Embed Size (px)

Citation preview

Is there manufacturer loyalty in the UK’s B2B automotive market?

23/06/2016

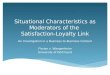

Fleet sales = Cars, LCVs, HGVs, pool cars, motability, courtesy cars, daily rental

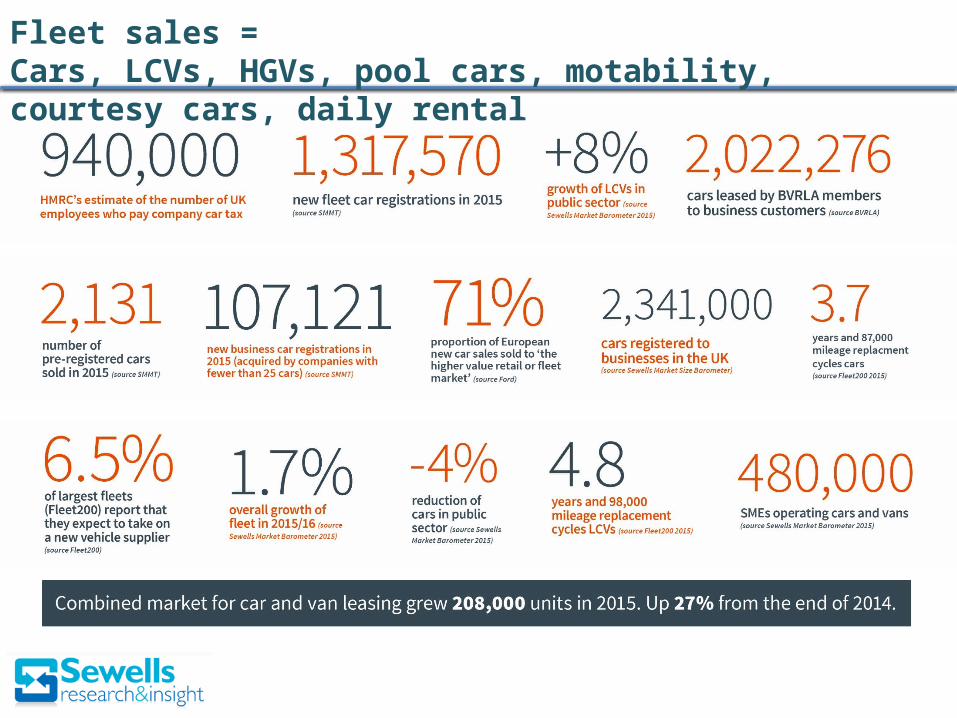

38% (485,000) of UK companies manage business cars and/or LCVs

UK fleets

70%

25%

4%1%

250+ employees

50-249 employees

10-49 employees

1-9 employees

UK fleet vehicles

55%

45%

250+ employees

< 250 employees

Source: Sewells Fleet Market Barometer 2015Sample size, 1,000 UK businesses (1+ employees)

