Embed Size (px)

Citation preview

Corporate Governance Training for Directors

Anar Aliyev

Operations Officers

IFC Mongolia Corporate Governance Project

April 27, 2012

Corporate governance involves a set of relationships between a company’s management, its board, its shareholders and other stakeholders. Corporate governance also provides the structure through which the objectives of the company are set, and the means of attaining those objectives and monitoring performance are determined.

The OECD Principles of Corporate GovernanceParis, France, 2004

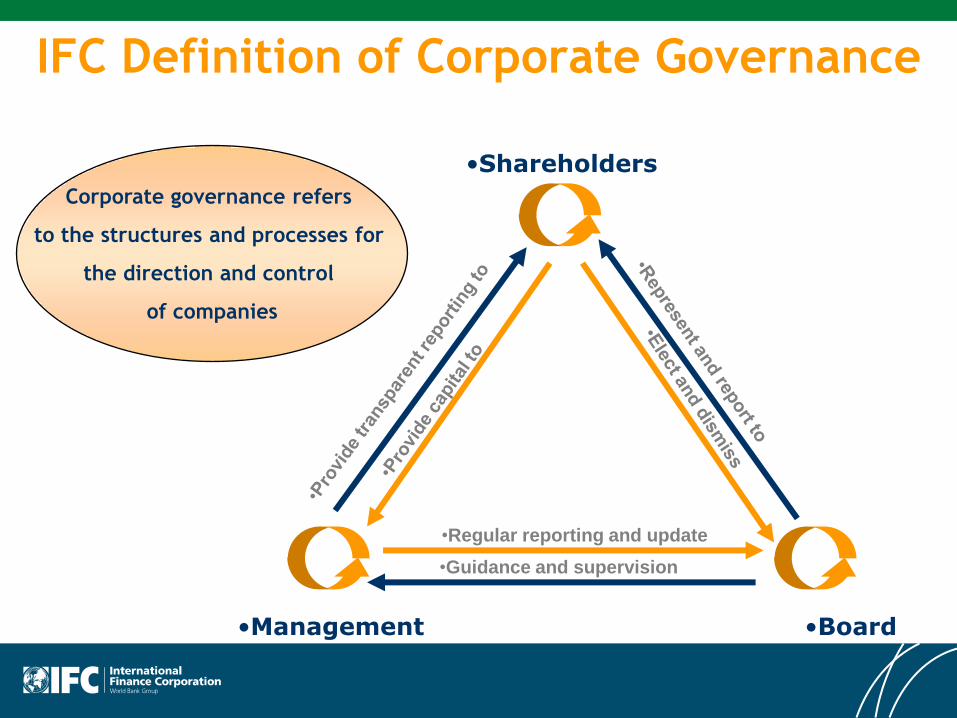

Corporate Governance Defined

Corporate governance refers

to the structures and processes for

the direction and control

of companies

•Shareholders

•Board•Management

•Regular reporting and update

•Guidance and supervision

IFC Definition of Corporate Governance

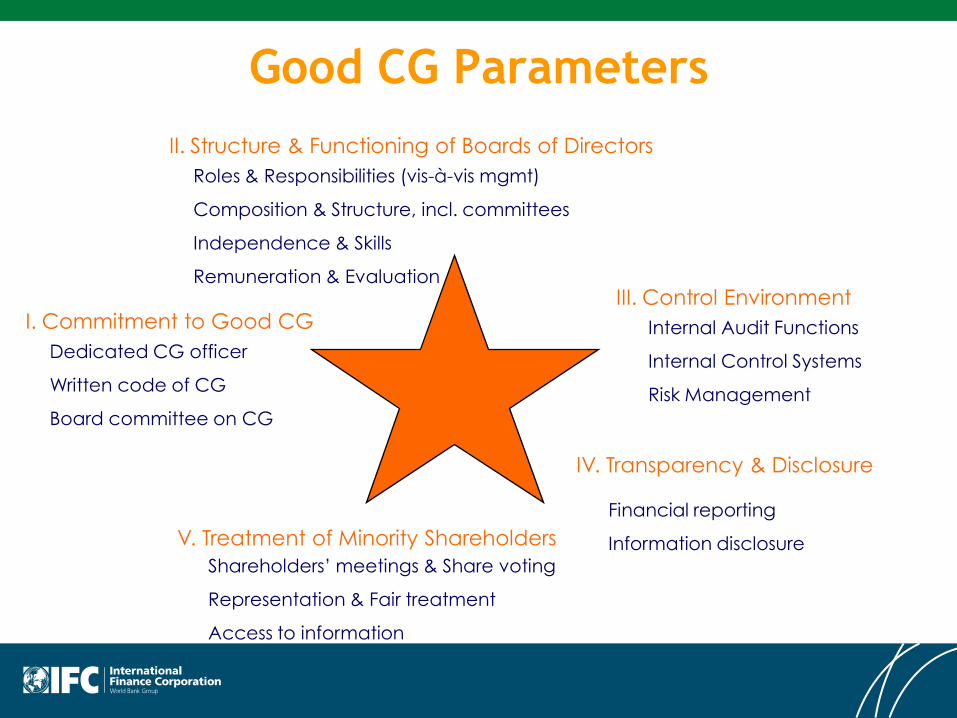

Good CG Parameters

II. Structure & Functioning of Boards of Directors

IV. Transparency & Disclosure

V. Treatment of Minority Shareholders

I. Commitment to Good CG

Roles & Responsibilities (vis-à-vis mgmt)

Composition & Structure, incl. committees

Independence & Skills

Remuneration & Evaluation

Dedicated CG officer

Written code of CG

Board committee on CG

Financial reporting

Information disclosure Shareholders’ meetings & Share voting

Representation & Fair treatment

Access to information

III. Control Environment

• Internal Audit Functions

• Internal Control Systems

• Risk Management

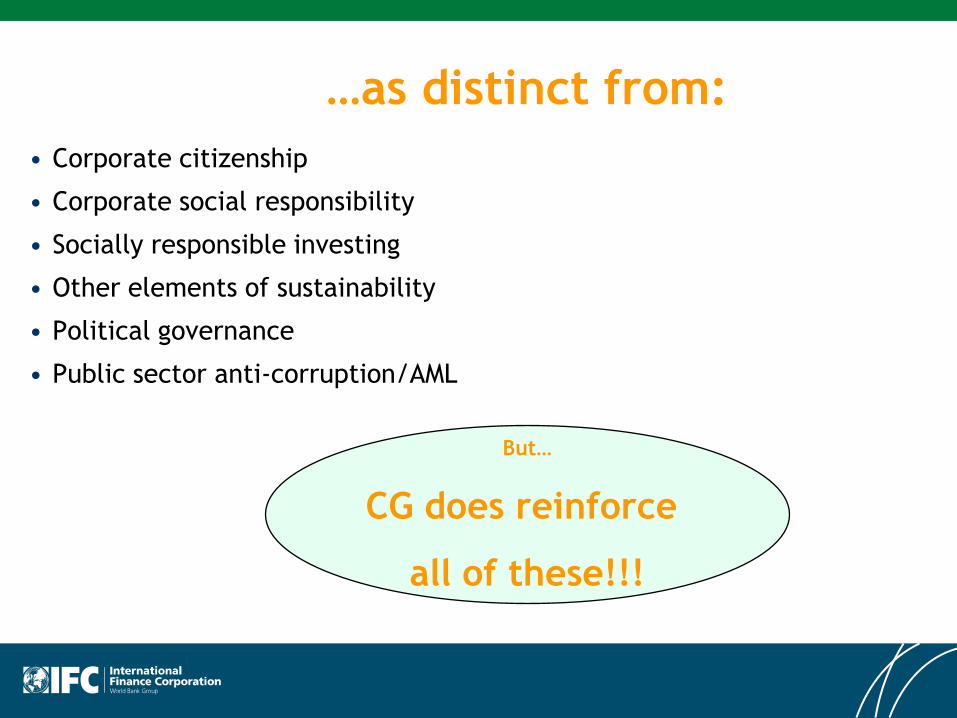

But…

CG does reinforce

all of these!!!

