Embed Size (px)

Citation preview

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587

US Venture Capital & Startup Traction Report

2015

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-65872

IntroductionThis report analyzes venture funding trends for US startups from 2006 to present. At Mattermark we pride ourselves on providing the startup ecosystem with information on how businesses grow, raise funding, and evolve. We believe utilization of these resources should be combined with your special knowledge of your industry, region and role. Startup investments and business decisions hold a level of risk on the part of investors, founders, employees, services providers, and anyone who stands to benefit from these transactions.

We hope that this report both informs your future conversations and helps you head into 2016 fundraising and deal making with better data for your upcoming business decisions.

Sincerely,

Danielle Morrill, CEO & Cofounder of Mattermark

Data Sources

Mattermark uses a broad range of sources to present the most complete picture possible of the startup ecosystem. In addition to extensive primary source research sourced specifically for this report, Mattermark uses publicly-available data from AngelList (www.angel.co), Crunchbase (www.crunchbase.com), NASDAQ, (www.nasdaq.com), the United States Securities and Exchange Commission (www.sec.gov), and source relationships with thousands of investors, community leaders, and startup founders.

Please send any questions, comments, or corrections for the editor to [email protected].

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-65873

Table of ContentsDisclaimer

This information has been prepared by Mattermark, Inc. solely for informational purposes. It is not, and should not be regarded as, investment advice, as a recommendation regarding any particular security, or as a course of action. Opinions expressed herein are current opinions as of the date appearing in this material only and are subject to change without notice.

No part of this document may be reproduced in any manner, in whole or in part, without the prior written permission of Mattermark, Inc. This information is provided with the understanding that, with respect to the material provided herein, you will make your own independent decision with respect to any course of action based on your own judgment, and that you are capable of understanding and assessing the merits of a course of action.

Neither the information, nor any opinion contained herein, constitute a solicitation or offer by Mattermark, Inc. to buy or sell any securities, futures, options, or other financial instruments or provide any investment advice or service. Mattermark, Inc. does not purport to, and does not, in any fashion, provide broker/dealer, consulting, or any related services. Mattermark, Inc. shall not have any liability for any damages of any kind whatsoever relating to this material. By accepting this material, you acknowledge, understand, and accept the foregoing.

4 10 Year Market Overview

13 Pre Series A

18 Series A

23 Series B

29 Series C

34 Late Stage

40 Methodology Notes

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 5

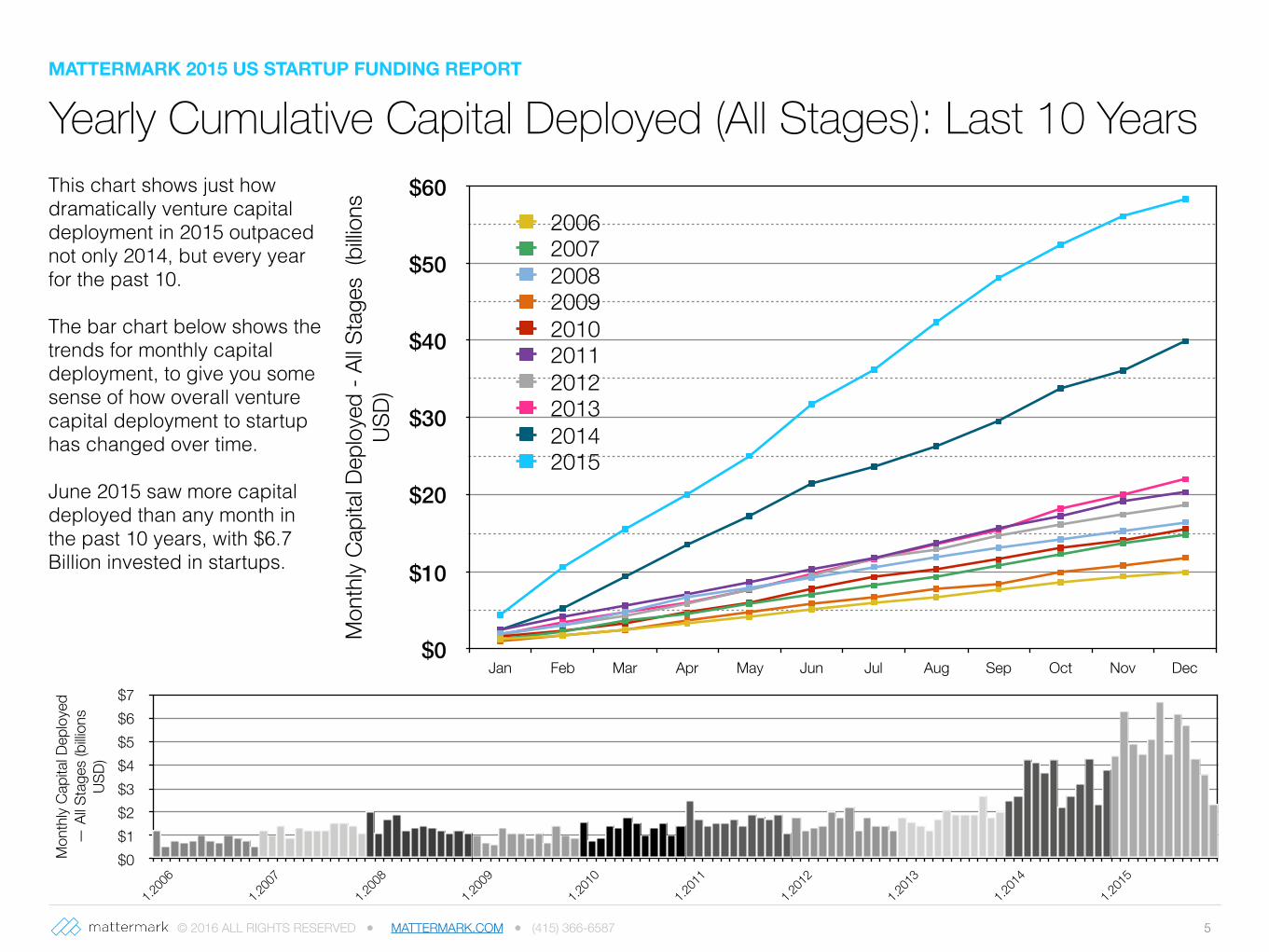

Yearly Cumulative Capital Deployed (All Stages): Last 10 YearsThis chart shows just how dramatically venture capital deployment in 2015 outpaced not only 2014, but every year for the past 10.

The bar chart below shows the trends for monthly capital deployment, to give you some sense of how overall venture capital deployment to startup has changed over time.

June 2015 saw more capital deployed than any month in the past 10 years, with $6.7 Billion invested in startups.

Mon

thly

Capi

tal D

eplo

yed

- All S

tage

s (b

illion

s US

D)

$0

$10

$20

$30

$40

$50

$60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2006200720082009201020112012201320142015

MATTERMARK 2015 US STARTUP FUNDING REPORTM

onth

ly Ca

pita

l Dep

loye

d —

All S

tage

s (b

illion

s US

D)

$0$1$2$3$4$5$6$7

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 6

Annu

al De

al Vo

lume

by S

tage

0

200

400

600

800

1,000

1,200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Seed/Angel Series A Series B Series C Late Stage

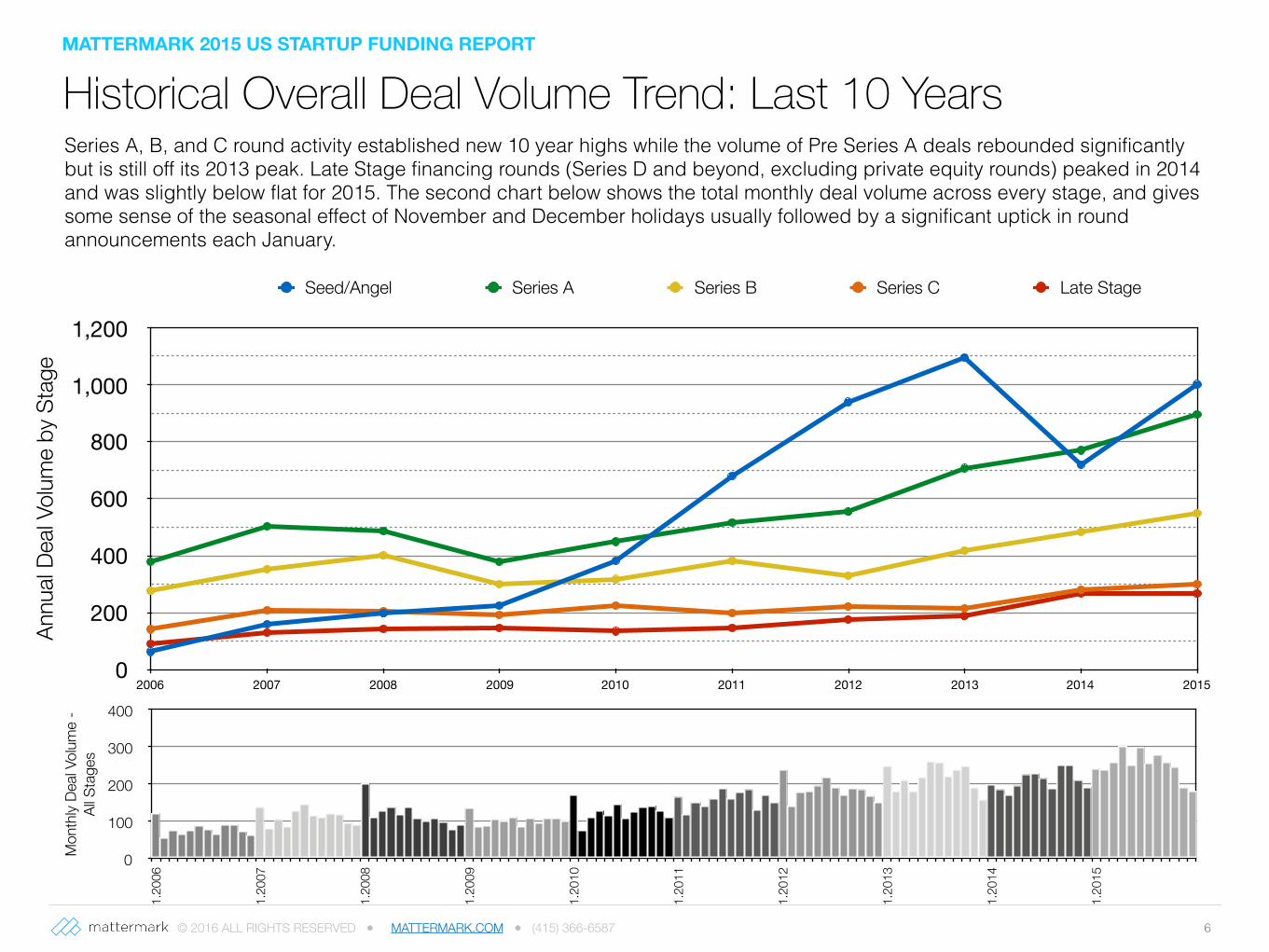

Historical Overall Deal Volume Trend: Last 10 YearsSeries A, B, and C round activity established new 10 year highs while the volume of Pre Series A deals rebounded significantly but is still off its 2013 peak. Late Stage financing rounds (Series D and beyond, excluding private equity rounds) peaked in 2014 and was slightly below flat for 2015. The second chart below shows the total monthly deal volume across every stage, and gives some sense of the seasonal effect of November and December holidays usually followed by a significant uptick in round announcements each January.

Mon

thly

Deal

Volum

e -

All S

tage

s

0

100

200

300

400

1.20

06

1.20

07

1.20

08

1.20

09

1.20

10

1.20

11

1.20

12

1.20

13

1.20

14

1.20

15

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 7

S&P

500

Inde

x (^

SPX

)

0

500

1,000

1,500

2,000

2,500

Capi

tal D

eplo

yed

(billi

ons U

SD)

$0

$5

$10

$15

$20

$25

Q1

'06

Q2

'06

Q3

'06

Q4

'06

Q1

'07

Q2

'07

Q3

'07

Q4

'07

Q1

'08

Q2

'08

Q3

'08

Q4

'08

Q1

'09

Q2

'09

Q3

'09

Q4

'09

Q1

'10

Q2

'10

Q3

'10

Q4

'10

Q1

'11

Q2

'11

Q3

'11

Q4

'11

Q1

'12

Q2

'12

Q3

'12

Q4

'12

Q1

'13

Q2

'13

Q3

'13

Q4

'13

Q1

'14

Q2

'14

Q3

'14

Q4

'14

Q1

'15

Q2

'15

Q3

'15

Q4

'15

Quarterly Startup Investment Startup Investment 10 Year Trend Quarter-End S&P 500 S&P 500 10 Year Trend

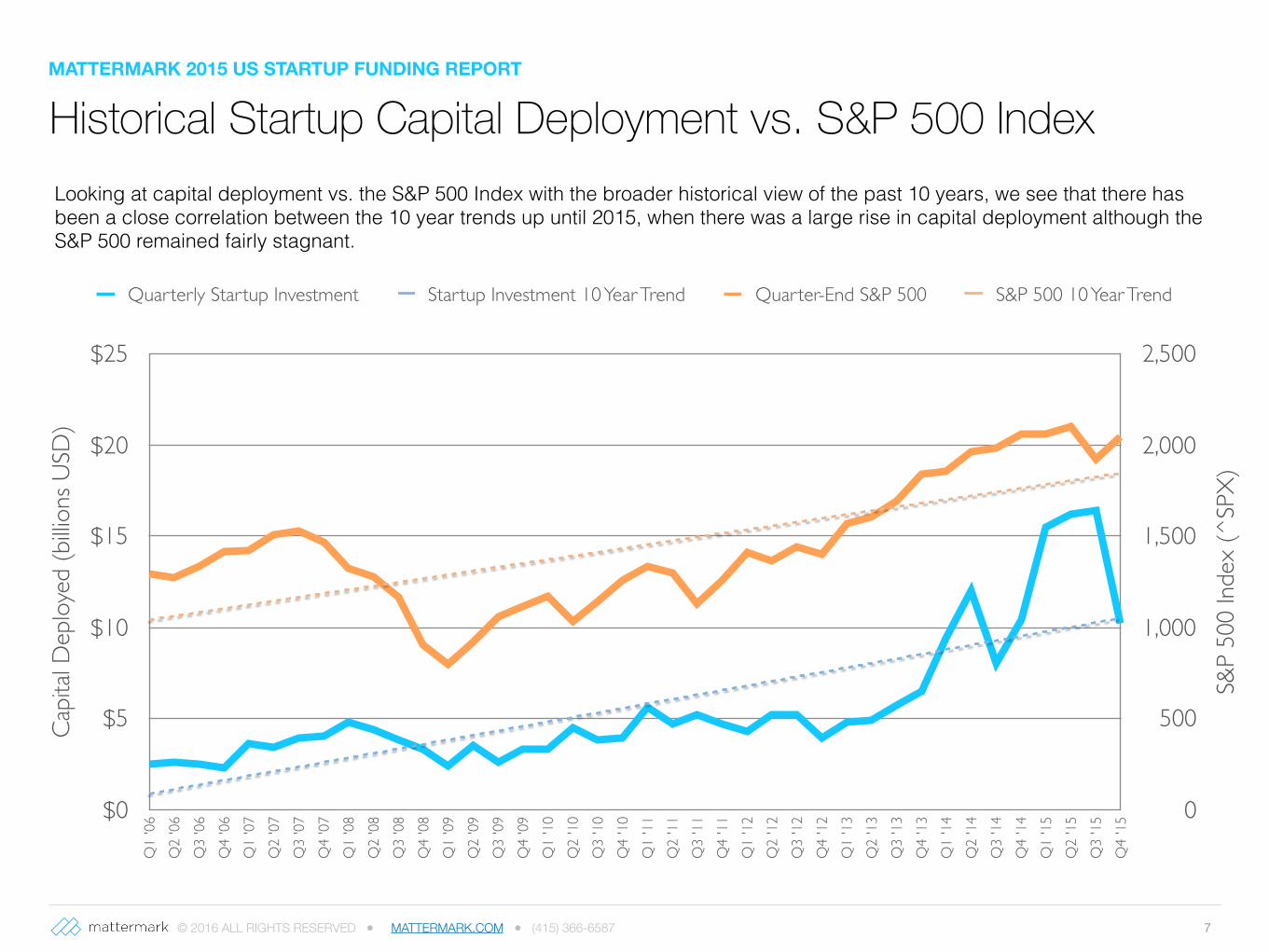

Historical Startup Capital Deployment vs. S&P 500 IndexLooking at capital deployment vs. the S&P 500 Index with the broader historical view of the past 10 years, we see that there has been a close correlation between the 10 year trends up until 2015, when there was a large rise in capital deployment although the S&P 500 remained fairly stagnant.

