Embed Size (px)

Citation preview

Jérôme JACQUEMIN Country Manager, Advisory France

DNV GL

DNV GL © 2015 SAFER, SMARTER, GREENERDNV GL © 2015

Beyond Integration: three dynamics reshaping renewables and the grid

2

20 May 2015

DNV GL © 2015

These are interesting times…

3

“The days of ‘monopolized’ power are coming to an end...

get smarter or get out of the way”

Energy Management Supervisor, Government/related agency, North America

Thinking big picture…

DNV GL © 20154

Policy ProductionTransmission

& DistributionUse

DNV GL - Energy

Power testing, inspections and

certification

Renewables advisory services

Renewables certification

Electricity transmission and distribution

Smart grids and smart cities

Energy market and policy design

Energy management and operations

services

Energy efficiency services

Software

Policy Production Transmission & distribution Use

DNV GL © 2015

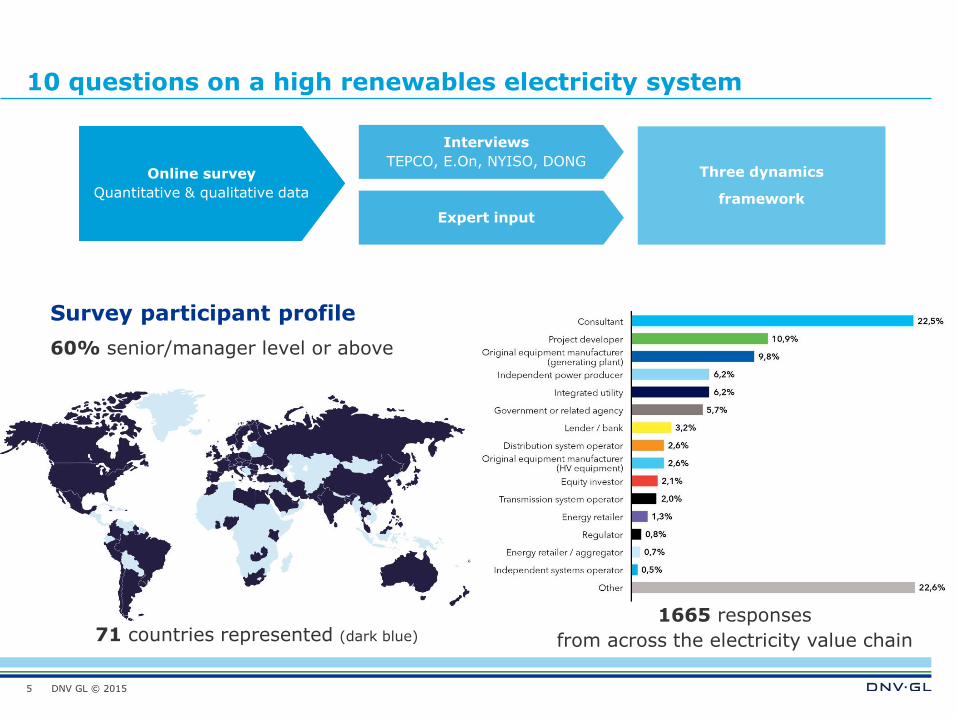

1665 responses

from across the electricity value chain

10 questions on a high renewables electricity system

5

Online survey

Quantitative & qualitative data

Interviews

TEPCO, E.On, NYISO, DONG

Survey participant profile

60% senior/manager level or above

Three dynamics

framework

71 countries represented (dark blue)