…as distinct from:

• Corporate citizenship

• Corporate social responsibility

• Socially responsible investing

• Other elements of sustainability

• Political governance

• Public sector anti-corruption/AML

Why Do Investors Care About CG?

• Portfolio performance

• Development mission

• Reputational risk / reputational agent

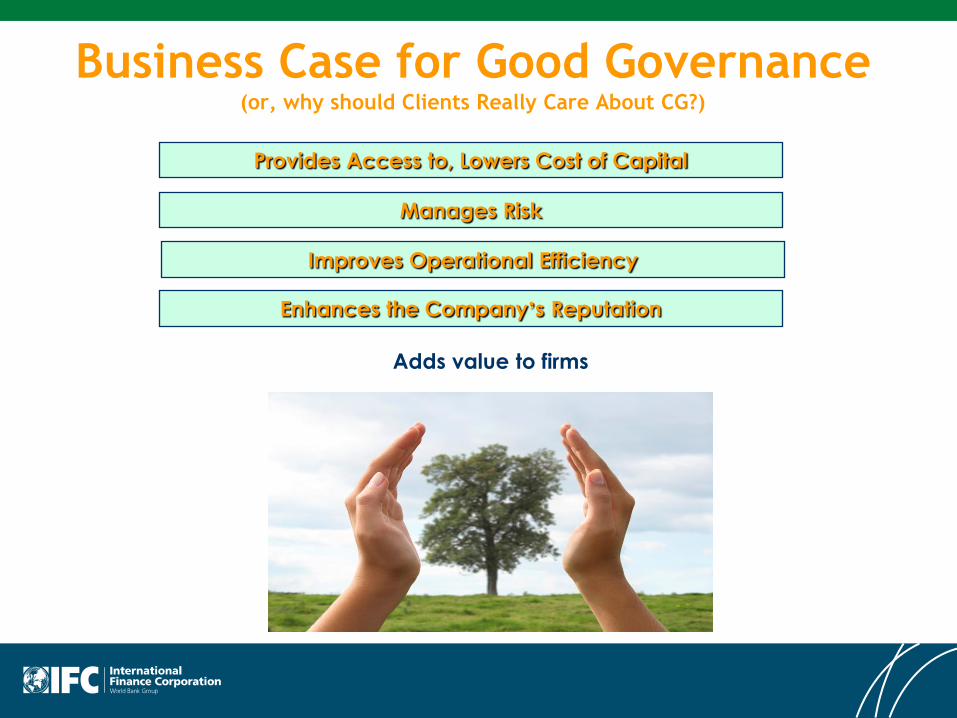

Business Case for Good Governance (or, why should Clients Really Care About CG?)