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-65879

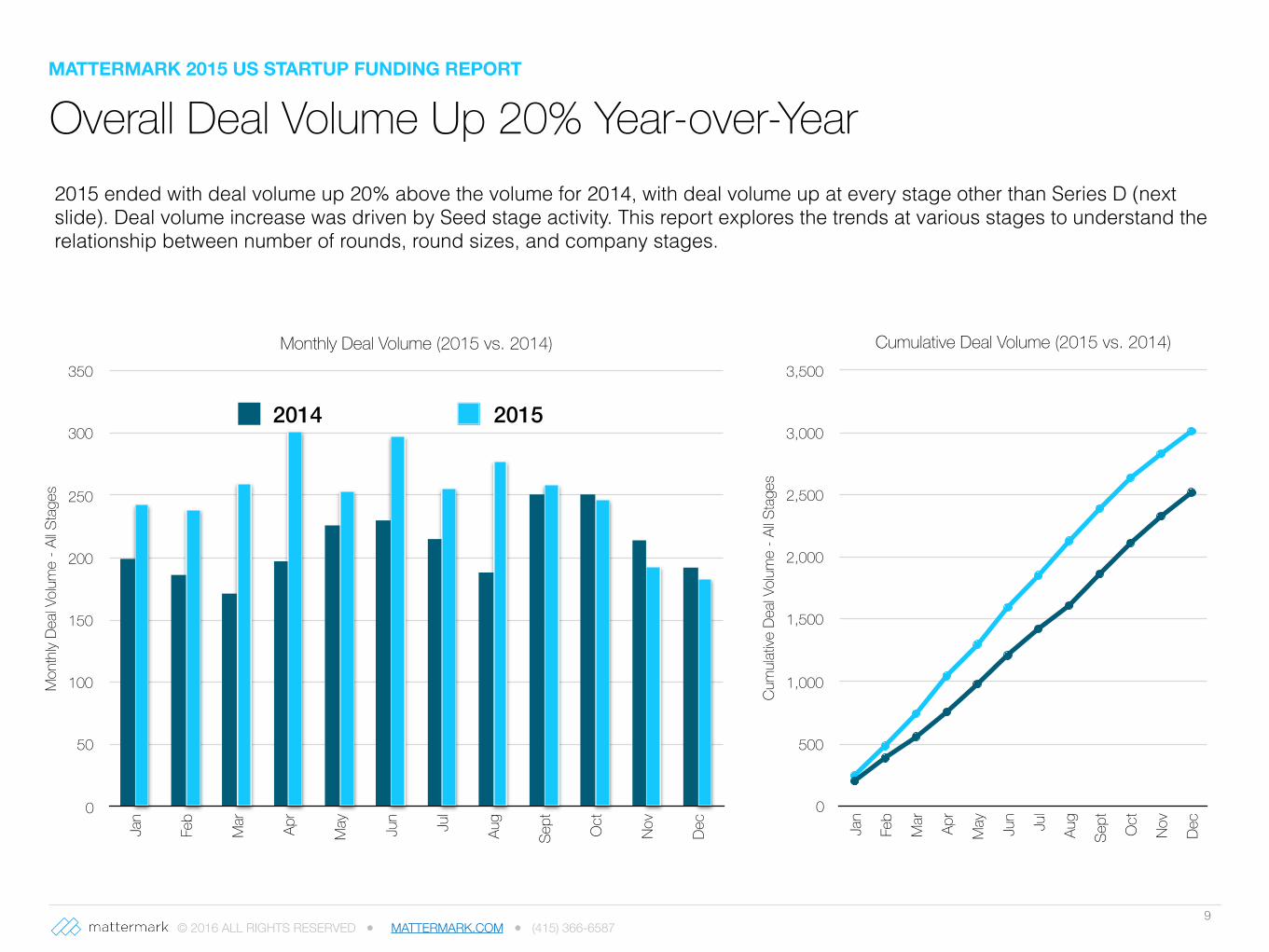

Overall Deal Volume Up 20% Year-over-Year

Monthly Deal Volume (2015 vs. 2014)

Mon

thly

Deal

Volum

e - A

ll Sta

ges

0

50

100

150

200

250

300

350

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

2014 2015

2015 ended with deal volume up 20% above the volume for 2014, with deal volume up at every stage other than Series D (next slide). Deal volume increase was driven by Seed stage activity. This report explores the trends at various stages to understand the relationship between number of rounds, round sizes, and company stages.

Cumulative Deal Volume (2015 vs. 2014)

Cum

ulativ

e De

al Vo

lume

- All S

tage

s

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 10An

nual

Dea

l Vol

ume

by S

tage

0

200

400

600

800

1,000

1,200

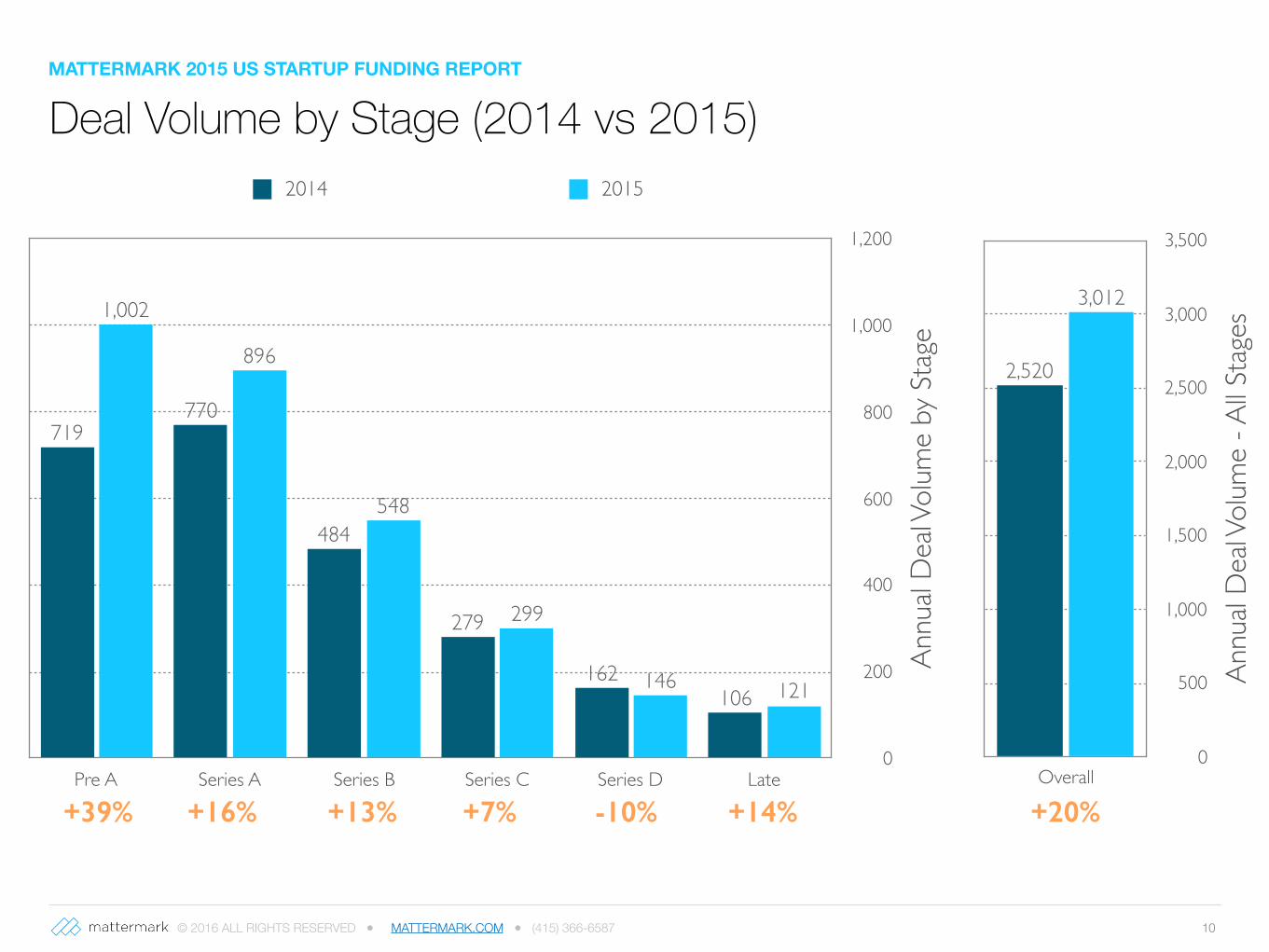

Pre A Series A Series B Series C Series D Late

2014 2015

121146

299

548

896

1,002

106162

279

484

770719

+39% +16% +13% +7% -10% +14%

Annu

al D

eal V

olum

e - A

ll Sta

ges

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Overall

3,012

2,520

+20%

Deal Volume by Stage (2014 vs 2015)MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658711

Capital Deployment by Month (2015 vs. 2014)

Mon

thly

Capi

tal D

eploy

ed -

All S

tage

s (b

illions

USD

)

$0

$1

$2

$3

$4

$5

$6

$7

$8

Jan

Feb

Mar Apr

May Jun

July

Aug

Sept Oct

Nov

Dec

2014 2015

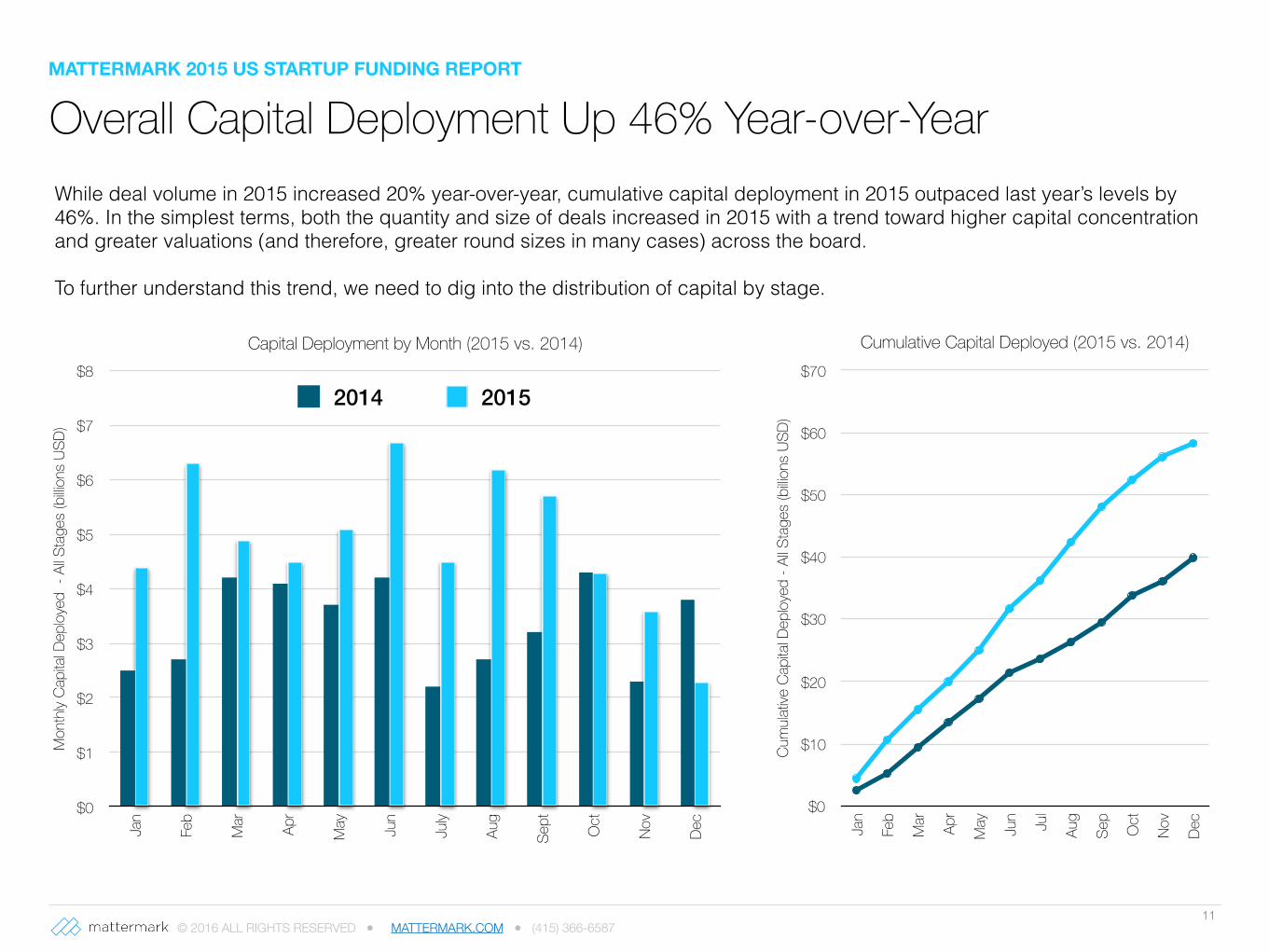

While deal volume in 2015 increased 20% year-over-year, cumulative capital deployment in 2015 outpaced last year’s levels by 46%. In the simplest terms, both the quantity and size of deals increased in 2015 with a trend toward higher capital concentration and greater valuations (and therefore, greater round sizes in many cases) across the board.

To further understand this trend, we need to dig into the distribution of capital by stage.

Cumulative Capital Deployed (2015 vs. 2014)

Cum

ulativ

e Ca

pita

l Dep

loyed

- Al

l Sta

ges

(billio

ns U

SD)

$0

$10

$20

$30

$40

$50

$60

$70

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Overall Capital Deployment Up 46% Year-over-YearMATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 12An

nual

Capi

tal D

eplo

yed

by S

tage

(billi

ons

USD

)

$0

$5

$10

$15

$20

$25

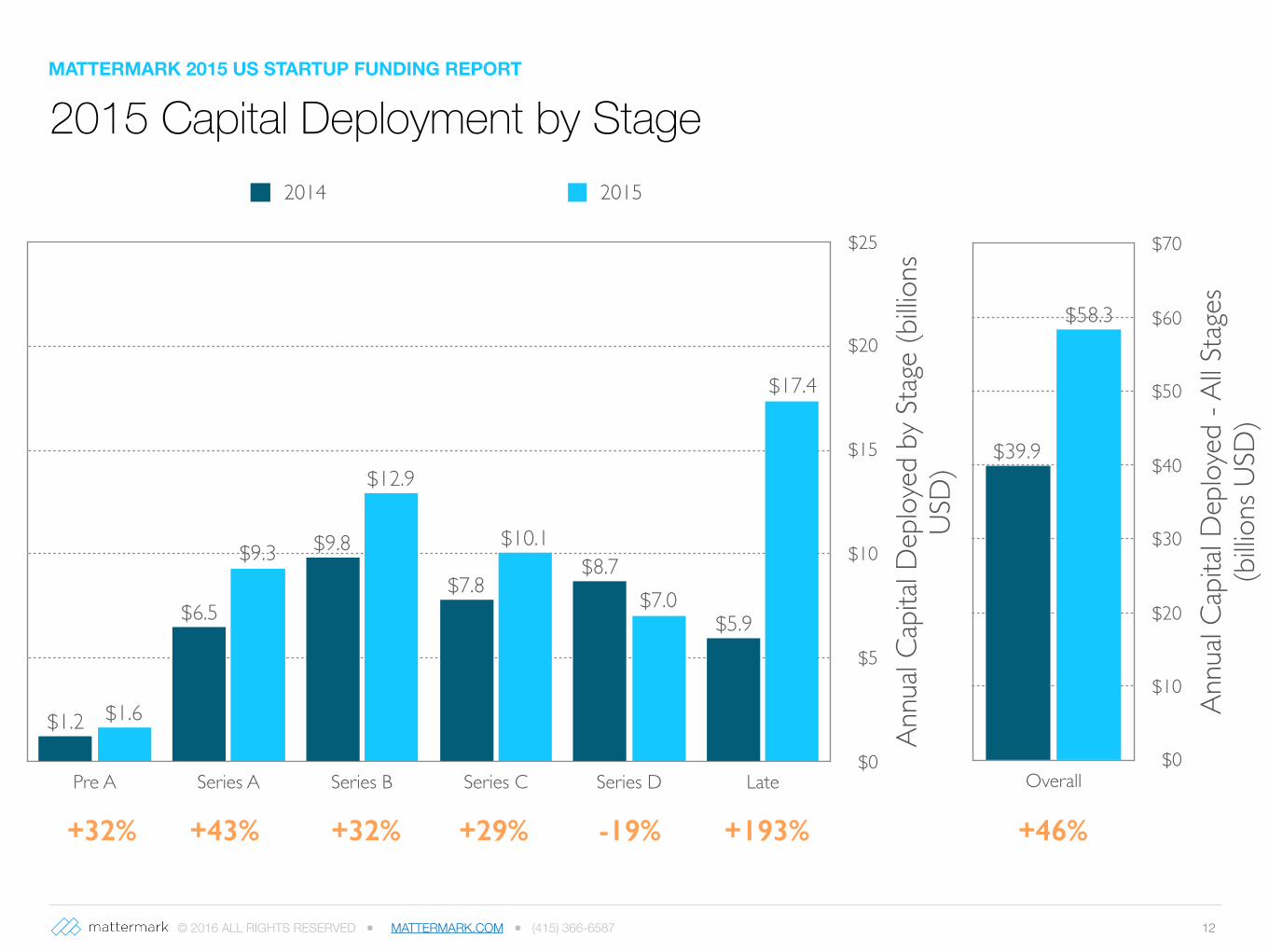

Pre A Series A Series B Series C Series D Late

2014 2015

$17.4

$7.0

$10.1

$12.9

$9.3

$1.6

$5.9

$8.7$7.8

$9.8

$6.5

$1.2

+32% +43% +32% +29% -19% +193%

Annu

al Ca

pita

l Dep

loye

d - A

ll Sta

ges

(billi

ons U

SD)

