 offices

worldwide. Additional information is available at http://www.platts.com.

This information has been prepared by The Steel Index ("TSI"). Use of the information presented here is at your sole risk, and any

content, material and/or data presented or otherwise obtained through your use of the information in this document is at your own

discretion and risk and you will be solely responsible for any damage to you personally or your company or organisation or

business associates whatsoever which in anyway results from the use, reliance or application of such content material and/or

information. Certain data has been obtained from various sources (listed on the final page) and any copyright existing in such

data shall remain the property of the source. Except for the foregoing, TSI retains all copyright within this document. The copying

or redistribution of any part of this document without the express written authority of TSI is forbidden.