Manages Risk

Enhances the Company’s Reputation

Provides Access to, Lowers Cost of Capital

Adds value to firms

Improves Operational Efficiency

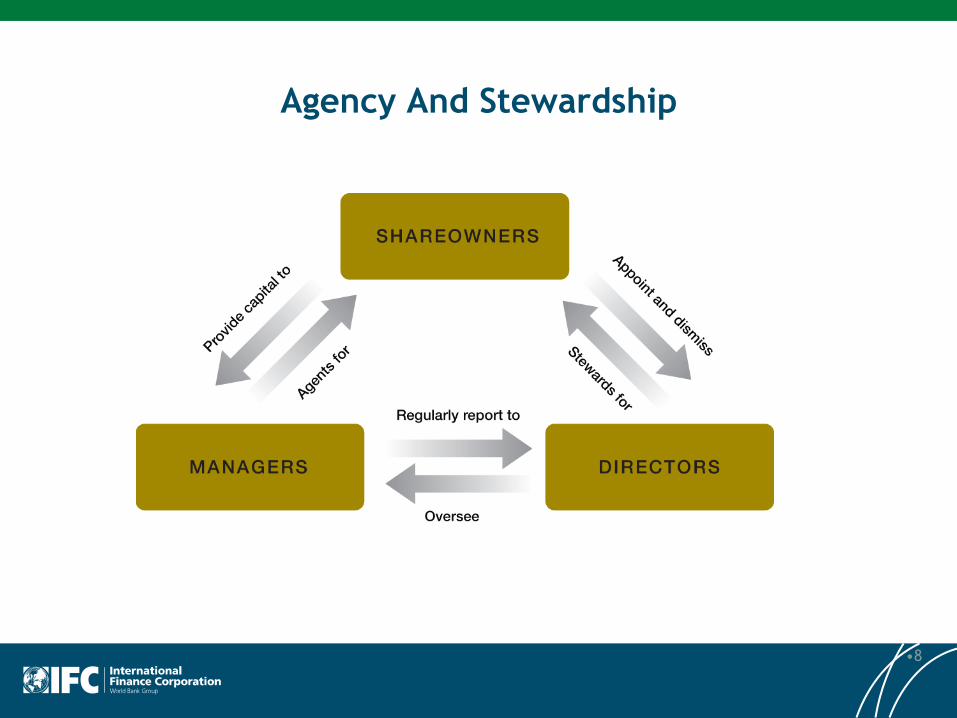

Agency And Stewardship

•8

•9

Corporate Governance System

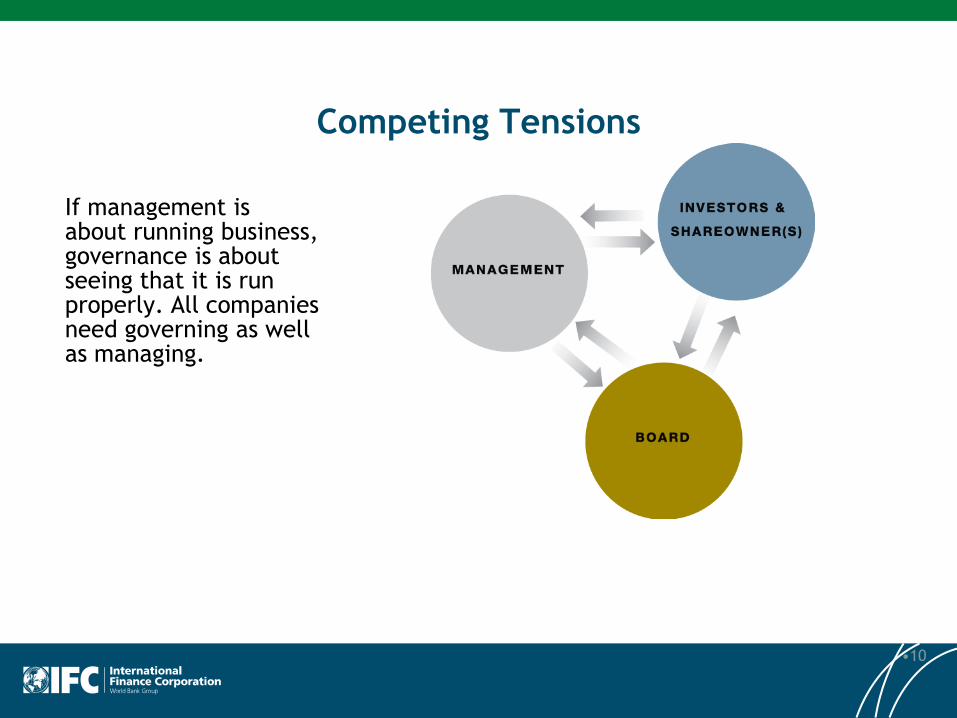

Competing Tensions

If management is about running business, governance is about seeing that it is run properly. All companies need governing as well as managing.

•10

‘Foundation of Reform’

“I see corporate governance as a foundation of reform which strengthens and modernizes an economy.…”

“Without corporate governance reforms, the alternatives would be monopolies….”

“The corporation must be a separate, autonomous legal personality with rights, duties, and responsibilities.”

Jesus P. Estanislao, President, Founder

Institute for Corporate Directors in the Philippines

•11

Strong commitment to corporate governance reforms

•G

ood b

oard

pra

cti

ces

•A

ppro

pri

ate

contr

ol

envir

onm

ent

and p

rocess

es

•Str

ong r

egim

e o

f

•dis

clo

sure

and t

ransp

are

ncy

•Pro

tecti

on o

f (m

inori

ty)