Expert input

DNV GL © 2015

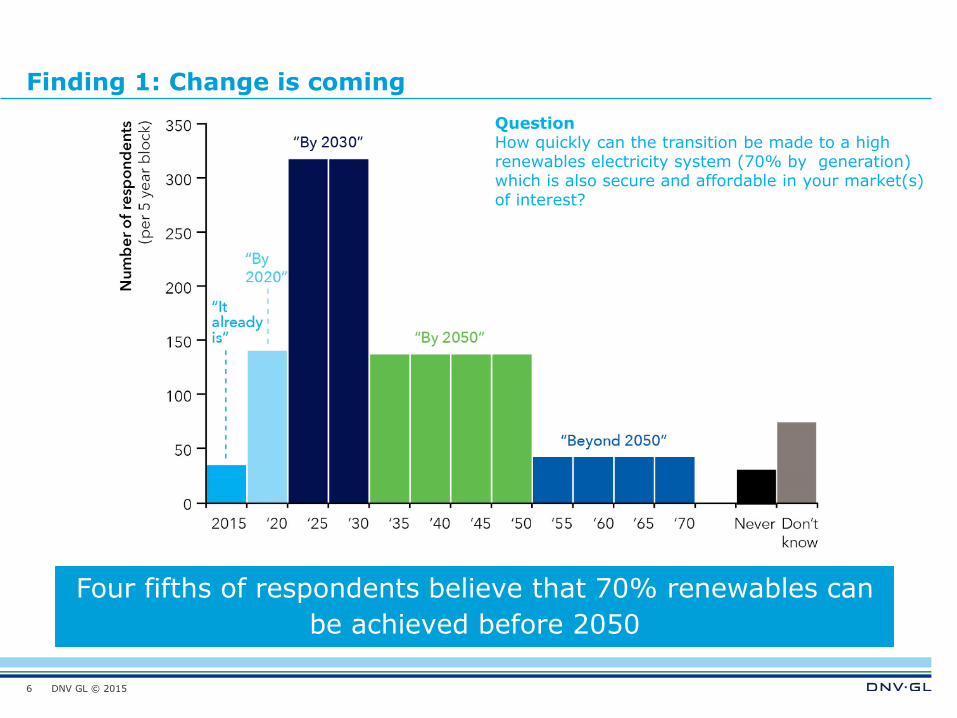

Finding 1: Change is coming

6

Four fifths of respondents believe that 70% renewables can

be achieved before 2050

QuestionHow quickly can the transition be made to a high renewables electricity system (70% by generation) which is also secure and affordable in your market(s) of interest?

DNV GL © 2015

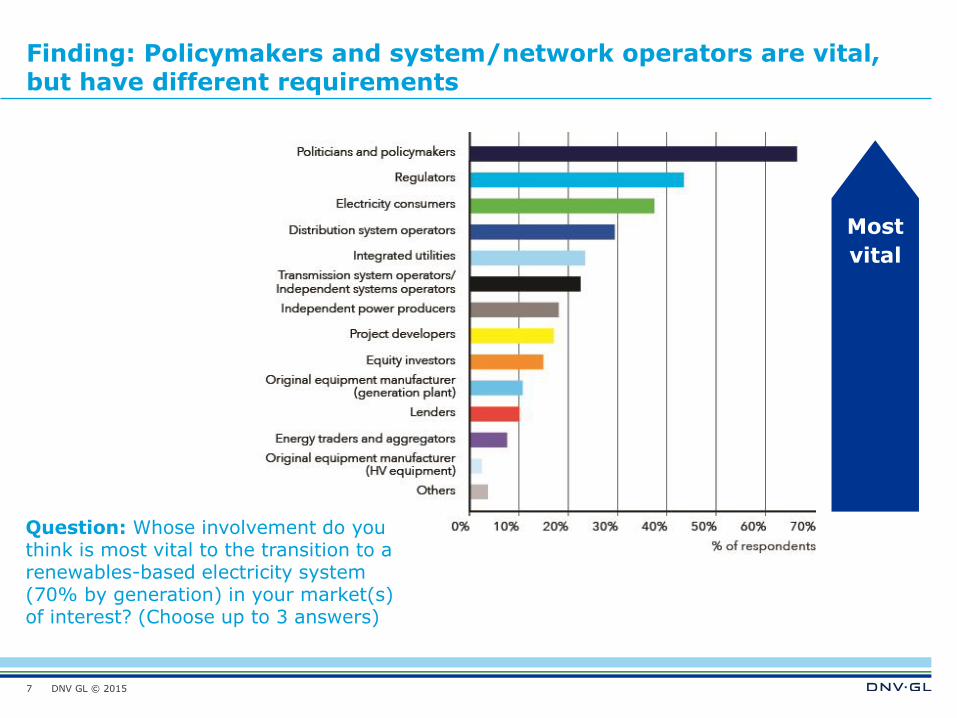

Finding: Policymakers and system/network operators are vital, but have different requirements

7

Question: Whose involvement do you think is most vital to the transition to a renewables-based electricity system (70% by generation) in your market(s) of interest? (Choose up to 3 answers)

