Embed Size (px)

Citation preview

Evolving Prospect for the Global Economy,

China’s New Normal and its Relevance to

Mongolia

Presentation at the Economic research Institute Mongolia

Bert Hofman, World Bank

Ulaanbaatar, March 25 2016

1

THE WORLD EONOMY IN THE

SHORT AND (VERY) LONG RUN

2

The World Economy

Source: ICP Program http://siteresources.worldbank.org/ICPINT/Resources/270056-

1183395201801/Summary-of-Results-and-Findings-of-the-2011-International-Comparison-Program.pdf

Mongolia

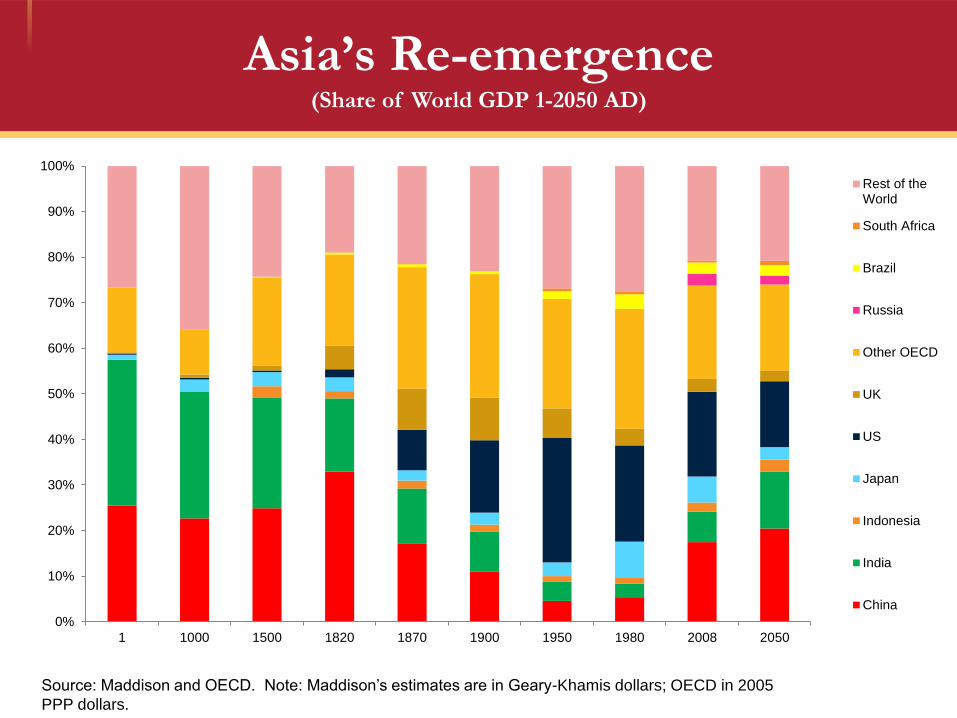

Asia’s Re-emergence(Share of World GDP 1-2050 AD)

Source: Maddison and OECD. Note: Maddison’s estimates are in Geary-Khamis dollars; OECD in 2005

PPP dollars.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 1000 1500 1820 1870 1900 1950 1980 2008 2050

Rest of theWorld

South Africa

Brazil

Russia

Other OECD

UK

US

Japan

Indonesia

India

China

Emerging Markets Catching Up as

OECD Productivity Slows

5Source: Conference Board, staff estimates. Note: Output per employee in 2014 US$ (converted to US$

using 2014 market exchange rates) Labor productivity growth five year moving average centered on final

year.

0

5,000

10,000

15,000

20,000

25,000

-0.3

0.7

1.7

2.7

3.7

4.7

5.7

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Gobal labor productivity growth OECD Labor productivity growth Output per employed person

Output per Employee (rhs)

Global labor productivity growth (lhs)

OECD Labor productivity growth (lhs)

Lower Global Inequality, but a Squeezed

(Western) Middle Class

6

Change in real income per global income

percentile 1988-2008

Source: Branko Milanovic

An Older, Urban World

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

China

2050

Urbanization

Old-age dependency ratio

EU

2050

Japan 2050

India 2050

EU 2010

Brazil 2050

US 2050

US 2010

Nigeria

2050

India 2010

China

Brazil 2010 Korea 2050

Indonesia 2050

Japan

Nigeria

Pakistan 2050

Size of bubbles

corresponds with

population of age 15-65Indonesia

2010

Philippines

Pakistan 2010

Korea 2010

Russia

Russia

2010

Vietnam 2050

Vietnam 2010

Source: World Bank Nutrition Population and Health

Database, UN Population Database

8

GDP Growth (Percent)

Source: World Bank.