$0

$10

$20

$30

$40

$50

$60

$70

Overall

$58.3

$39.9

+46%

2015 Capital Deployment by StageMATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 14

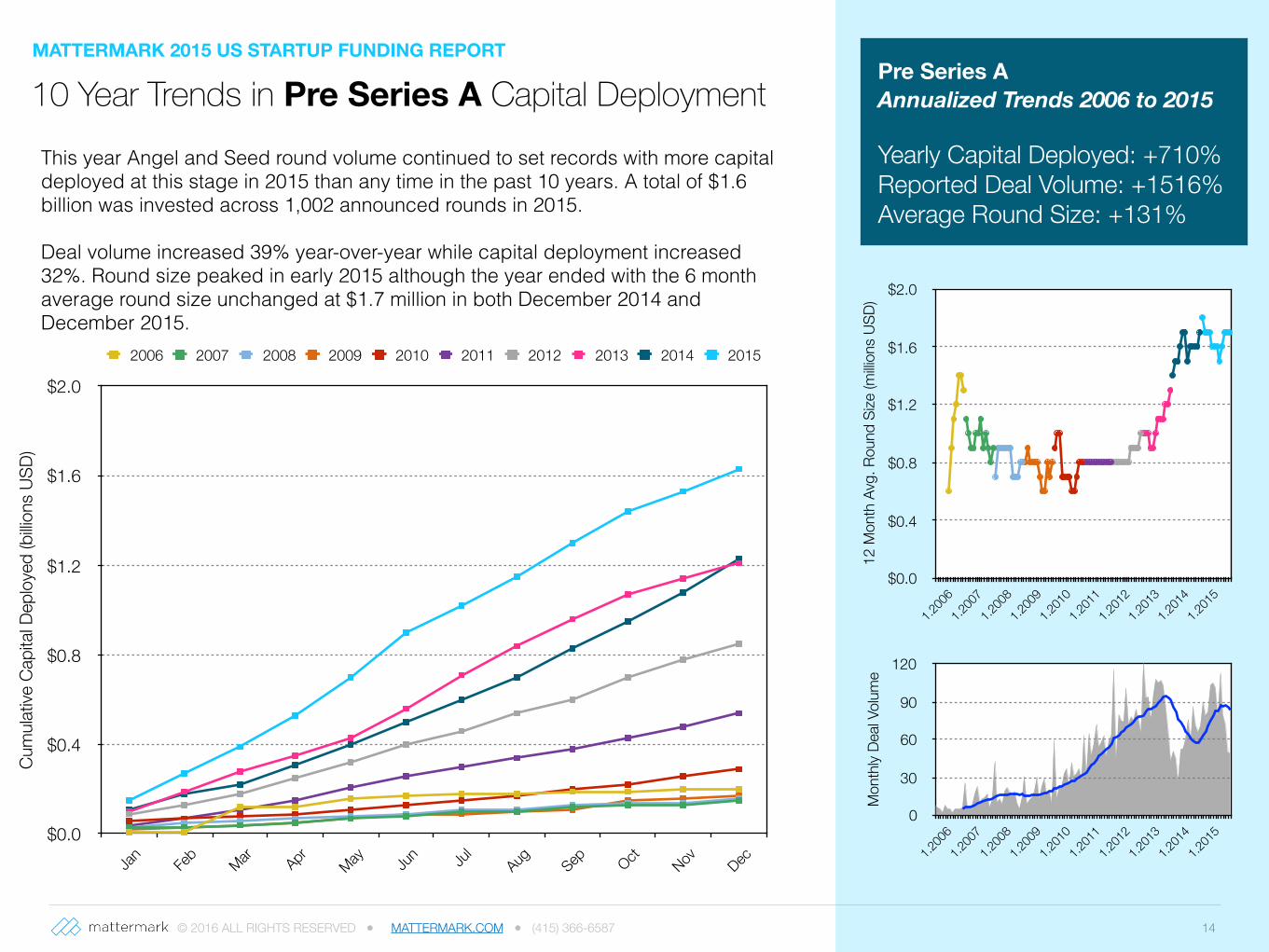

10 Year Trends in Pre Series A Capital DeploymentMATTERMARK 2015 US STARTUP FUNDING REPORT

Cum

ulativ

e Ca

pita

l Dep

loye

d (b

illion

s US

D)

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

Jan Feb

Mar Apr May Jun Ju

lAug Sep Oct Nov Dec

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Pre Series A Annualized Trends 2006 to 2015

Yearly Capital Deployed: +710% Reported Deal Volume: +1516% Average Round Size: +131%

12 M

onth

Avg

. Rou

nd S

ize (m

illion

s US

D)

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Mon

thly

Deal

Volum

e

0

30

60

90

120

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

This year Angel and Seed round volume continued to set records with more capital deployed at this stage in 2015 than any time in the past 10 years. A total of $1.6 billion was invested across 1,002 announced rounds in 2015.

Deal volume increased 39% year-over-year while capital deployment increased 32%. Round size peaked in early 2015 although the year ended with the 6 month average round size unchanged at $1.7 million in both December 2014 and December 2015.

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658715

Mon

thly

Capi

tal D

eploy

ed (m

illions

USD

)

$0

$40

$80

$120

$160

$200Ja

n

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec Cu

mula

tive

Capi

tal D

eploy

ed (m

illions

USD

)

$0

$400

$800

$1,200

$1,600

$2,000

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

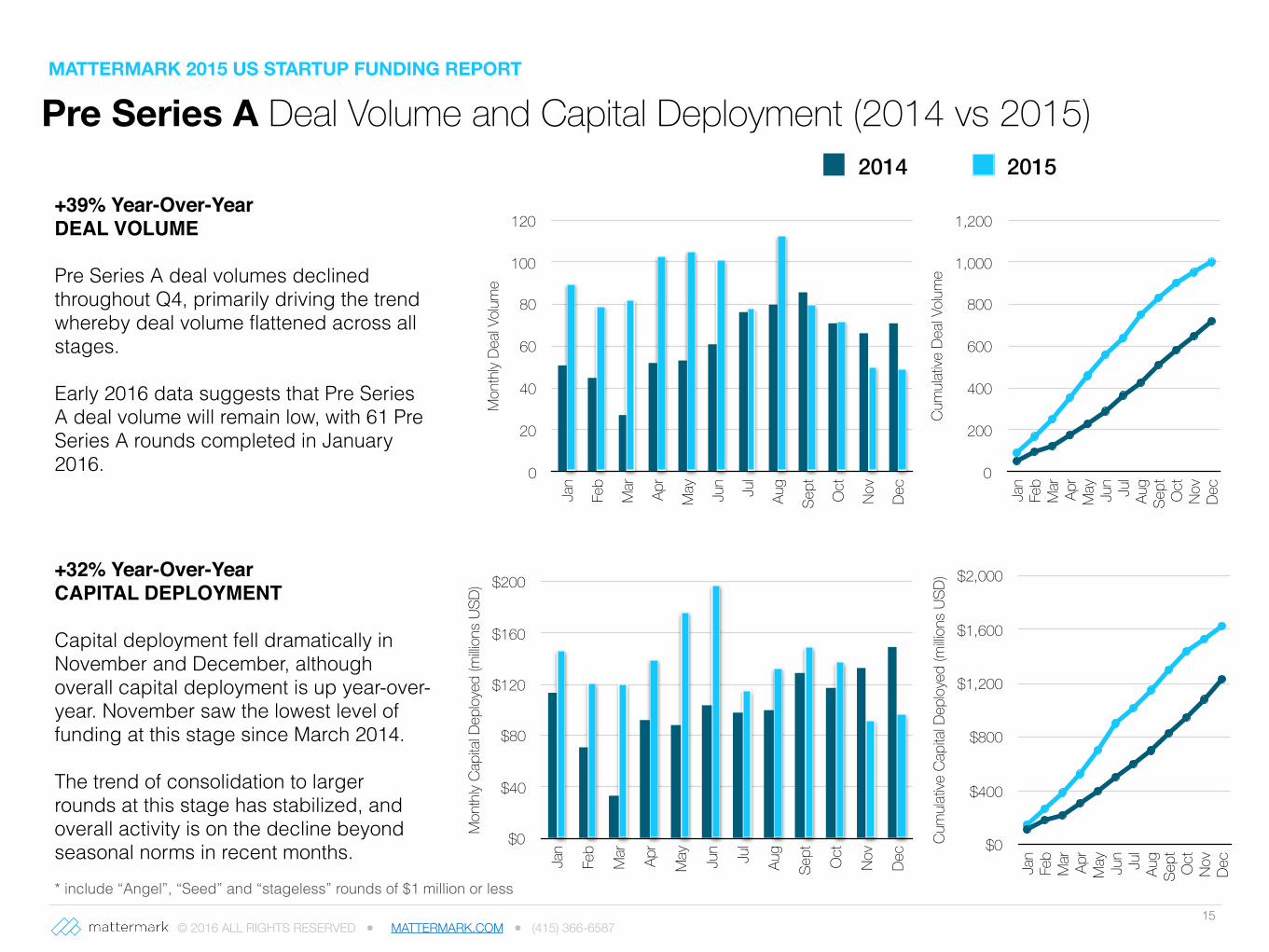

Pre Series A Deal Volume and Capital Deployment (2014 vs 2015)

Mon

thly

Deal

Volum

e0

20

40

60

80

100

120

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

2014 2015

Cum

ulativ

e De

al Vo

lume

0

200

400

600

800

1,000

1,200

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

+39% Year-Over-YearDEAL VOLUME

Pre Series A deal volumes declined throughout Q4, primarily driving the trend whereby deal volume flattened across all stages.

Early 2016 data suggests that Pre Series A deal volume will remain low, with 61 Pre Series A rounds completed in January 2016.

+32% Year-Over-YearCAPITAL DEPLOYMENT

Capital deployment fell dramatically in November and December, although overall capital deployment is up year-over-year. November saw the lowest level of funding at this stage since March 2014.

The trend of consolidation to larger rounds at this stage has stabilized, and overall activity is on the decline beyond seasonal norms in recent months.* include “Angel”, “Seed” and “stageless” rounds of $1 million or less

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658716

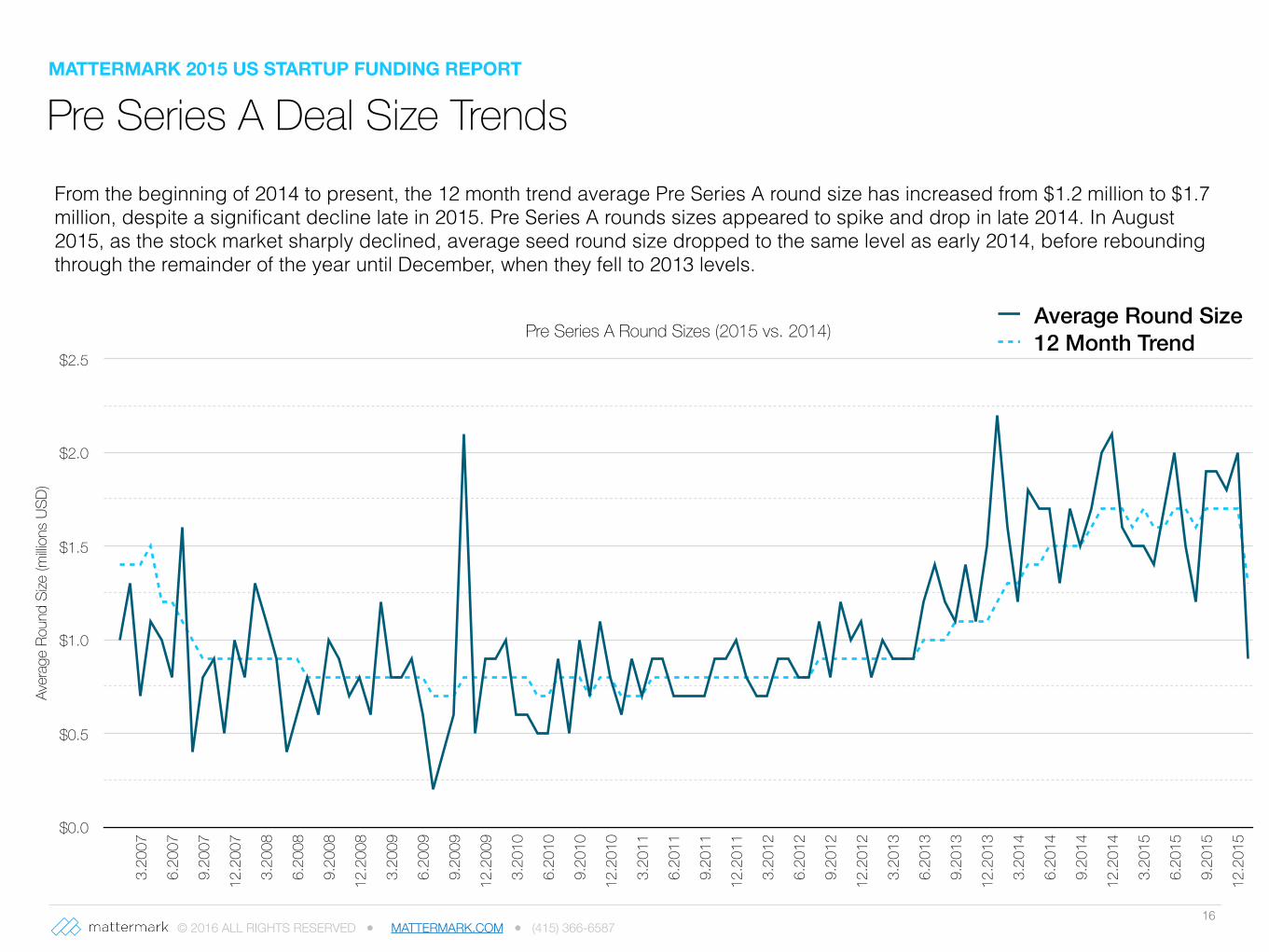

From the beginning of 2014 to present, the 12 month trend average Pre Series A round size has increased from $1.2 million to $1.7 million, despite a significant decline late in 2015. Pre Series A rounds sizes appeared to spike and drop in late 2014. In August 2015, as the stock market sharply declined, average seed round size dropped to the same level as early 2014, before rebounding through the remainder of the year until December, when they fell to 2013 levels.