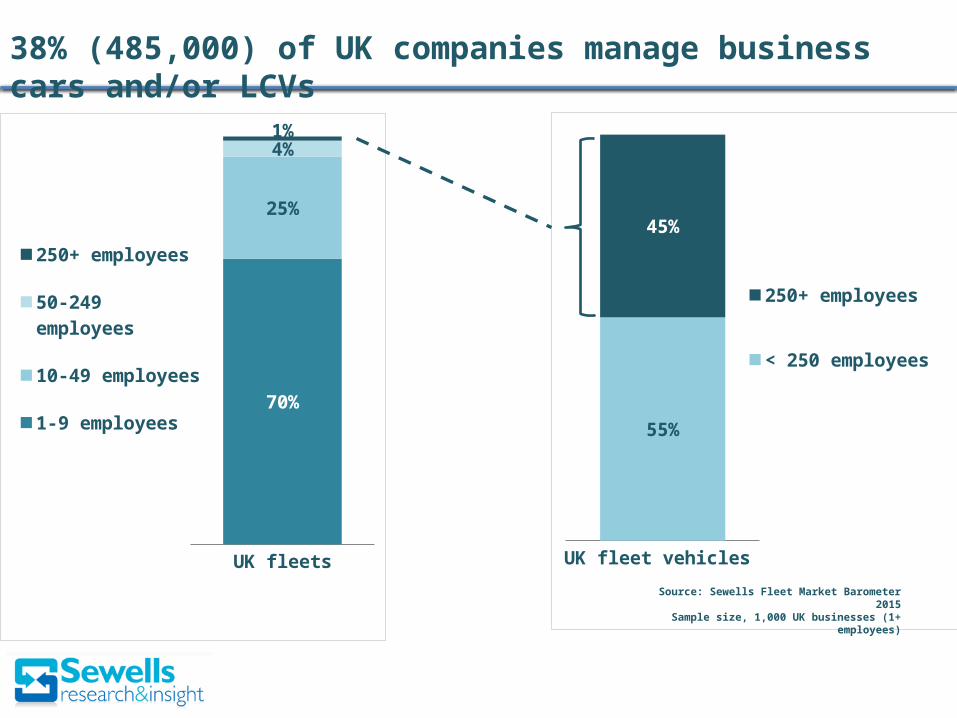

Can one fleet supplier reconcile all of these competing demands?

User chooser

LCV drivers Cash allowance

Restricted badge drivers

Grey Fleet

Business, fleet and driver decision making groups

Source: Sewells SME Fleet Dynamics 2016

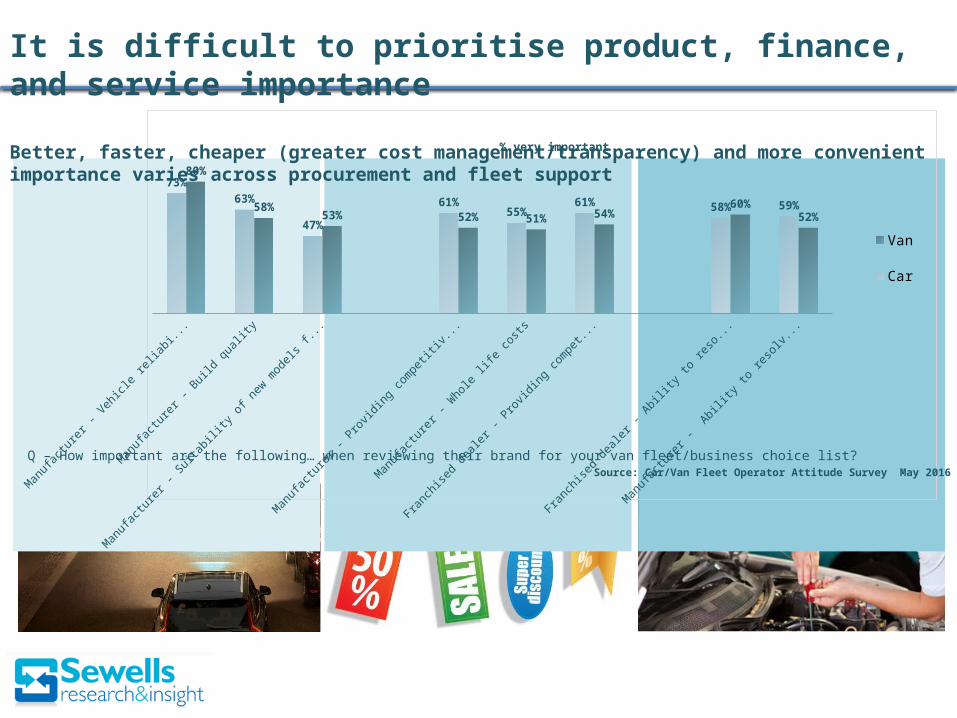

52%60%

54%51%52%53%58%

80%

59%58%61%55%

61%

47%

63%73%

% very important

Van

Car

It is difficult to prioritise product, finance, and service importance

Better, faster, cheaper (greater cost management/transparency) and more convenient importance varies across procurement and fleet support