Most

vital

DNV GL © 2015

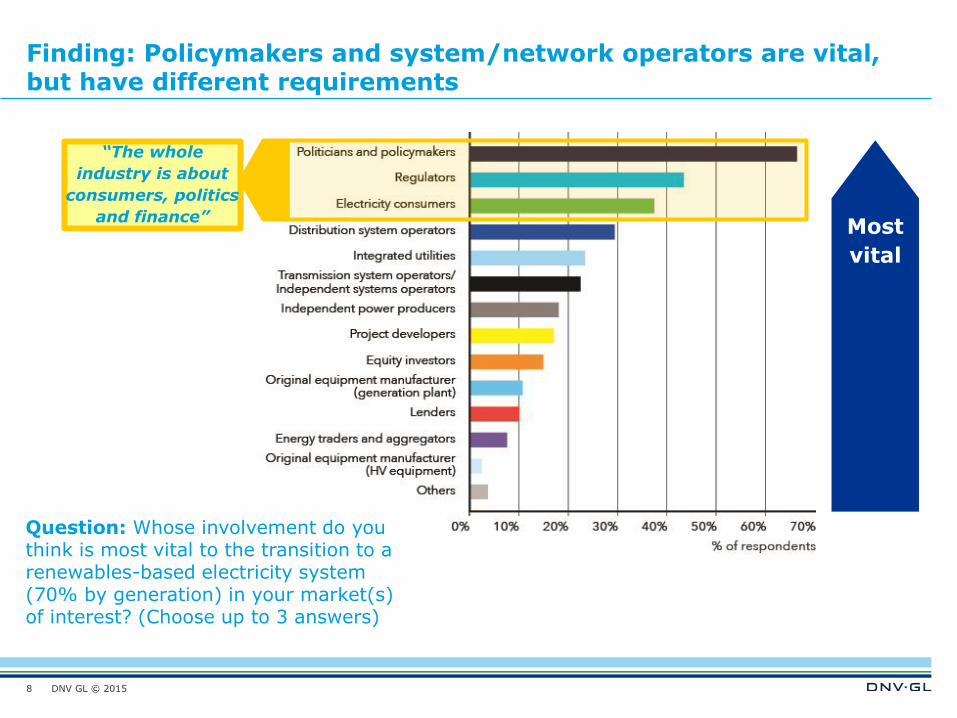

Finding: Policymakers and system/network operators are vital, but have different requirements

8

Question: Whose involvement do you think is most vital to the transition to a renewables-based electricity system (70% by generation) in your market(s) of interest? (Choose up to 3 answers)

Most

vital

“The whole

industry is about

consumers, politics

and finance”

DNV GL © 2015

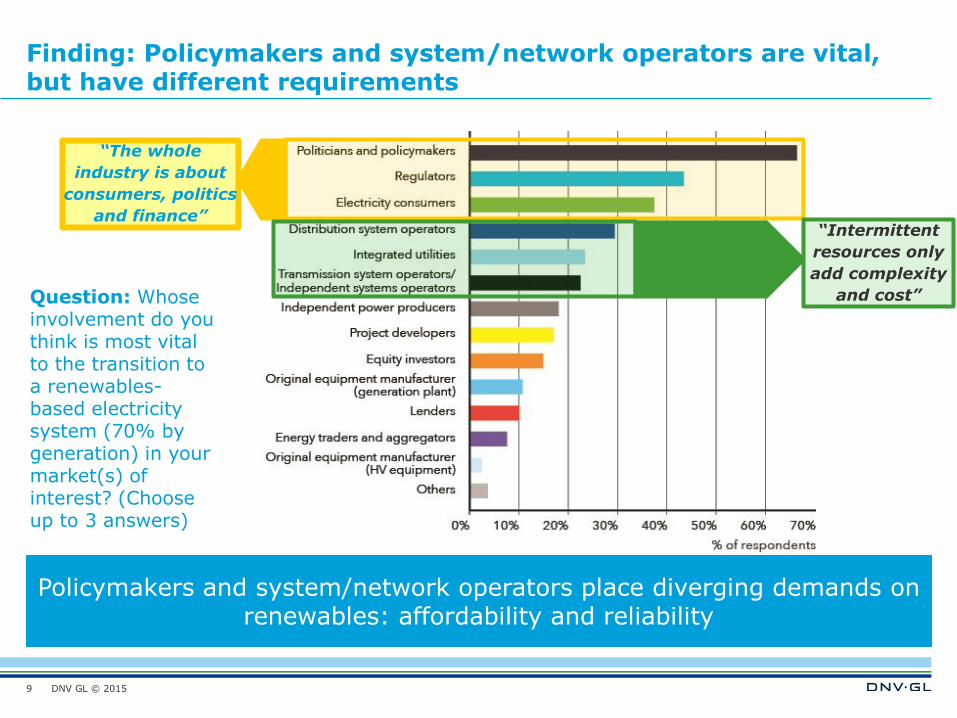

Finding: Policymakers and system/network operators are vital, but have different requirements

