Embed Size (px)

Citation preview

Global Export Market Opportunities and

End Market Growth for Plastics

Presented By:

Michael D. Taylor

Vice President, International Affairs and Trade

SPI South Regional Workshop

BMW Performance Center

Greer, South Carolina

September 15, 2015

Agenda Overview of the U.S. Economy and Manufacturing

U.S. Plastics Industry

Trade Flows & Global Market Opportunities

SPI’s Plastics Market Watch Series

Focus on Automotive, Medical & Packaging End Markets

Q&A

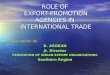

Real GDP Growth through 2016

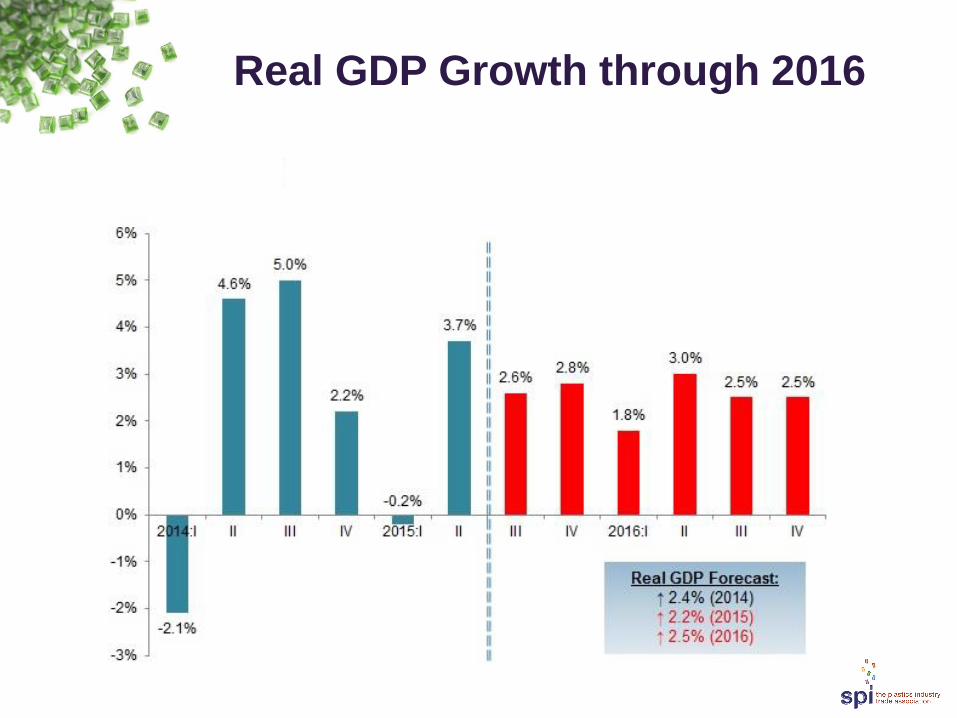

ISM Manufacturing Purchasing

Managers’ Index

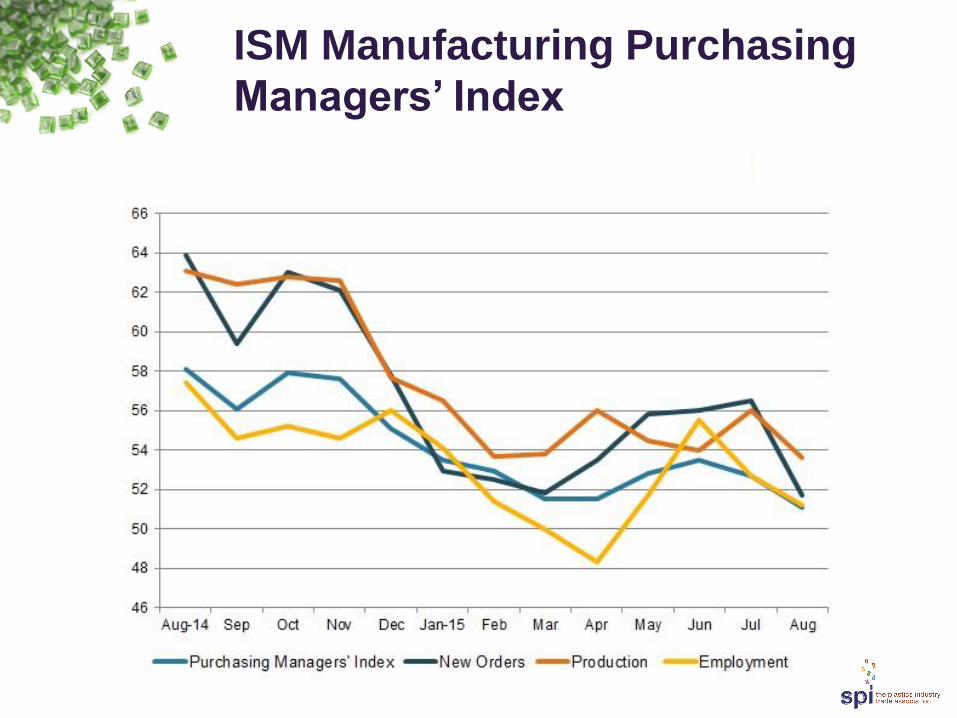

U.S. Demand for Plastics sets

New High Level

$0

$50

$100

$150

$200

$250

$300

$350

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$ in b

illio

ns

Machinery Molds Plastic Products Resin

Apparent Consumption = Shipments + Imports – Exports

Source: SPI “Global Business Trends” (2015)