share

ow

ner

rights

•The five key elements of

good corporate governance

Five Elements of Corporate Governance

•12

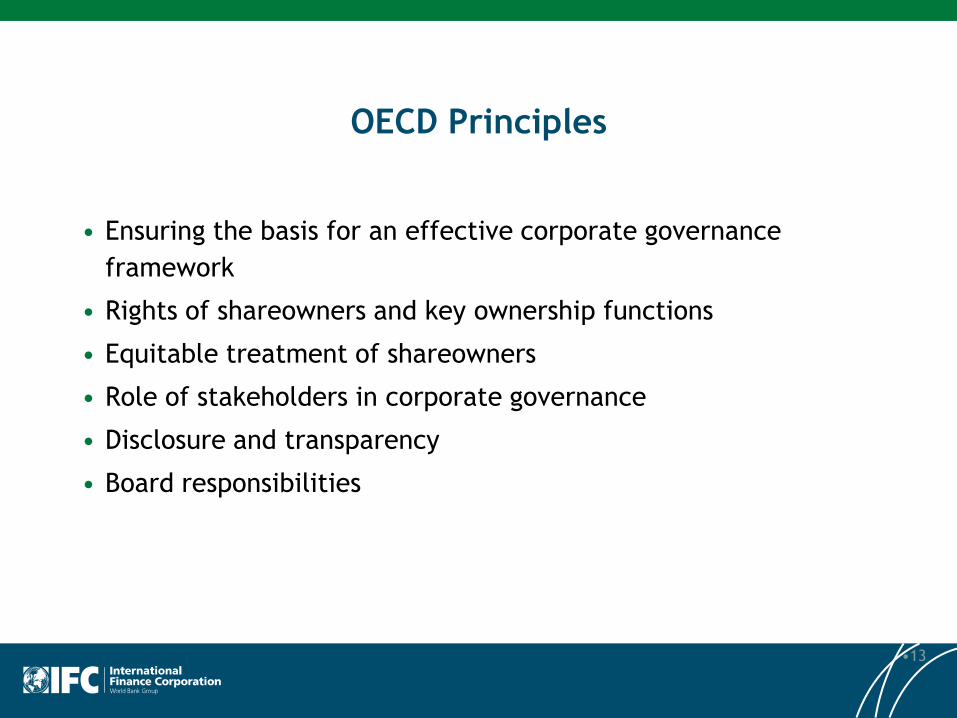

OECD Principles

• Ensuring the basis for an effective corporate governance

framework

• Rights of shareowners and key ownership functions

• Equitable treatment of shareowners

• Role of stakeholders in corporate governance

• Disclosure and transparency

• Board responsibilities

•13

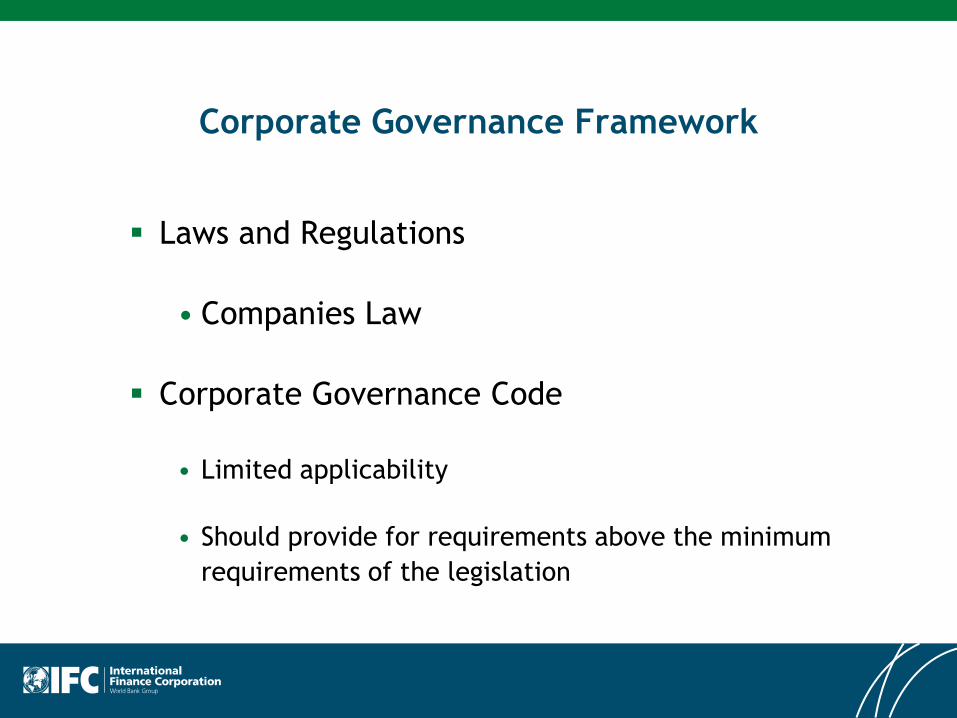

Corporate Governance Framework

Laws and Regulations

• Companies Law

Corporate Governance Code

• Limited applicability

• Should provide for requirements above the minimum

requirements of the legislation

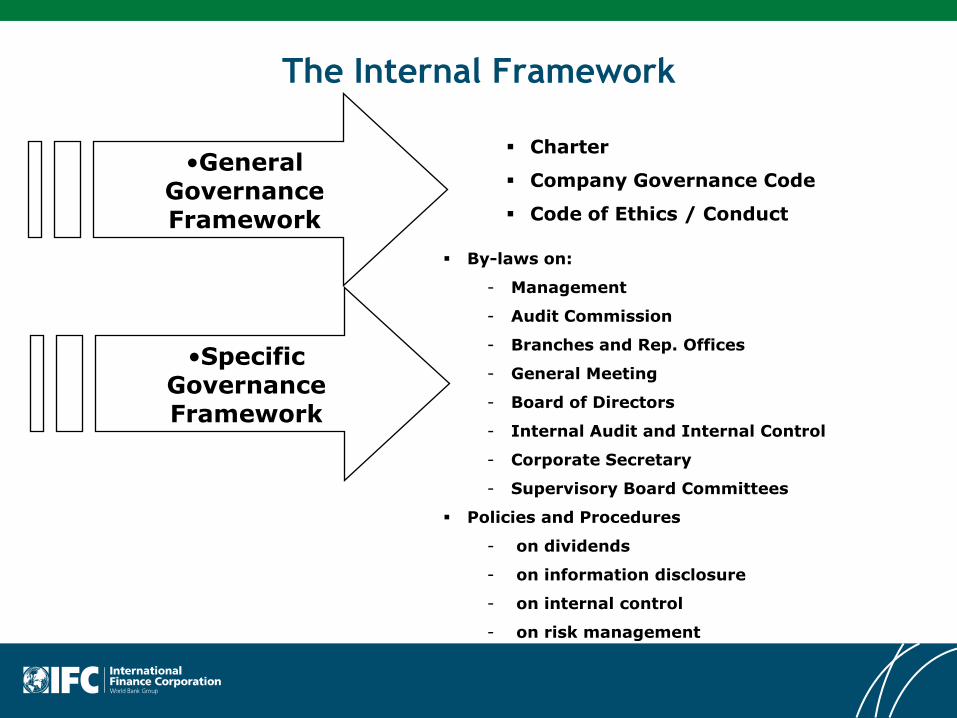

Charter

Company Governance Code

Code of Ethics / Conduct

By-laws on:

- Management

- Audit Commission

- Branches and Rep. Offices

- General Meeting

- Board of Directors

- Internal Audit and Internal Control

- Corporate Secretary

- Supervisory Board Committees

Policies and Procedures

- on dividends

- on information disclosure

- on internal control

- on risk management

•General GovernanceFramework

•Specific GovernanceFramework

The Internal Framework

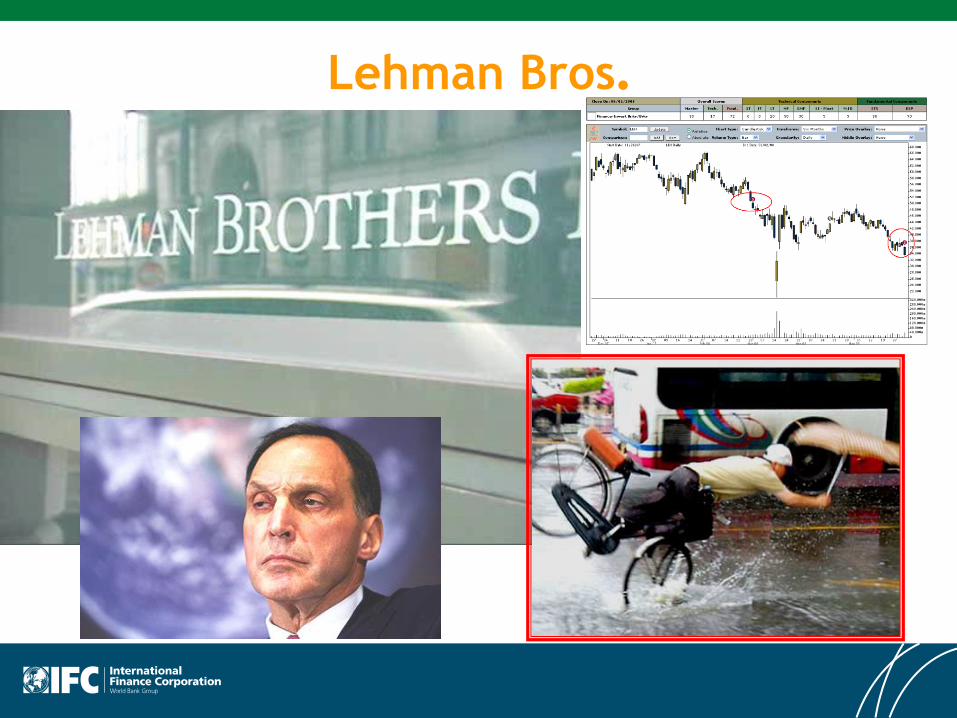

Risk 1 The board of directors is not up to the task of overseeing the strategy, management

and performance of the company.

– No proper “check and balance” of managers – e.g., UBS, Barings, Lehman

Brothers

Risk 2 The company’s risk management and controls are insufficient to ensure sound

stewardship of the company’s assets and compliance with relevant regulations.

– Catastrophic operating systems failure – e.g., Enron, Lehman Brothers.

Olympus

Risk 3 The company’s financial disclosures are not a relevant, faithful, and timely

representation of its economic transactions and resources.

– Fraudulent numbers shared with investors/capital markets – e.g., Enron,

Satyam, Olympus,

Risk 4 The company’s minority shareholders’ rights are inadequate or abused.

– Minority shareholders rights trampled or they need courts for recourse –

e.g., Mitsubishi, Samsung

Risk 5 The IFC potential investee company and its shareholders have not demonstrated a

commitment to implementing high quality CG policies and practices.

