Embed Size (px)

Citation preview

A SWIFT perspective on the evolution of the payments businessMatthieu de HeeringHead of Russia, CIS and Mongolia - SWIFT

National Payments Forum – Moscow – 09-Nov-2016

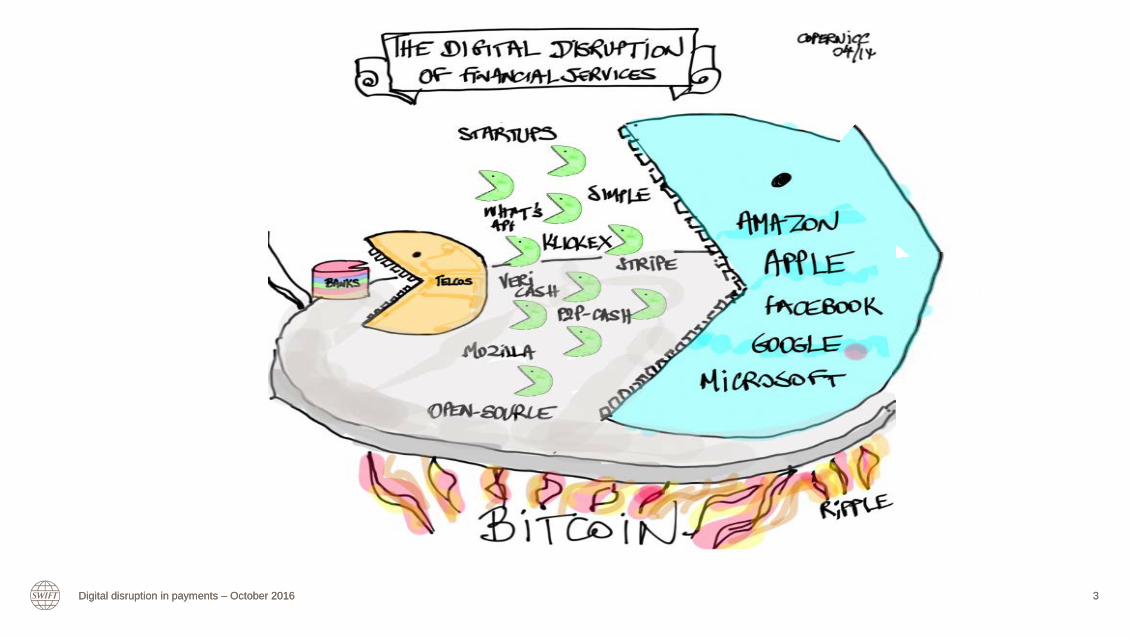

Digital disruption in payments

33Digital disruption in payments – October 2016Digital disruption in payments – October 2016

4

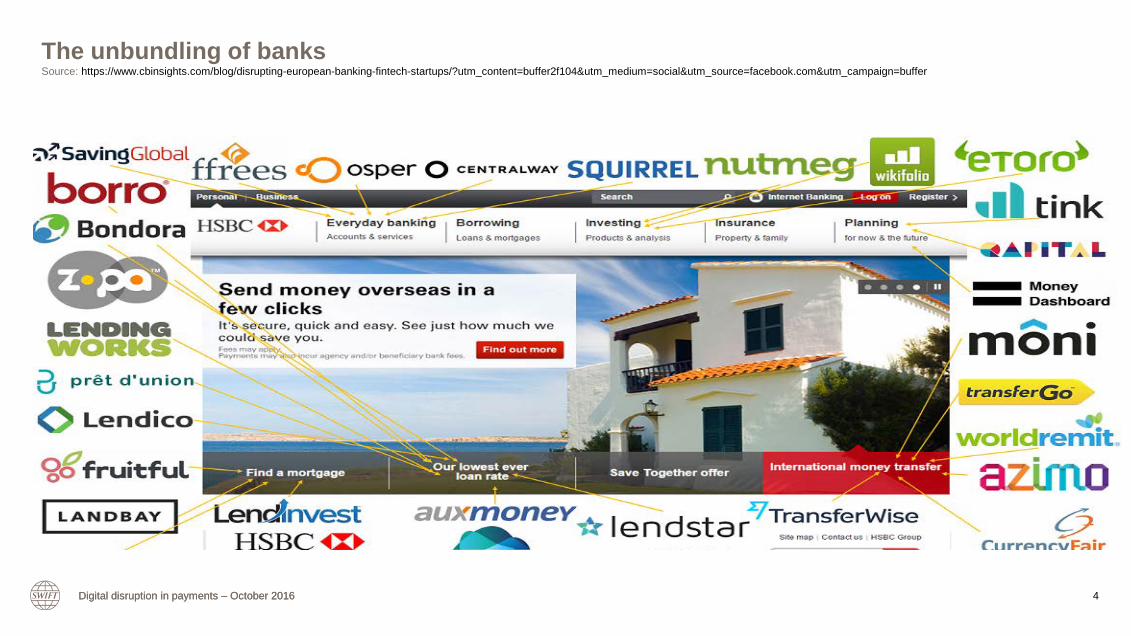

The unbundling of banksSource: https://www.cbinsights.com/blog/disrupting-european-banking-fintech-startups/?utm_content=buffer2f104&utm_medium=social&utm_source=facebook.com&utm_campaign=buffer

Digital disruption in payments – October 2016Digital disruption in payments – October 2016

5

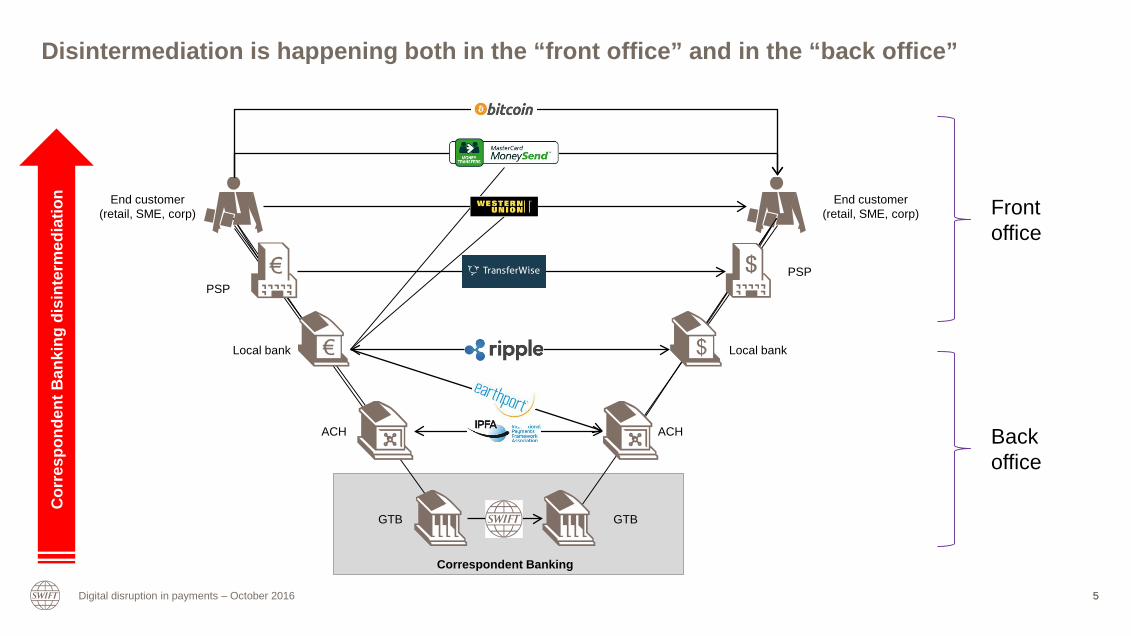

Disintermediation is happening both in the “front office” and in the “back office”

5

Front office

Backoffice

Local bank Local bank

PSPPSP

ACH ACH

GTB GTB

End customer (retail, SME, corp)

End customer (retail, SME, corp)