Pre Series A Round Sizes (2015 vs. 2014)

Aver

age

Roun

d Si

ze (m

illions

USD

)

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

3.20

07

6.20

07

9.20

07

12.2

007

3.20

08

6.20

08

9.20

08

12.2

008

3.20

09

6.20

09

9.20

09

12.2

009

3.20

10

6.20

10

9.20

10

12.2

010

3.20

11

6.20

11

9.20

11

12.2

011

3.20

12

6.20

12

9.20

12

12.2

012

3.20

13

6.20

13

9.20

13

12.2

013

3.20

14

6.20

14

9.20

14

12.2

014

3.20

15

6.20

15

9.20

15

12.2

015

Average Round Size12 Month Trend

Pre Series A Deal Size TrendsMATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658717

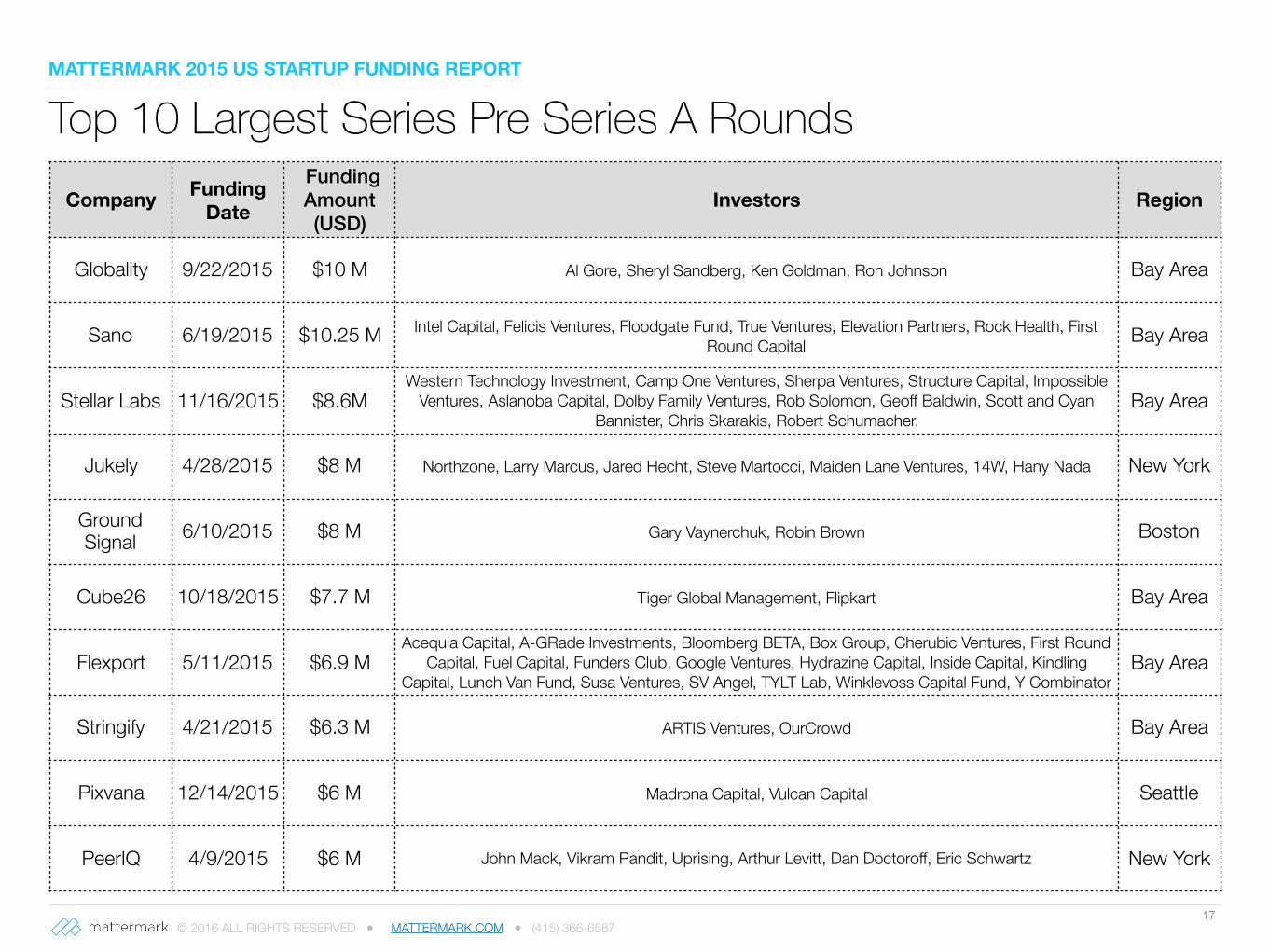

Top 10 Largest Series Pre Series A RoundsCompany Funding

Date

Funding Amount (USD)

Investors Region

Globality 9/22/2015 $10 M Al Gore, Sheryl Sandberg, Ken Goldman, Ron Johnson Bay Area

Sano 6/19/2015 $10.25 M Intel Capital, Felicis Ventures, Floodgate Fund, True Ventures, Elevation Partners, Rock Health, First Round Capital Bay Area

Stellar Labs 11/16/2015 $8.6MWestern Technology Investment, Camp One Ventures, Sherpa Ventures, Structure Capital, Impossible

Ventures, Aslanoba Capital, Dolby Family Ventures, Rob Solomon, Geoff Baldwin, Scott and Cyan Bannister, Chris Skarakis, Robert Schumacher.

Bay Area

Jukely 4/28/2015 $8 M Northzone, Larry Marcus, Jared Hecht, Steve Martocci, Maiden Lane Ventures, 14W, Hany Nada New York

Ground Signal 6/10/2015 $8 M Gary Vaynerchuk, Robin Brown Boston

Cube26 10/18/2015 $7.7 M Tiger Global Management, Flipkart Bay Area

Flexport 5/11/2015 $6.9 MAcequia Capital, A-GRade Investments, Bloomberg BETA, Box Group, Cherubic Ventures, First Round

Capital, Fuel Capital, Funders Club, Google Ventures, Hydrazine Capital, Inside Capital, Kindling Capital, Lunch Van Fund, Susa Ventures, SV Angel, TYLT Lab, Winklevoss Capital Fund, Y Combinator

Bay Area

Stringify 4/21/2015 $6.3 M ARTIS Ventures, OurCrowd Bay Area

Pixvana 12/14/2015 $6 M Madrona Capital, Vulcan Capital Seattle

PeerIQ 4/9/2015 $6 M John Mack, Vikram Pandit, Uprising, Arthur Levitt, Dan Doctoroff, Eric Schwartz New York

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 19

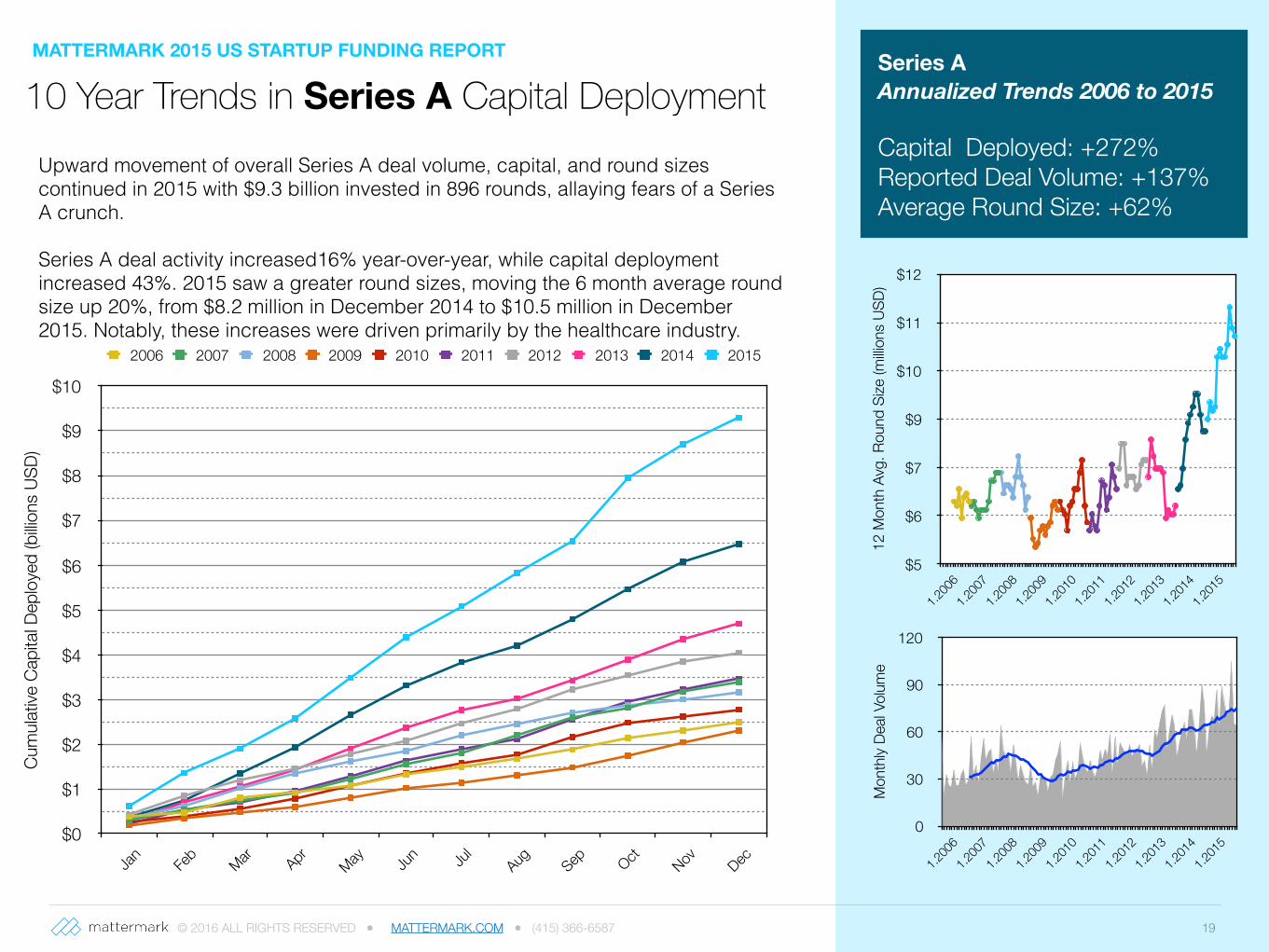

10 Year Trends in Series A Capital DeploymentMATTERMARK 2015 US STARTUP FUNDING REPORT

Cum

ulativ

e Ca

pita

l Dep

loye

d (b

illion

s US

D)

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

Jan Feb

Mar Apr May Jun Ju

lAug Sep Oct Nov Dec

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Series A Annualized Trends 2006 to 2015

Capital Deployed: +272% Reported Deal Volume: +137% Average Round Size: +62%

12 M

onth

Avg

. Rou

nd S

ize (m

illion

s US

D)

$5

$6

$7

$9

$10

$11

$12

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Mon

thly

Deal

Volum

e

0

30

60

90

120

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Upward movement of overall Series A deal volume, capital, and round sizes continued in 2015 with $9.3 billion invested in 896 rounds, allaying fears of a Series A crunch.

Series A deal activity increased16% year-over-year, while capital deployment increased 43%. 2015 saw a greater round sizes, moving the 6 month average round size up 20%, from $8.2 million in December 2014 to $10.5 million in December 2015. Notably, these increases were driven primarily by the healthcare industry.

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658720

Mon

thly

Capi

tal D

eploy

ed (b

illions

USD

)

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Cumulative Capital Deployed

Cum

ulativ

e Ca

pita

l Dep

loyed

(billio

ns U

SD)

$0

$2

$4

$6

$8

$10

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Mon

thly

Deal

Volum

e0

20

40

60

80

100

120

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

2014 2015

Cum

ulativ

e De

al Vo

lume

0

200

400

600

800

1,000

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

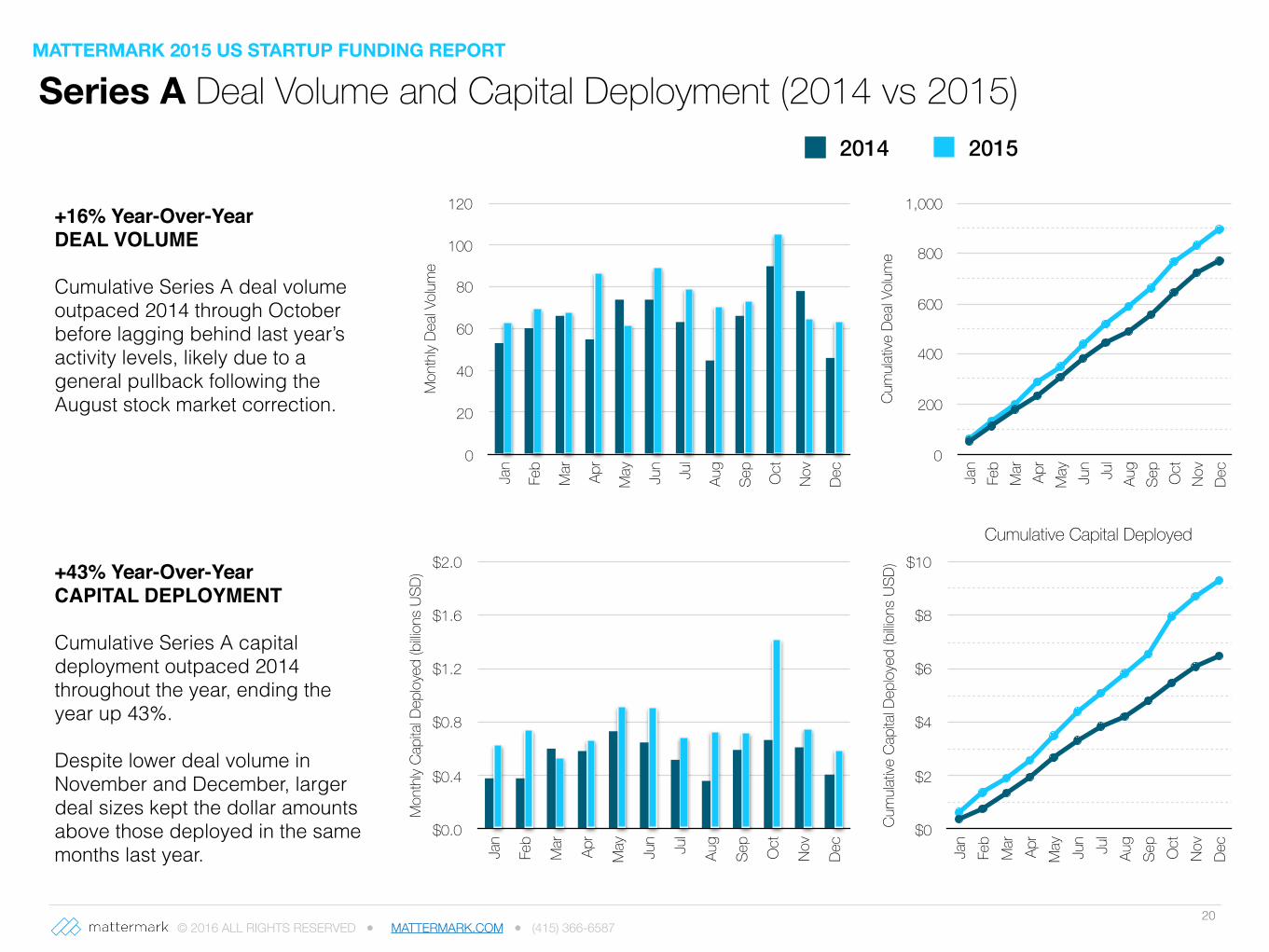

+16% Year-Over-YearDEAL VOLUME

Cumulative Series A deal volume outpaced 2014 through October before lagging behind last year’s activity levels, likely due to a general pullback following the August stock market correction.

+43% Year-Over-YearCAPITAL DEPLOYMENT

Cumulative Series A capital deployment outpaced 2014 throughout the year, ending the year up 43%.

Despite lower deal volume in November and December, larger deal sizes kept the dollar amounts above those deployed in the same months last year.

MATTERMARK 2015 US STARTUP FUNDING REPORT

Series A Deal Volume and Capital Deployment (2014 vs 2015)

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658721

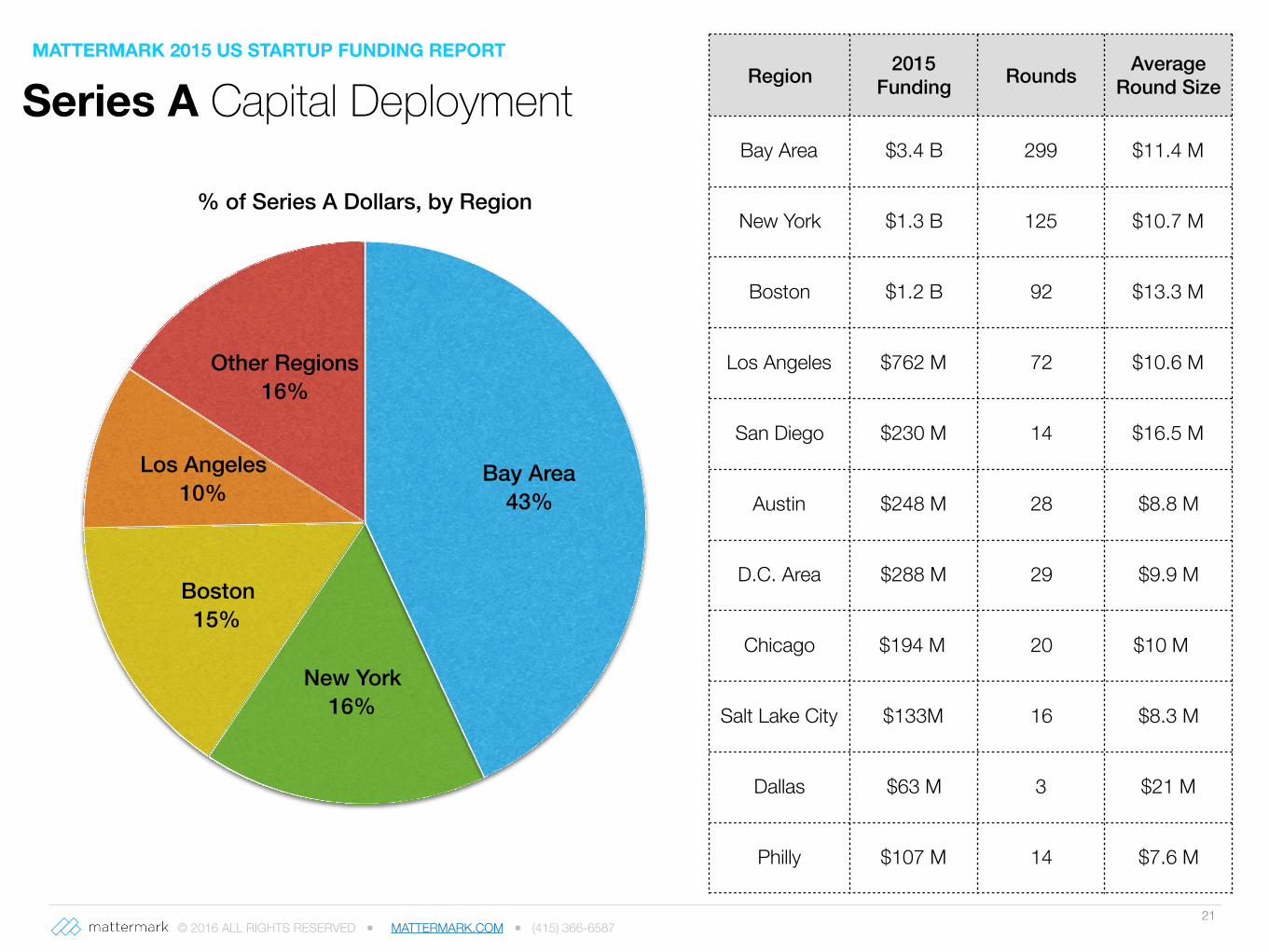

% of Series A Dollars, by Region

Other Regions 16%

Los Angeles 10%

Boston 15%

New York 16%

Bay Area 43%

Series A Capital DeploymentMATTERMARK 2015 US STARTUP FUNDING REPORT

Region 2015 Funding Rounds Average

Round Size

Bay Area $3.4 B 299 $11.4 M

New York $1.3 B 125 $10.7 M

Boston $1.2 B 92 $13.3 M

Los Angeles $762 M 72 $10.6 M

San Diego $230 M 14 $16.5 M

Austin $248 M 28 $8.8 M

D.C. Area $288 M 29 $9.9 M

Chicago $194 M 20 $10 M

Salt Lake City $133M 16 $8.3 M

Dallas $63 M 3 $21 M

Philly $107 M 14 $7.6 M

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658722

The Largest Series A Rounds in 2015Company Date Amount

(USD) Investors Region

Karhoo 10/29/2015 $250 M Nick Gatfield, David Kowitz New York

Denali Therapeutics 5/14/2015 $217 M Flagship Ventures, ARCH Venture Partners, F-Prime Capital Partners, Alaska Permanent Fund Bay Area