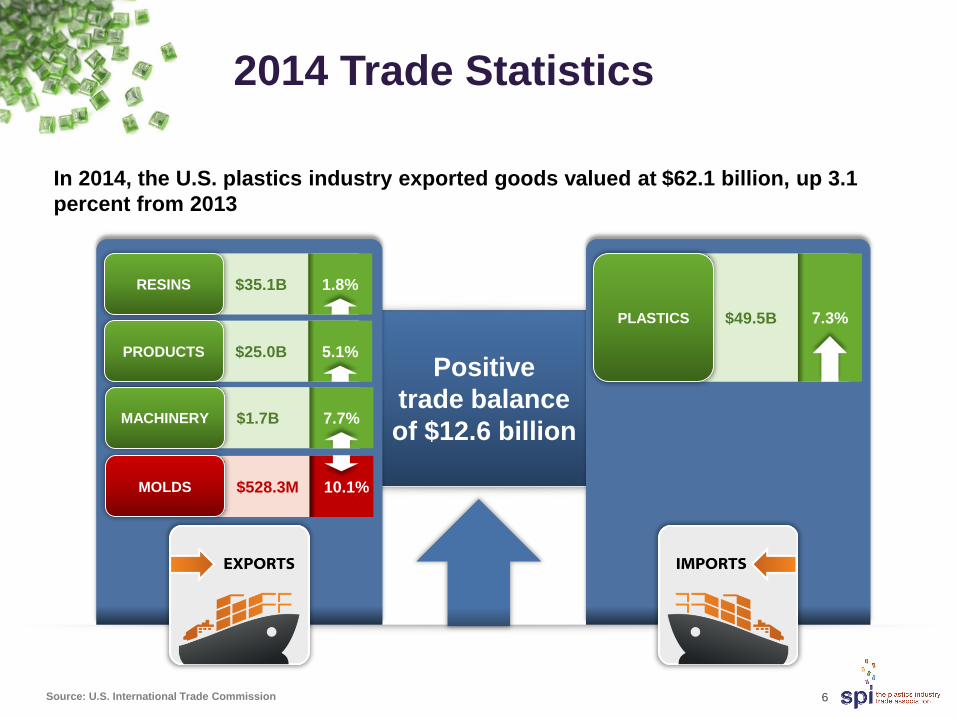

Positive

trade balance

of $12.6 billion

$49.5B PLASTICS 7.3%

2014 Trade Statistics

6

In 2014, the U.S. plastics industry exported goods valued at $62.1 billion, up 3.1

percent from 2013

$35.1B RESINS 1.8%

$25.0B PRODUCTS 5.1%

$528.3M MOLDS 10.1%

$1.7B MACHINERY 7.7%

Source: U.S. International Trade Commission

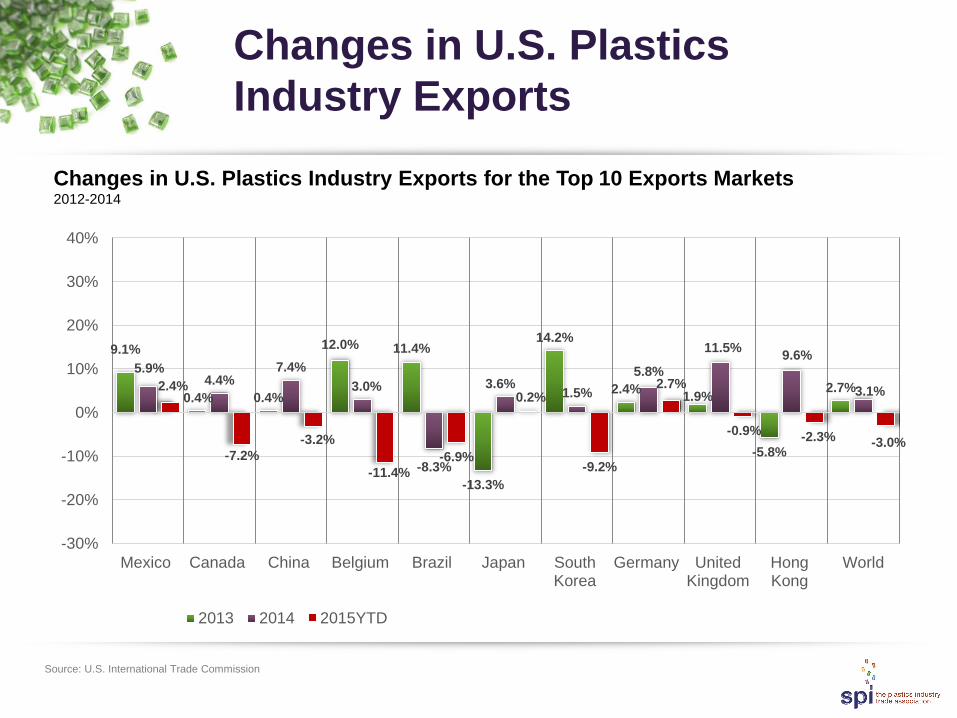

Changes in U.S. Plastics

Industry Exports

9.1%

0.4% 0.4%

12.0% 11.4%

-13.3%

14.2%

2.4% 1.9%

-5.8%

2.7%

5.9% 4.4%

7.4%

3.0%

-8.3%

3.6% 1.5%

5.8%

11.5% 9.6%

3.1% 2.4%

-7.2%

-3.2%

-11.4%

-6.9%

0.2%

-9.2%

2.7%

-0.9% -2.3% -3.0%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Mexico Canada China Belgium Brazil Japan SouthKorea

Germany UnitedKingdom

HongKong

World

2013 2014 2015YTD

Changes in U.S. Plastics Industry Exports for the Top 10 Exports Markets 2012-2014