Correspondent Banking

Cor

resp

onde

nt B

anki

ng d

isin

term

edia

tion

Digital disruption in payments – October 2016

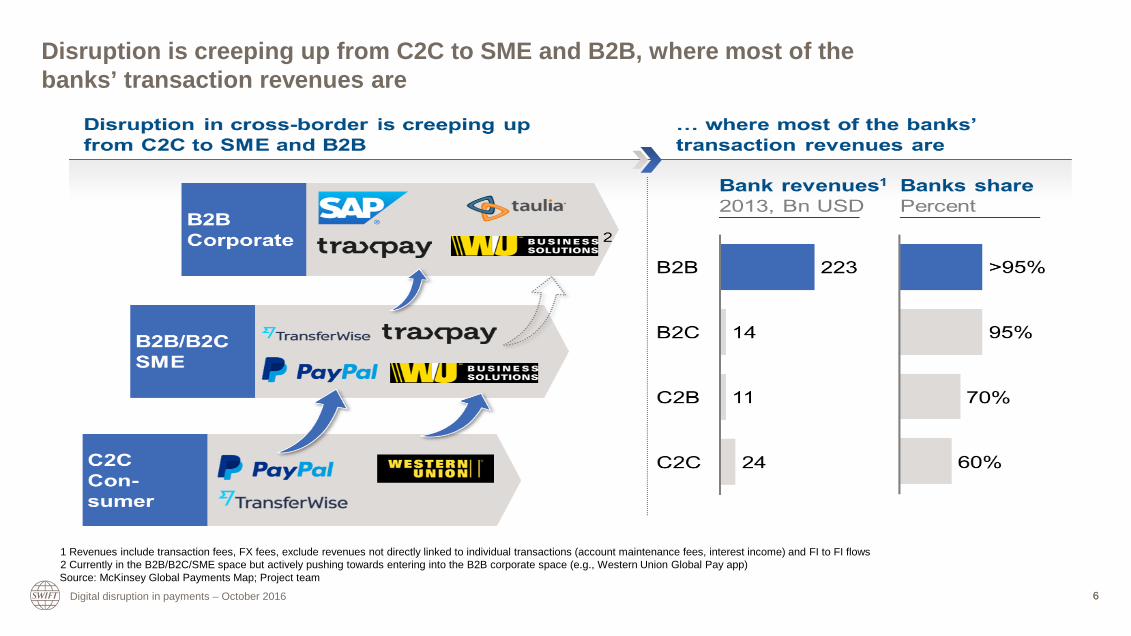

Disruption is creeping up from C2C to SME and B2B, where most of the banks’ transaction revenues are

Source: McKinsey Global Payments Map; Project team

1 Revenues include transaction fees, FX fees, exclude revenues not directly linked to individual transactions (account maintenance fees, interest income) and FI to FI flows2 Currently in the B2B/B2C/SME space but actively pushing towards entering into the B2B corporate space (e.g., Western Union Global Pay app)

66Digital disruption in payments – October 2016

Distributed ledger technologies (DLT) can present some opportunities

Distributed database

Information propagation

Beyond payments, e.g. trade

financeTraceability

77Digital disruption in payments – October 2016

Digital disruption in payments – October 2016 8

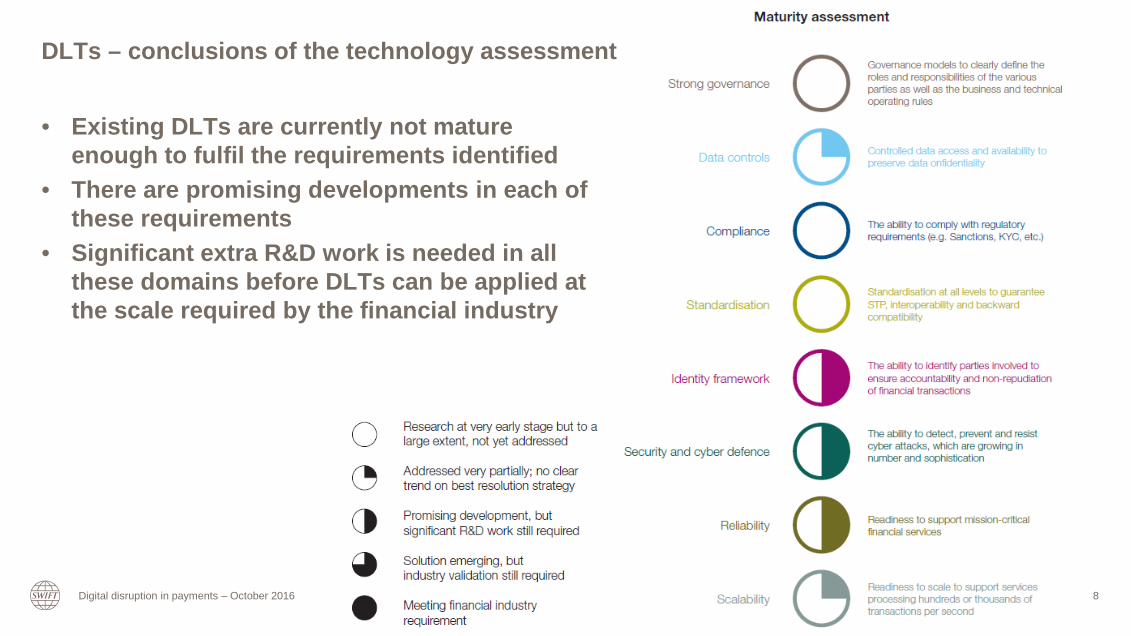

DLTs – conclusions of the technology assessment

• Existing DLTs are currently not mature enough to fulfil the requirements identified

• There are promising developments in each of these requirements

• Significant extra R&D work is needed in all these domains before DLTs can be applied at the scale required by the financial industry

9

Need for change, also rejuvenate business model

Technology Business

Digital disruption in payments – October 2016

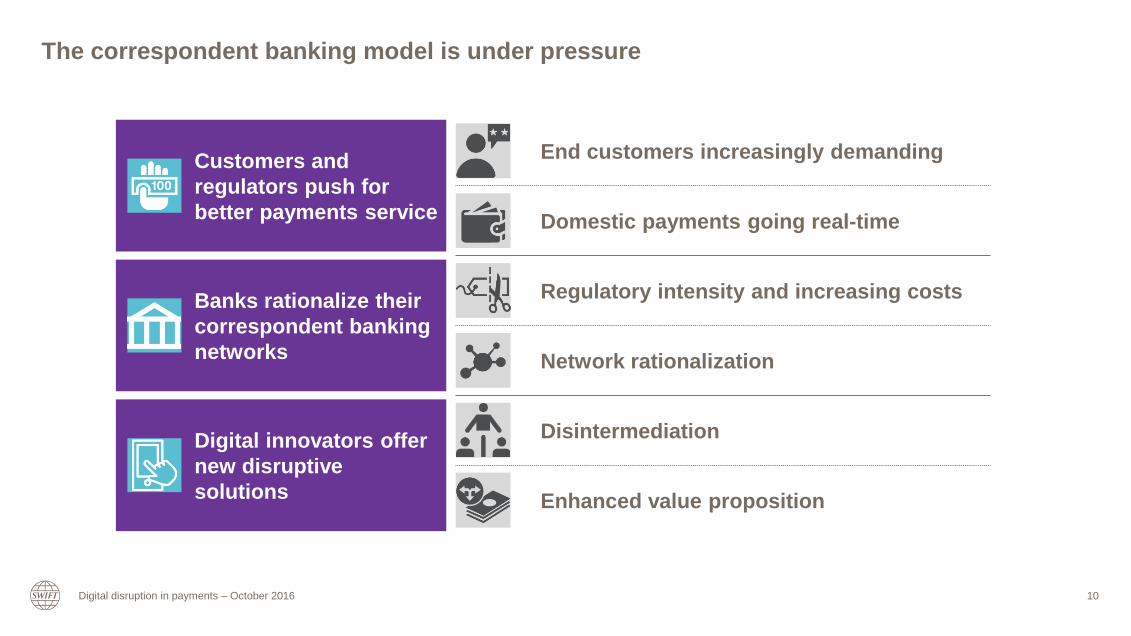

The correspondent banking model is under pressure

Customers and regulators push for better payments service

Banks rationalize their correspondent banking networks

Digital innovators offer new disruptive solutions

End customers increasingly demanding

Domestic payments going real-time

Regulatory intensity and increasing costs

Network rationalization

Enhanced value proposition

Disintermediation

Digital disruption in payments – October 2016 10

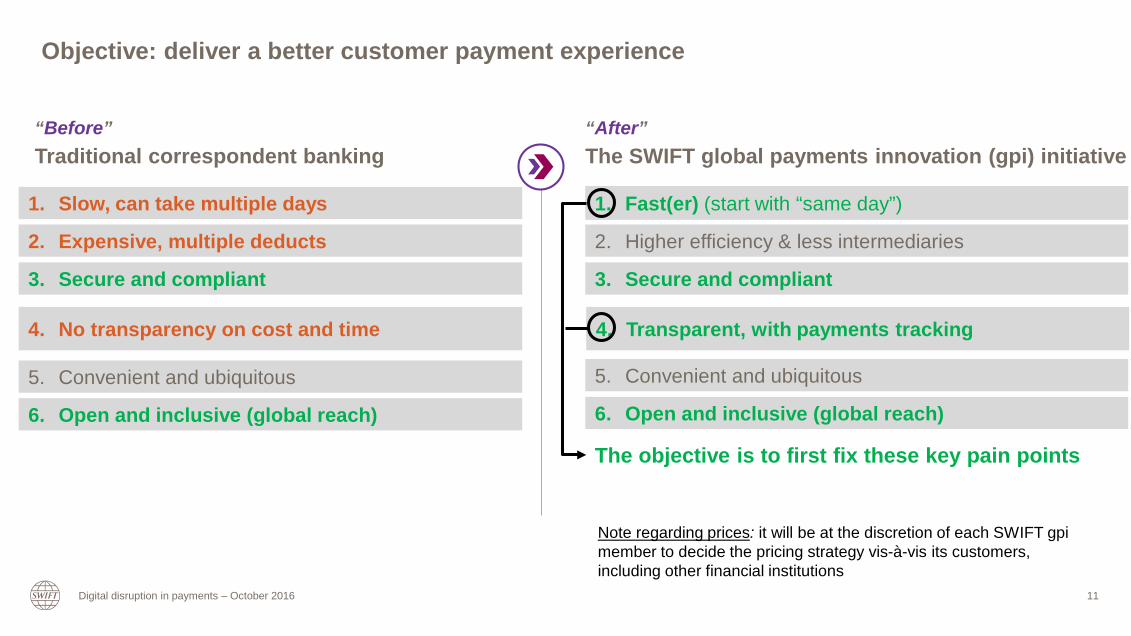

Objective: deliver a better customer payment experience

“Before”Traditional correspondent banking

“After”The SWIFT global payments innovation (gpi) initiative

1. Slow, can take multiple days

2. Expensive, multiple deducts

3. Secure and compliant

4. No transparency on cost and time

5. Convenient and ubiquitous

6. Open and inclusive (global reach)

1. Fast(er) (start with “same day”)

2. Higher efficiency & less intermediaries

3. Secure and compliant

4. Transparent, with payments tracking

5. Convenient and ubiquitous

6. Open and inclusive (global reach)

The objective is to first fix these key pain points

Note regarding prices: it will be at the discretion of each SWIFT gpimember to decide the pricing strategy vis-à-vis its customers, including other financial institutions