Gritstone Oncology 10/20/2015 $102 M Frazier Healthcare Ventures, Clarus Ventures, Versant Ventures, The Column Group, Redmile Group, Casdin Capital, Transformational Healthcare Opportunity Bay Area

Clover Health 9/17/2015 $100 M Athyrium Capital Management, First Round Capital Bay Area

Turing Pharmaceuticals 8/10/2015 $90 M Martin Shkreli New York

Calhoun Vision 6/4/2015 $69 M Longitude Capital, RA Capital Management, H.I.G. BioVentures Los Angeles

NerdWallet 5/12/2015 $64 M RRE Ventures, iGlobe Partners, Institutional Venture Partners (IVP) Bay Area

Atreca 10/20/2015 $56 M Bill & Melinda Gates Foundation, Mission Bay Capital, GlaxoSmithKline Bay Area

Neon Therapeutics 10/1/2015 $55 M Clal Biotechnology Industries, Access Industries, Rock Ventures Boston

Decibel Therapeutics 10/14/2015 $52 M SR One, Third Rock Ventures Boston

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 24

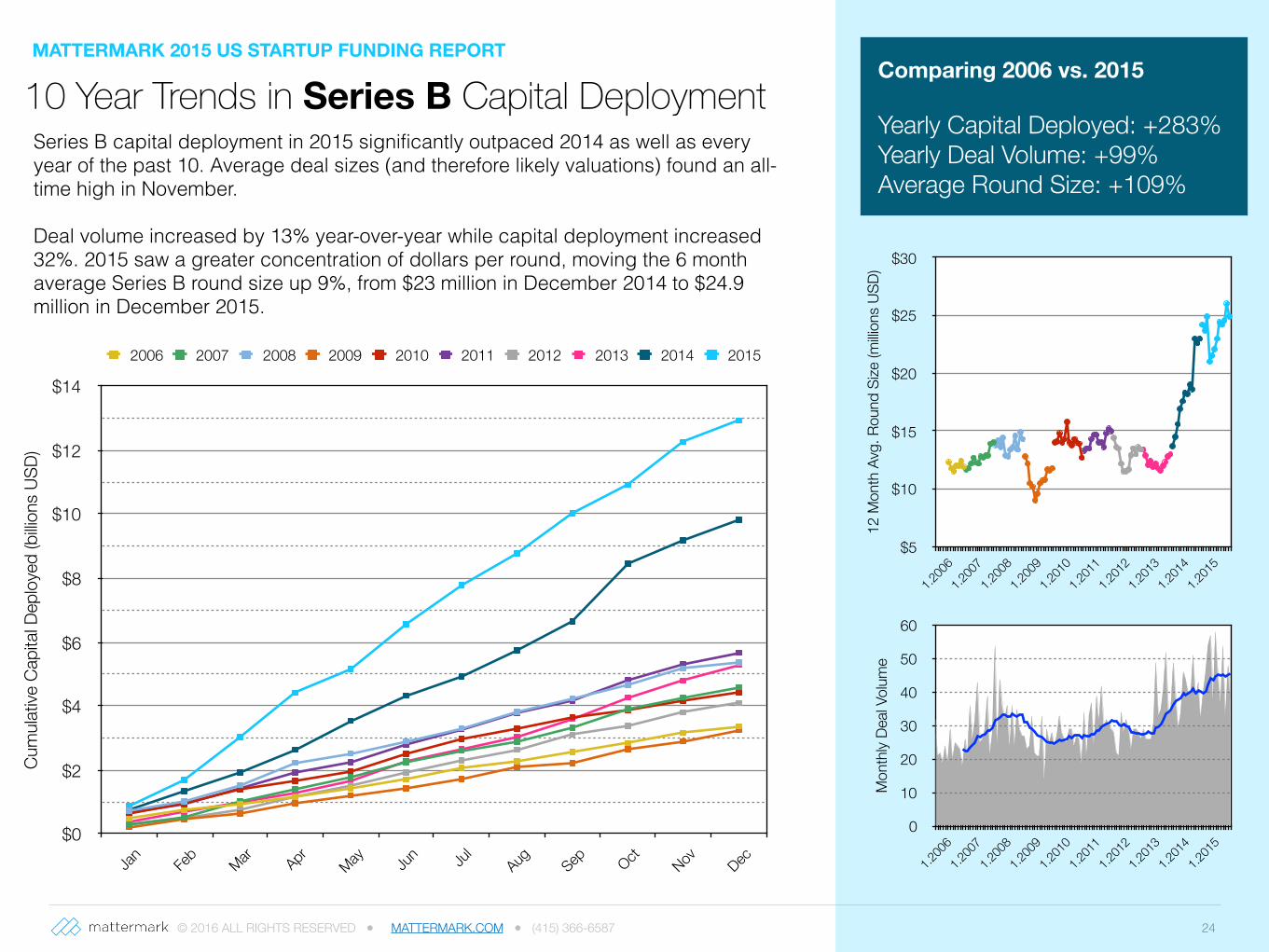

10 Year Trends in Series B Capital DeploymentMATTERMARK 2015 US STARTUP FUNDING REPORT

Cum

ulativ

e Ca

pita

l Dep

loye

d (b

illion

s US

D)

$0

$2

$4

$6

$8

$10

$12

$14

Jan Feb

Mar Apr May Jun Ju

lAug Sep Oct Nov Dec

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Comparing 2006 vs. 2015

Yearly Capital Deployed: +283% Yearly Deal Volume: +99% Average Round Size: +109%

12 M

onth

Avg

. Rou

nd S

ize (m

illion

s US

D)

$5

$10

$15

$20

$25

$30

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Mon

thly

Deal

Volum

e

0

10

20

30

40

50

60

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

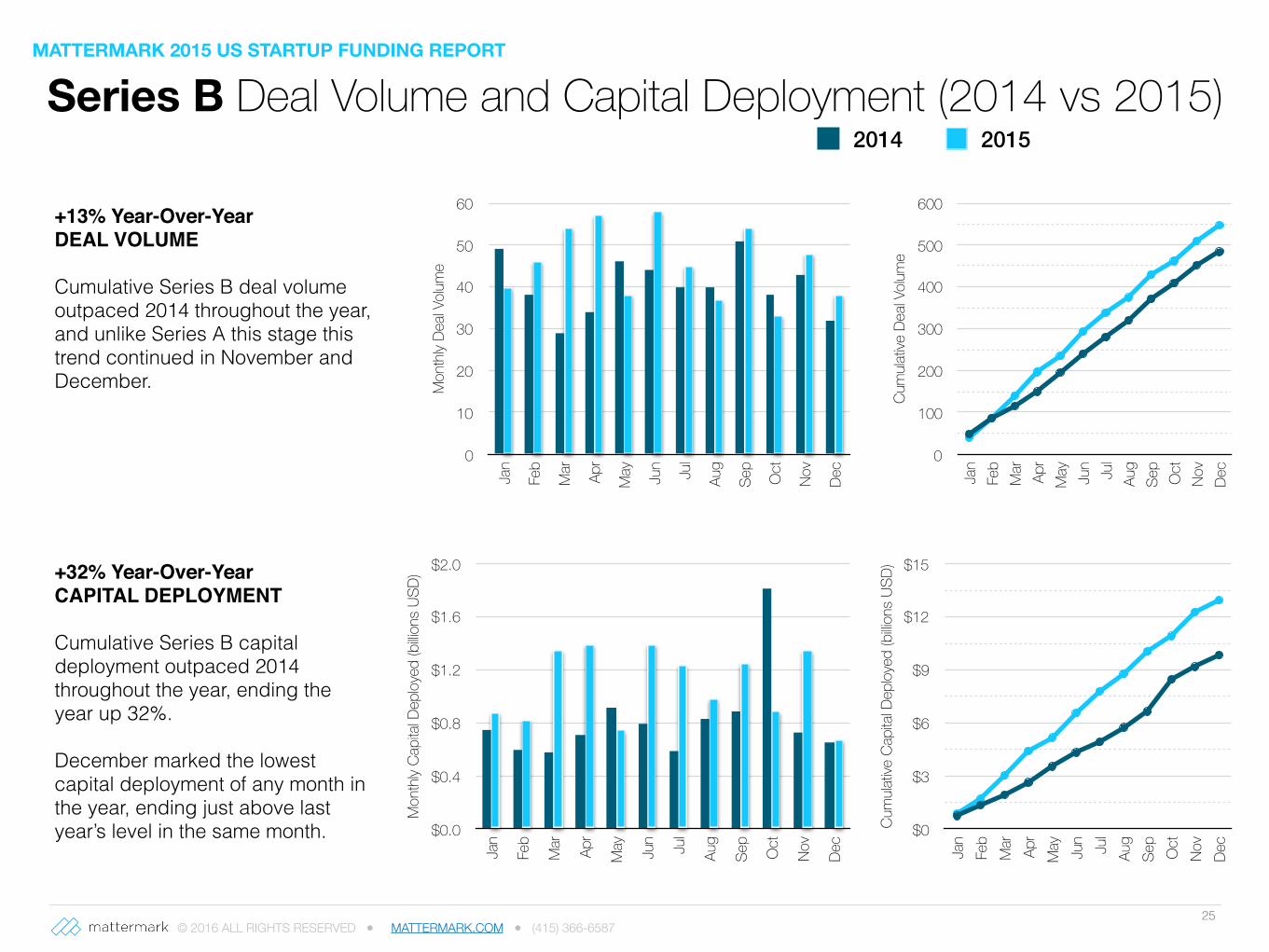

Series B capital deployment in 2015 significantly outpaced 2014 as well as every year of the past 10. Average deal sizes (and therefore likely valuations) found an all-time high in November.

Deal volume increased by 13% year-over-year while capital deployment increased 32%. 2015 saw a greater concentration of dollars per round, moving the 6 month average Series B round size up 9%, from $23 million in December 2014 to $24.9 million in December 2015.

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587

Series B Deal Volume and Capital Deployment (2014 vs 2015)

25

Mon

thly

Capi

tal D

eploy

ed (b

illions

USD

)

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Cum

ulativ

e Ca

pita

l Dep

loyed

(billio

ns U

SD)

$0

$3

$6

$9

$12

$15

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Mon

thly

Deal

Volum

e0

10

20

30

40

50

60

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

2014 2015

Cum

ulativ

e De

al Vo

lume

0

100

200

300

400

500

600

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

+13% Year-Over-YearDEAL VOLUME

Cumulative Series B deal volume outpaced 2014 throughout the year, and unlike Series A this stage this trend continued in November and December.

+32% Year-Over-YearCAPITAL DEPLOYMENT

Cumulative Series B capital deployment outpaced 2014 throughout the year, ending the year up 32%.

December marked the lowest capital deployment of any month in the year, ending just above last year’s level in the same month.