Source: U.S. International Trade Commission

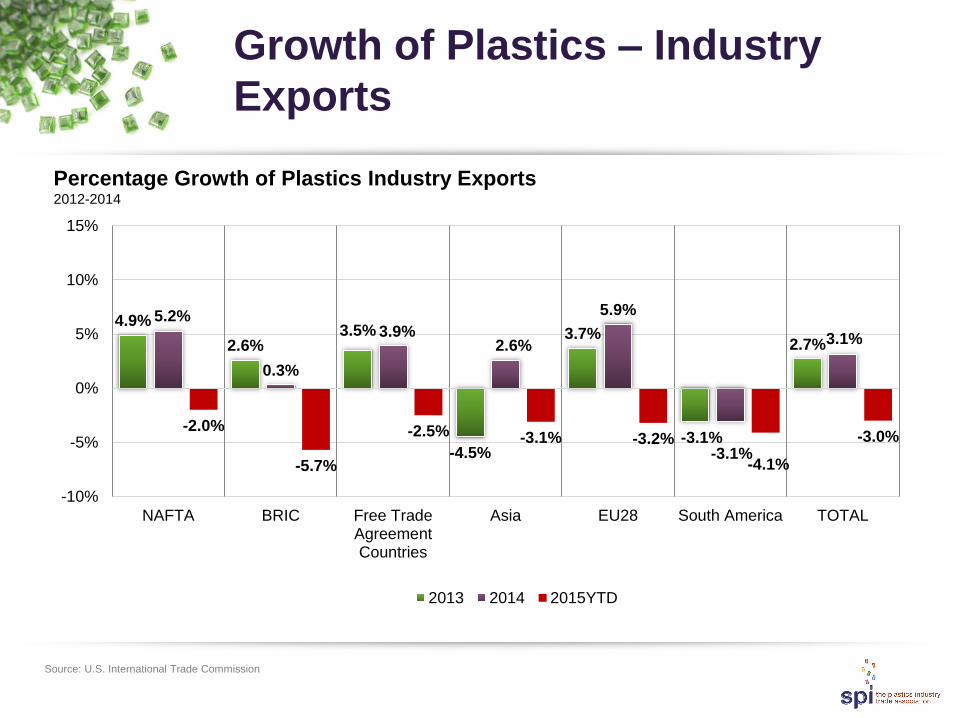

Growth of Plastics – Industry

Exports

4.9%

2.6% 3.5%

-4.5%

3.7%

-3.1%

2.7%

5.2%

0.3%

3.9% 2.6%

5.9%

-3.1%

3.1%

-2.0%

-5.7%

-2.5% -3.1% -3.2%

-4.1%

-3.0%

-10%

-5%

0%

5%

10%

15%

NAFTA BRIC Free TradeAgreementCountries

Asia EU28 South America TOTAL

2013 2014 2015YTD

Percentage Growth of Plastics Industry Exports 2012-2014

Source: U.S. International Trade Commission

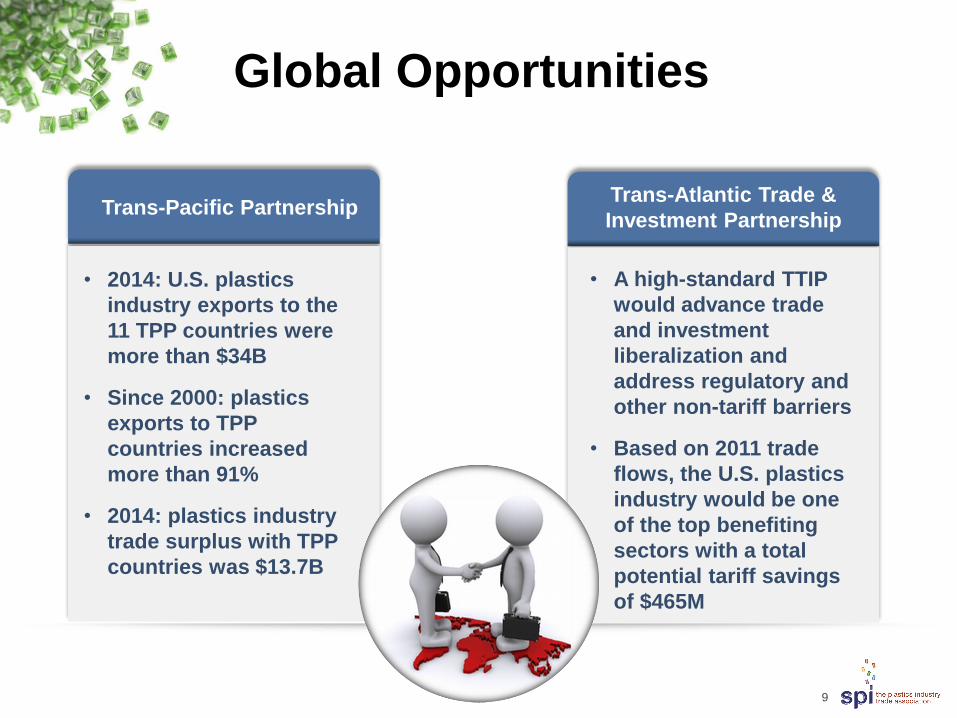

Trans-Pacific Partnership Trans-Atlantic Trade &

Investment Partnership

Global Opportunities

9

• 2014: U.S. plastics

industry exports to the

11 TPP countries were

more than $34B

• Since 2000: plastics

exports to TPP

countries increased

more than 91%

• 2014: plastics industry

trade surplus with TPP

countries was $13.7B

• A high-standard TTIP

would advance trade

and investment

liberalization and

address regulatory and

other non-tariff barriers

• Based on 2011 trade

flows, the U.S. plastics

industry would be one

of the top benefiting

sectors with a total

potential tariff savings

of $465M

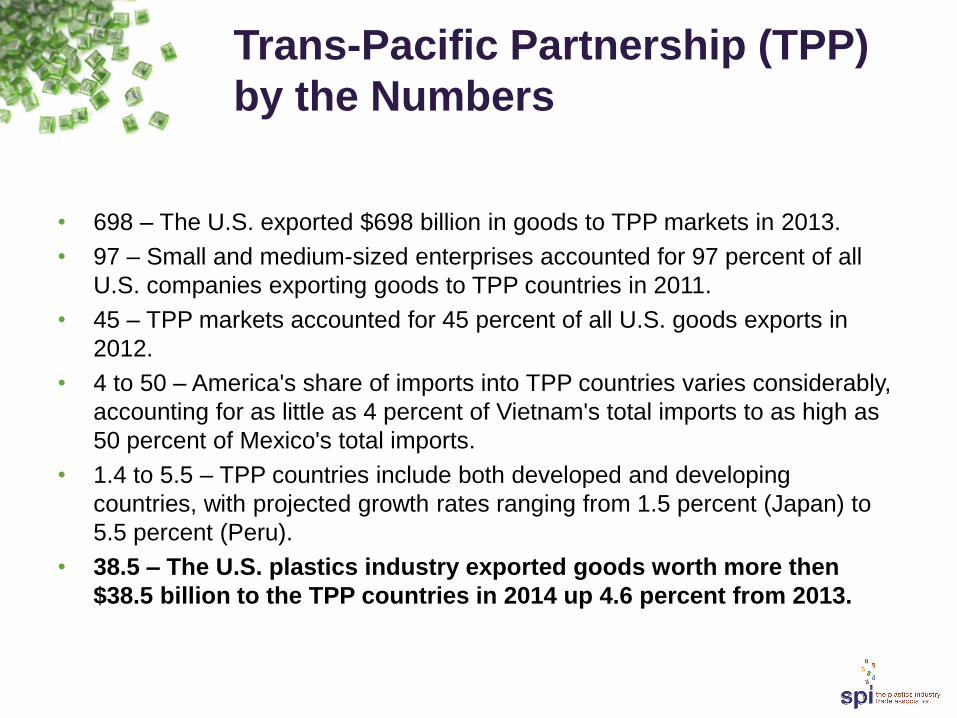

Trans-Pacific Partnership (TPP)

by the Numbers

• 698 – The U.S. exported $698 billion in goods to TPP markets in 2013.