– Much of what investors see is window dressing – e.g., Tyco

Goal: Assess and Mitigate CG Risk –IFC approach

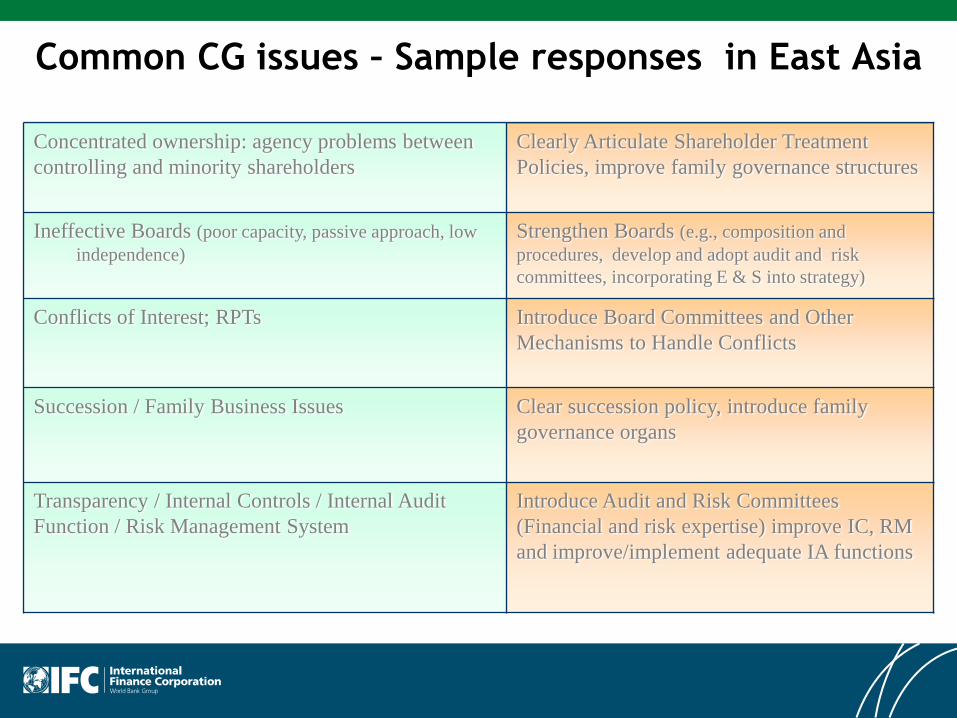

Common CG issues – Sample responses in East Asia

Concentrated ownership: agency problems between

controlling and minority shareholders

Clearly Articulate Shareholder Treatment

Policies, improve family governance structures

Ineffective Boards (poor capacity, passive approach, low

independence)

Strengthen Boards (e.g., composition and

procedures, develop and adopt audit and risk

committees, incorporating E & S into strategy)

Conflicts of Interest; RPTs Introduce Board Committees and Other

Mechanisms to Handle Conflicts

Succession / Family Business Issues Clear succession policy, introduce family

governance organs

Transparency / Internal Controls / Internal Audit

Function / Risk Management System

Introduce Audit and Risk Committees

(Financial and risk expertise) improve IC, RM

and improve/implement adequate IA functions

Board Practices

What’s wrong with this picture?Board of Directors

Average age: 68 (two board members 80+)

# of women: 1

# of bankers: 2

1 director is a theatre producer

1 direction also on American Red Cross

3 new members since turn of the century

majority of board not financially literate

Others all appointed in 1994 (at time of IPO)

Chair of the Board, CEO, and Chair of the Risk

and finance committee – all the same person

The other member of the 2 person committee

80+

Risk and Finance committee met once in 2007

Lehman Bros.

Board’s Role

“The board’s role is to provide entrepreneurial leadership of the

company within a framework of prudent and effective controls….”

United Kingdom Combined Code (2006)

•The board should exercise compelling and relentless leadership and

should not underestimate the power of leading by example -

evidenced by high levels of visibility and integrity, strong

communications, and demanding expectations. This leadership should

be clear to all within the organization, as well as shareholders and

other stakeholders.”

Boardroom Behaviours

A report prepared for Sir David Walker

by the Institute of Chartered Secretaries and Administrators , UK

June 2009

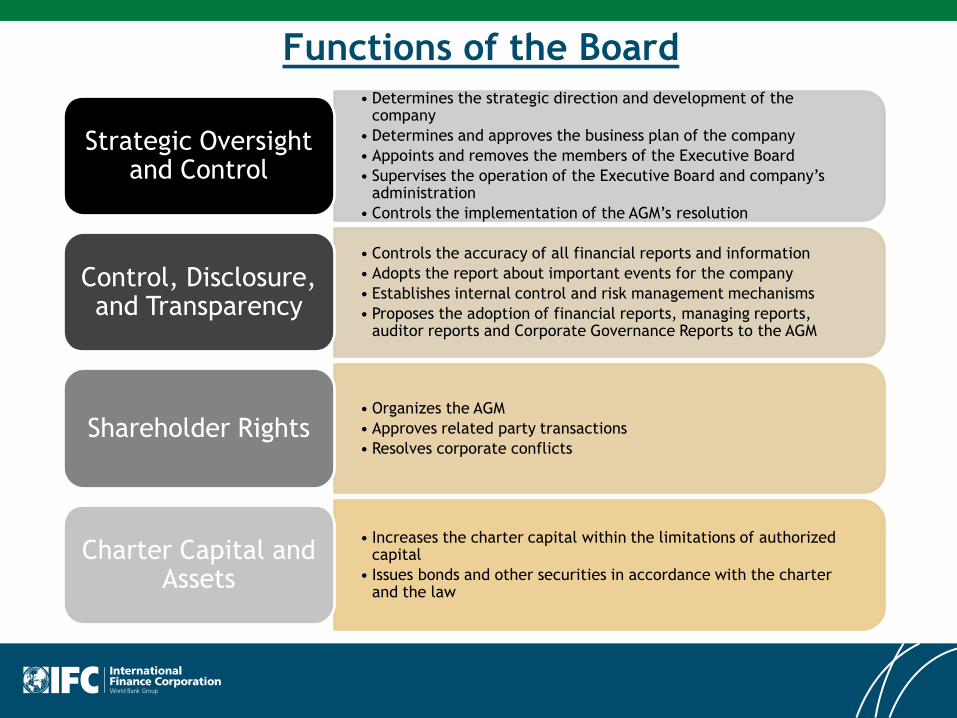

Functions of the Board• Determines the strategic direction and development of the

company

• Determines and approves the business plan of the company

• Appoints and removes the members of the Executive Board

• Supervises the operation of the Executive Board and company’s administration

• Controls the implementation of the AGM’s resolution

Strategic Oversight and Control

• Controls the accuracy of all financial reports and information

• Adopts the report about important events for the company

• Establishes internal control and risk management mechanisms

• Proposes the adoption of financial reports, managing reports, auditor reports and Corporate Governance Reports to the AGM

Control, Disclosure, and Transparency

• Organizes the AGM

• Approves related party transactions

• Resolves corporate conflictsShareholder Rights

• Increases the charter capital within the limitations of authorized capital

• Issues bonds and other securities in accordance with the charter and the law

Charter Capital and Assets

Board Types

• One-tier or unitary

• Two-tier or dual

• Supervisory Board

• Management Board

• Simple Majority

One share – 1 vote

• Cumulative voting – recommended international

practice

Used for election of Directors;

Allows the minority shareholders to have

their representative in the Supervisory Board;

1 share – “X” votes (X – is the total number of

seats in the Board of Directors)

Election of Directors

Board Size

Companies should choose a board size that will enable them to:

•Hold productive, constructive discussions

•Make prompt, rational decisions

•Efficiently organize the work of its committees, if these are established

CG Theories on composition of the Board

Shareholders

Agency Theory

Resource

Dependence Theory

Stewardship Theory

•Advice and Counsel

•Legitimacy

•Channels for communicating

information between the firm

and external organizations

•Assistance in obtaining

resources or commitments

from important elements

outside the firm

Board of Directors

Management

Access to

resources

Monitoring

Advising role

Focus on internal vs. external and

independent and non-independent

Focus on directors who can maximize

the provision of important resources

to the firm

Focus on internal vs.