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658726

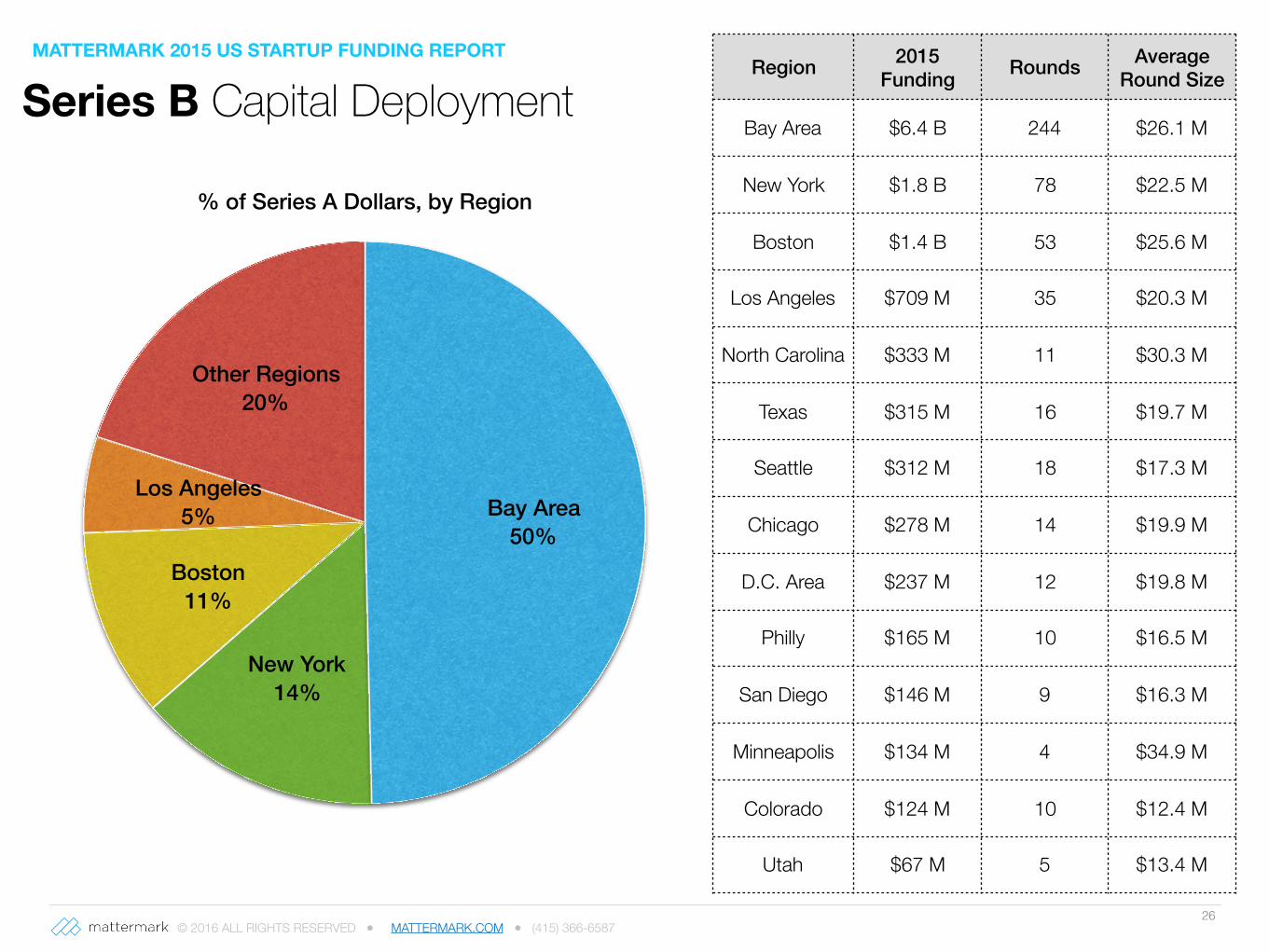

% of Series A Dollars, by Region

Other Regions 20%

Los Angeles 5%

Boston 11%

New York 14%

Bay Area 50%

Series B Capital DeploymentMATTERMARK 2015 US STARTUP FUNDING REPORT

Region 2015 Funding Rounds Average

Round Size

Bay Area $6.4 B 244 $26.1 M

New York $1.8 B 78 $22.5 M

Boston $1.4 B 53 $25.6 M

Los Angeles $709 M 35 $20.3 M

North Carolina $333 M 11 $30.3 M

Texas $315 M 16 $19.7 M

Seattle $312 M 18 $17.3 M

Chicago $278 M 14 $19.9 M

D.C. Area $237 M 12 $19.8 M

Philly $165 M 10 $16.5 M

San Diego $146 M 9 $16.3 M

Minneapolis $134 M 4 $34.9 M

Colorado $124 M 10 $12.4 M

Utah $67 M 5 $13.4 M

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658727

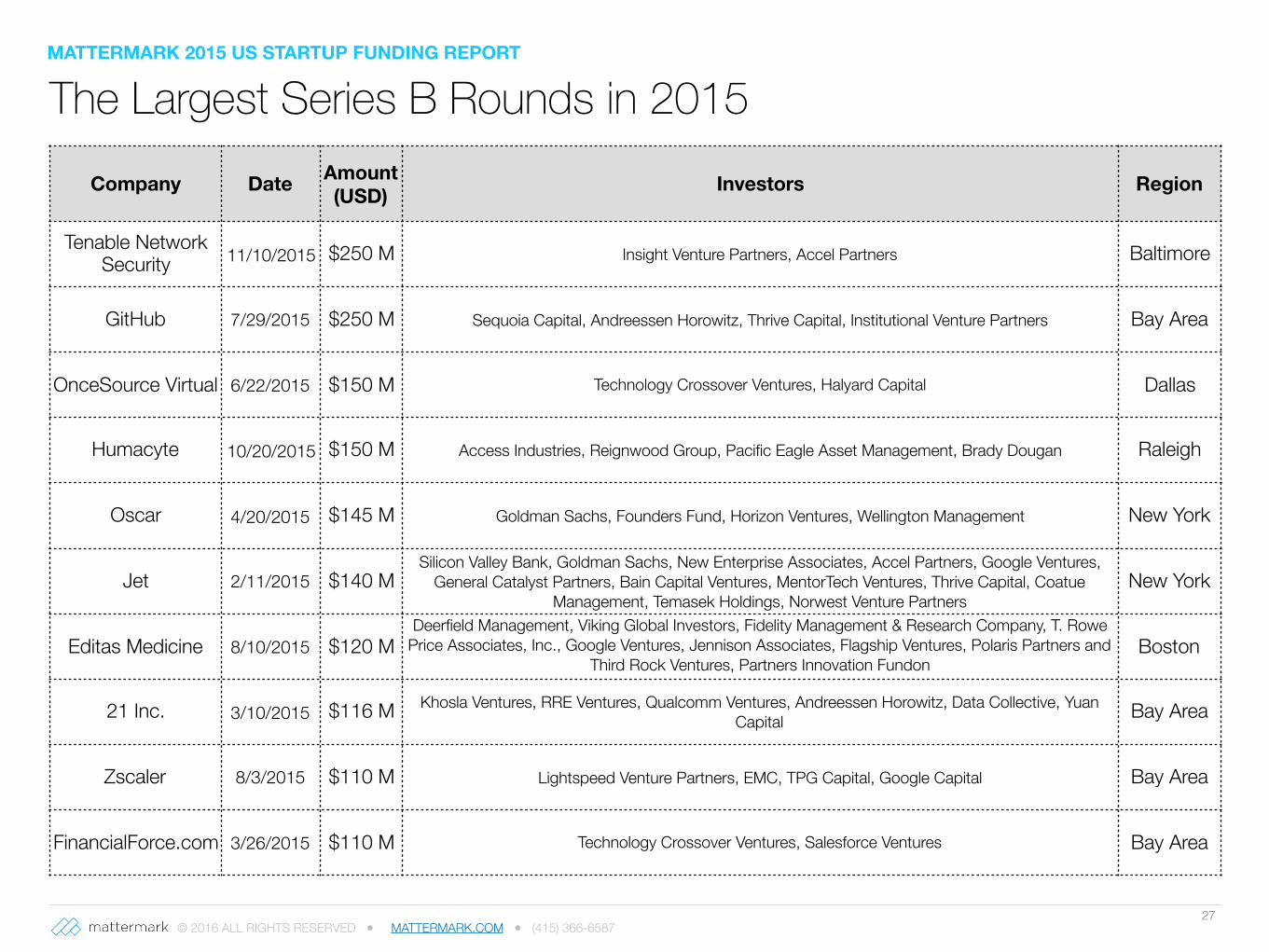

The Largest Series B Rounds in 2015Company Date Amount

(USD) Investors Region

Tenable Network Security 11/10/2015 $250 M Insight Venture Partners, Accel Partners Baltimore

GitHub 7/29/2015 $250 M Sequoia Capital, Andreessen Horowitz, Thrive Capital, Institutional Venture Partners Bay Area

OnceSource Virtual 6/22/2015 $150 M Technology Crossover Ventures, Halyard Capital Dallas

Humacyte 10/20/2015 $150 M Access Industries, Reignwood Group, Pacific Eagle Asset Management, Brady Dougan Raleigh

Oscar 4/20/2015 $145 M Goldman Sachs, Founders Fund, Horizon Ventures, Wellington Management New York

Jet 2/11/2015 $140 MSilicon Valley Bank, Goldman Sachs, New Enterprise Associates, Accel Partners, Google Ventures,

General Catalyst Partners, Bain Capital Ventures, MentorTech Ventures, Thrive Capital, Coatue Management, Temasek Holdings, Norwest Venture Partners

New York

Editas Medicine 8/10/2015 $120 MDeerfield Management, Viking Global Investors, Fidelity Management & Research Company, T. Rowe

Price Associates, Inc., Google Ventures, Jennison Associates, Flagship Ventures, Polaris Partners and Third Rock Ventures, Partners Innovation Fundon

behalf of certain clients, Khosla Ventures, EcoR1 Capital, Casdin Capital, Omega Funds,

Boston

21 Inc. 3/10/2015 $116 M Khosla Ventures, RRE Ventures, Qualcomm Ventures, Andreessen Horowitz, Data Collective, Yuan Capital Bay Area

Zscaler 8/3/2015 $110 M Lightspeed Venture Partners, EMC, TPG Capital, Google Capital Bay Area

FinancialForce.com 3/26/2015 $110 M Technology Crossover Ventures, Salesforce Ventures Bay Area

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 29

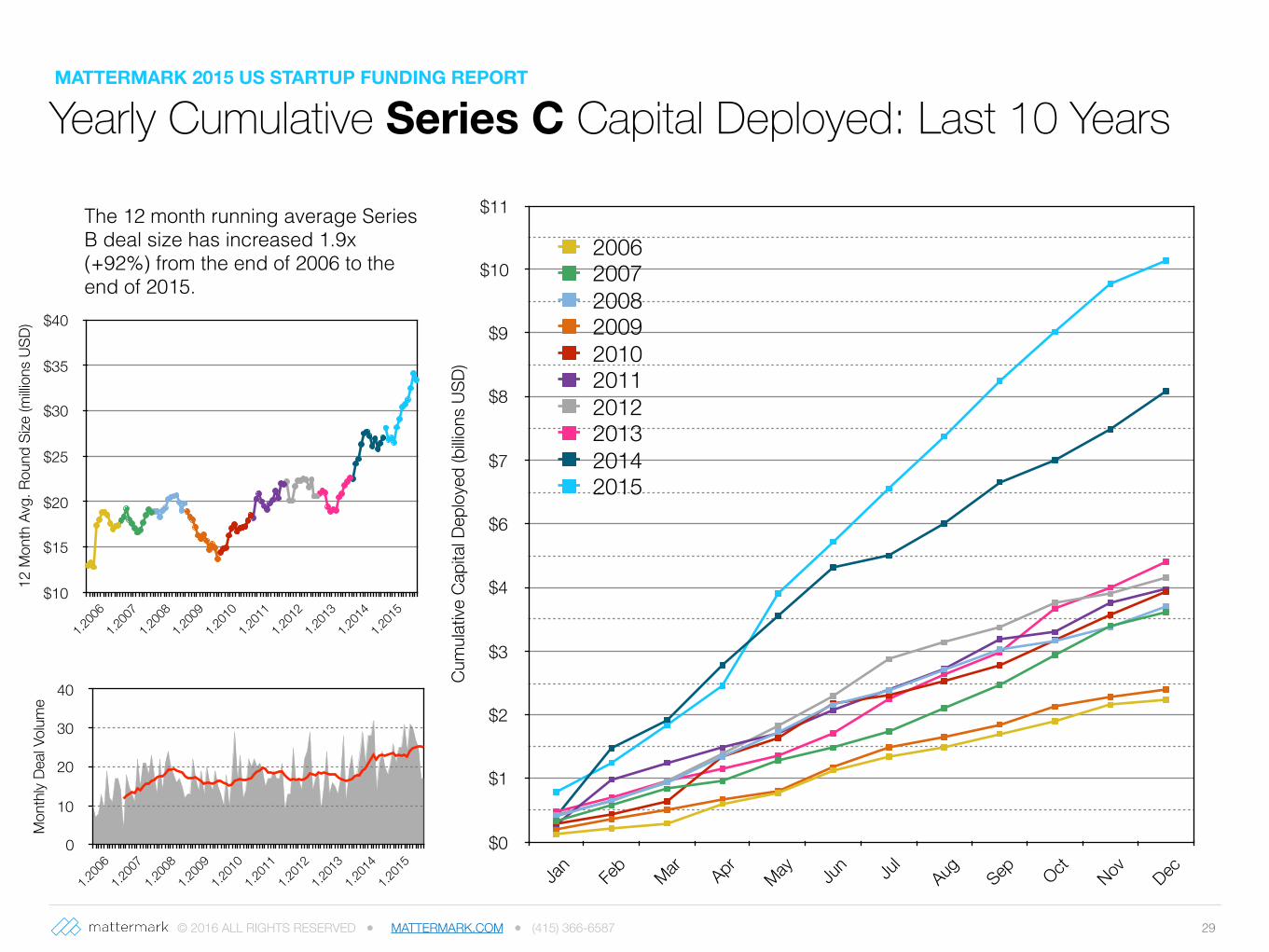

Yearly Cumulative Series C Capital Deployed: Last 10 Years

The 12 month running average Series B deal size has increased 1.9x (+92%) from the end of 2006 to the end of 2015.

Cum

ulativ

e Ca

pita

l Dep

loye

d (b

illion

s US

D)

$0

$1

$2

$3

$4

$6

$7

$8

$9

$10

$11

Jan Feb

Mar Apr May Jun Ju

lAug Sep Oct Nov Dec

2006200720082009201020112012201320142015

12 M

onth

Avg

. Rou

nd S

ize (m

illion

s US

D)

$10

$15

$20

$25

$30

$35

$40

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Mon

thly

Deal

Volum

e

0

10

20

30

40

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587

Series C Deal Volume and Capital Deployment (2014 vs 2015)

30

Mon

thly

Capi

tal D

eploy

ed (b

illions

USD

)

$0.0

$0.5

$1.0

$1.5

$2.0Ja

n

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

Cum

ulativ

e Ca

pita

l Dep

loyed

(billio

ns U

SD)

$0

$3

$6

$9

$12

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

Mon

thly

Deal

Volum

e0

5

10

15

20

25

30

35

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

2014 2015

Cum

ulativ

e De

al Vo

lume

0

50

100

150

200

250

300

350

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

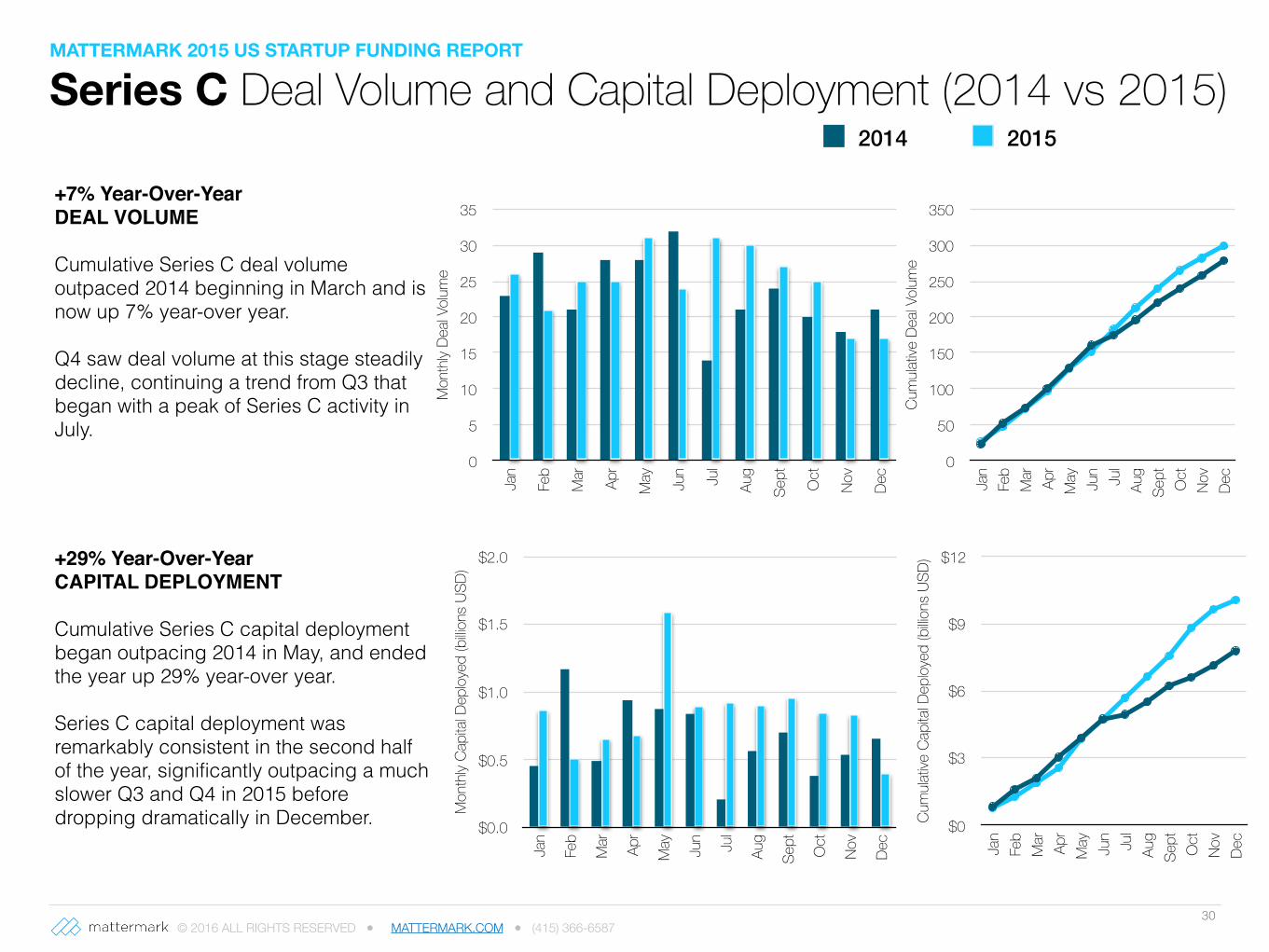

+7% Year-Over-YearDEAL VOLUME

Cumulative Series C deal volume outpaced 2014 beginning in March and is now up 7% year-over year.

Q4 saw deal volume at this stage steadily decline, continuing a trend from Q3 that began with a peak of Series C activity in July.

+29% Year-Over-YearCAPITAL DEPLOYMENT

Cumulative Series C capital deployment began outpacing 2014 in May, and ended the year up 29% year-over year.

Series C capital deployment was remarkably consistent in the second half of the year, significantly outpacing a much slower Q3 and Q4 in 2015 before dropping dramatically in December.