• 97 – Small and medium-sized enterprises accounted for 97 percent of all

U.S. companies exporting goods to TPP countries in 2011.

• 45 – TPP markets accounted for 45 percent of all U.S. goods exports in

2012.

• 4 to 50 – America's share of imports into TPP countries varies considerably,

accounting for as little as 4 percent of Vietnam's total imports to as high as

50 percent of Mexico's total imports.

• 1.4 to 5.5 – TPP countries include both developed and developing

countries, with projected growth rates ranging from 1.5 percent (Japan) to

5.5 percent (Peru).

• 38.5 – The U.S. plastics industry exported goods worth more then

$38.5 billion to the TPP countries in 2014 up 4.6 percent from 2013.

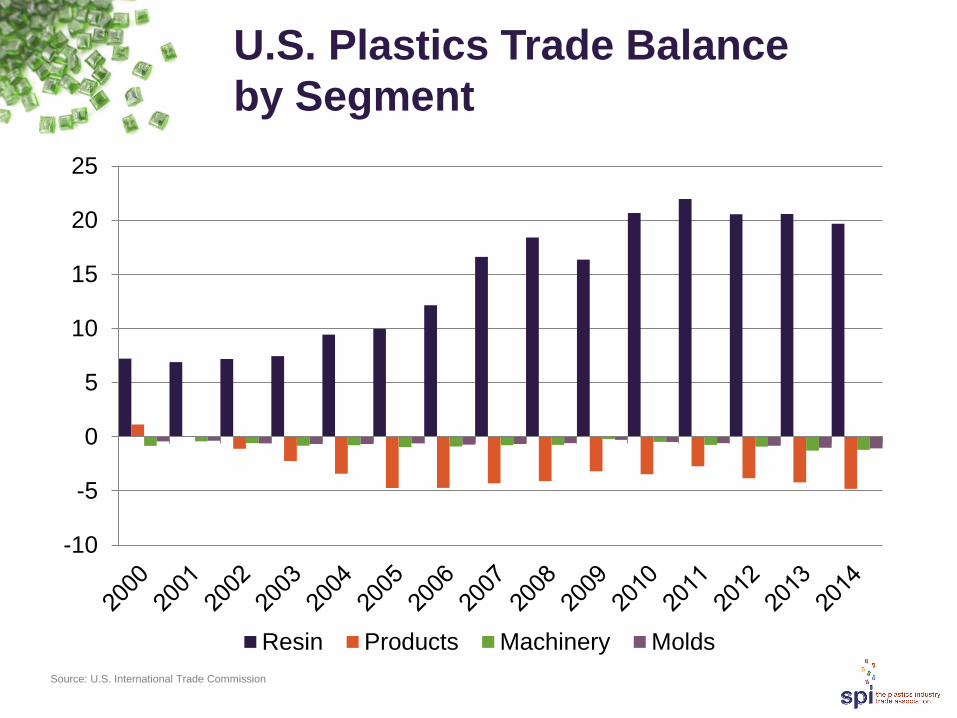

U.S. Plastics Trade Balance

by Segment

Source: U.S. International Trade Commission

-10

-5

0

5

10

15

20

25

Resin Products Machinery Molds

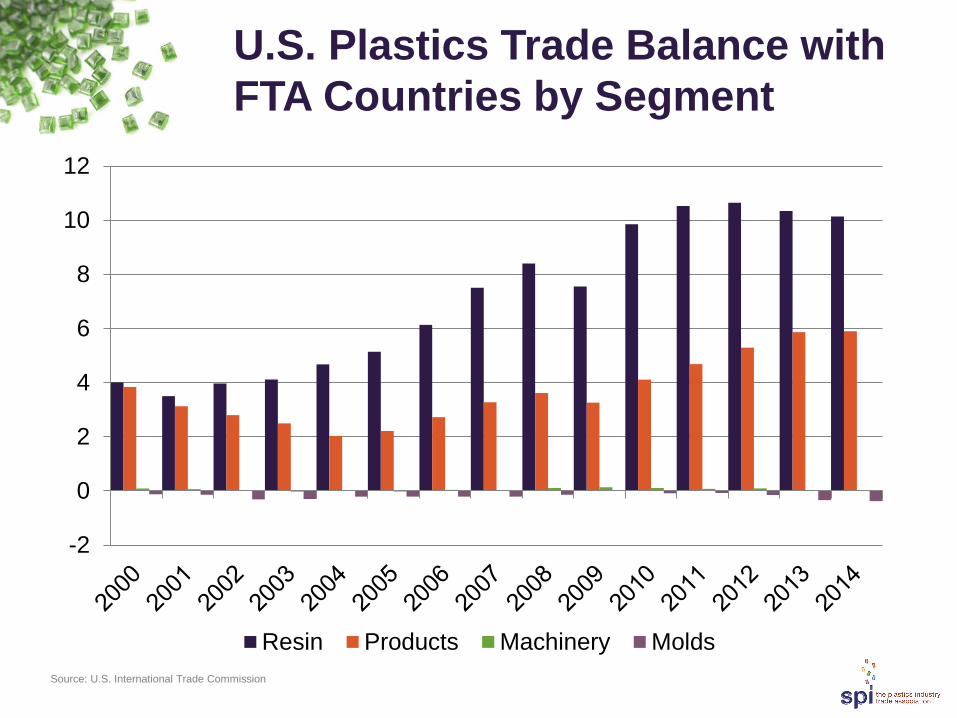

U.S. Plastics Trade Balance with

FTA Countries by Segment

Source: U.S. International Trade Commission

-2

0

2

4

6

8

10

12

Resin Products Machinery Molds

Trade Agreements Benefit

U.S. Exports

• Exports to FTA partners are up 57% since 2009.

• 46% of U.S. goods exports go to our trade agreement partners.

• U.S. export growth to our FTA partners (57%) has grown more rapidly than exports to the rest of the world (44%).

• In 2013, 21 of 50 states had record-high exports to these partners.

• As a share of goods export value, exports from SMEs exceed the overall worldwide average of 33% in many FTA markets, including new partners South Korea, Colombia, and Panama.

• The U.S. has a $15.2 billion trade surplus in non-oil products with our FTA partners, nearly 70% higher than the 2009 value nearly 70% higher than the 2009 value.

• In 2014, the U.S. plastics industry had more than a $20.9 billion surplus with our twenty FTA partners.