9

Question: Whose involvement do you think is most vital to the transition to a renewables-based electricity system (70% by generation) in your market(s) of interest? (Choose up to 3 answers)

“The whole

industry is about

consumers, politics

and finance”“Intermittent

resources only

add complexity

and cost”

Policymakers and system/network operators place diverging demands on renewables: affordability and reliability

DNV GL © 2015

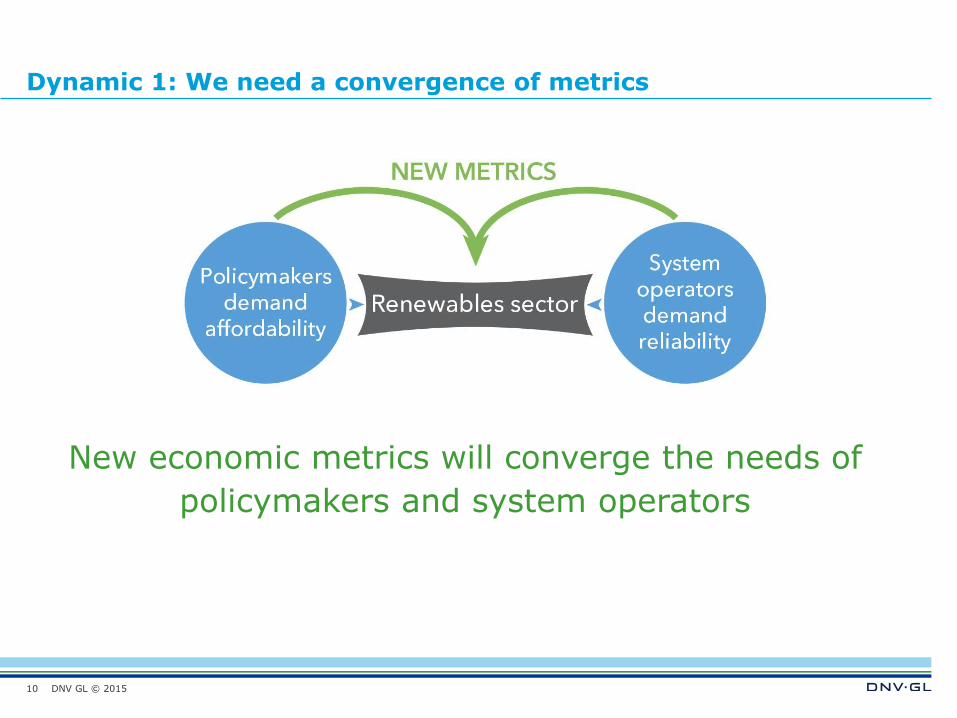

Dynamic 1: We need a convergence of metrics

10

New economic metrics will converge the needs of

policymakers and system operators

DNV GL © 2015

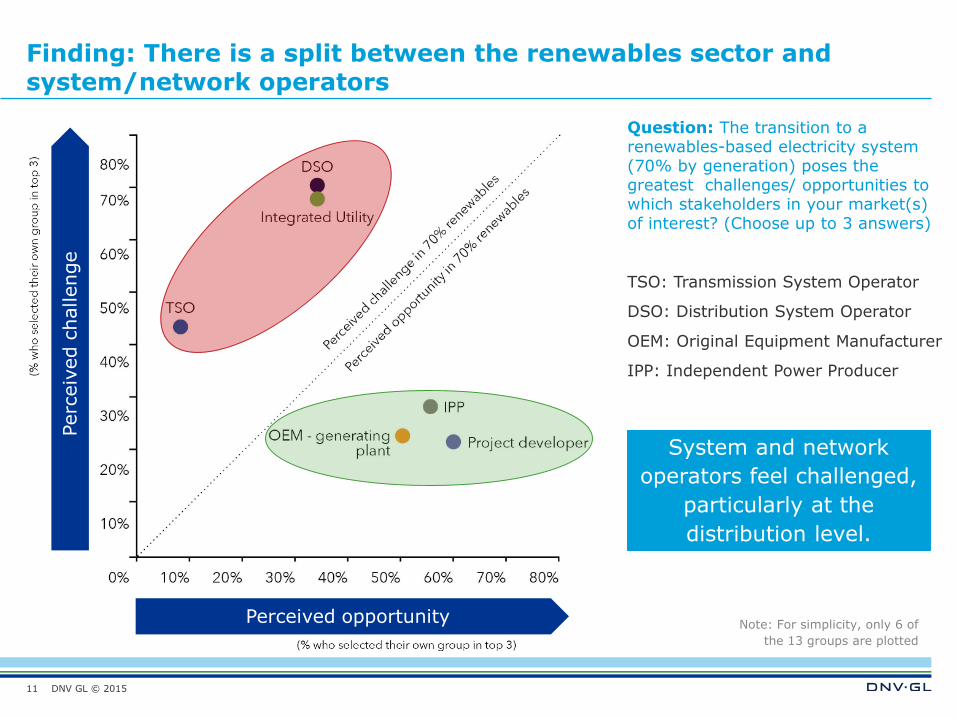

Finding: There is a split between the renewables sector and system/network operators

11