Note: Several countries were reclassified from middle-income to high-income country status in 2015, including Argentina, Hungary, and Venezuela.

All series have been adjusted to ensure a constant sample according to current income status.

-4

0

4

8

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

World High-income countries Developing countries

Global Growth:

Slower in 2015. Modest Pickup 2016 and beyond

9

GDP Growth(Percent)

Source: World Bank.

Note: Several countries were reclassified from middle-income to high-income country status in 2015, including Argentina, Hungary, and Venezuela. All series have been adjusted to ensure a

constant sample according to current income status.

Regional Forecasts

Current forecastChange from

October

2014 2015 2016 2017 2015 2016 2017

World 2.6 2.4 2.9 3.1 -0.1 -0.1 0.0

High-income countries 1.7 1.6 2.1 2.1 -0.1 0.0 0.0

Developing countries 4.9 4.3 4.8 5.3 0.0 -0.2 0.0

East Asia and Pacific 6.8 6.4 6.3 6.2 -0.1 -0.1 -0.1

Europe and Central Asia 2.3 2.1 3.0 3.5 0.5 -0.2 0.0

Latin America and Caribbean 1.5 -0.7 0.1 2.3 -0.4 -1.0 0.0

Middle East and North Africa 2.5 2.5 5.1 5.8 0.2 0.7 0.7

South Asia 6.8 7.0 7.3 7.5 -0.1 -0.1 0.0

Sub-Saharan Africa 4.6 3.4 4.2 4.7 -0.3 -0.3 -0.2

Diminishing Expectations

10

Change in growth forecast for 2020 from 2010-2015

Source: World Bank

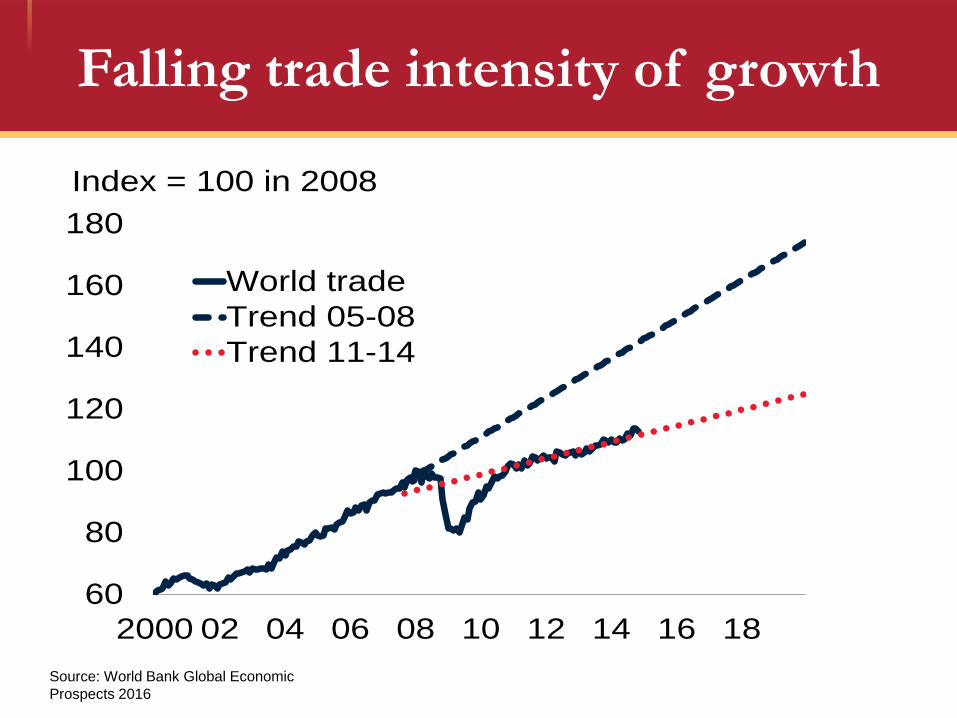

Falling trade intensity of growth

60

80

100

120

140

160

180

2000 02 04 06 08 10 12 14 16 18

World trade

Trend 05-08

Trend 11-14

Index = 100 in 2008

Source: World Bank Global Economic

Prospects 2016

All that Debt

12Source: BIS

13

FED expected to move up

Individual FED Board Member’s projection of

the Federal Funds Rate, percent

Source: Federal reserve board, Financial Times

A SLOWING, CHANGING

CHINA

14

Ties that Bind

15

84%

35%

45%

50%

25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Exports (2015) Imports (2015) Tourists (2015) Registered foreigncompanies (2014)

FDI (2005-13)

China’s share in Mongolia’s key economic variables

Mongolia’s dramatic export shift

16

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mongolia’s export share per destination, percent

China European Union United States Russia Japan Switserland Kazakhstan Other

Source: IMF Directions of Trade

China’s New Normal

Note: World Bank projections. These assume progressive implementation of reforms announced in the 3rd Plenum of

the Central Committee of the 18th Party Congress

0

1

2

3

4

5

6

7

8

2014 2015 2016 2017 2018 2019 2020

private consumption government consumption gross capital formation next exports GDP

