Embed Size (px)

Citation preview

Business risks in mining & metals 2014-15

Business Council of MongoliaSeptember 2014

Page 2 Top ten business risks for mining and metals 2014/15

Business risks in mining and metals 2014-15

1Productivity improvement

2Capital dilemmas

3Social license to operate

4Resource nationalism

5Capital projects

6Price & currency volatility

7Infrastructure access

8Sharing the benefits

9Balancing talent needs

10Access to water and energy

Page 3 Top ten business risks for mining and metals 2014/15

Business risks in mining and metals 2014-15

Up from 2013 Same as 2013Down from 2013

Page 4 Top ten business risks for mining and metals 2014/15

Productivity improvement

And yet this has been in an environment of:• Ongoing improvements in equipment, efficiency and reliability• Significant investment in the sector by OEMs• Engineering and technological advancements

1

Focus on production growth at any cost meant diminished focus on productivity which has been on the decline since 2000

Underlying reasons• Significant gaps in skills• Labour costs exceed the rate of inflation• Insufficient knowledge of operating in a

cost-constrained environment• Ineffective portfolio management• Issues with capital allocation• Poor project execution• Slow pace of innovation in mining technology• Lack of substitution of capital for labour

Page 5 Top ten business risks for mining and metals 2014/15

Examples• Gradual reductions of manpower at operating mining companies, and many mining services companies• Many workers retaining employment have been placed on temporary “slowdown”• Moves to bring mineral processing in-country• Construction of better (non-dirt/desert) roads

The future• Miners have been dealing with the issue by implementing cost-cutting solutions. A narrow focus on point solutions or continuous improvement will not

close the gap and could even be counter-productive.• Real gains will only be achieved when a step change in infrastructure availability occurs (i.e. moving transport logistics from trucks to trains).

Mongolia – Examples of productivity improvement initiatives1

Page 6 Top ten business risks for mining and metals 2014/15

Capital management1 Capital optimization Capitalgrowth

Improving financial strength and flexibility Holistic, returns-focused approach to theportfolio

Disciplined,strategic growth

• Gearing levels reducing• High cost operations closed• Improved financing terms• Improved cash flow coverage

• Priorities and investment criteria communicated• Disposals underway/completed/

on hold

• Productivity gains• Tightening of investment appraisal• Innovation

Mid-tiers

What next?Majors

2a Capital allocation: progress made along a journey of capital transformation

2 3

Page 7 Top ten business risks for mining and metals 2014/15

Explorers:capital crisis

14%Decline in q-o-q junior equity

proceeds in 1Q14

$0.5mAmount raised by nearly half

of 1Q14 junior issues

38%Fall in iron ore price from

12m high

31:9Ratio of negative to

positive/neutral ratings actionsover 1H 2014*

Mid-tiers: persistentcredit risk for some

14%Increase in y-o-y EBITDA

$6bApprox. value

of completed divestmentsin 2013

Majors:internal capital

Capital access: fortunes are diverging as the “wealth gap” widens2b

Page 8 Top ten business risks for mining and metals 2014/15

With little prospect in sight of a broad-based recovery in the availability of risk capital to the juniorsector, and with commodity price volatility remaining a persistent credit risk, small and mid-tier companies must:• Remain focused on cost and capital management• Be knowledgeable about the full range of financing options and providers, along with the short-term and long-term risks and costs attached to each• Ensure awareness of capital market conditions in order to capture transient windows of opportunity• Explore prospects for joint ventures and strategic partnerships – with suppliers, investors, offtakers and other mining companies• Demonstrate a unique investment proposition – management expertise, project quality, optionality• Be realistic about funding costs

Mongolia – Capital allocation and access –Mitigation, knowledge and preparedness is key