Question: The transition to a renewables-based electricity system (70% by generation) poses the greatest challenges/ opportunities to which stakeholders in your market(s) of interest? (Choose up to 3 answers)

Note: For simplicity, only 6 of

the 13 groups are plotted

System and network

operators feel challenged,

particularly at the

distribution level.

TSO: Transmission System Operator

DSO: Distribution System Operator

OEM: Original Equipment Manufacturer

IPP: Independent Power Producer

Perceived opportunity

Perc

eiv

ed c

hallenge

DNV GL © 2015

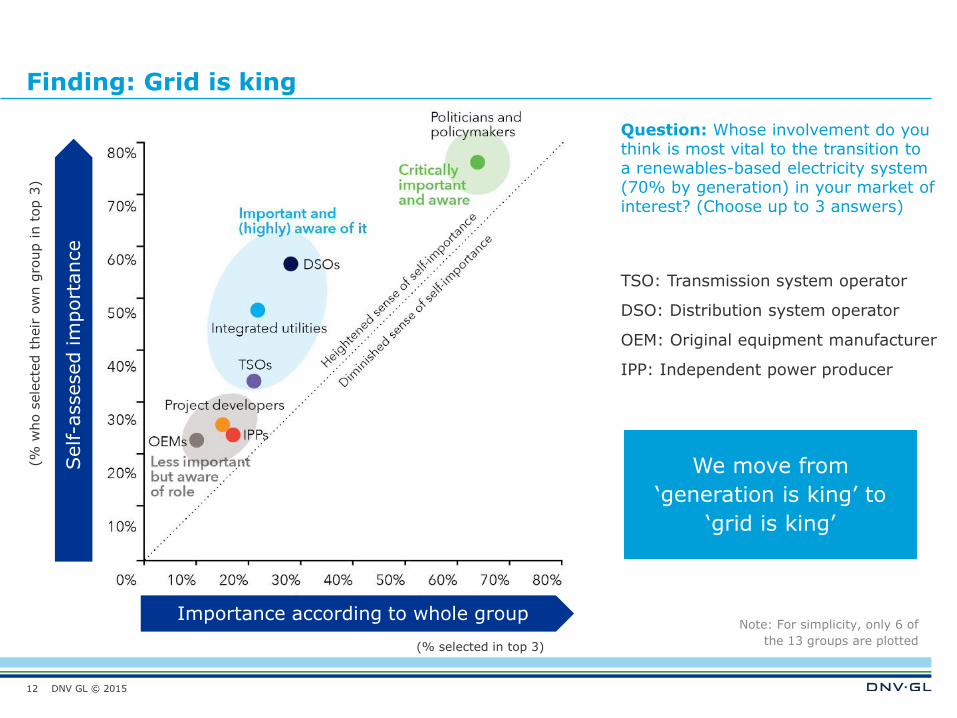

Finding: Grid is king

12

We move from

‘generation is king’ to

‘grid is king’

Question: Whose involvement do you think is most vital to the transition to a renewables-based electricity system (70% by generation) in your market of interest? (Choose up to 3 answers)