external and access to

information

Institutional Theory

Legitimacy

Focus on prevailing

institutionalized norms

in the organizational

field and society

Social Network Theory

Trust

Focus on social

networks of the

principal stakeholders

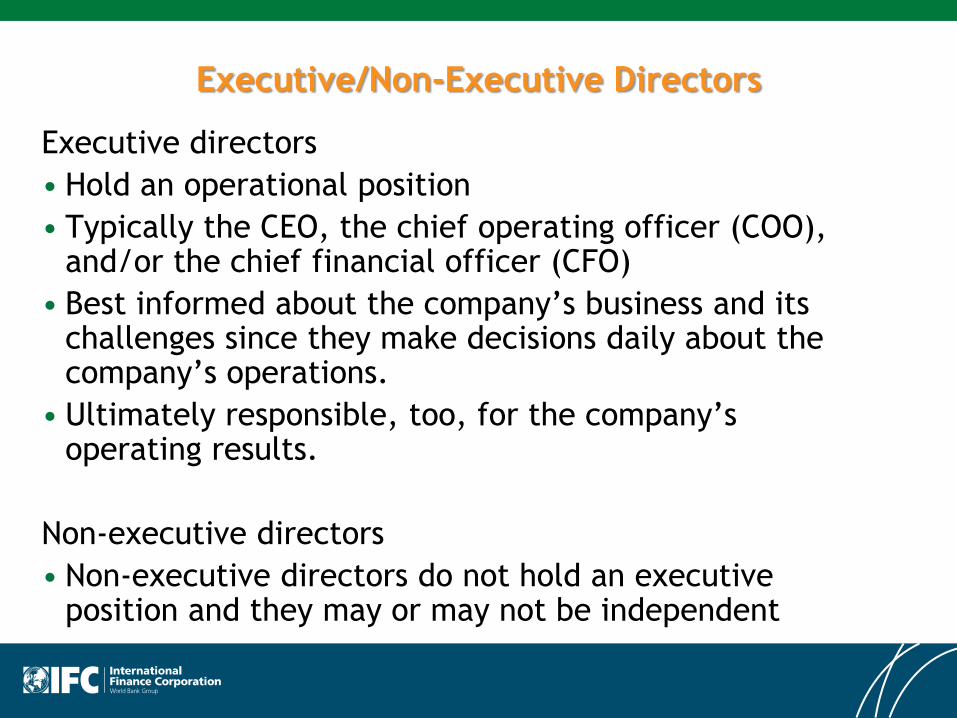

Executive/Non-Executive Directors

Executive directors

• Hold an operational position

• Typically the CEO, the chief operating officer (COO), and/or the chief financial officer (CFO)

• Best informed about the company’s business and its challenges since they make decisions daily about the company’s operations.

• Ultimately responsible, too, for the company’s operating results.

Non-executive directors

• Non-executive directors do not hold an executive position and they may or may not be independent

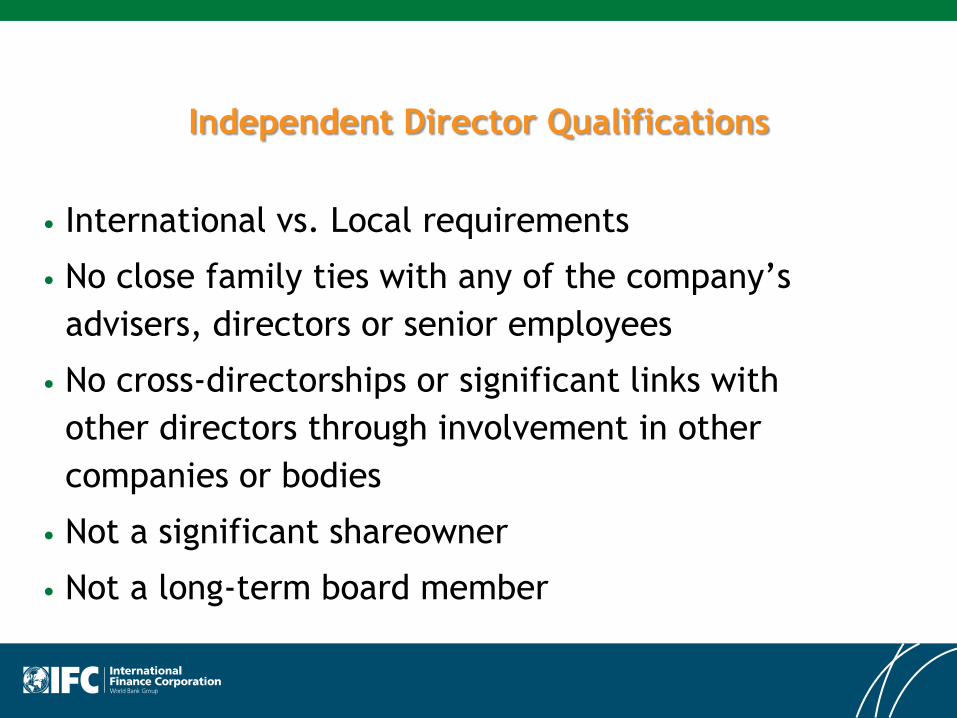

Independent Director Qualifications

• International vs. Local requirements

• No close family ties with any of the company’s

advisers, directors or senior employees

• No cross-directorships or significant links with

other directors through involvement in other

companies or bodies

• Not a significant shareowner

• Not a long-term board member

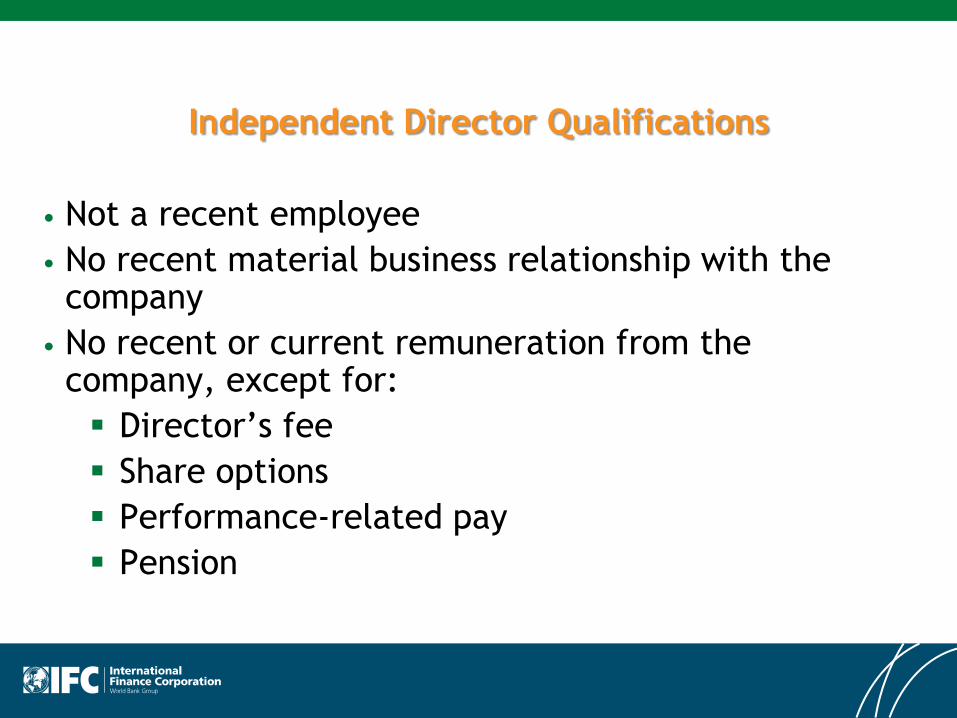

Independent Director Qualifications

• Not a recent employee

• No recent material business relationship with the company

• No recent or current remuneration from the company, except for:

Director’s fee

Share options

Performance-related pay

Pension

Importance of Independent Directors

Independent, non-executive directors should

constructively challenge and contribute to the

development of strategy.