Source: U.S. Department of Commerce

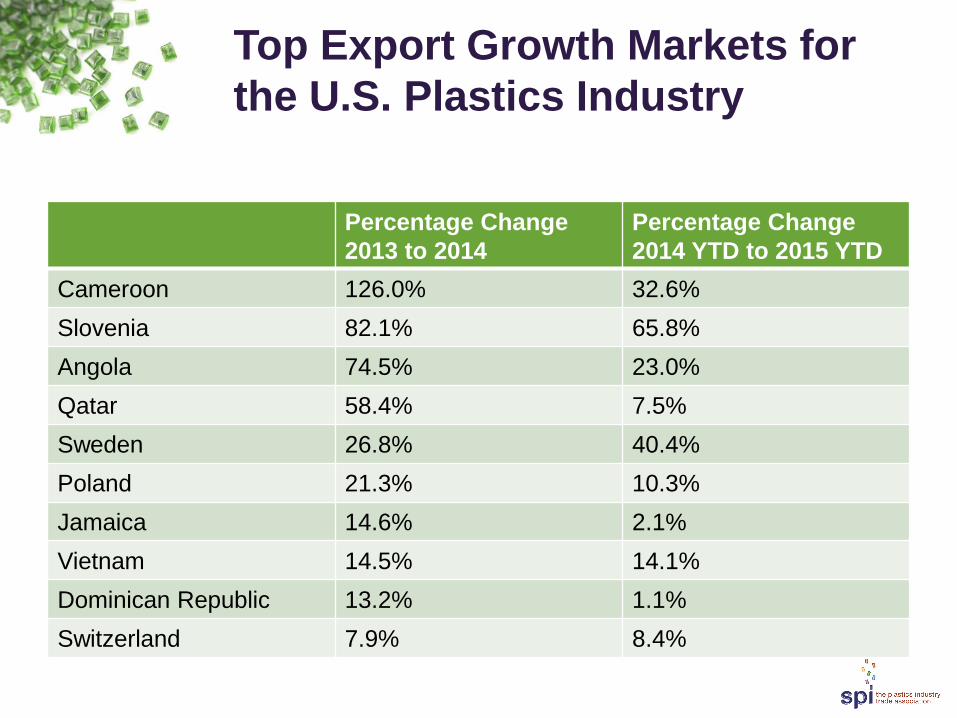

Top Export Growth Markets for

the U.S. Plastics Industry

Percentage Change

2013 to 2014

Percentage Change

2014 YTD to 2015 YTD

Cameroon 126.0% 32.6%

Slovenia 82.1% 65.8%

Angola 74.5% 23.0%

Qatar 58.4% 7.5%

Sweden 26.8% 40.4%

Poland 21.3% 10.3%

Jamaica 14.6% 2.1%

Vietnam 14.5% 14.1%

Dominican Republic 13.2% 1.1%

Switzerland 7.9% 8.4%

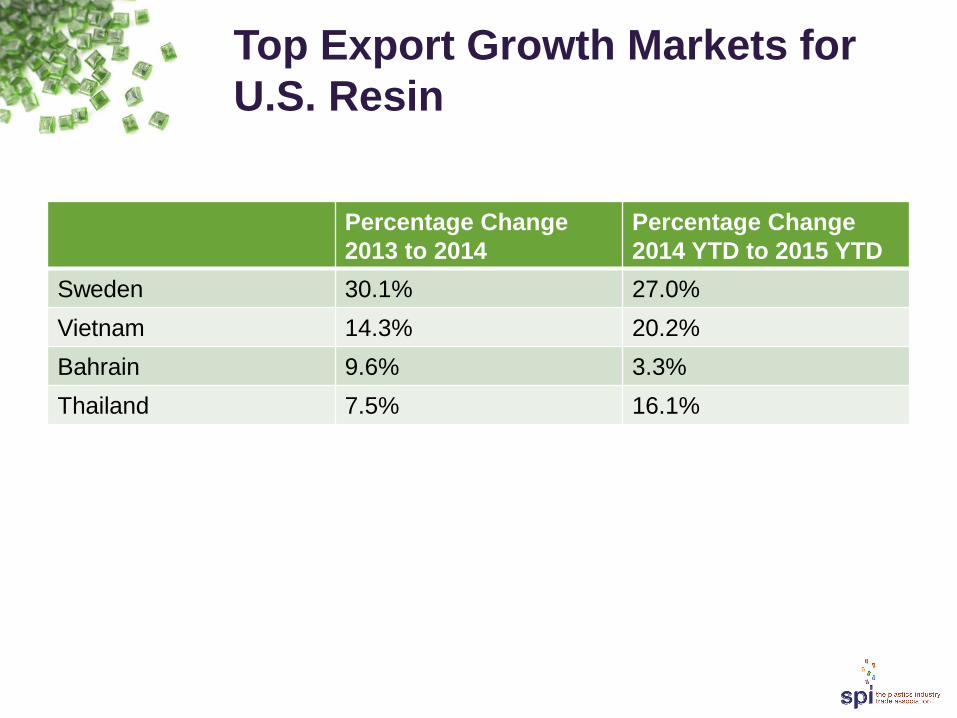

Top Export Growth Markets for

U.S. Resin

Percentage Change

2013 to 2014

Percentage Change

2014 YTD to 2015 YTD

Sweden 30.1% 27.0%

Vietnam 14.3% 20.2%

Bahrain 9.6% 3.3%

Thailand 7.5% 16.1%

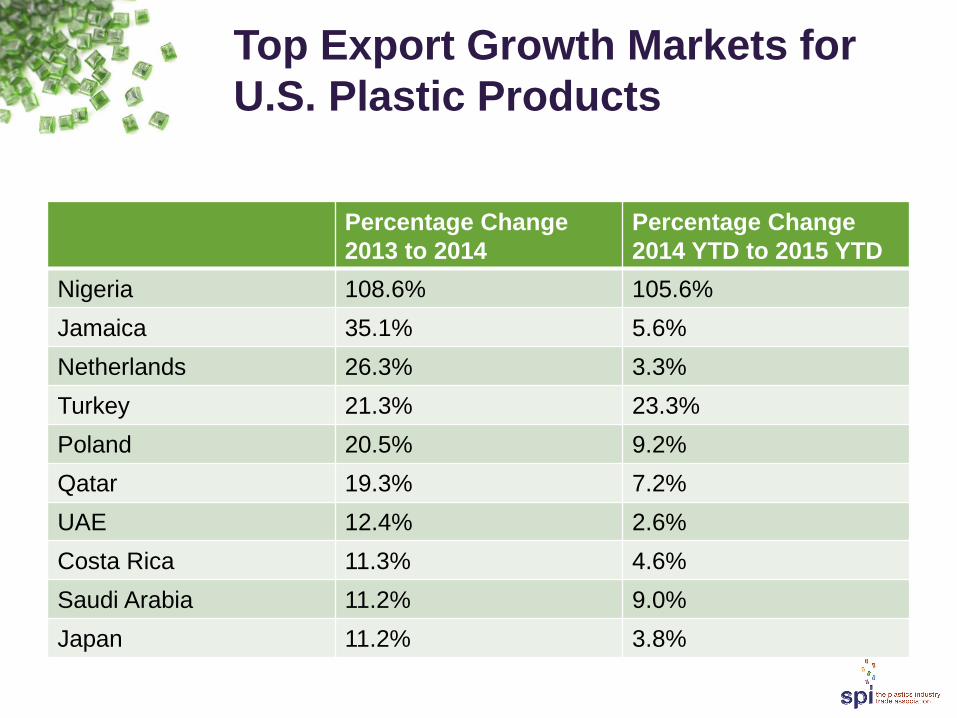

Top Export Growth Markets for

U.S. Plastic Products

Percentage Change

2013 to 2014

Percentage Change

2014 YTD to 2015 YTD

Nigeria 108.6% 105.6%

Jamaica 35.1% 5.6%

Netherlands 26.3% 3.3%

Turkey 21.3% 23.3%

Poland 20.5% 9.2%