GDP Growth Rate and Percentage Point Contribution to Growth

Growing less, but adding more

Change in GDP, Absolute Value, bn. 2005 US$

-1000

-500

0

500

1000

1500

1981 1986 1991 1996 2001 2006 2011

China US Japan Eurozone

Bn. 2005$

Source: World Bank Estimates

The Largest Manufacturer in the World

0

2E+12

4E+12

6E+12

8E+12

1E+13

1.2E+13

1.4E+13

2000 2005 2010 2012 2013

China European Union Japan India United States ROW

Current US$

Manufacturing Value Added Current $

Source: World Development Indicators

Largest Exporter

0

2E+12

4E+12

6E+12

8E+12

1E+13

1.2E+13

1.4E+13

1.6E+13

1980 1985 1990 1995 2000 2005 2010 2012 2013

China France Germany Japan India Korea, Rep. United States United Kingdom Rest of EU

Current US$

Exports of Goods and Services, Current US$

Source: World Development Indicators

Largest Energy User

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

1980 1985 1990 1995 2000 2005 2010 2012

China European Union Japan India United States ROW

Kiloton coal eq.

Energy Use, Kilotons of Coal Equivalent

Source: World Development Indicators

Largest Consumer of many Commodities

Source: World Economic Forum based on BP Statistical review of World Energy 2015, , World Bureau of Metal Statistics, US

Department of Agriculture, JP Morgan, Wall Street Journal,

Services now more important than

Industry

39

40

41

42

43

44

45

46

47

48

49

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

Service Industry

Percent of GDP

Source: National Bureau of Statistics

Though structural change in real terms

is less pronounced

0

0.1

0.2

0.3

0.4

0.5

0.6

1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

Agriculture Industry Services

Share of GDP, calculated at 2005 constant prices

China is still less urbanized than

expected on the basis of income

0

10

20

30

40

50

60

70

80

90

100

100 1000 10000 100000

China

China 1990

China 2000

China

2010

Income per capita, constant

Urbanization

Source: World Development Indicators and Staff Estimates

Urbanization will facilitate services

industry

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 60 70 80 90 100

Services value added (% of GDP)

Urban population (% total)

Taiwan, China (1962-2009) Japan (1955-2011)

Korea (1965-2011) China (1978-2011)

China’s exports becoming more

sophisticated

-4

-3

-2

-1

0

1

2

3

900 9000 90000

China 1995-2012

South Sudan

Qatar

Singapore

Malaysia

RussiaIndia

Brazi

Germany

Japan

USA

Economic Complexity Index

GDP Per Capita 2012 (2011 PPP$. Log Scale)

Source: AJG Simoes, CA Hidalgo. The Economic Complexity Observatory: An Analytical Tool for Understanding the Dynamics of Economic