Independent directors should scrutinize the

performance of management in meeting agreed

upon goals and objectives, and monitor the

reporting of performance.

Importance of Independent Directors

Independent directors should satisfy themselves

that financial information is accurate, and that

financial controls and systems of risk

management are robust and defensible.

Independent directors are responsible for

determining appropriate levels of remuneration

for executive directors, have a prime role in

appointing, and where necessary removing,

senior management, and in succession planning.

Board Proceedings

Preparation for Board Meetings

• Setting the agenda and its content

• The annual calendar

• Board meeting frequency

• Board briefing papers, management reports

Board Agenda

• Approval of minutes of last meeting

• Formal approval of matters requiring limited

discussion

• Executives' reports – company performance

• CEO financial performance

• Audit committee report

• Appointing external auditors (if applicable)

• Remunerations report

Meeting Minutes

• Location, date of the meeting

• Names of the persons who participated in the meeting and

those absent

• Principal points arising during discussion

• A record of board decisions

Annual Calendar of Board Activities

Standing items

• Approve meetings of previous meeting

• Approve unbudgeted capital expenditures over

• Review actual versus budgeted financial results

• Approve board committee reports

February

• 1 year assessment

• Dividend declaration

• Growth strategy discussion

• Strategy review

March

• Review financial performance versus competitors

April

• Authorization of foundation contribution

• Business plan review for next financial year

June

• Review / approve strategic plan

• Business unit No. 1 strategy review

• Review of chairman’s personal objectives

• Dividend declaration

• Annual meeting resolutions

• Set meeting schedule for next calendar year

• Litigation review

September

• Annual organization matters (committees, officer elections)

• Dividend declaration

• Annual shareowners meeting

• Review financial performance versus competitors

• Appoint external auditors

October

• Strategic plan review

December

• Approve annual budget

• Management development update

• Dividend declaration

• Strategy review

Instruments to Enhance Effectiveness

• Board by-law setting out procedural rules

Clarifies leadership roles and core responsibilities

Reserves matters specifically reserved to board

Sets management delegations and reporting arrangements

• Comprehensive induction for new directors

Legal and regulatory obligations

Financial structure of business, budgets and KPIs

Understanding of strategic priorities and current status

Familiarize with business operations, e.g. site visits

• Annual board work plan

Meetings and budget cycle, annual reporting

• Code of ethics or statement of business principles

Defines corporate values and conduct of staff and directors

•

Directors’ Duties

Fiduciary Duties

• Directors must act in a faithful, trustful manner

towards or on the company’s behalf, putting their

duty before personal interests.

• Considerations include:

Good faith

Proper purpose

Not to make secret profits

Avoiding conflicts of interest

Confidentiality

Duty Of Care

• Legal obligation imposed on directors requiring that they adhere to a reasonable standard of care while performing any acts that could potentially harm others

• Directors are normally expected to discharge their duties in:

Company’s best interests

Compliance with company’s code of conduct

Duty Of Loyalty Calls For Directors Not to

• Conduct transactions in which they have a

personal interest

• Accept a position in a competing company

• Enter into contractual relations with a competing

company

• Use the company’s assets, facilities for personal

use

• Use information, business opportunities received

in their official capacity for personal gain

• Accept gifts

• Making a self-interest transaction, competitive actions

• Insufficient control over financial operations, unfair

valuation of a deal

• Misleading statements or data, including in the issue

prospectus

• Disclosure of confidential information

• Deliberate bankruptcy

• Breach of antimonopoly and other laws

• Insufficient control over of the actions of other directors

Typical cases of liability

• Business judgment rule - no liability if director acted in

good faith, on an informed basis, and in the belief that

the decision was in the best interests of the company

• Indemnification

• Director and Officer Liability Insurance

Director Liability

Director Skills, Experience, Attributes

•Financial expertise

•Relevant industry experience

•Legal expertise

•Representatives of key stakeholders

•Experience of operating internationally

•Honesty and integrity

•Gender distribution

•Age distribution

Qualifications of Directors: Best Practice

• The trust of shareholders, other board members, managers and employees of the company

• The ability to relate to the interests of all stakeholders and make well-reasoned decisions

• The professional expertise and education

• International business experience, knowledge of national issues and trends, knowledge of the market, products and competitors

• The ability to translate knowledge and experience into solutions

Director’s Rights

• Access to information

• Reimbursement for expenses incurred

• Discharge their duties without interference

from co-directors

• Attend and participate in board meetings

• Notice of meetings

• Advice

• Delegation

Board Evaluation and Remuneration

•Why evaluate the board of directors?

• It improves board efficiency

• Focus on strategy

• Clarifies responsibility

• Better processes

• It improves accountability

• It makes the company more attractive to an

investor

Board Evaluation

• Types of Evaluations

• Self-evaluations

• Easy and simple

• Issue of bias

• Evaluations of the Whole Board

• Most common

• Evaluations of Individuals

• Most effective

• Most invasive

Board Evaluation

• Board Composition

• Committees

• Board Processes

• Board Responsibilities

• Individual Evaluations

What to Evaluate

Remuneration of Directors

• Flat established fee

• Fee based upon number of meetings attended

• Another form of reimbursement that is linked to

the company’s overall results of operations

Board Committees

• Aid to the board, not a substitution

• Generally no executive powers

• Focus on specialized areas of responsibilities

• Chair and members normally “independent”

• Key committees

• Audit (sometimes includes risk)

• Remuneration or compensation

• Nominations or governance

Benefits of Board Committees

• Assist the board in its decision making

Brings together non-executives and management

Allows detailed discussion on management matters

But, filters out operational issues that remain with

management

And, focuses on strategic decisions required of the board

• Supports board responsibilities in key areas

Audit, internal controls and risk

Executive compensation and management appointments

Governance issues and corporate policies

Nomination and selection of non-executive directors

Others, e.g. health, safety, environment, etc.