Qatar 19.3% 7.2%

UAE 12.4% 2.6%

Costa Rica 11.3% 4.6%

Saudi Arabia 11.2% 9.0%

Japan 11.2% 3.8%

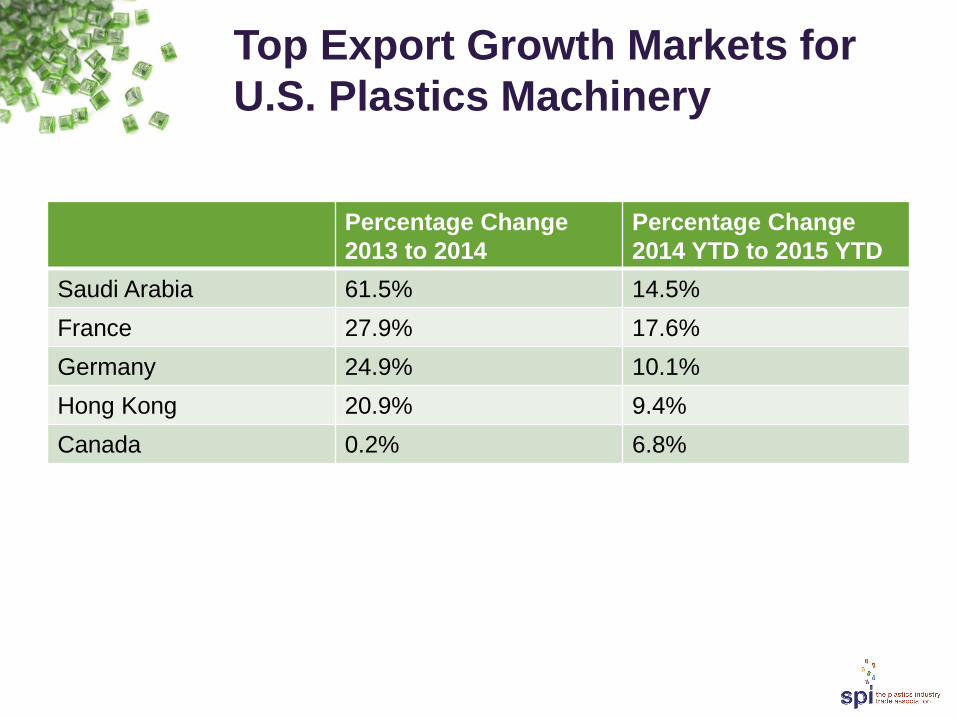

Top Export Growth Markets for

U.S. Plastics Machinery

Percentage Change

2013 to 2014

Percentage Change

2014 YTD to 2015 YTD

Saudi Arabia 61.5% 14.5%

France 27.9% 17.6%

Germany 24.9% 10.1%

Hong Kong 20.9% 9.4%

Canada 0.2% 6.8%

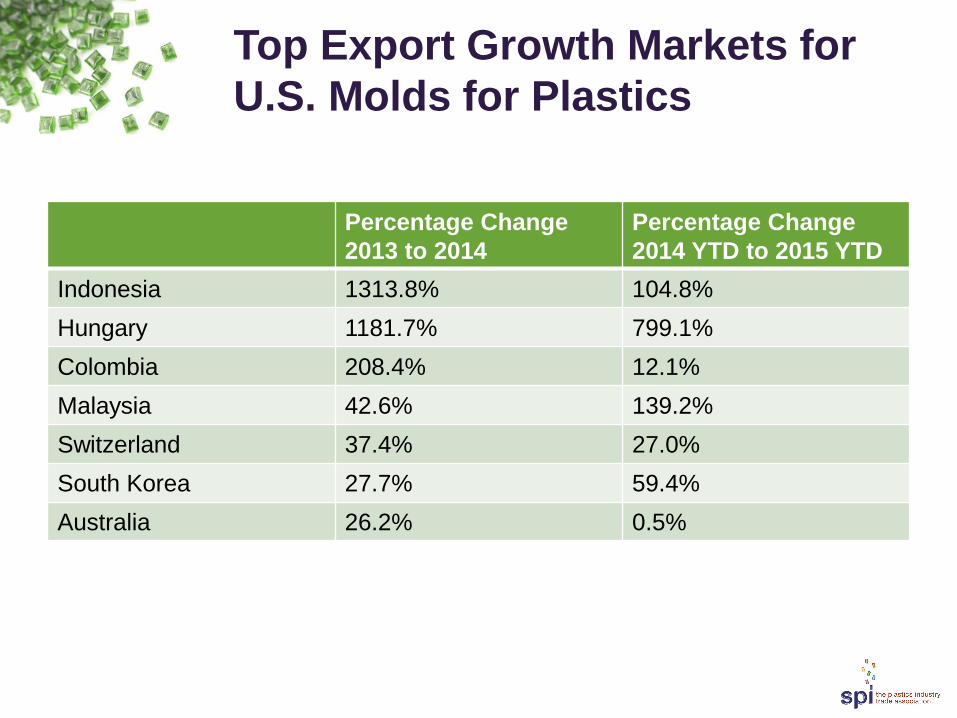

Top Export Growth Markets for

U.S. Molds for Plastics

Percentage Change

2013 to 2014

Percentage Change

2014 YTD to 2015 YTD

Indonesia 1313.8% 104.8%

Hungary 1181.7% 799.1%

Colombia 208.4% 12.1%

Malaysia 42.6% 139.2%

Switzerland 37.4% 27.0%

South Korea 27.7% 59.4%

Australia 26.2% 0.5%

SPI has launched a new series of reports looking at the

impact of the consumer on the business of plastics,

including demographics, economics, policy developments

and technological improvements for markets including:

Automotive & Transportation

Healthcare & Medical Devices

Packaging

Housing & Construction

This first publication under the SPI Market Watch series

explores the current state of plastics' role in the automotive

and transportation sector and looks into what the future

holds for the material.

Issue 1:

Automotive and

Transportation

Now Available for

Free!

Key Drivers for End Markets

Economic Indicators

Demographics

Technology

Policy

Consumer Trends

Resources

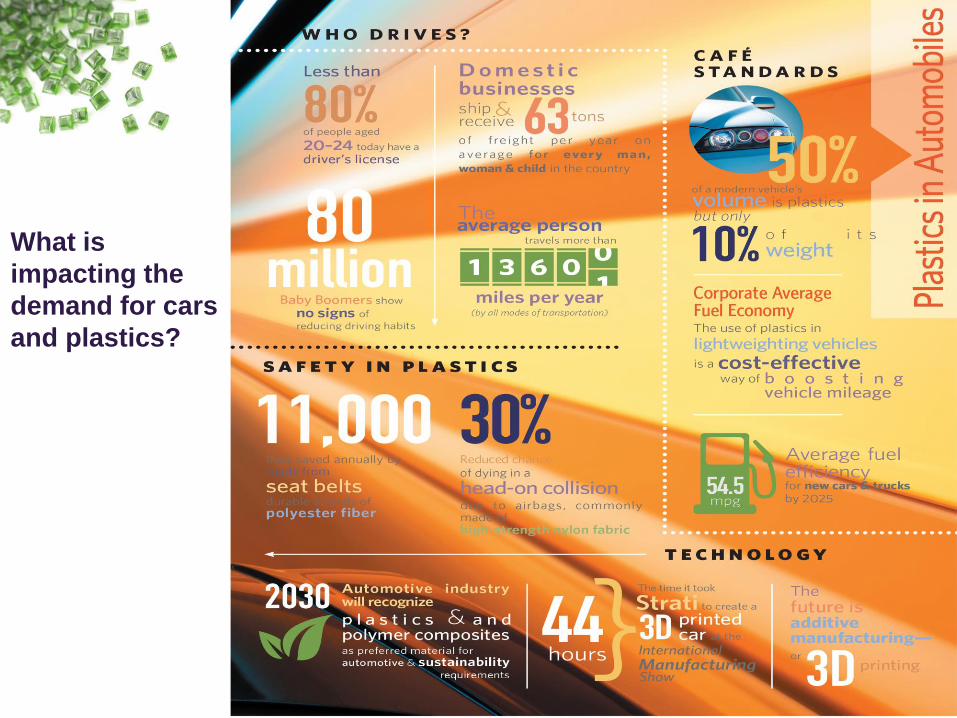

Market

What is

impacting the

demand for cars

and plastics?