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658731

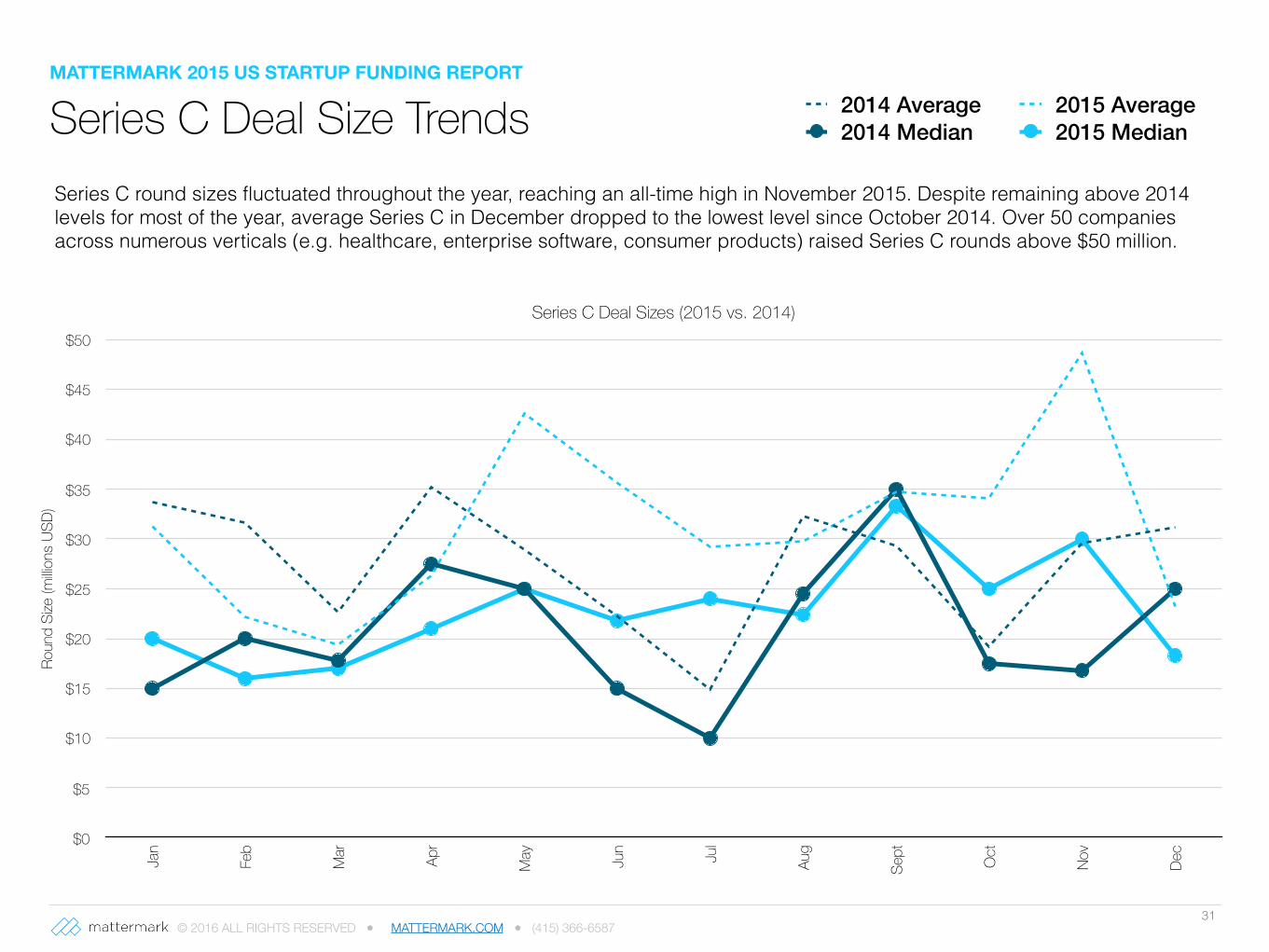

Series C round sizes fluctuated throughout the year, reaching an all-time high in November 2015. Despite remaining above 2014 levels for most of the year, average Series C in December dropped to the lowest level since October 2014. Over 50 companies across numerous verticals (e.g. healthcare, enterprise software, consumer products) raised Series C rounds above $50 million.

Series C Deal Sizes (2015 vs. 2014)

Roun

d Si

ze (m

illions

USD

)

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

2014 Average 2015 Average2014 Median 2015 Median Series C Deal Size Trends

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658732

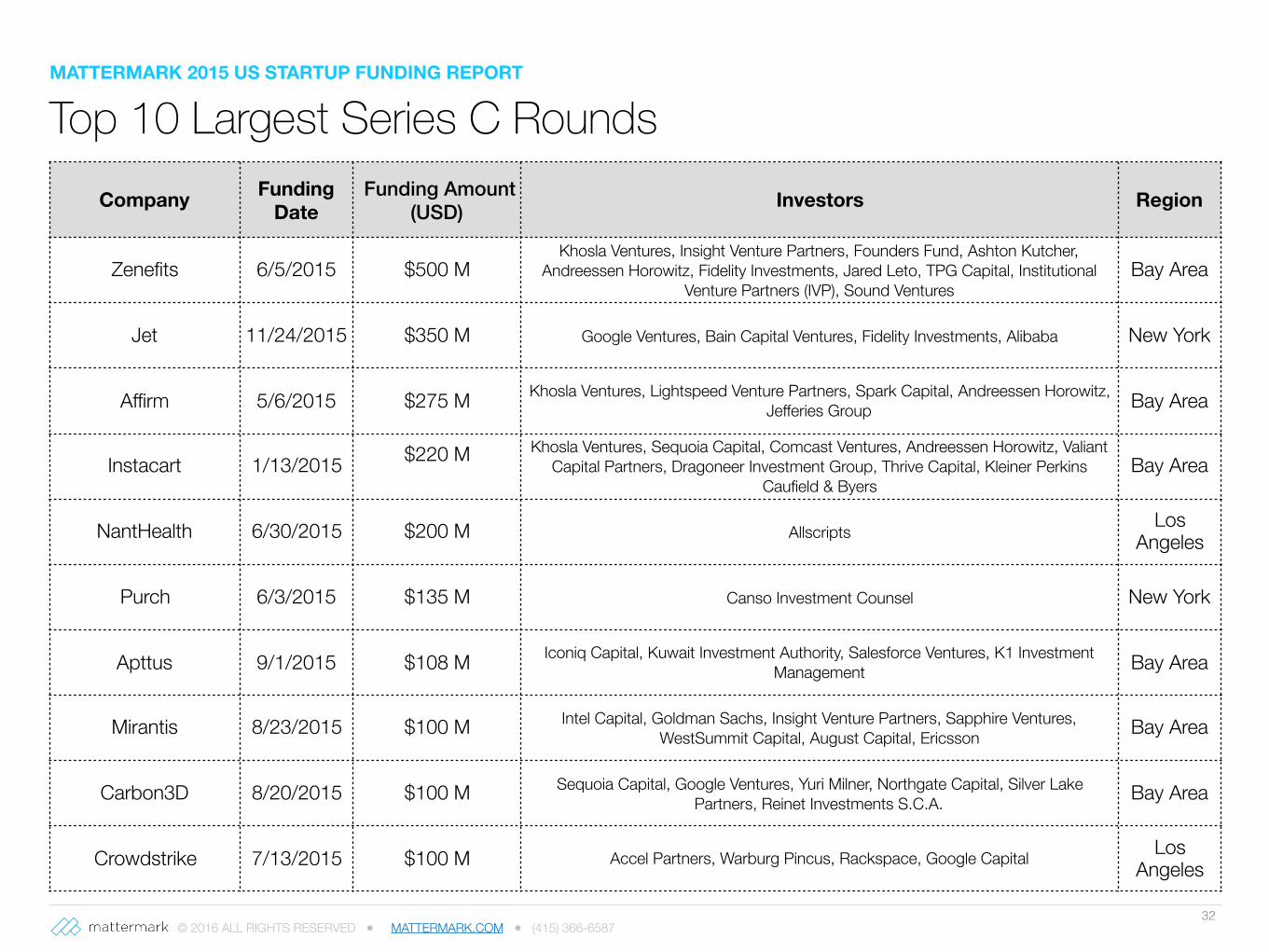

Top 10 Largest Series C RoundsCompany Funding

Date Funding Amount

(USD) Investors Region

Zenefits 6/5/2015 $500 MKhosla Ventures, Insight Venture Partners, Founders Fund, Ashton Kutcher,

Andreessen Horowitz, Fidelity Investments, Jared Leto, TPG Capital, Institutional Venture Partners (IVP), Sound Ventures

Bay Area

Jet 11/24/2015 $350 M Google Ventures, Bain Capital Ventures, Fidelity Investments, Alibaba New York

Affirm 5/6/2015 $275 M Khosla Ventures, Lightspeed Venture Partners, Spark Capital, Andreessen Horowitz, Jefferies Group Bay Area

Instacart 1/13/2015 $220 M Khosla Ventures, Sequoia Capital, Comcast Ventures, Andreessen Horowitz, Valiant Capital Partners, Dragoneer Investment Group, Thrive Capital, Kleiner Perkins

Caufield & ByersBay Area

NantHealth 6/30/2015 $200 M Allscripts Los Angeles

Purch 6/3/2015 $135 M Canso Investment Counsel New York

Apttus 9/1/2015 $108 M Iconiq Capital, Kuwait Investment Authority, Salesforce Ventures, K1 Investment Management Bay Area

Mirantis 8/23/2015 $100 M Intel Capital, Goldman Sachs, Insight Venture Partners, Sapphire Ventures, WestSummit Capital, August Capital, Ericsson Bay Area

Carbon3D 8/20/2015 $100 M Sequoia Capital, Google Ventures, Yuri Milner, Northgate Capital, Silver Lake Partners, Reinet Investments S.C.A. Bay Area

Crowdstrike 7/13/2015 $100 M Accel Partners, Warburg Pincus, Rackspace, Google Capital Los Angeles

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 34

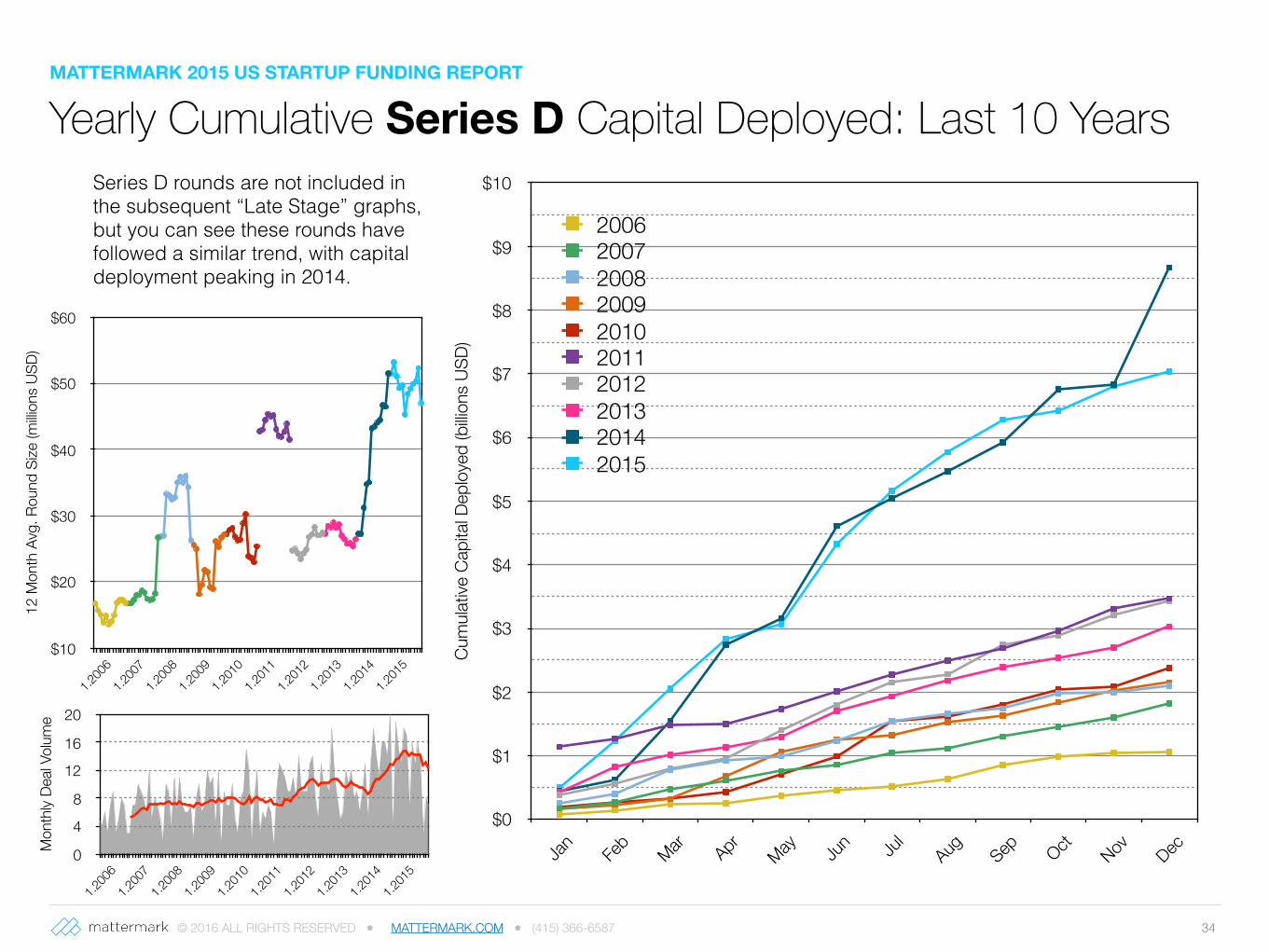

Yearly Cumulative Series D Capital Deployed: Last 10 YearsSeries D rounds are not included in the subsequent “Late Stage” graphs, but you can see these rounds have followed a similar trend, with capital deployment peaking in 2014.

Cum

ulativ

e Ca

pita

l Dep

loye

d (b

illion

s US

D)

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

Jan Feb

Mar Apr May Jun Ju

lAug Sep Oct Nov Dec

2006200720082009201020112012201320142015

12 M

onth

Avg

. Rou

nd S

ize (m

illion

s US

D)

$10

$20

$30

$40

$50

$60

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Mon

thly

Deal

Volum

e

0

4

8

12

16

20

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587 35

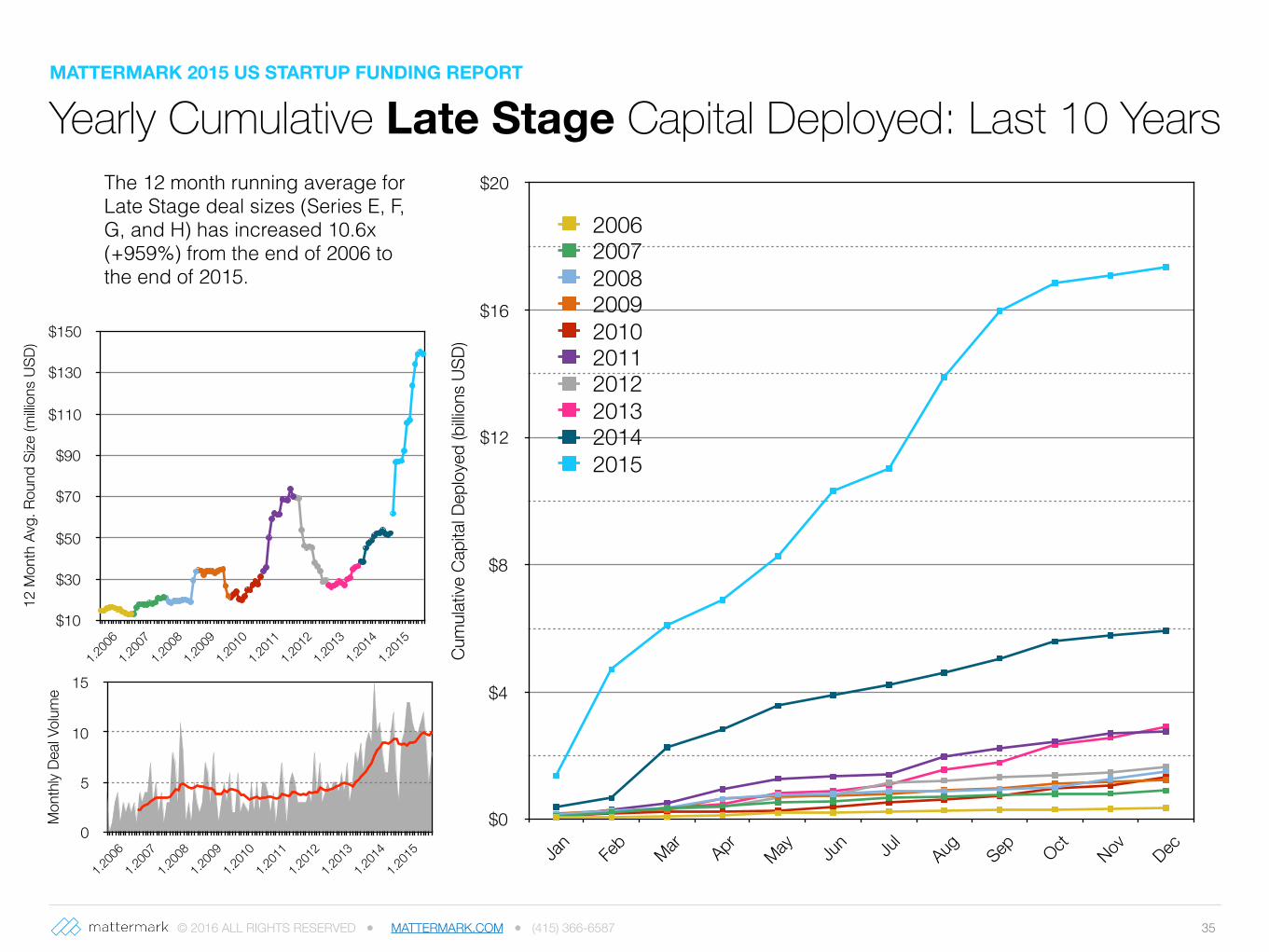

Yearly Cumulative Late Stage Capital Deployed: Last 10 Years

12 M

onth

Avg

. Rou

nd S

ize (m

illion

s US

D)

$10

$30

$50

$70

$90

$110

$130

$150

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

Cum

ulativ

e Ca

pita

l Dep

loye

d (b

illion

s US

D)

$0

$4

$8

$12

$16

$20

Jan Feb

Mar Apr May Jun Ju

lAug Sep Oct Nov Dec

2006200720082009201020112012201320142015

The 12 month running average for Late Stage deal sizes (Series E, F, G, and H) has increased 10.6x (+959%) from the end of 2006 to the end of 2015.