Q – How important are the following… when reviewing their brand for your van fleet/business choice list?Source: Car/Van Fleet Operator Attitude Survey May 2016

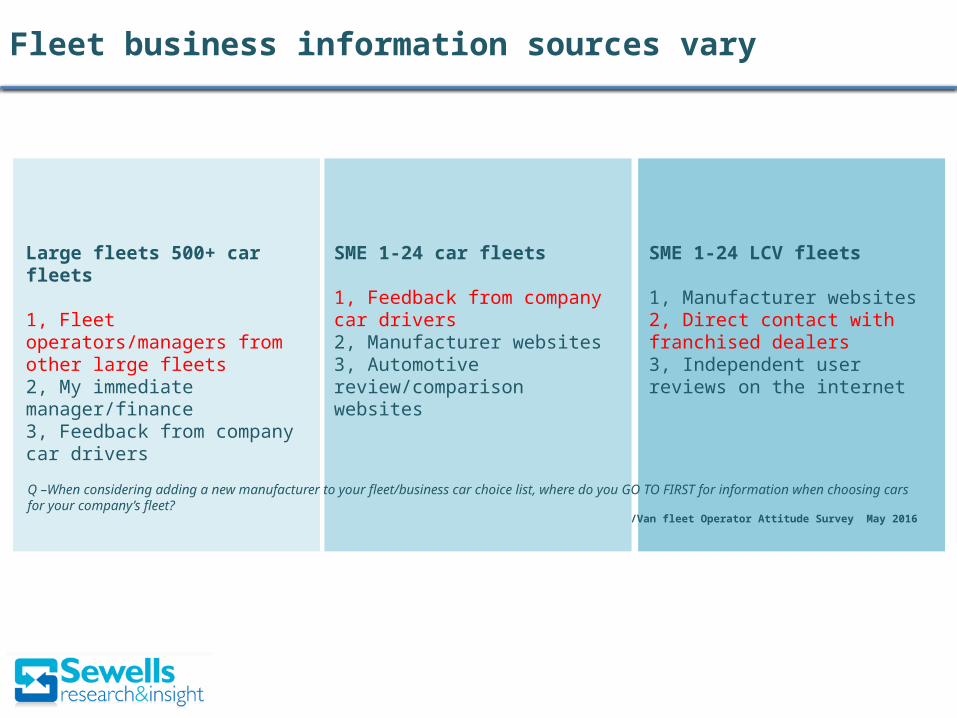

SME 1-24 LCV fleets

1, Manufacturer websites2, Direct contact with franchised dealers3, Independent user reviews on the internet

Source: Car/Van fleet Operator Attitude Survey May 2016

SME 1-24 car fleets

1, Feedback from company car drivers2, Manufacturer websites3, Automotive review/comparison websites

Large fleets 500+ car fleets

1, Fleet operators/managers from other large fleets2, My immediate manager/finance3, Feedback from company car drivers

Q –When considering adding a new manufacturer to your fleet/business car choice list, where do you GO TO FIRST for information when choosing cars for your company’s fleet?