2

Page 9 Top ten business risks for mining and metals 2014/15

Social license to operate

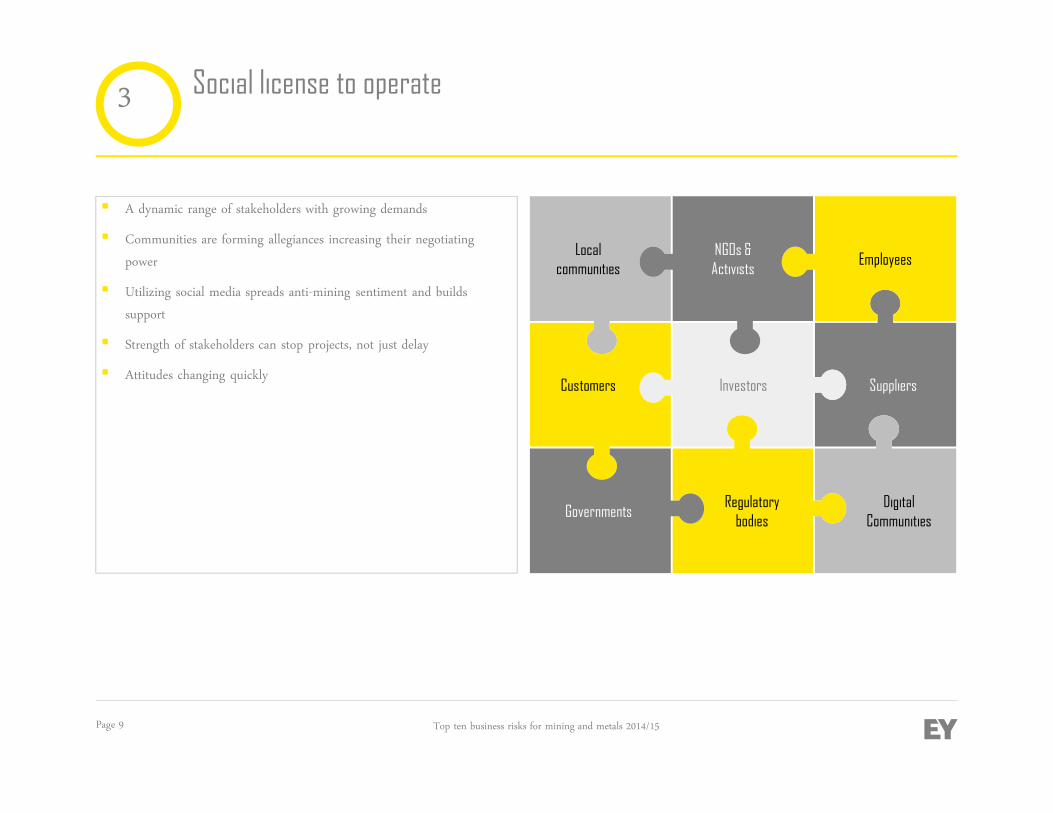

• A dynamic range of stakeholders with growing demands• Communities are forming allegiances increasing their negotiating

power• Utilizing social media spreads anti-mining sentiment and builds

support• Strength of stakeholders can stop projects, not just delay• Attitudes changing quickly

3

Localcommunities

NGOs &Activists

Employees

SuppliersInvestorsCustomers

DigitalCommunities

Regulatorybodies

Governments

Page 10 Top ten business risks for mining and metals 2014/15

Resource nationalism trends4

Mandated beneficiationIndonesia, South Africa and Zimbabwe

Use it or lose itJamaica, Indonesia, Bolivia

State ownershipSouth Africa

SeekingTrends

Higher value addHigher employment

Earlier oruninterrupted cashflow

More participation in upside

Page 11 Top ten business risks for mining and metals 2014/15

Mongolia - Social license to operate and resource nationalism

Examples – Social licence to operate• Denial of access by local groups to exploration sites• Claims of uranium contamination• Claims of dust pollution impacting livestock• Significant environmental protests in Ulaanbaatar• Public perception of the impacts of ninja mining on the legitimate mining community

Examples – Resource nationalism• The Mongolian Government has moved to reduce the perception of this as a major country risk through the following:

• Amendments to the legal and regulatory environment• Effective reductions to gold and coal royalty tax regimes• Changes to the exploration licencing framework and correcting previous issues

• This risk will remain to be considered significant until changes can be demonstrated to have been implemented, and have opera ted in a stable mannerfor a period of time

3/4

Page 12 Top ten business risks for mining and metals 2014/15

Why efficient capital project execution is more crucial than ever

Global mining investment pipeline (US$b)

465

562

676735

791

2009 2010 2011 2012 2013

A record US$791b of investment is in the pipeline for delivery – highestever

69% are facing cost overruns 50% are reporting schedule delays

EY’s research shows that the majority of these projects are facing delaysand/or cost escalations…

5

• Market pressure to better deliver on existing projects• Need to better plan next wave of projects to avoid failure

Page 13 Top ten business risks for mining and metals 2014/15

Mongolia – Capital project execution

Our research has shown the following key factors causing project delays and overruns:• Project management issues• Stakeholders’ conflicts• Resource constraints• Lack of supporting infrastructure• Regulatory policy-related challenges• Unfavourable external environment

All of these factors have been experienced in Mongolia.

5

Page 14 Top ten business risks for mining and metals 2014/15

Imbalance in the demand/supply equilibrium has led to higher volatility in commodity prices

Source: EY Analysis; Thomson Datastream

Differential impact of price volatility on commodities

0%

5%

10%

15%

20%

25%

30%

Gold Oil Copper Platinum Aluminium Iron ore Nickel

Annualized volatility in commodity prices (1H 2014) Driving volatility in the market• Exiting the supercycle• Increased regulation• Divergent central bank policies• Geopolitical risk• Provision of credit to traders• Withdrawal of banks from commodity markets

6

Volatility will continue for years to come and mining and metals companies must learn how to transact and invest in volatility