• Defined terms of reference and limitations

• Generally, no executive powers

•

Audit Committee

Role:

• Approves or recommends the approval of the appointment of external auditors and oversees their relationship with the company

• Monitors the effectiveness of, and receives regular reports from, the internal audit function

• Reviews financial statements, procedures, and systems of internal control over financial reporting

• Reviews arrangements for compliance with the requirements of regulators

• Receives reports on the operation of the company’s “whistleblower” arrangements

• May review the company’s risk-management framework

Composition:

• All independent, non-executive directors

Remuneration Committee

Role:

• Considers matters relating to board and

executive remuneration

• Approves changes to incentive and benefits plans

applicable to senior managers

• May be involved with remuneration decisions for

the entire company

Composition:

• All independent, non-executive directors

Corporate Governance And Nomination

Committee

Role:

• Considers matters relating to corporate governance,

including the composition of the board and the appointment

of new directors

• Oversees the annual performance evaluation of the board,

its committees, and the individual directors

• Reviews strategic human resource decisions and succession

plans for the chairman and other key board and executive

positions

Composition:

• All independent, non-executive directors

Relationship with Executive Bodies

• Board’s primary role

Provide guidance to and monitoring the performance of

the senior management for the benefit of all shareholders

• The relation of the board vis-à-vis management in following

areas

Setting strategy and vision of the company

Selection of CEO and senior management/approving

executive compensation

Oversight of internal controls, external audit and

preparation of financial statements

Authorization of major capital expenditures and large-value

transactions

Oversight of human resources policy

•

Relationship with Executive Bodies

Management presenting information to the board:

– Identify and provide all material information

necessary for the board to provide adequate

oversight

– Analyze how changes in industry and economy affect

the strategy

– Describe action plans to stay on track, on schedule,

and on budget

– Report to the board regularly and fully on progress -

identify and disclose risk to the board

– Monitor and inform about risk changes

– Make reasonable and realistic recommendations to

the board

Succession Planning

• A succession planning policy is needed to ensure

the business continuity of the Company’s

operations and establish a formal process of

authority delegation in the normal course of

business as well as in emergency situations.

•To put individuals who could perform

executive functions sin the future in positions

where they can build necessary skills

60 of 9

Role of the Board in Succession Planning

• Nominations and Remuneration Committee

develops the key positions succession policy.

• The Board reviews and approves (in coordination

with the CEO) succession policy

• The Board reviews candidates for the General

Director’s position.

•

Board’s Role in Financial Oversight

• Duty to maintain proper accounting records

• Periodic reporting of financial position, performance

• Establishing, monitoring proper internal controls

• Ensuring proper external controls and audit

• Skills, knowledge required by directors

•

The Board and Risk Management The board should know about and evaluate the:

• Most significant risks facing the company

• Possible effects on shareowners

• Company’s management of a crisis

• Importance of stakeholder confidence in the organization

• Communications with the investment community

The board should ensure that:

• Sufficient time is devoted to discuss risk strategy

• Appropriate levels of awareness exist throughout the company

• Risk-management processes work effectively

• A clear risk-management policy is published

Board Oversight of Control Environment

Building Effective Board Governance

• Defining key board roles

Board Chairman

Board Directors - executive and non-executive

• Putting in place board governance arrangements

Board committees to support decision process

Supporting functions to regulate processes

Board procedures and rules, e.g. conflicts of interest

Delegated authorities for management

• Ensuring proper oversight and supervision

Management reporting and public disclosures

Assurance processes and controls

•

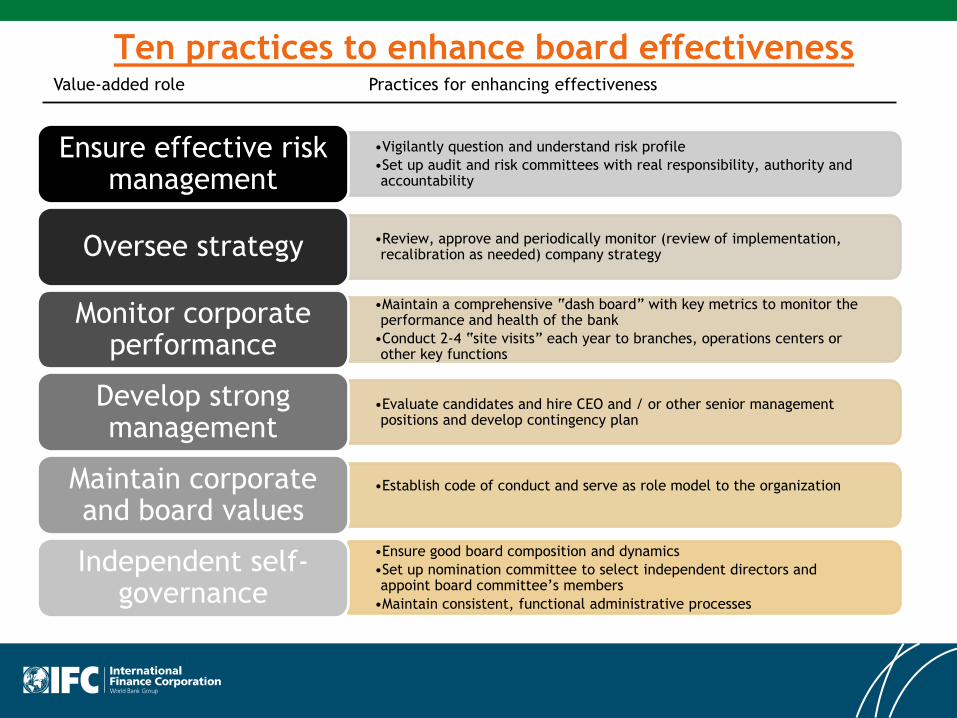

Ten practices to enhance board effectivenessValue-added role Practices for enhancing effectiveness

•Vigilantly question and understand risk profile

•Set up audit and risk committees with real responsibility, authority and accountability

Ensure effective risk management

•Review, approve and periodically monitor (review of implementation, recalibration as needed) company strategyOversee strategy

•Maintain a comprehensive “dash board” with key metrics to monitor the performance and health of the bank

•Conduct 2-4 “site visits” each year to branches, operations centers or other key functions

Monitor corporate performance

•Evaluate candidates and hire CEO and / or other senior management positions and develop contingency plan

Develop strong management

•Establish code of conduct and serve as role model to the organizationMaintain corporate and board values

•Ensure good board composition and dynamics

•Set up nomination committee to select independent directors and appoint board committee’s members

•Maintain consistent, functional administrative processes

Independent self-governance

And how is your board?

•Low Involvement •High Involvement

Passive

Board

Certifying

Board

Engaged

Board

Intervening

Board

Operating

Board

•At discretion

of GD

•Limited

activity &

participation

•Limited

accountability

•Ratifies Mgmt.

preferences

•Certifies to SHs

that GD meets

expectations

•Takes corrective

action only as

ultimate ratio

•Understands

role of ind.

directors

•Informed about

GDs performance

•Established a

succession plan

•Provides insight,

advice & support

to mgmt.

•Understands its

responsibility to

oversee mgmt.

•Guides & judges

the GD

•Has right skills

mix to add value

•Define roles and

responsibility of

Board vs. Mgmt.

•Intensely

involved in

decision-making

around key issues

•Frequent &

intense

meetings, often

on short notice

•Makes key

decisions that

mgmt. then

implements

•Fills gaps in

mgmt.

experience

•Source: HBR, David A. Nadler,

Building Better Boards

Anar Aliyev

Operations Officers

IFC Mongolian Corporate Governance Project

E-mail: [email protected]