Fleet business information sources vary

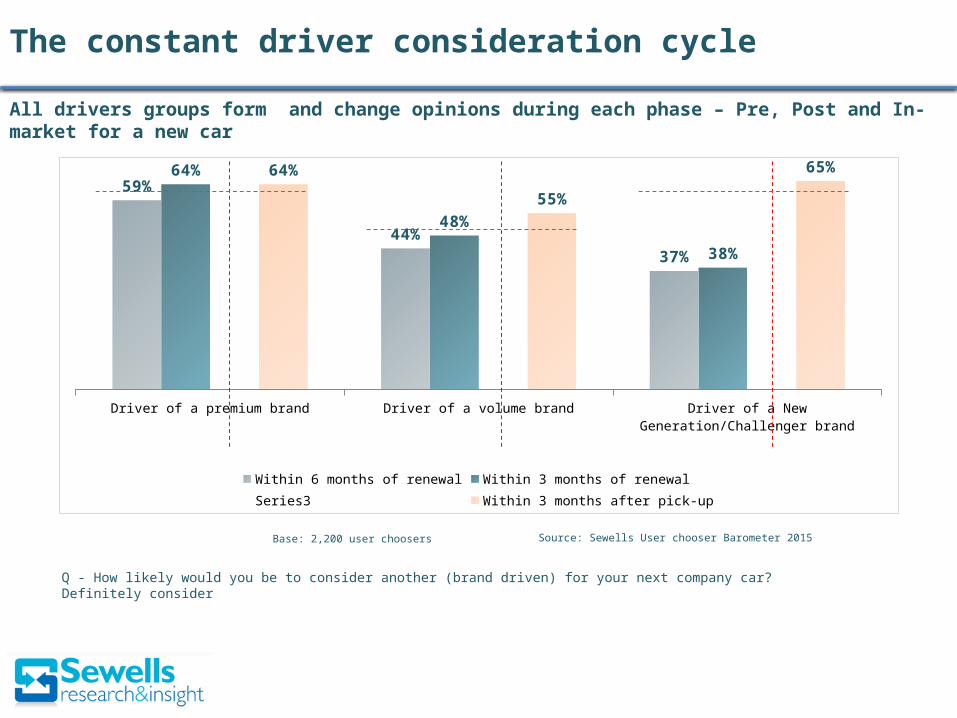

Driver of a premium brand Driver of a volume brand Driver of a New Generation/Challenger brand

59%

44%

37%

64%

48%

38%

64%

55%

65%

Within 6 months of renewal Within 3 months of renewal Series3 Within 3 months after pick-up

Q - How likely would you be to consider another (brand driven) for your next company car? Definitely consider

Base: 2,200 user choosers

The constant driver consideration cycle

All drivers groups form and change opinions during each phase – Pre, Post and In-market for a new car

Source: Sewells User chooser Barometer 2015

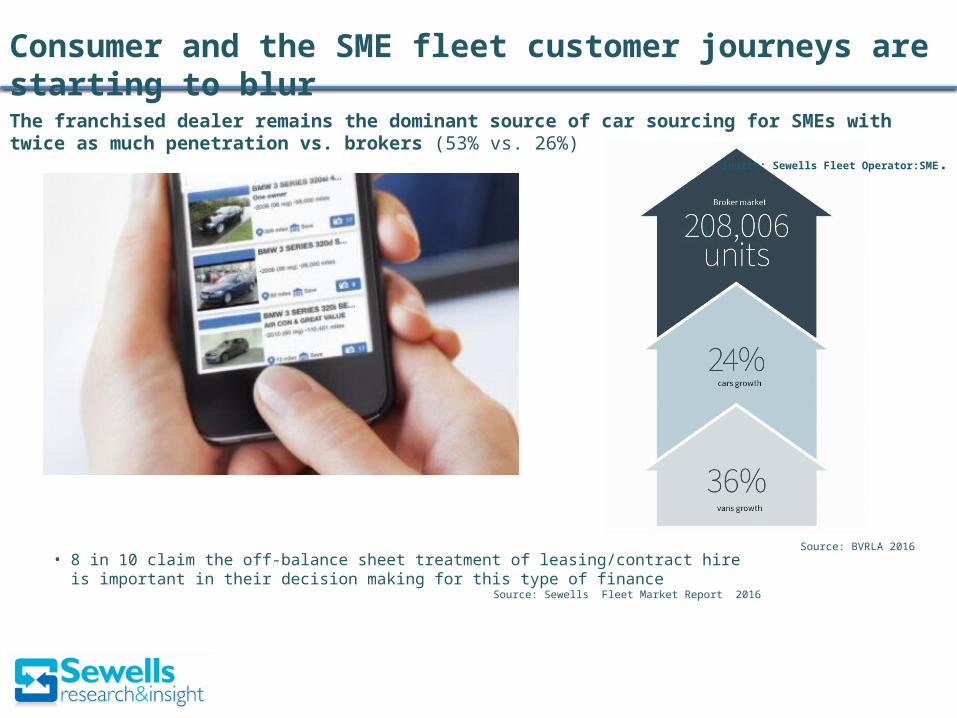

Disruptions to existing supplier relationships

• 8 in 10 claim the off-balance sheet treatment of leasing/contract hire is important in their decision making for this type of finance