TSO: Transmission system operator

DSO: Distribution system operator

OEM: Original equipment manufacturer

IPP: Independent power producer

Importance according to whole group

Self-a

ssesed

import

ance

(% selected in top 3)

(% w

ho s

ele

cte

d t

heir

ow

n g

roup in t

op 3

)

Note: For simplicity, only 6 of

the 13 groups are plotted

DNV GL © 2015

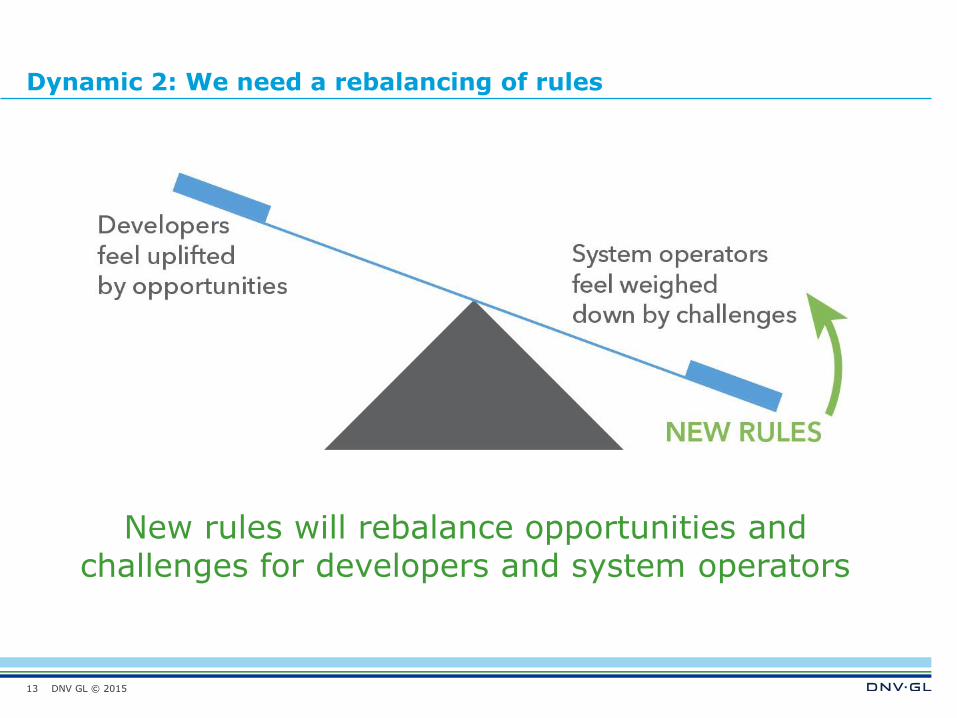

Dynamic 2: We need a rebalancing of rules

13

New rules will rebalance opportunities andchallenges for developers and system operators