Digital disruption in payments – October 2016 11

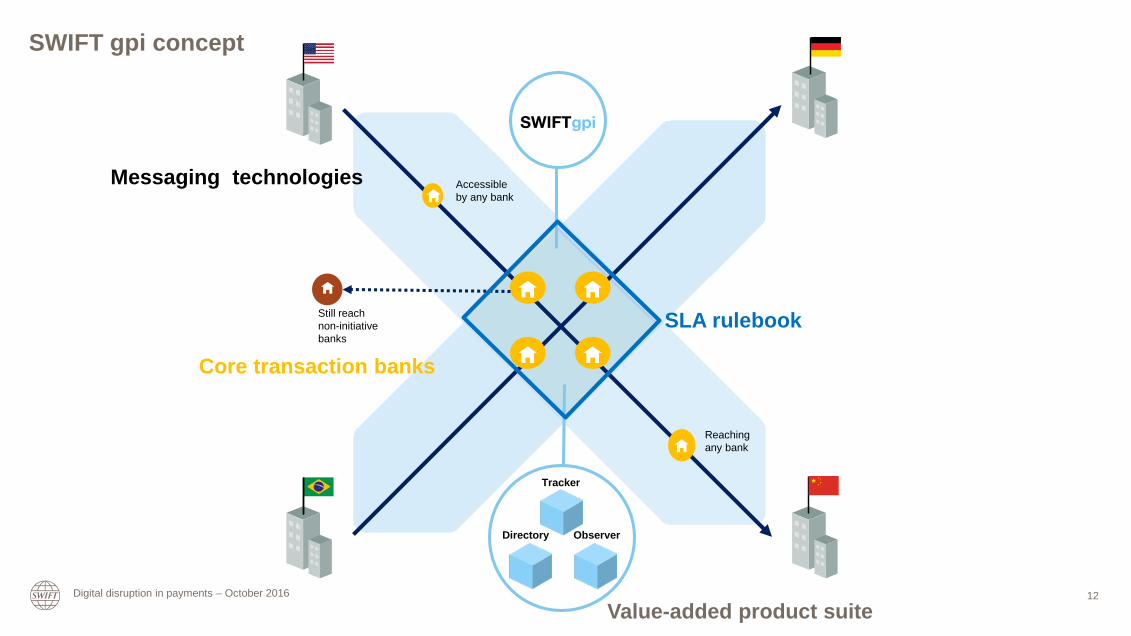

Still reachnon-initiativebanks

Accessibleby any bank

Reachingany bank

Tracker

Directory Observer

SWIFT gpi concept

SLA rulebook

Core transaction banks

Value-added product suite

Messaging technologies

Digital disruption in payments – October 2016 12

Digital disruption in payments – October 2016

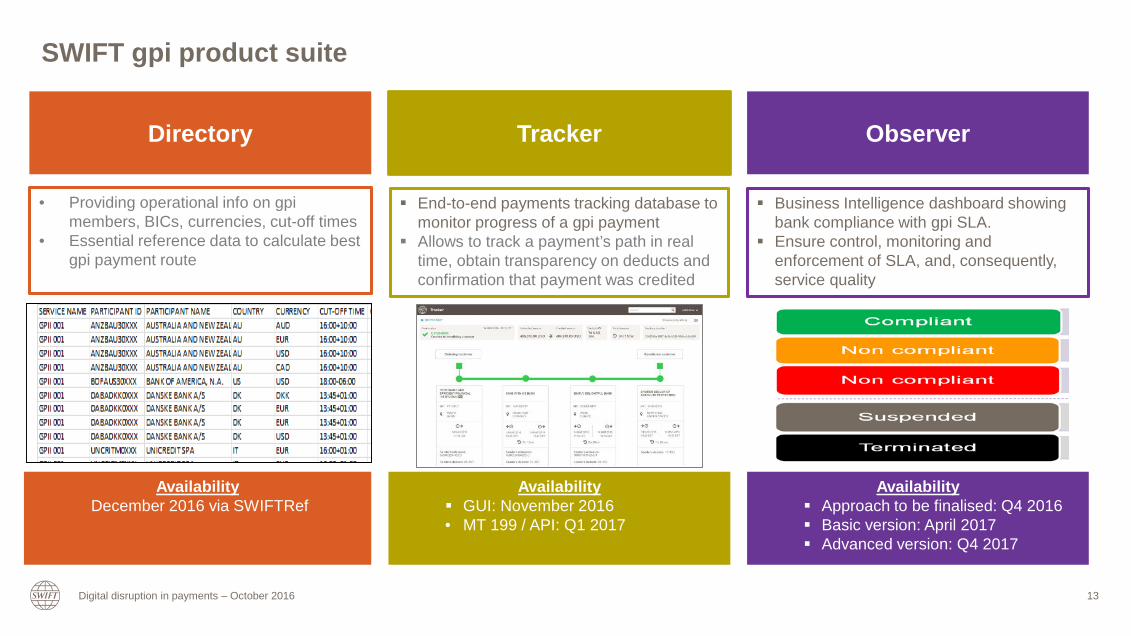

SWIFT gpi product suite

Directory Tracker Observer

End-to-end payments tracking database to monitor progress of a gpi payment

Allows to track a payment’s path in real time, obtain transparency on deducts and confirmation that payment was credited

Business Intelligence dashboard showing bank compliance with gpi SLA.

Ensure control, monitoring and enforcement of SLA, and, consequently, service quality

AvailabilityDecember 2016 via SWIFTRef

Availability GUI: November 2016• MT 199 / API: Q1 2017

Availability Approach to be finalised: Q4 2016 Basic version: April 2017 Advanced version: Q4 2017

• Providing operational info on gpimembers, BICs, currencies, cut-off times

• Essential reference data to calculate best gpi payment route

13

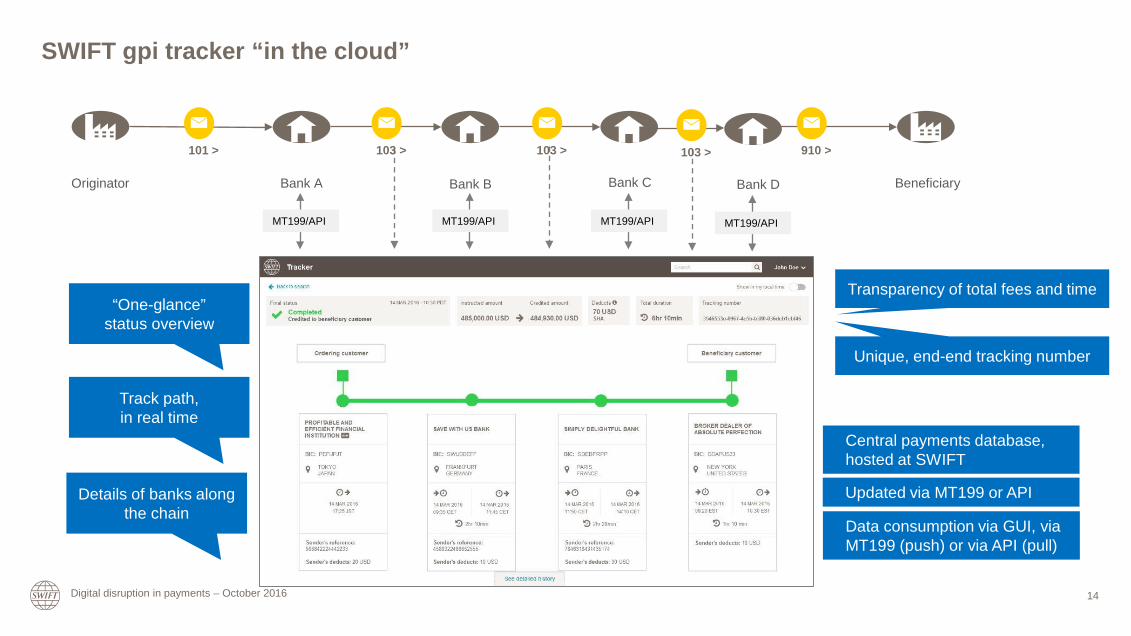

Central payments database, hosted at SWIFT

Updated via MT199 or API

Data consumption via GUI, via MT199 (push) or via API (pull)