Page 15 Top ten business risks for mining and metals 2014/15

Infrastructure access

• New projects are in areas with low to medium logistics ratings• Three stakeholder groups – Government, capital providers and mining and metal companies need to work out new infrastructure solutions now

7

Logistics rating

Low

High

Page 16 Top ten business risks for mining and metals 2014/15

Declining economic value retained vs rising costs (2011 vs 2013)

Source: EY consolidation of company sustainability reports

0

50,000

100,000

150,000

200,000

Operating costs - suppliers, etc Economic value retained Employees Payment to capital providers(shareholders & interest)

Government Communities

US$m

2011 2013

ExamplesPeru – 225 social conflicts in May 2014 – 66.2% of those related to mining and hydrocarbon projects

Three largest platinum miners have lost more than US$2b in combined revenue as result of strikes in South Africa

Sharing the benefits – managing divergent stakeholders8

Page 17 Top ten business risks for mining and metals 2014/15

Balancing talent needs9

Short-term relief from skills shortage due to cyclical reduction in workforce in 2013/14

• May be difficult to rehire skilled workers in the future• Sector is unattractive to new graduates and over 50% leave in the first five years of employment• Attrition increases to above 70% in 10 years of employment

Structural skills shortage increasing

• Wages increasing over inflation in emerging markets are driving increased substitution of capital for labour. This is creating demand for more skilledlabour.

Real labour cost

• Underlying issues of skills shortages remain

Page 18 Top ten business risks for mining and metals 2014/15

Water and energy risk to increase

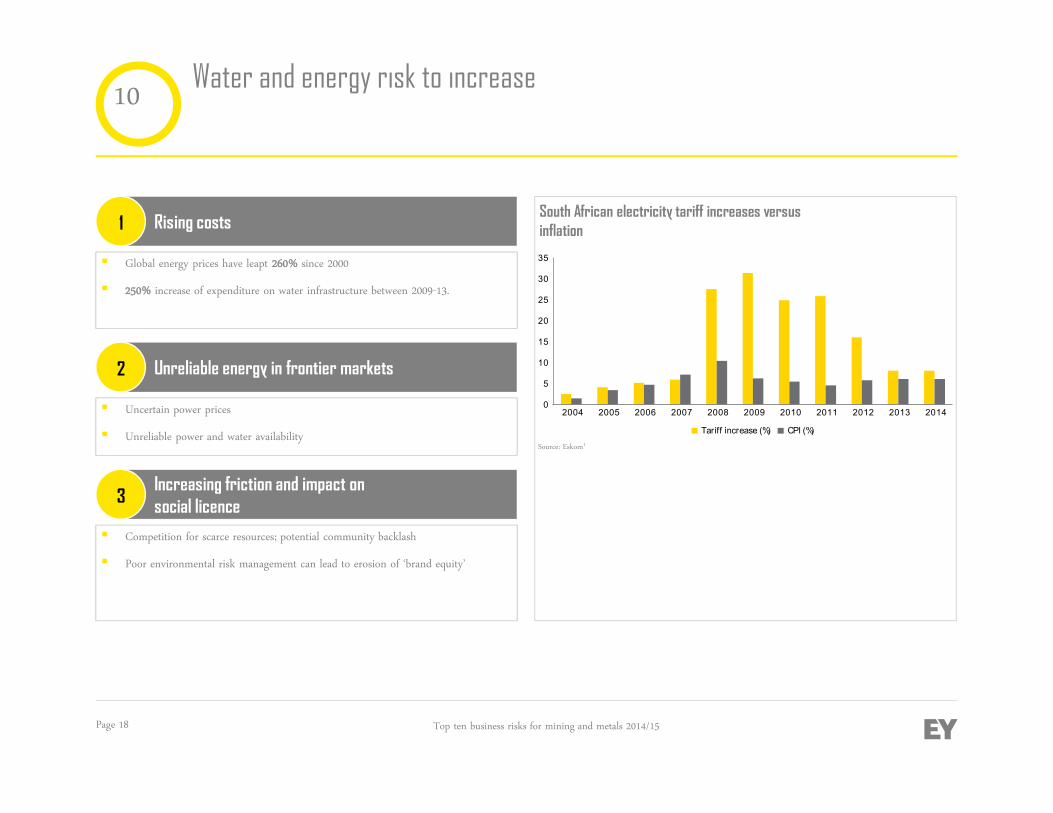

1 Rising costs

• Global energy prices have leapt 260% since 2000• 250% increase of expenditure on water infrastructure between 2009-13.

2 Unreliable energy in frontier markets

• Uncertain power prices• Unreliable power and water availability

3Increasing friction and impact onsocial licence

• Competition for scarce resources; potential community backlash• Poor environmental risk management can lead to erosion of ‘brand equity’

0

5

10

15

20

25

30

35

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Tariff increase (%) CPI (%)

South African electricity tariff increases versusinflation

Source: Eskom1

10

Page 19 Top ten business risks for mining and metals 2014/15

Under the radar risks – 11 to 20