DNV GL © 2015

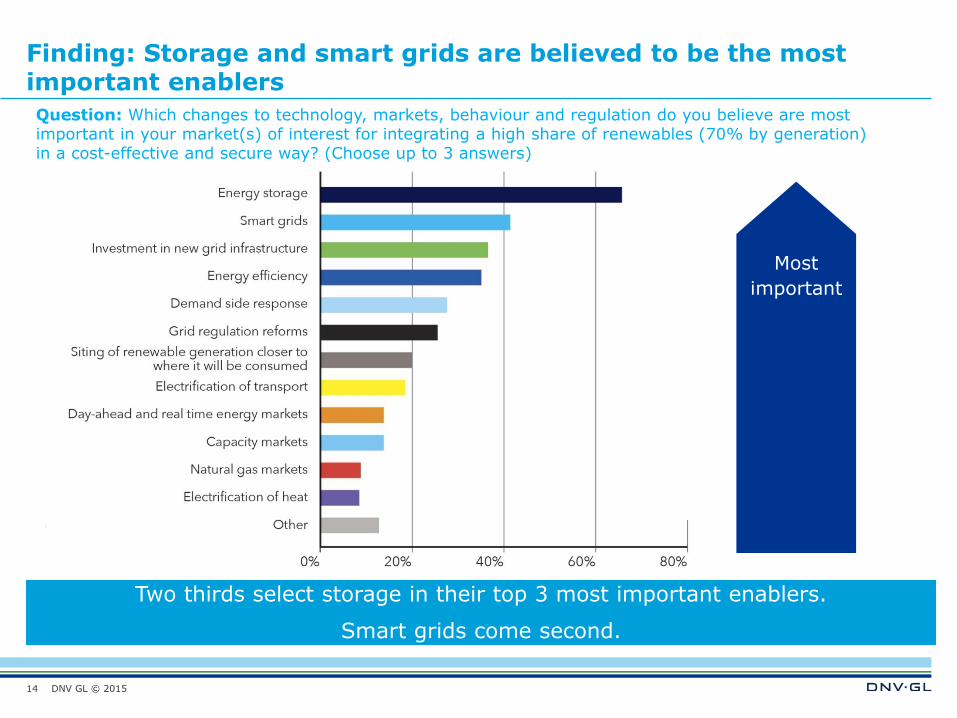

Finding: Storage and smart grids are believed to be the most important enablers

14

Question

Question: Which changes to technology, markets, behaviour and regulation do you believe are most important in your market(s) of interest for integrating a high share of renewables (70% by generation) in a cost-effective and secure way? (Choose up to 3 answers)

Two thirds select storage in their top 3 most important enablers.

Smart grids come second.