SWIFT gpi tracker “in the cloud”

Bank A Bank BOriginator BeneficiaryBank C

Digital disruption in payments – October 2016

MT199/API

101 > 103 > 103 > 910 >

MT199/API MT199/API

“One-glance”status overview

Track path, in real time

Details of banks along the chain

Transparency of total fees and time

Unique, end-end tracking number

Bank D

103 >

MT199/API

14

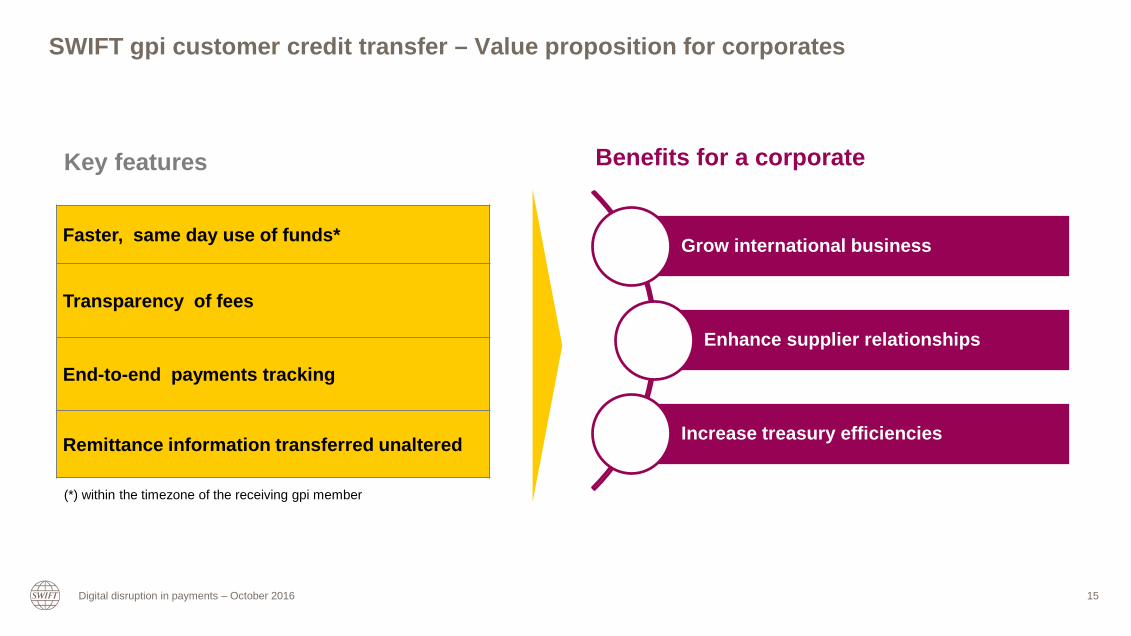

SWIFT gpi customer credit transfer – Value proposition for corporates

Faster, same day use of funds*

Transparency of fees

End-to-end payments tracking

Remittance information transferred unaltered

Digital disruption in payments – October 2016

Grow international business

Enhance supplier relationships

Increase treasury efficiencies

Benefits for a corporate Key features

(*) within the timezone of the receiving gpi member

15

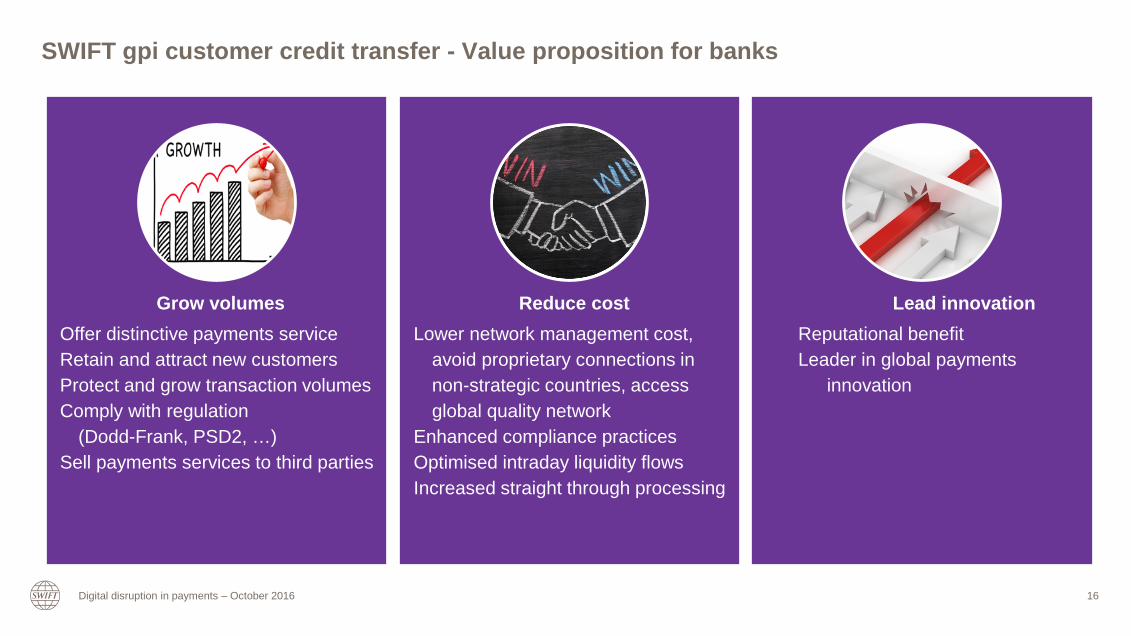

SWIFT gpi customer credit transfer - Value proposition for banks

Grow volumesOffer distinctive payments serviceRetain and attract new customersProtect and grow transaction volumesComply with regulation

(Dodd-Frank, PSD2, …)Sell payments services to third parties

Reduce costLower network management cost,

avoid proprietary connections in non-strategic countries, access global quality network

Enhanced compliance practicesOptimised intraday liquidity flowsIncreased straight through processing

Lead innovationReputational benefitLeader in global payments

innovation

Digital disruption in payments – October 2016 16

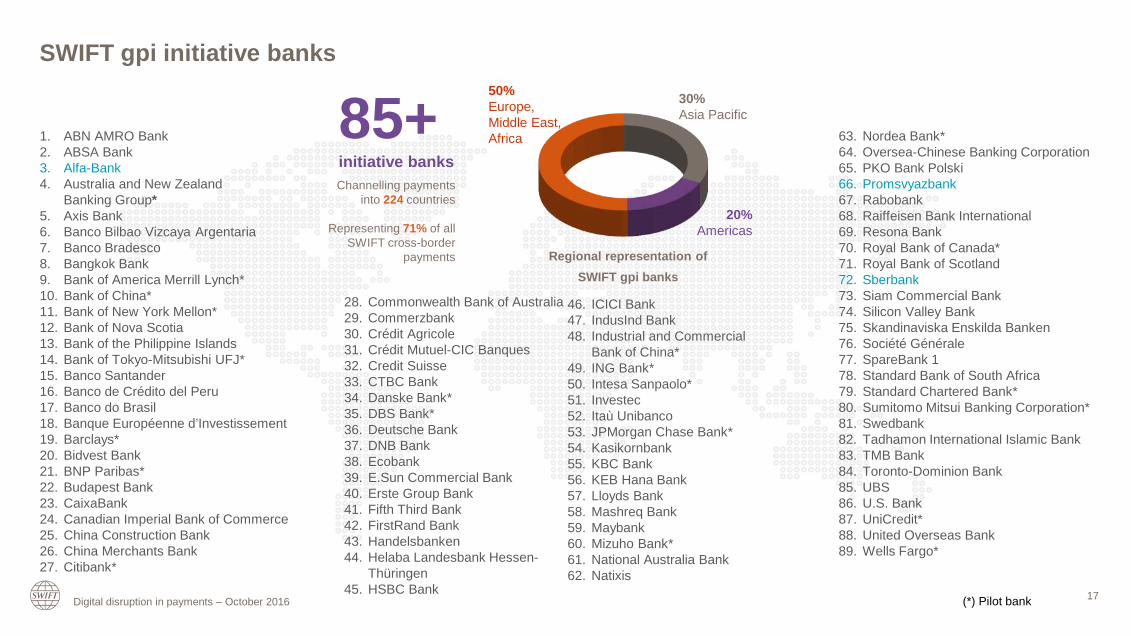

SWIFT gpi initiative banks

Regional representation ofSWIFT gpi banks

50% Europe, Middle East,Africa

30% Asia Pacific

20%Americas

63. Nordea Bank* 64. Oversea-Chinese Banking Corporation65. PKO Bank Polski66. Promsvyazbank67. Rabobank68. Raiffeisen Bank International69. Resona Bank70. Royal Bank of Canada*71. Royal Bank of Scotland72. Sberbank73. Siam Commercial Bank74. Silicon Valley Bank75. Skandinaviska Enskilda Banken76. Société Générale77. SpareBank 178. Standard Bank of South Africa79. Standard Chartered Bank*80. Sumitomo Mitsui Banking Corporation*81. Swedbank82. Tadhamon International Islamic Bank83. TMB Bank84. Toronto-Dominion Bank85. UBS86. U.S. Bank87. UniCredit*88. United Overseas Bank89. Wells Fargo*