Mon

thly

Deal

Volum

e

0

5

10

15

1.200

61.2

007

1.200

81.2

009

1.201

01.2

011

1.201

21.2

013

1.201

41.2

015

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587

Late Stage* Deal Volume and Capital Deployment (2014 vs 2015)

36

Mon

thly

Capi

tal D

eploy

ed (b

illions

USD

)

$0

$1

$2

$3

$4

$5Ja

n

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

Cum

ulativ

e Ca

pita

l Dep

loyed

(billio

ns U

SD)

$0

$6

$12

$18

$24

$30

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

Mon

thly

Deal

Volum

e0

10

20

30

40

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

2014 2015

Cum

ulativ

e De

al Vo

lume

0

75

150

225

300

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

-0.4% Year-Over-YearDEAL VOLUME

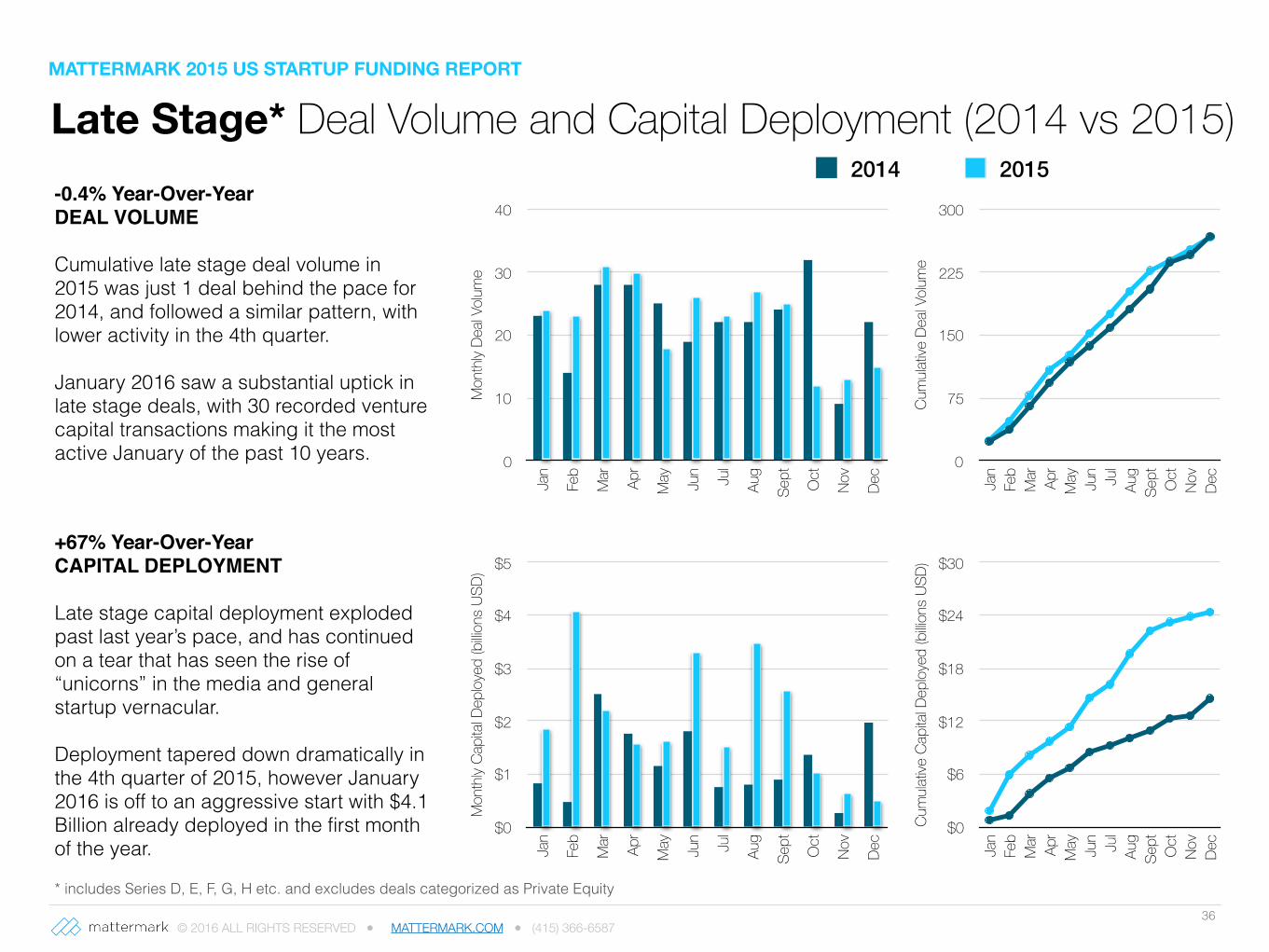

Cumulative late stage deal volume in 2015 was just 1 deal behind the pace for 2014, and followed a similar pattern, with lower activity in the 4th quarter.

January 2016 saw a substantial uptick in late stage deals, with 30 recorded venture capital transactions making it the most active January of the past 10 years.

+67% Year-Over-YearCAPITAL DEPLOYMENT

Late stage capital deployment exploded past last year’s pace, and has continued on a tear that has seen the rise of “unicorns” in the media and general startup vernacular.

Deployment tapered down dramatically in the 4th quarter of 2015, however January 2016 is off to an aggressive start with $4.1 Billion already deployed in the first month of the year.

* includes Series D, E, F, G, H etc. and excludes deals categorized as Private Equity

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658737

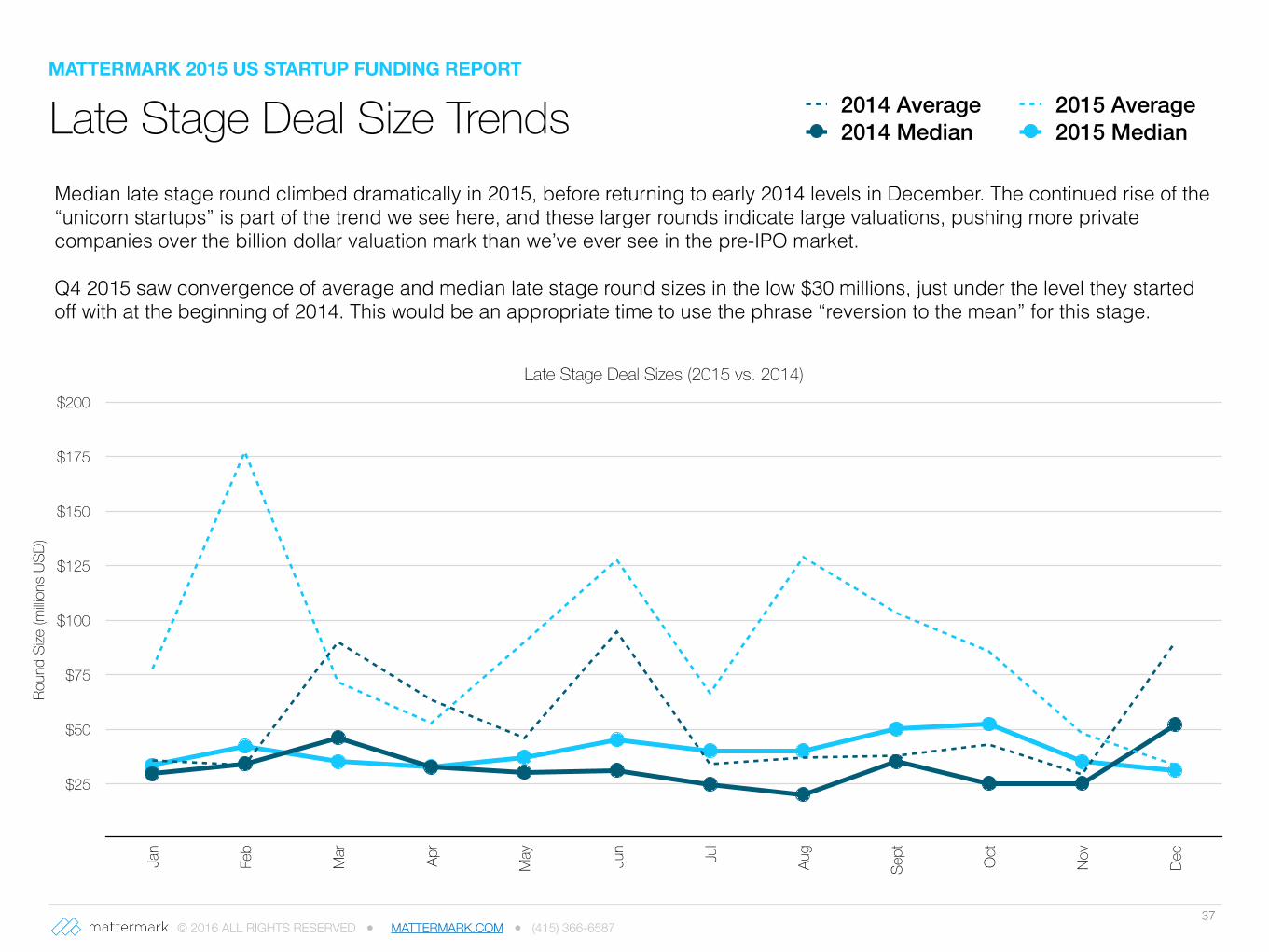

Median late stage round climbed dramatically in 2015, before returning to early 2014 levels in December. The continued rise of the “unicorn startups” is part of the trend we see here, and these larger rounds indicate large valuations, pushing more private companies over the billion dollar valuation mark than we’ve ever see in the pre-IPO market.

Q4 2015 saw convergence of average and median late stage round sizes in the low $30 millions, just under the level they started off with at the beginning of 2014. This would be an appropriate time to use the phrase “reversion to the mean” for this stage.

Late Stage Deal Sizes (2015 vs. 2014)

Roun

d Si

ze (m

illions

USD

)

$25

$50

$75

$100

$125

$150

$175

$200

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sept Oct

Nov

Dec

2014 Average 2015 Average2014 Median 2015 Median Late Stage Deal Size Trends

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658738

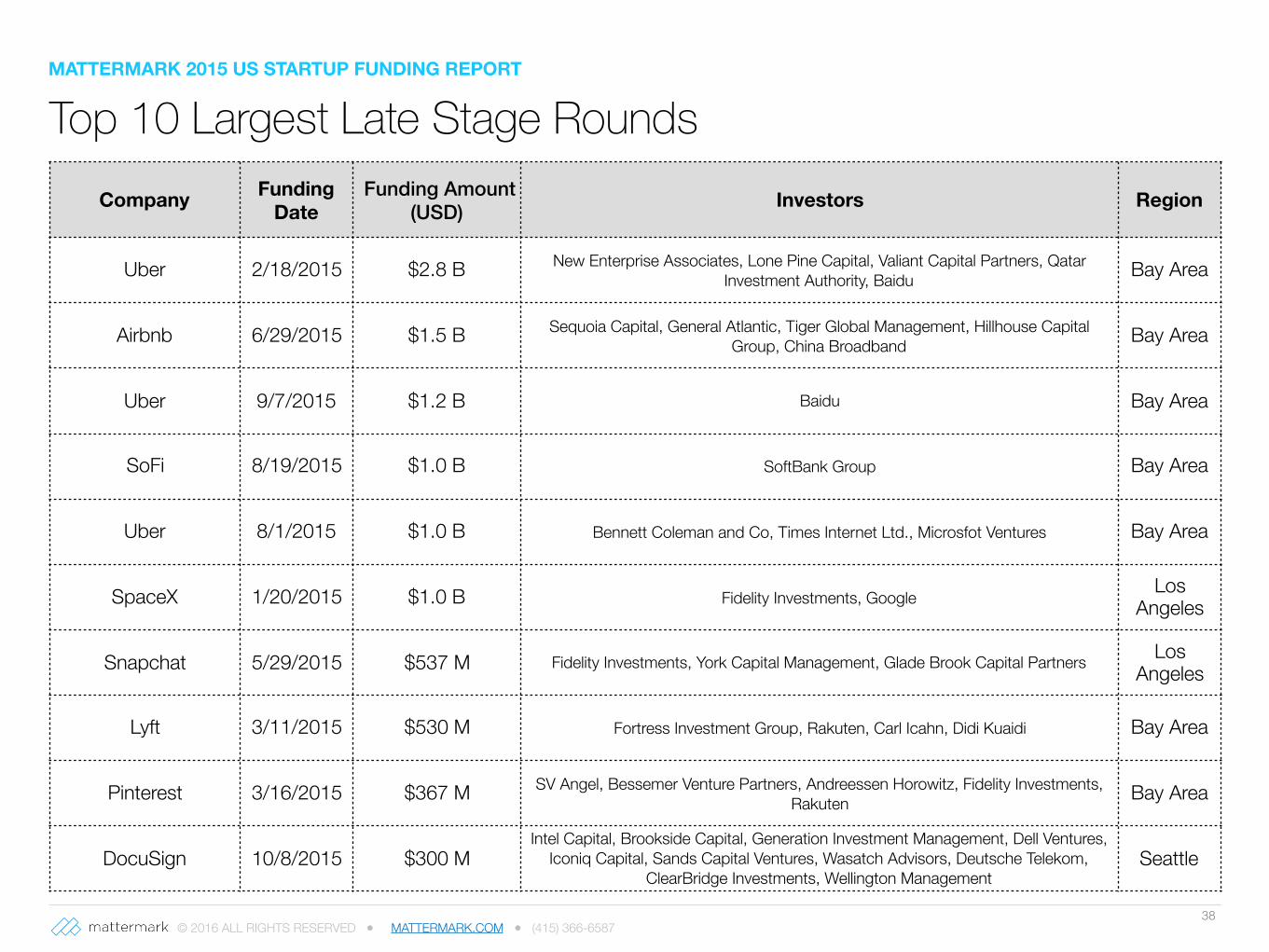

Top 10 Largest Late Stage RoundsCompany Funding

Date Funding Amount

(USD) Investors Region

Uber 2/18/2015 $2.8 B New Enterprise Associates, Lone Pine Capital, Valiant Capital Partners, Qatar Investment Authority, Baidu Bay Area

Airbnb 6/29/2015 $1.5 B Sequoia Capital, General Atlantic, Tiger Global Management, Hillhouse Capital Group, China Broadband Bay Area

Uber 9/7/2015 $1.2 B Baidu Bay Area

SoFi 8/19/2015 $1.0 B SoftBank Group Bay Area

Uber 8/1/2015 $1.0 B Bennett Coleman and Co, Times Internet Ltd., Microsfot Ventures Bay Area

SpaceX 1/20/2015 $1.0 B Fidelity Investments, Google Los Angeles

Snapchat 5/29/2015 $537 M Fidelity Investments, York Capital Management, Glade Brook Capital Partners Los Angeles

Lyft 3/11/2015 $530 M Fortress Investment Group, Rakuten, Carl Icahn, Didi Kuaidi Bay Area

Pinterest 3/16/2015 $367 M SV Angel, Bessemer Venture Partners, Andreessen Horowitz, Fidelity Investments, Rakuten Bay Area

DocuSign 10/8/2015 $300 MIntel Capital, Brookside Capital, Generation Investment Management, Dell Ventures,

Iconiq Capital, Sands Capital Ventures, Wasatch Advisors, Deutsche Telekom, ClearBridge Investments, Wellington Management

Seattle

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-658739

MethodologyTime Period

For this report we examined Q1-4 2015 Venture activity and funding trends in the year prior, as well at 5 and 10 year historical benchmarks.

Funding Rounds

For population statistics referencing “Venture-Backed” startups, inclusion for analysis was restricted to deals that disclosed the amount of funding raised.

Criteria

All analyses include USA companies. Metropolitan regions reflect Combined Statistical Areas as defined by the United States Office of Management and Budget.

Data Sources

Mattermark uses a broad range of sources to present the most complete picture possible of the startup ecosystem. In addition to extensive primary source research sourced specifically for this report, Mattermark uses publicly-available data from AngelList (www.angel.co), Crunchbase (www.crunchbase.com), NASDAQ, (www.nasdaq.com), the United States Securities and Exchange Commission (www.sec.gov), and source relationships with thousands of investors, community leaders, and startup founders.

Please send any questions, comments, or corrections for the editor to [email protected].

MATTERMARK 2015 US STARTUP FUNDING REPORT

© 2016 ALL RIGHTS RESERVED ● MATTERMARK.COM ● (415) 366-6587

Mattermark is where big data and machine learning bring science to the art of deal making. Our groundbreaking analytics are helping thousands of professionals research, prospect, track, qualify, and benchmark signals of growth and news coverage for 1M+

private and public technology companies from around the world.

Join the leading venture capital firms, angel investors, corporate and business development professionals, commercial real estate brokers, venture banks, private equity

firms, hedge funds, top tier consulting firms, and sales and marketing professionals.

Get Access to Mattermark Data