Source: Sewells Fleet Market Report 2016

Source: BVRLA 2016

Consumer and the SME fleet customer journeys are starting to blur

The franchised dealer remains the dominant source of car sourcing for SMEs with twice as much penetration vs. brokers (53% vs. 26%)

Source: Sewells Fleet Operator:SME.

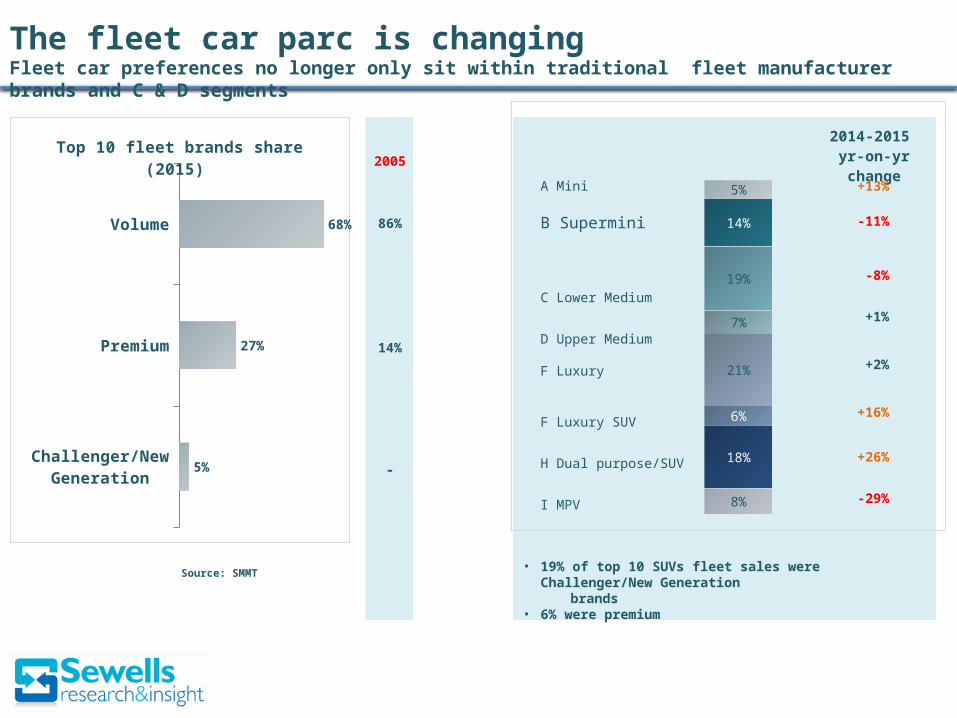

8%

18%

6%

21%

7%

19%

14%

5%

2014-2015 yr-on-yr change

A Mini

B Supermini

C Lower Medium

D Upper Medium

F Luxury

F Luxury SUV

H Dual purpose/SUV

I MPV

• 19% of top 10 SUVs fleet sales were Challenger/New Generation brands• 6% were premium

+13%

-11%

-8%

+1%

+2%

+16%

+26%

-29%

The fleet car parc is changingFleet car preferences no longer only sit within traditional fleet manufacturer brands and C & D segments