46. ICICI Bank47. IndusInd Bank48. Industrial and Commercial

Bank of China*49. ING Bank*50. Intesa Sanpaolo*51. Investec52. Itaù Unibanco53. JPMorgan Chase Bank*54. Kasikornbank55. KBC Bank56. KEB Hana Bank57. Lloyds Bank58. Mashreq Bank59. Maybank60. Mizuho Bank*61. National Australia Bank62. Natixis

28. Commonwealth Bank of Australia29. Commerzbank30. Crédit Agricole31. Crédit Mutuel-CIC Banques32. Credit Suisse33. CTBC Bank34. Danske Bank*35. DBS Bank*36. Deutsche Bank37. DNB Bank38. Ecobank39. E.Sun Commercial Bank40. Erste Group Bank41. Fifth Third Bank42. FirstRand Bank43. Handelsbanken44. Helaba Landesbank Hessen-

Thüringen 45. HSBC Bank

(*) Pilot bank

1. ABN AMRO Bank2. ABSA Bank3. Alfa-Bank4. Australia and New Zealand

Banking Group*5. Axis Bank6. Banco Bilbao Vizcaya Argentaria7. Banco Bradesco8. Bangkok Bank9. Bank of America Merrill Lynch*10. Bank of China*11. Bank of New York Mellon*12. Bank of Nova Scotia13. Bank of the Philippine Islands14. Bank of Tokyo-Mitsubishi UFJ*15. Banco Santander16. Banco de Crédito del Peru17. Banco do Brasil18. Banque Européenne d’Investissement19. Barclays*20. Bidvest Bank21. BNP Paribas*22. Budapest Bank23. CaixaBank24. Canadian Imperial Bank of Commerce25. China Construction Bank 26. China Merchants Bank27. Citibank*

Digital disruption in payments – October 2016

85+initiative banksChannelling payments

into 224 countries

Representing 71% of all SWIFT cross-border

payments

17

Digital disruption in payments – October 2016

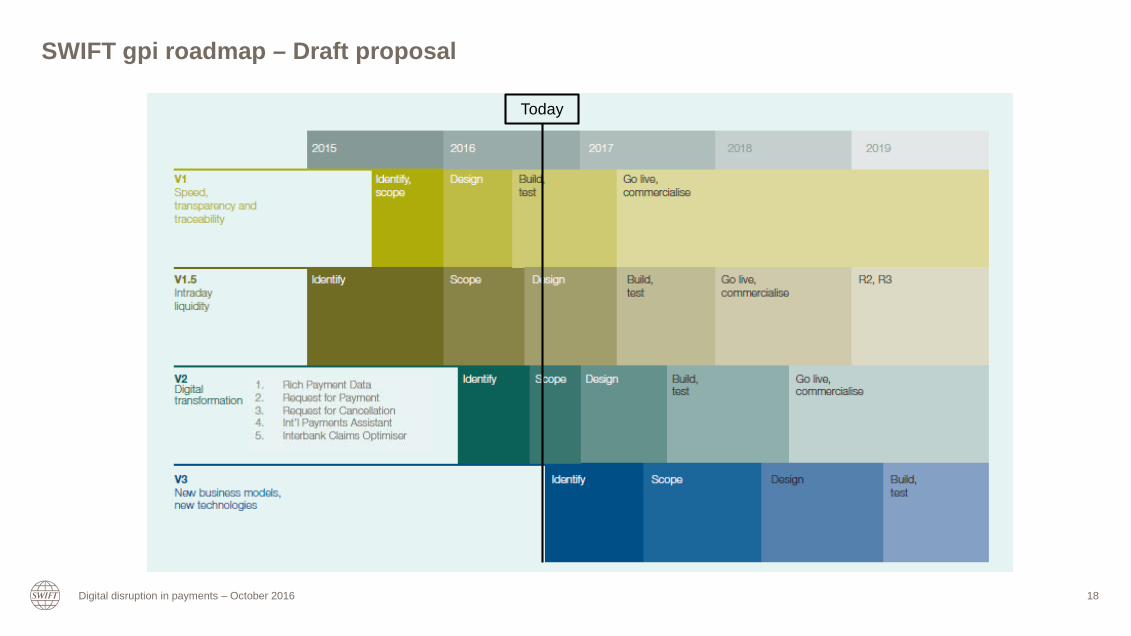

SWIFT gpi roadmap – Draft proposal

Today

18

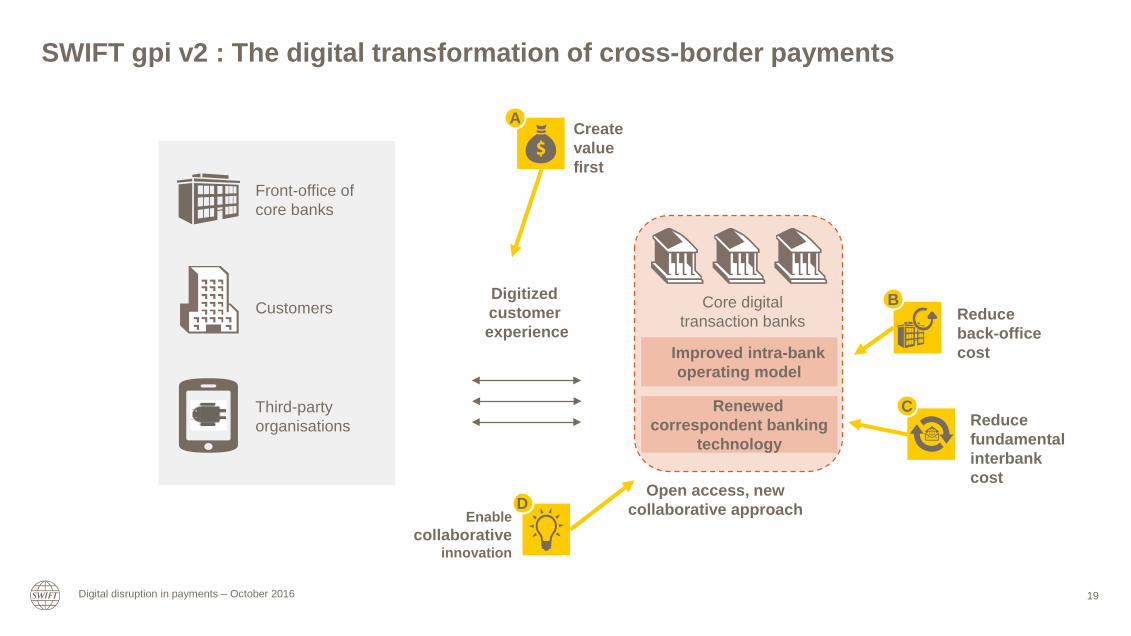

SWIFT gpi v2 : The digital transformation of cross-border payments

Digitized customer experience

Front-office of core banks

Third-party organisations

Customers

Renewed correspondent banking

technology

Improved intra-bank operating model

Open access, new collaborative approach

Core digital transaction banks

Create value first

Reduce back-office cost

Enable collaborative

innovation

Reduce fundamental interbank cost

A

B

C

D

Digital disruption in payments – October 2016 19

Market Infrastructures

v01

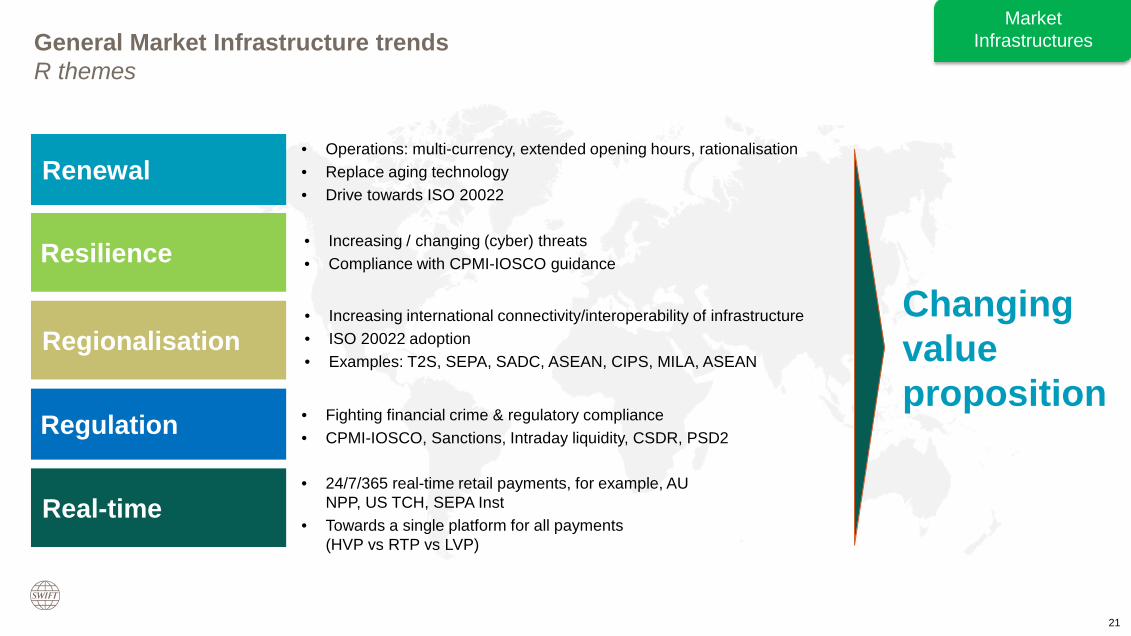

General Market Infrastructure trends R themes

21

• Fighting financial crime & regulatory compliance• CPMI-IOSCO, Sanctions, Intraday liquidity, CSDR, PSD2