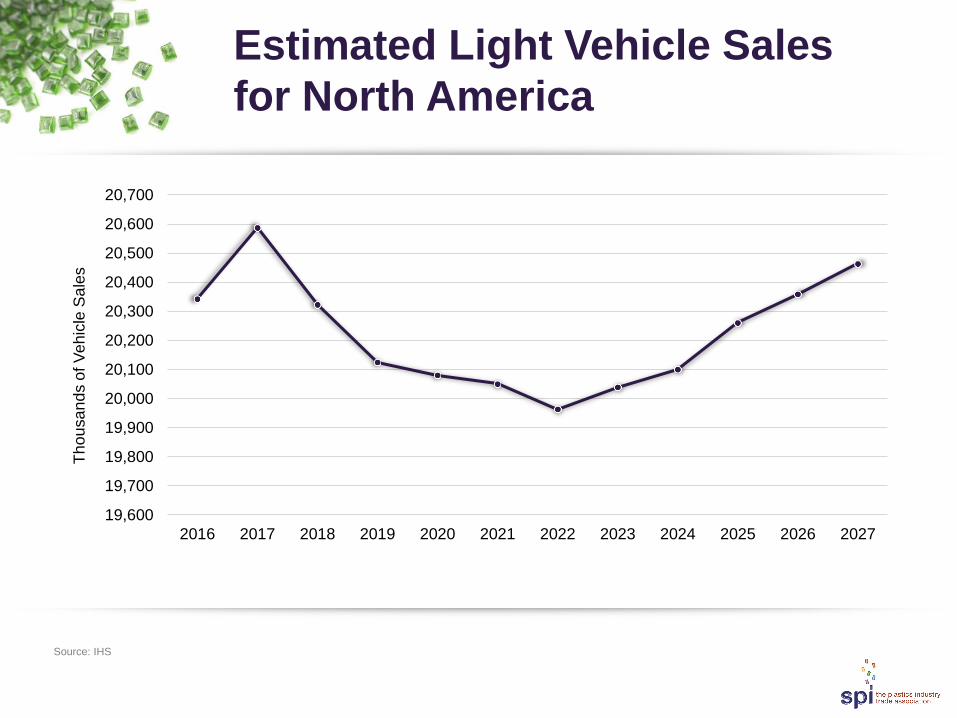

Estimated Light Vehicle Sales

for North America

19,600

19,700

19,800

19,900

20,000

20,100

20,200

20,300

20,400

20,500

20,600

20,700

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Th

ou

sa

nd

s o

f V

eh

icle

Sa

les

Source: IHS

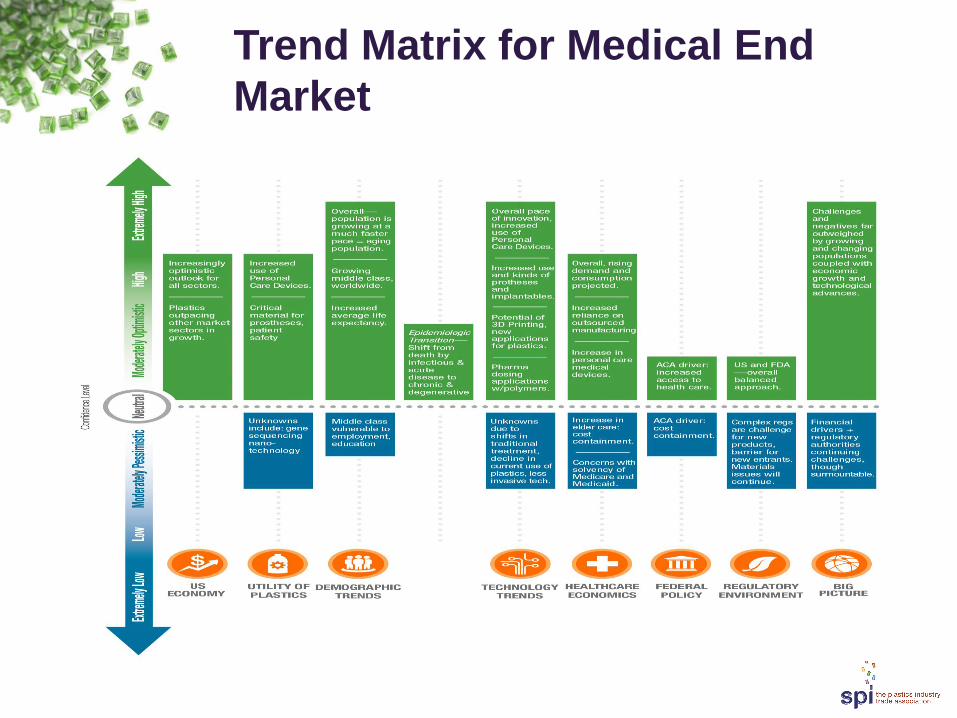

Trend Matrix for Medical End

Market

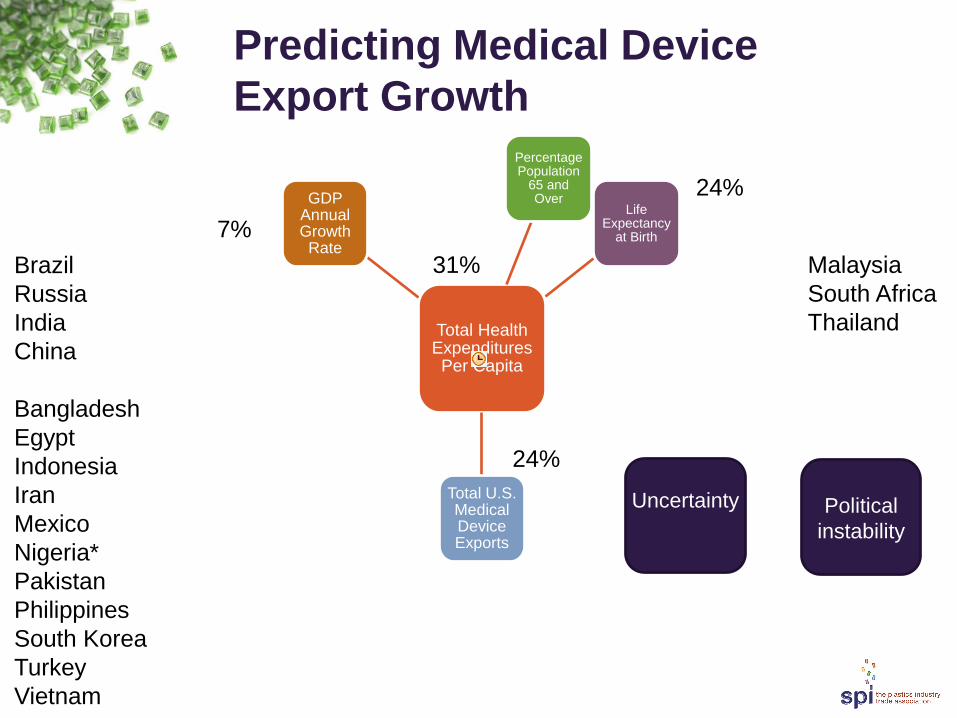

24%

31%

7%

24%

Total Health Expenditures Per Capita

Percentage Population

65 and Over

Life Expectancy

at Birth

Total U.S. Medical Device Exports

GDP Annual Growth Rate

Malaysia

South Africa

Thailand

Brazil

Russia

India

China

Bangladesh

Egypt

Indonesia

Iran

Mexico

Nigeria*

Pakistan

Philippines

South Korea

Turkey

Vietnam

Predicting Medical Device

Export Growth

Political

instability

Uncertainty

Global Plastic Packaging Market

Expected to Rise

• The global plastic packaging market was valued at US$259.65 billion in 2013 and is expected to reach US$370.25 billion by 2020.

• In terms of volume, the plastic packaging market was 78,400.2 kilo tons in 2013.

• Asia Pacific accounted for the highest demand for plastic packaging in 2013, which was over 35% of the market share.

• This trend is expected to continue over the forecast period on account of rapid economic development in this region resulting in the growth of industries such as food & beverages, personal care products and pharmaceuticals among others.

• Regions in the Rest of the World are expected to witness significant increase in consumption of packaging due to economic development in countries such as Brazil.

25

Key Factors Driving the Growth

of Plastic Packaging

• Increasing demand for plastic packaging in the healthcare industry is

expected to be one of the key factors driving the growth of this

market.

• In addition, expansion of the food & beverages market, which is the

largest application of plastic packaging, is expected to fuel growth.

• Furthermore, rising consumer preference towards light weight,

durable and highly aesthetic packaging is expected to significantly

encourage growth of the market over the next few years.

• Demand for plastic packaging was highest from the food &

beverages sector and accounted for over 65% of the market share

in 2013.

26

Thank You!

谢谢 Merci Vielen Dank

Grazie ありがとうございました 감사합니다

Obrigado Спасибо Gracias Teşekkürler

Questions & Answers

Michael Taylor

202-974-5232

![Uflex conferred with the Export Award for Metalized Polyester Film by 'The Plastics Export Promotion Council' [Company Update]](https://img.pdfslide.us/doc/110x75/577cb1411a28aba7118b9639/uflex-conferred-with-the-export-award-for-metalized-polyester-film-by-the.jpg)