Development. Workshops at the Twenty-Fifth AAAI Conference on Artificial Intelligence. (2011) and https://atlas.media.mit.edu/en/rankings/country/

accessed 9-2—2015

Note: ECI combines metrics of the diversity of countries and the ubiquity of products to create measures of the relative complexity of a country’s

exports

China’s exports becoming more

sophisticated

1995 2012

Source: AJG Simoes, CA Hidalgo. The Economic Complexity Observatory: An Analytical Tool for Understanding the Dynamics of Economic

Development. Workshops at the Twenty-Fifth AAAI Conference on Artificial Intelligence. (2011) and https://atlas.media.mit.edu/en/rankings/country/

accessed 9-2--2015

Quality rapidly catching up

29

China is becoming more innovative

0

100

200

300

400

500

600

700

800

900

1989 1992 1995 1998 2001 2004 2007 2010

Resident Patens Applications per 10000 Population

China India Malaysia Russia Germany USA UK Brazil

Rapid real appreciation reduced current

account surpluses

31

-2

0

2

4

6

8

10

12

14

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Current Account

Percent of GDP

80

90

100

110

120

130

140REER (RHS)

Index, 2010 = 100

Source: World Bank Prospects group

More real appreciation to come

Source: World Development Indicators, Staff Estimates

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

700 7000 70000

Series2Series4

Domestic/International

Prices ("Real Exchange

Other countries 2013

China 1991-2013

Income per capita 2013, PPP $ log

USA

Korea

Japan

Australia

Burundi

Eurozo

Norway

SingaporQatar

LuxembourUK

Cuba

Macao,

Importance of external demand

declining

0

5

10

15

20

25

30

35

40

45

50

1980 1985 1990 1995 2000 2005 2010

Eurozone

China

Japan

Exports as a share of

GDP, Percent

Source: WDI

Real estate leading the investment

slowdown

0

5

10

15

20

25

30

35

40

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Fixed Asset Investment, yoy % FAI: Real Estate, yoy %

Source: National Bureau of Statistics through

CIEC

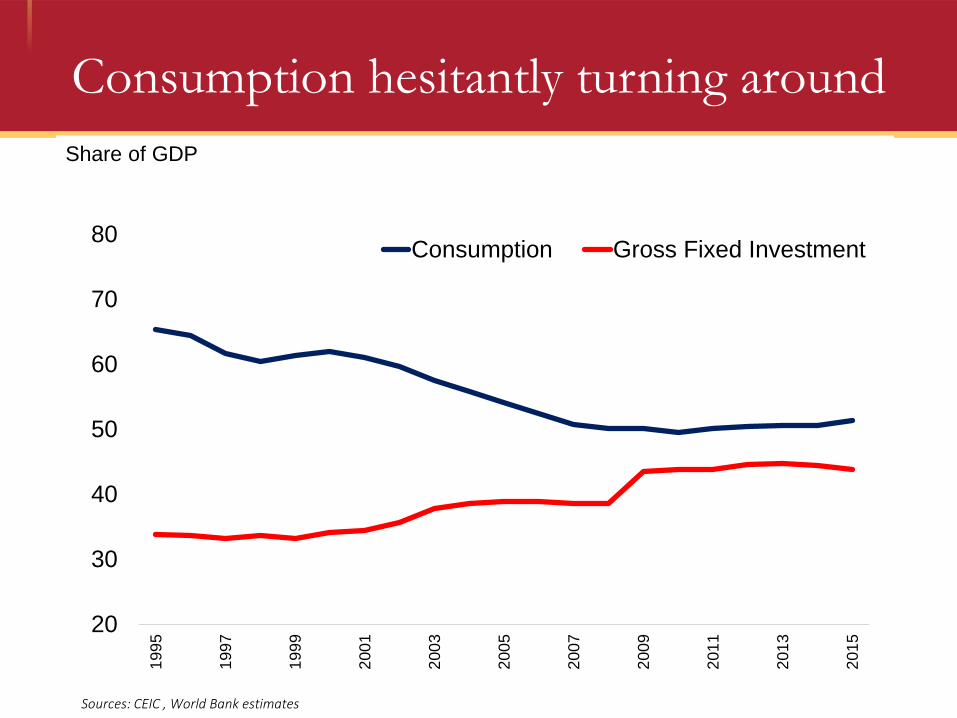

Consumption hesitantly turning around

Sources: CEIC , World Bank estimates

20

30

40

50

60

70

80

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

Consumption Gross Fixed Investment

Share of GDP

Household Income Share Increasing

Sources: CEIC , World Bank estimates

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Household disposable income Wages