• Increasing / changing (cyber) threats• Compliance with CPMI-IOSCO guidance

• Operations: multi-currency, extended opening hours, rationalisation• Replace aging technology• Drive towards ISO 20022

• Increasing international connectivity/interoperability of infrastructure• ISO 20022 adoption• Examples: T2S, SEPA, SADC, ASEAN, CIPS, MILA, ASEAN

Regulation

Regionalisation

Renewal

Resilience

• 24/7/365 real-time retail payments, for example, AU NPP, US TCH, SEPA Inst

• Towards a single platform for all payments (HVP vs RTP vs LVP)

Real-time

Changingvalue proposition

Market Infrastructures

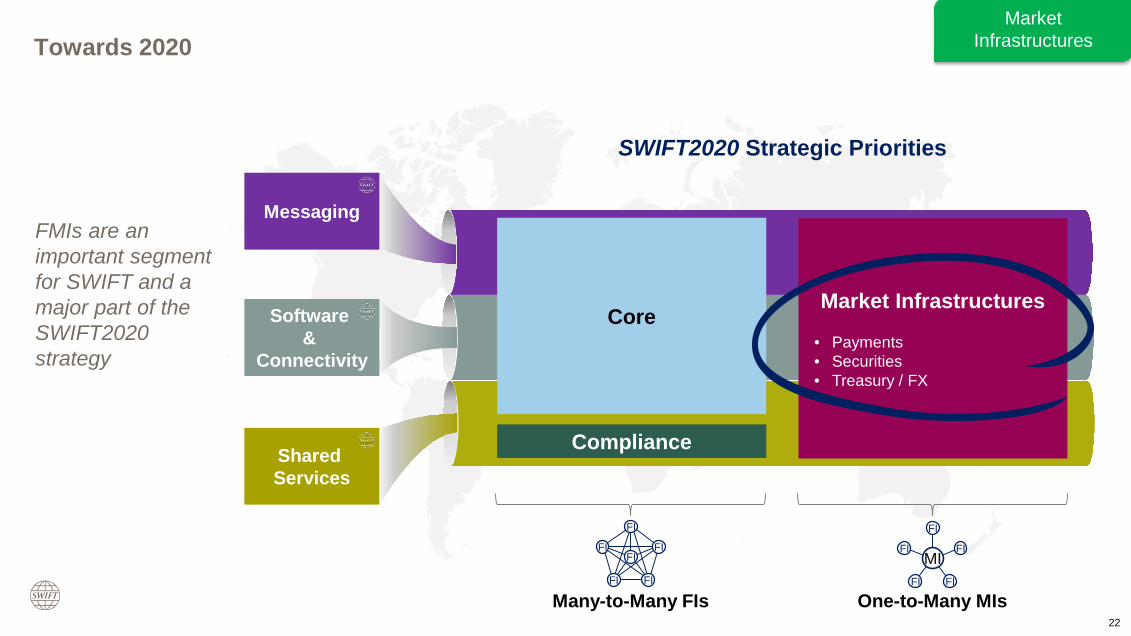

Towards 2020

22

SWIFT2020 Strategic Priorities

Software &

Connectivity

Messaging

Shared Services

One-to-Many MIsMany-to-Many FIs

MIFI

FI

FI

FI

FI

FI

FI

FI

FI

FI

FI

Market Infrastructures

• Payments• Securities• Treasury / FX

Core

Compliance

FMIs are an important segment for SWIFT and a major part of the SWIFT2020 strategy

Market Infrastructures

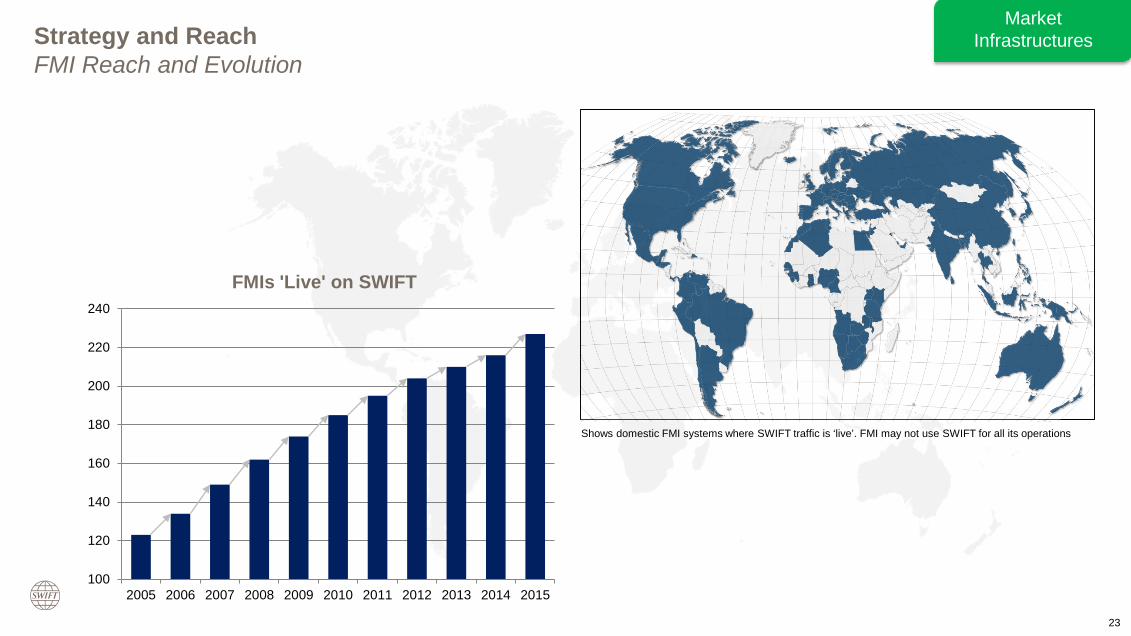

Strategy and ReachFMI Reach and Evolution

23

Shows domestic FMI systems where SWIFT traffic is ‘live’. FMI may not use SWIFT for all its operations