Most

important

DNV GL © 2015

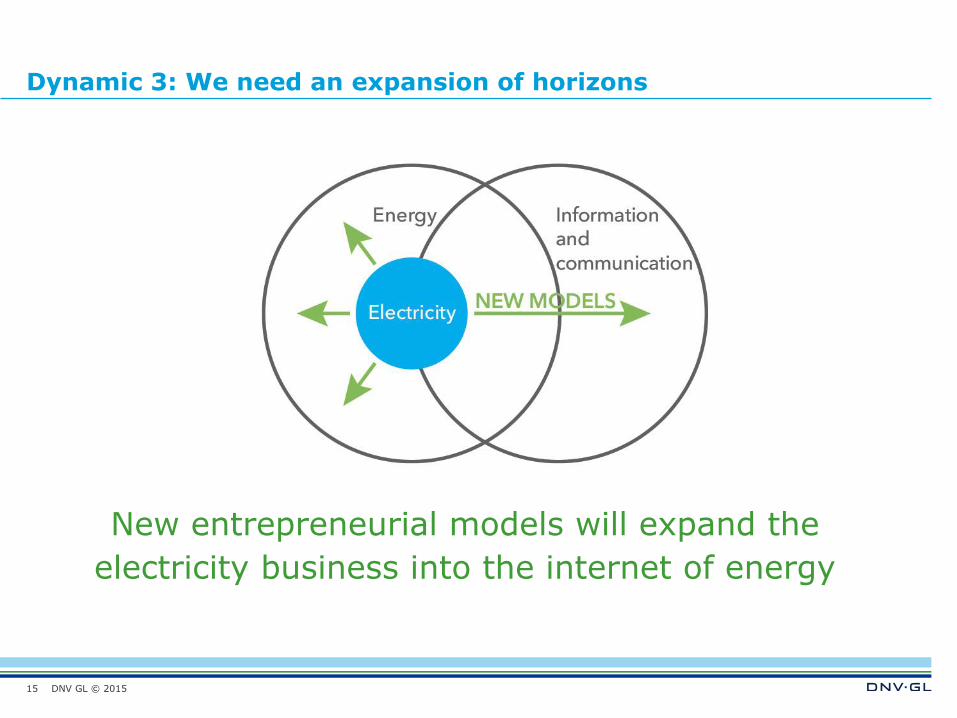

Dynamic 3: We need an expansion of horizons

15

New entrepreneurial models will expand the

electricity business into the internet of energy

DNV GL © 2015

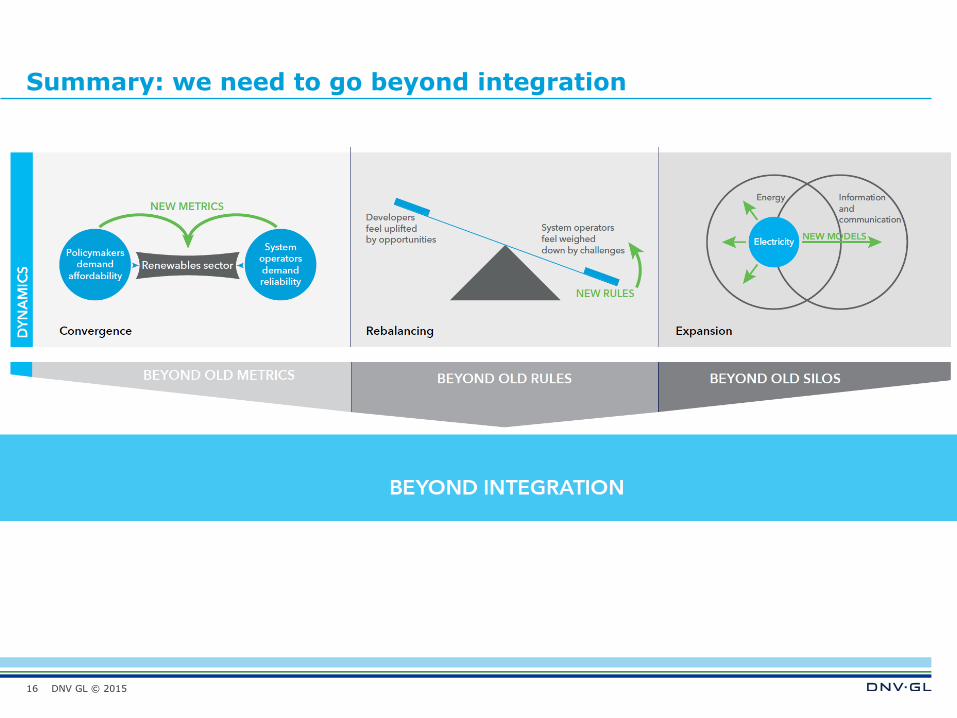

Summary: we need to go beyond integration

16

DNV GL © 2015

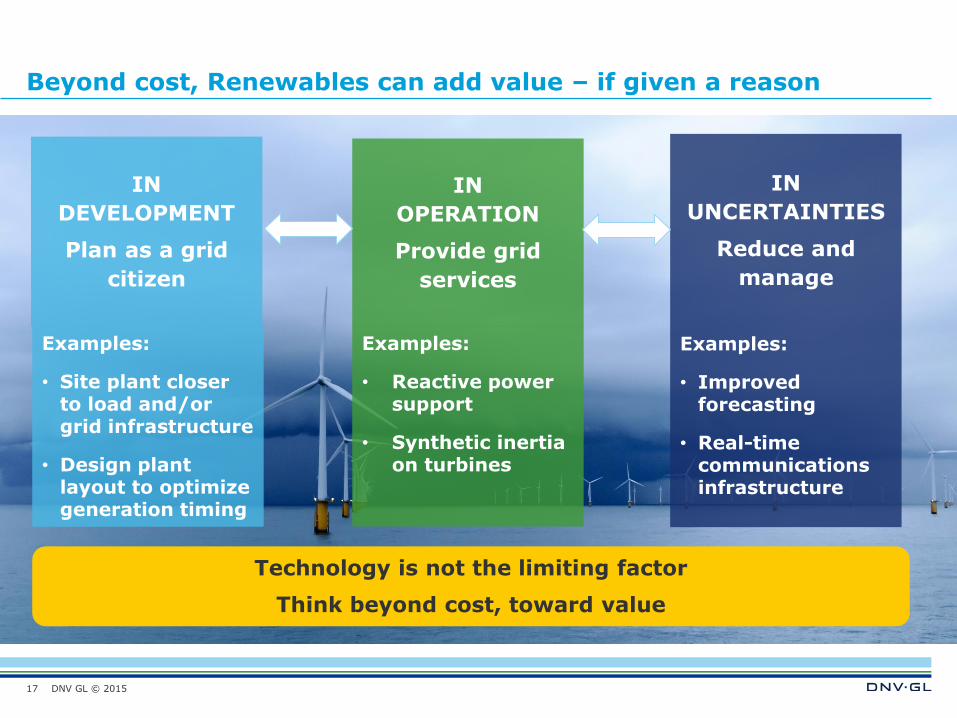

Beyond cost, Renewables can add value – if given a reason

17

IN

DEVELOPMENT

Plan as a grid

citizen

IN

UNCERTAINTIES

Reduce and

manage

Examples:

• Improved forecasting

• Real-time communications infrastructure

Examples:

• Site plant closer to load and/or grid infrastructure

• Design plant layout to optimize generation timing

IN

OPERATION

Provide grid

services

Examples:

• Reactive power support

• Synthetic inertia on turbines

Technology is not the limiting factor

Think beyond cost, toward value