The Aftermath of a Credit Binge

10

15

20

25

30

35

40

2007 2007 2008 2008 2009 2009 2010 2010 2011 2011 2012 2012 2013 2013 2014 2014 2015

Aggregate financing (stock,% yoy) All loan (stock,% yoy)

Growth in outstanding total credit stock (% yoy)

Sources: CEIC

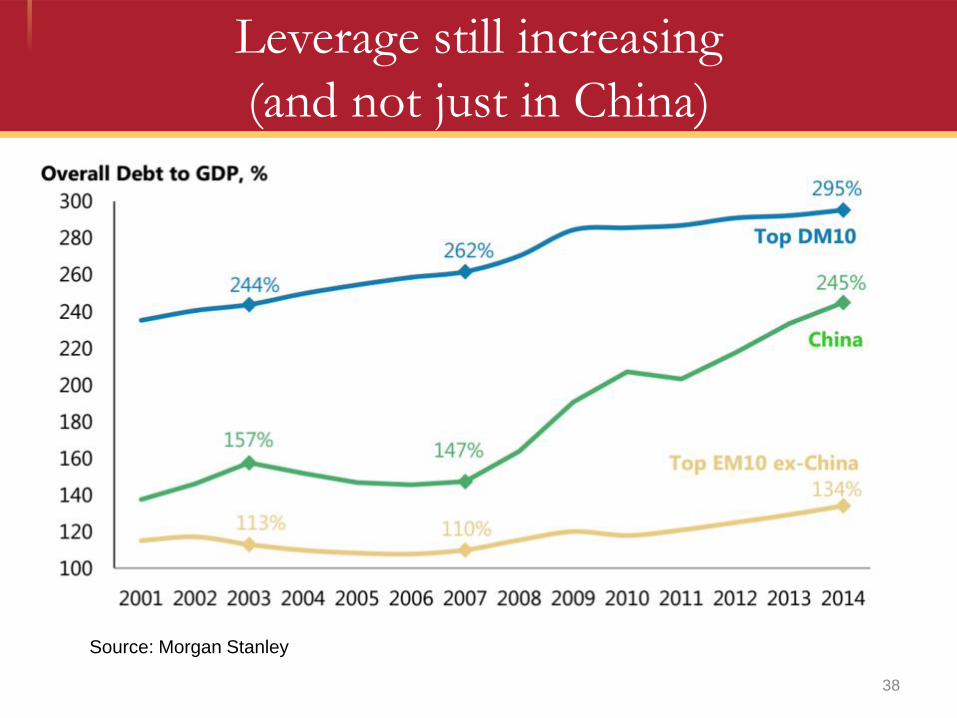

Leverage still increasing

(and not just in China)

38

Source: Morgan Stanley

39Source: Bloomberg

Corporate debt the biggest risk

Rapid Credit Growth Tends to Result in

Non-performing Loans

R² = 0.338

0

5

10

15

20

25

30

35

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

NP

Ls

to

Gro

ss

To

tal L

oa

ns

Actual/Predicted Private Credit to GDP

All other countries HIC G20 Non-Asia MIC East Asia MIC China

Cost of Environmental Damage

Rising

0

100

200

300

400

500

600

1990 1995 2000 2005 2010 2012

Carbon Dioxide Damage Energy Depletion Mineral Depletion

Net Forest Depletion Particulate Emission Damage

Bn. Current US$

Source: World Development Indicators

Though not as a share of GDP

0

2

4

6

8

10

12

1990 1995 2000 2005 2010 2012

Carbon Dioxide Damage Energy Depletion Mineral Depletion

Net Forest Depletion Particulate Emission Damage

Percent of Gross National

Income

Source: World Development Indicators

The Big Global Issue

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0 5 10 15 20 25

China

US

EU

Sustainable Emission per Capita: 1.7 ton per year

to keep global warming<2 degrees (IPCC)

India

Latin America

Japan

Russia

South

IndonesiaCO2 emissions per capita

CO2 emissions per Unit of

GDP (2005 PPP $)

Source: World Development Indicators. Note: Emissions exclude change in land

use. Bubble indicates total emissions

China’s energy intensity is falling

Source: IEA Energy Outlook 2015

China’s copper intensity of GDP among

highest in the world

45Source: International Copper Studies Group

SPILLOVERS FROM CHINA’S

SLOWDOWN

46

47

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

EM Global

BRICS China

Source: World Bank staff estimates.