100

120

140

160

180

200

220

240

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

FMIs 'Live' on SWIFT

Market Infrastructures

High Value Payments

September 2016

v01

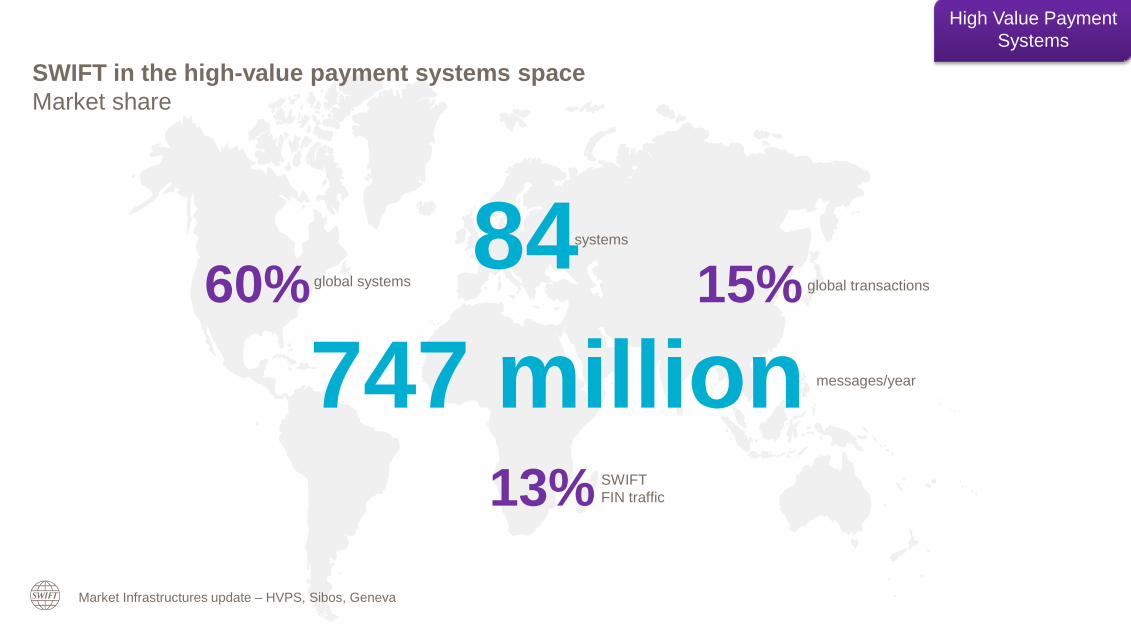

60% 84747 million messages/year

global systems

systems

15% global transactions

13% SWIFT FIN traffic

Market Infrastructures update – HVPS, Sibos, Geneva

SWIFT in the high-value payment systems spaceMarket share

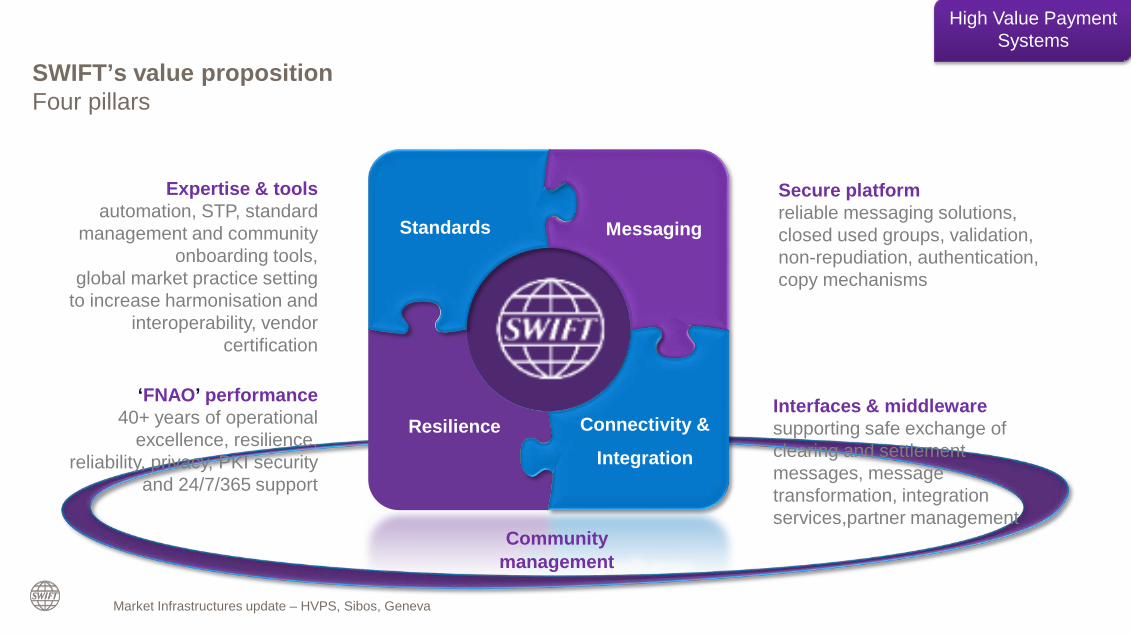

High Value Payment Systems

Standards Messaging

Resilience Connectivity &

Integration

Secure platformreliable messaging solutions, closed used groups, validation, non-repudiation, authentication, copy mechanisms

Expertise & toolsautomation, STP, standard

management and community onboarding tools,

global market practice setting to increase harmonisation and

interoperability, vendor certification

‘FNAO’ performance40+ years of operational

excellence, resilience, reliability, privacy, PKI security

and 24/7/365 support

Interfaces & middlewaresupporting safe exchange of clearing and settlement messages, message transformation, integration services,partner management

Market Infrastructures update – HVPS, Sibos, Geneva

SWIFT’s value propositionFour pillars

Communitymanagement

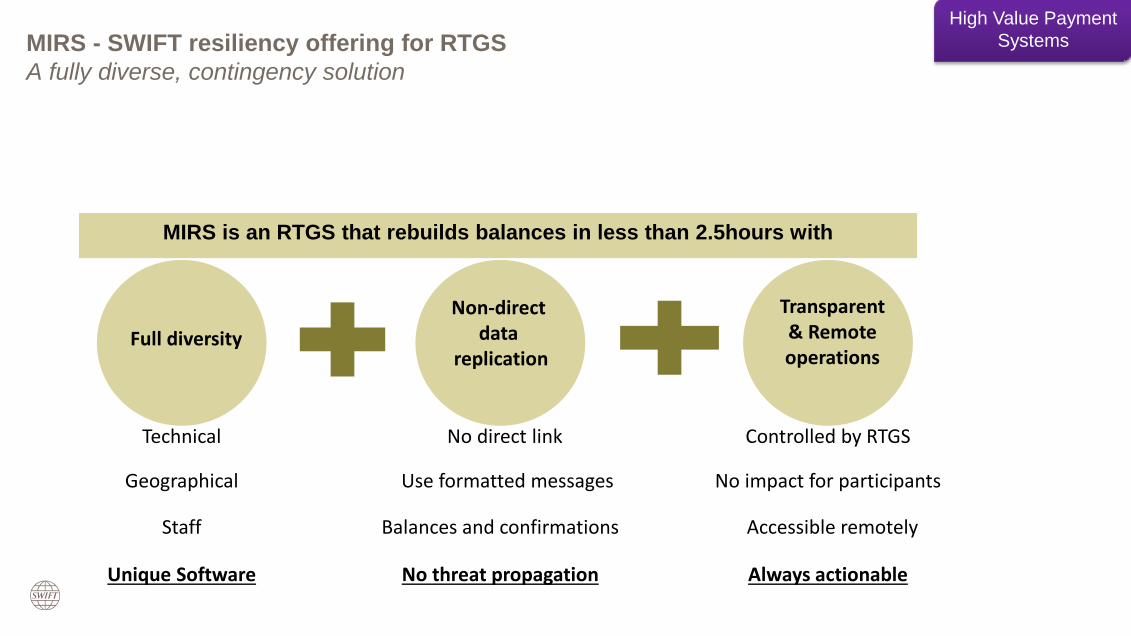

High Value Payment Systems

Technical

Full diversity

Geographical

Staff

Unique Software

Non-direct data

replication

Transparent& Remoteoperations

No direct link

Use formatted messages

Balances and confirmations

No threat propagation

Controlled by RTGS

No impact for participants

Accessible remotely

Always actionable

MIRS is an RTGS that rebuilds balances in less than 2.5hours with

MIRS - SWIFT resiliency offering for RTGSA fully diverse, contingency solution

High Value Payment Systems

Real-Time Payments

September 2016

v01

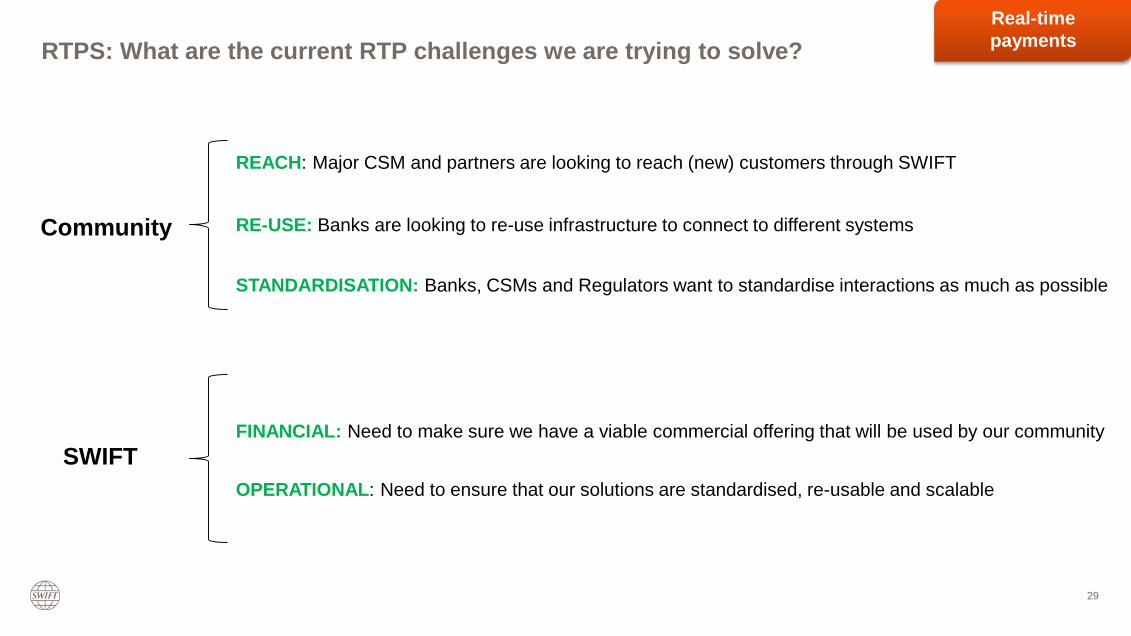

RTPS: What are the current RTP challenges we are trying to solve?