Source: SMMT

Challenger/New Gen-eration

Premium

Volume

5%

27%

68%

Top 10 fleet brands share (2015) 2005

86%

14%

-

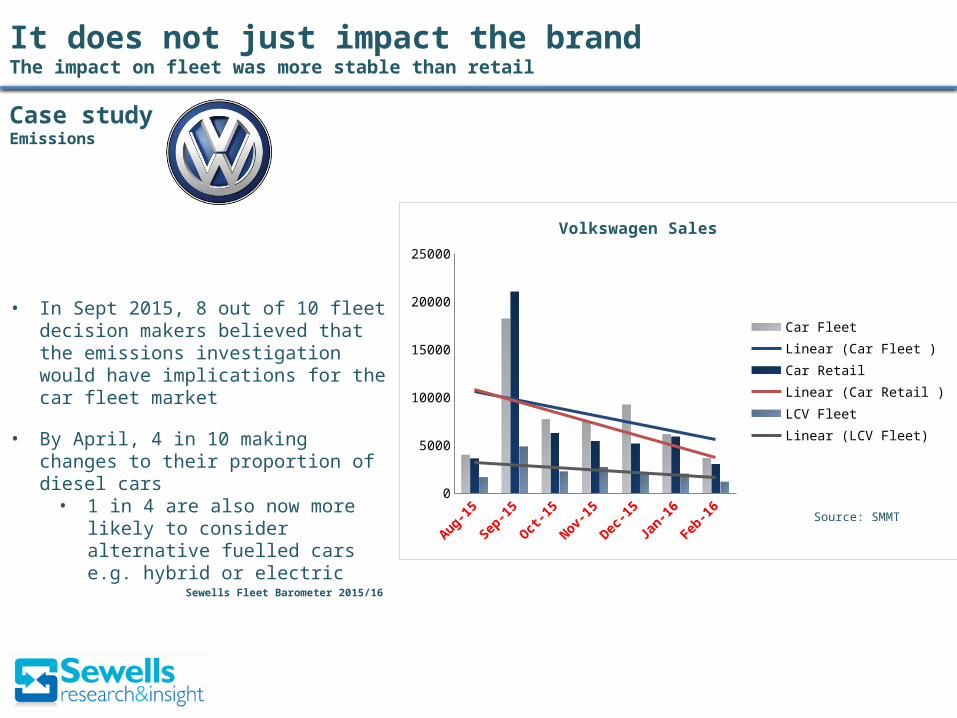

• In Sept 2015, 8 out of 10 fleet decision makers believed that the emissions investigation would have implications for the car fleet market

• By April, 4 in 10 making changes to their proportion of diesel cars• 1 in 4 are also now more likely to

consider alternative fuelled cars e.g. hybrid or electric

Sewells Fleet Barometer 2015/16

Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-160

5000

10000

15000

20000

25000

Volkswagen Sales

Car Fleet Linear (Car Fleet )Car Retail Linear (Car Retail )LCV FleetLinear (LCV Fleet)