Note: Cumulated impulse responses of EM and global growth at the two-year horizon. The shock size is such that BRICS growth declines by one percentage point on

impact. The shock size for China is calibrated such that its growth declines by exactly the same amount as BRICS at the end of two years. Solid bars denote the median

and the error bars denote the 33-66 percent confidence bands.

Large Spillovers from Slowing BRICS

Decline in BRICS and China Growth on Other Emerging Markets and World (Percentage point)

48

Decline in each of the BRICS growth (1 pp) on Global and Other EM growth(Percentage point)

Source: World Bank staff estimates.

Notes: Cumulated impulse responses at the end of two years due to a one percentage point decline on impact in China growth. EM excludes BRICS. Global is GDP-

weighted average of BRICS, EM, FM, and G7 responses. Bars represent medians, and error bars 16-84 percent confidence bands.

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

Global EM excl. BRICS

China Russia Brazil India South Africa

China a Source of Global Spillovers

49

Slowing China Affects Commodity Exporters More

Decline in China Growth (1 pp) on Emerging Markets Growth(Percentage point)

Source: World Bank staff estimates.

Left: Cumulated impulse responses of GDP growth, at the two year horizon, due to a one percentage point decline in China growth. For each group, the figures refer to the cross-sectional

average response across all the countries in that group.

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

Commodity exporter Commodity importer

ANNEX: RECENT FINANCIAL

MARKET VOLATILITY

50

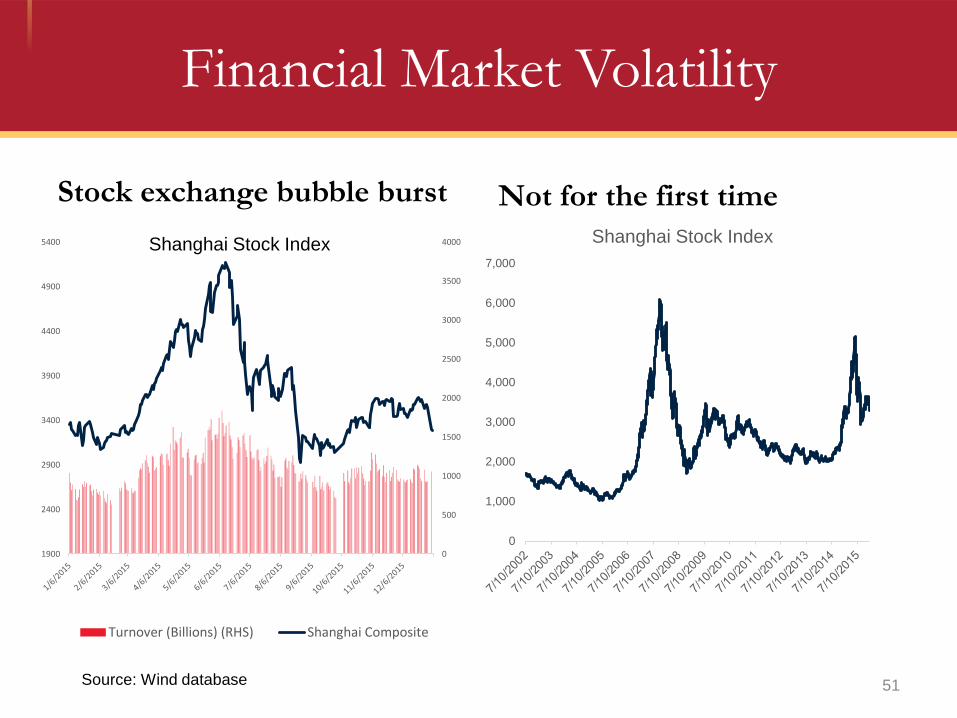

Financial Market Volatility

Stock exchange bubble burst Not for the first time

51

0

500

1000

1500

2000

2500

3000

3500

4000

1900

2400

2900

3400

3900

4400

4900

5400

Turnover (Billions) (RHS) Shanghai Composite

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Shanghai Stock IndexShanghai Stock Index