REACH: Major CSM and partners are looking to reach (new) customers through SWIFT

RE-USE: Banks are looking to re-use infrastructure to connect to different systems

STANDARDISATION: Banks, CSMs and Regulators want to standardise interactions as much as possible

OPERATIONAL: Need to ensure that our solutions are standardised, re-usable and scalable

Community

SWIFTFINANCIAL: Need to make sure we have a viable commercial offering that will be used by our community

29

Real-time payments

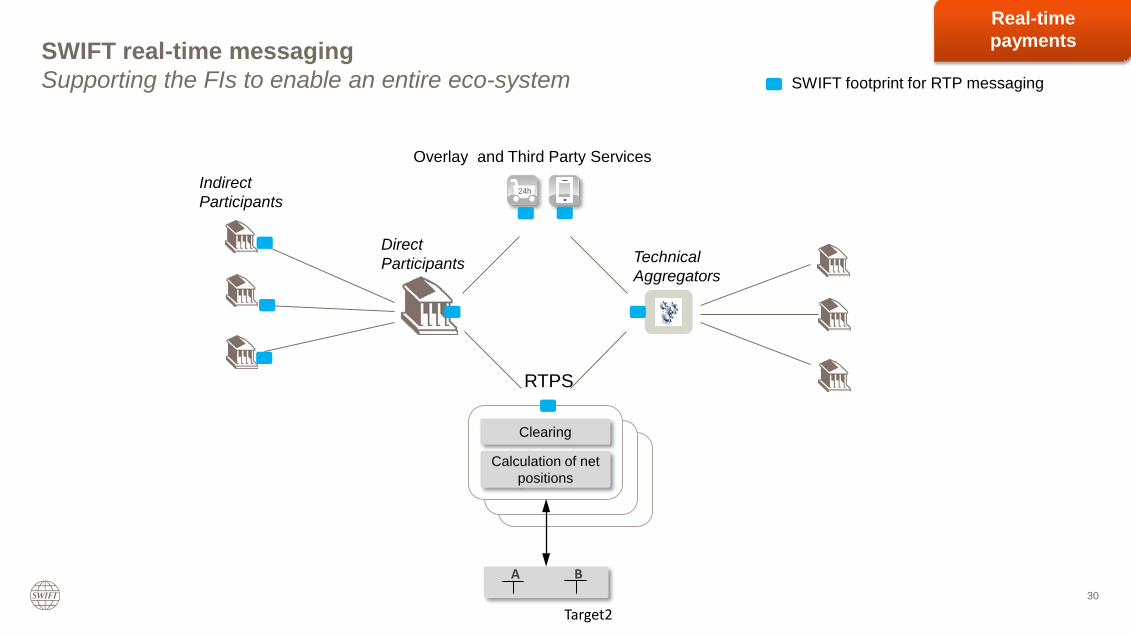

SWIFT real-time messagingSupporting the FIs to enable an entire eco-system

A B

Target2

Clearing

Calculation of net positions

24h

Overlay and Third Party Services

RTPS

DirectParticipants

Indirect Participants

Technical Aggregators

SWIFT footprint for RTP messaging

30

Real-time payments

ISO 20022 Harmonisation Charter

September 2016

v01

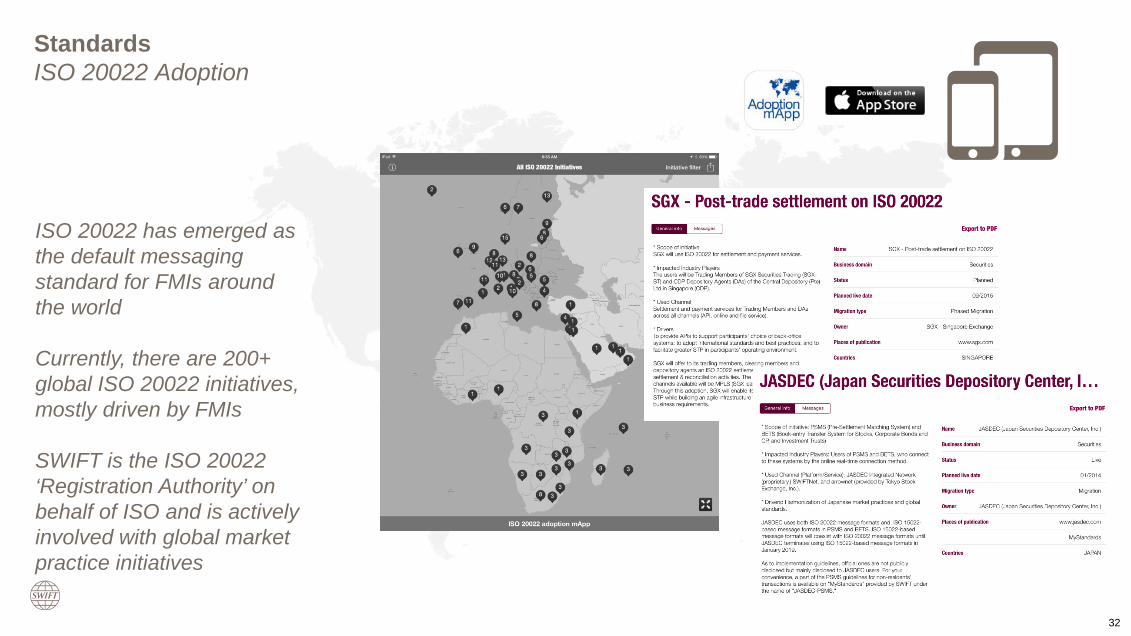

StandardsISO 20022 Adoption

32

ISO 20022 has emerged as the default messaging standard for FMIs around the world

Currently, there are 200+ global ISO 20022 initiatives, mostly driven by FMIs

SWIFT is the ISO 20022 ‘Registration Authority’ on behalf of ISO and is actively involved with global market practice initiatives

Share information• ISO 20022 information including Message

types, release timelines, and declaration of compliance with global market practice

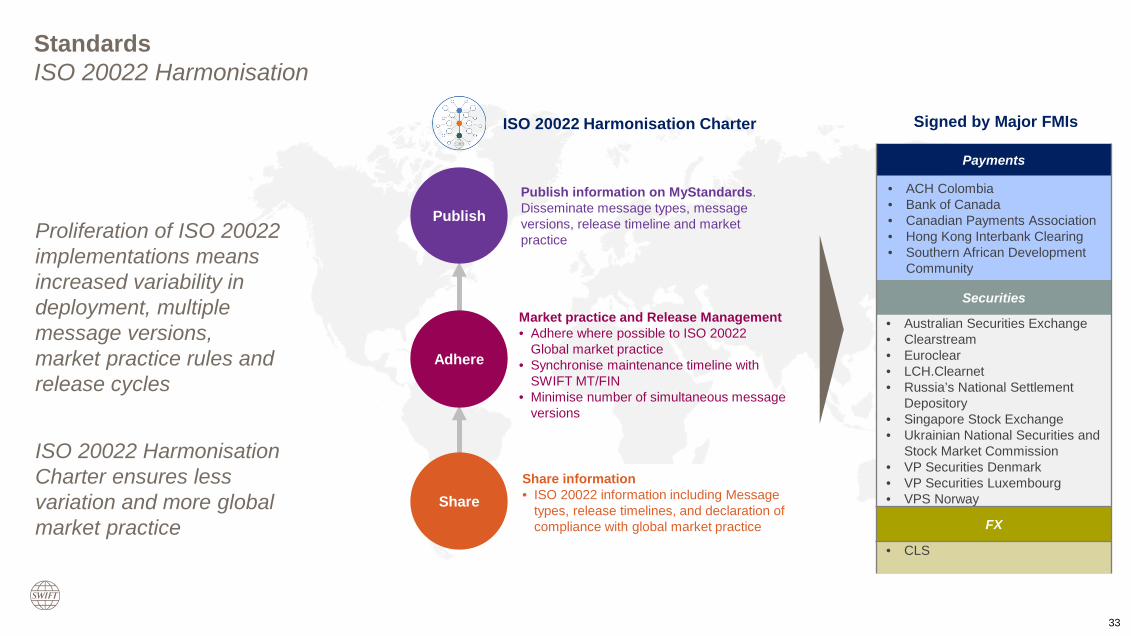

StandardsISO 20022 Harmonisation

33

Publish

Adhere

Share

Publish information on MyStandards. Disseminate message types, message versions, release timeline and market practice

ISO 20022 Harmonisation Charter

Proliferation of ISO 20022 implementations means increased variability in deployment, multiple message versions, market practice rules and release cycles

ISO 20022 HarmonisationCharter ensures less variation and more global market practice

Signed by Major FMIs

Payments

• ACH Colombia• Bank of Canada• Canadian Payments Association• Hong Kong Interbank Clearing• Southern African Development

Community

Securities

• Australian Securities Exchange• Clearstream• Euroclear• LCH.Clearnet• Russia’s National Settlement

Depository• Singapore Stock Exchange• Ukrainian National Securities and

Stock Market Commission• VP Securities Denmark• VP Securities Luxembourg• VPS Norway

FX

• CLS

Market practice and Release Management• Adhere where possible to ISO 20022

Global market practice• Synchronise maintenance timeline with

SWIFT MT/FIN• Minimise number of simultaneous message

versions

www.swift.com

SWIFT Instant Payment Solution 34