Source: SMMT

It does not just impact the brandThe impact on fleet was more stable than retail

Case study Emissions

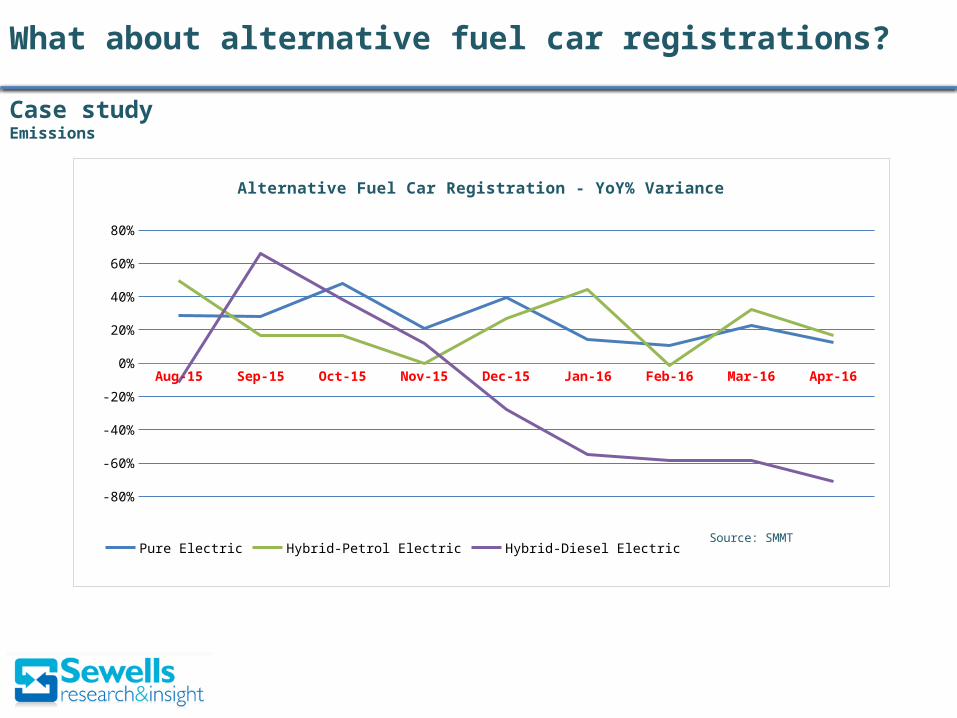

Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Alternative Fuel Car Registration - YoY% Variance

Pure Electric Hybrid-Petrol Electric Hybrid-Diesel ElectricSource: SMMT

What about alternative fuel car registrations?

Case study Emissions

Pledge to accelerate the introduction of an ultra low emissions zone in London.

At least 5 other UK expected to follow

Barriers to adoption:• Electric vehicle range and access to charge

points

41% of fleets have introduced/considering the introduction of hybrid vehicles over diesel. 20% are considering electric vehicles

Source: Sewells Alternative White Paper 2016

By 2020 estimates say 10% of new car registrations will be electricFour years, one vehicle replacement cycle to act

Conclusion: Prioritising future customer groups

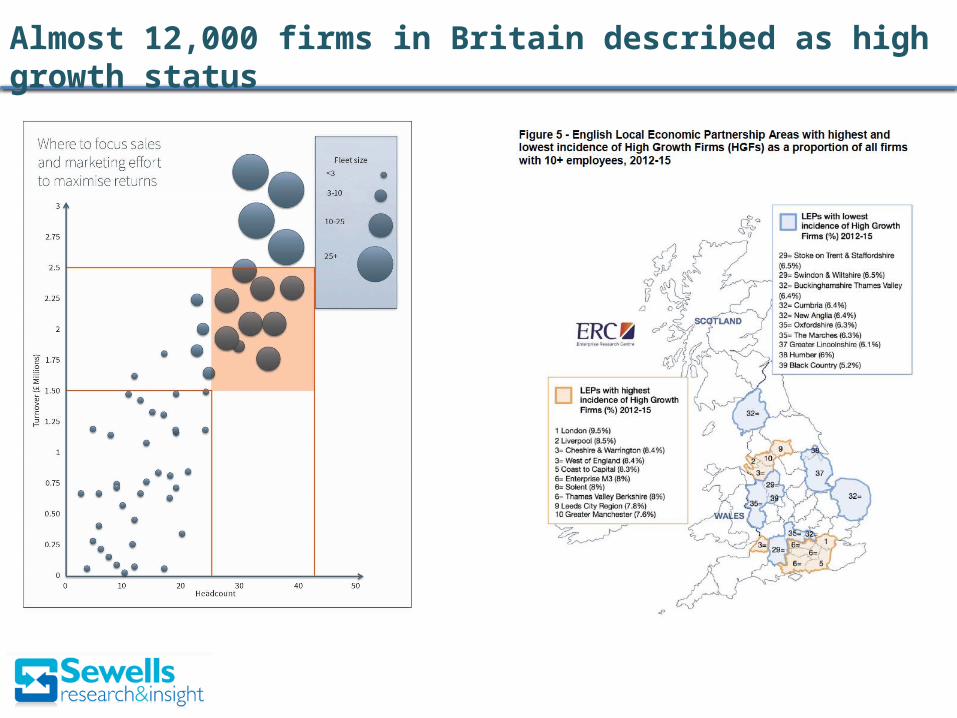

Almost 12,000 firms in Britain described as high growth status

Segments: Trade, Business, Delivery, Administration, Professional services, Manufacturing, Public sector man's meat is another man's poison

Trade Services Professional Services

There are influencers during key stages of business growth