Source: Wind database

Mixed results of circuit breakers

52

0

2000

4000

6000

8000

10000

12000

14000

16000

2800

2900

3000

3100

3200

3300

3400

3500

3600

09

:30

09

:56

10

:22

10

:48

11

:14

13

:09

13

:35

14

:01

14

:27

14

:53

09

:48

10

:14

10

:40

11

:06

13

:01

13

:27

13

:53

14

:19

14

:45

09

:40

10

:06

10

:32

10

:58

11

:24

13

:19

13

:45

14

:11

14

:37

09

:32

09

:58

10

:24

10

:50

11

:16

13

:11

13

:37

14

:03

14

:29

14

:55

09

:50

10

:16

10

:42

11

:08

13

:03

13

:29

13

:55

14

:21

14

:47

2016-01-04 2016-01-05 2016-01-06 2016-01-07 2016-01-08

Volume Price

Source: Wind database

Financial Market Volatility

Pressures on RMB/USD5.9500

6.0500

6.1500

6.2500

6.3500

6.4500

6.5500

6.6500

Spot rate Reference rate

Upper bound Lower bound

August 10-January 5

Driven by capital outflows

53Source: Wind database

Financial Market Volatility

And arbitrage opportunities

-0.14

-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

But RMB Basket still in a band

0.93

0.95

0.97

0.99

1.01

1.03

1.05

1.07

RMB/USD RMB/Basket

Upper Bound Lower Bound

54

CNY/CNH spread, negative values indicate that onshore rate is higher

(stronger) than offshore rates

Source: Wind database

Financial Market Volatility

Interbank rate surprisingly calm

0.8

1.3

1.8

2.3

2.8

Per

cen

t

CN: Shanghai Interbank Offered Rate (SHIBOR): Overnight

CN: Shanghai Interbank Offered Rate (SHIBOR): 1 Week

Lots of volatility in Hong Kong

0.0

2.0

4.0

6.0

8.0

10.0

12.0

6/1/2015 7/1/2015 8/1/2015 9/1/2015 10/1/2015 11/1/2015 12/1/2015 1/1/2016

Per

cen

t

CNH HIBOR Fixing: TMA: Overnight

CNH HIBOR Fixing: TMA: 1 Week

55Source: CIEC Data

56

U.S. Monetary Policy:Slower Tightening Cycle; Gap Remains

U.S. Policy Interest Rates(Percent)

Source: World Bank, Bloomberg, US Federal Open Market Committee.

Note: Left panel: Past tightening cycles refers to average of Fed fund rate hikes during previous tightening cycles (December 86, March 88, February 94,

March 97, June 99, and June 04). Market expectations as of December 15.

0

1

2

3

4

Dec-14 Dec-15 Dec-16 Dec-17

FOMC expectations

Past tightening cycles

Gap between FOMC and Market Expectations(Basis points)

0

40

80

120

160

Ma

r-1

4

Ju

n-1

4

Sep

-14

Dec

-14

Mar-

15

Ju

n-1

5

Sep

-15

Dec

-15

2016

2017

57

Private Debt and Credit Growth

in Emerging Markets

Source: World Bank, International Monetary Fund, Bank for International Settlements.

Left panel: Weighted-average of debt-to-GDP ratios of households and non-financial corporations in Brazil, Russia, India, South Africa, Mexico, Indonesia, Malaysia, and Turkey. Right

panel: EM with general government debt above 60 percent of GDP in 2015 include Brazil, Egypt, India, Hungary, Morocco, Pakistan.

Number of Emerging Markets with

Elevated Government Debt(Percent, share of countries)

Financial Market Turbulence: Elevated Debt

(Percent of GDP, percent)

10

15

20

25

80

90

100

110

120

130

2010 2011 2012 2013 2014 2015

Private debt

Credit growth (RHS)

0

20

40

60

80

Debt >

40% of GDP

Debt >

60% of GDP

2007 2015