Embed Size (px)

Citation preview

YEAR January 2013

COPYRIGHT

DISCLAIMER

CONTACTS

YES BANK Ltd.

Registered and Head Office

th9 Floor, Nehru Centre,Dr. Annie Besant Road,Worli, Mumbai - 400 018

Tel : +91 22 6669 9000Fax : +91 22 2497 4088

Northern Regional Office

48, Nyaya Marg, ChanakyapuriNew Delhi – 110 021

Tel : +91 11 6656 9000Email : [email protected] : www.yesbank.in

TERI-Business Council for Sustainable Development (BCSD)

The Energy and Resources Institute (TERI)Core 6C, Darbari Seth Block, Habitat PlaceIndia Habitat Center, Lodhi RoadNew Delhi - 110 003

Tel : (+91 11) 2468 2100, 41504900Fax : (+91 11) 2468 2144, 2468 2145Email : [email protected] : www.teriin.org/bcsd

TITLE Electric Vehicles: Challenges & Opportunities in India

AUTHORS

Lead authors : Samir Karnik, Nitin Sukh (Responsible Banking Team, YES BANK)

Contributors : Agneev Mukherjee, Sarobjit Pal, Akshima Tejas Ghate,

Sangeetha Ann Wilson (TERI BCSD)

No part of this publication may be reproduced in any form by photo, photoprint,

microfilm or any other means without the written permission of YES BANK Ltd. and TERI

BCSD.

This report is the publication of YES BANK Limited (“YES BANK”) & TERI BCSD and so YES BANK & TERI BCSD have editorial control over the content, including opinions, advice, statements, services, offers etc. that is represented in this report. However, YES BANK & TERI BCSD will not be liable for any loss or damage caused by the reader's reliance on information obtained through this report. This report may contain third party contents and third-party resources. YES BANK & TERI BCSD takes no responsibility for third party content, advertisements or third party applications that are printed on or through this report, nor does it take any responsibility for the goods or services provided by its advertisers or for any error, omission, deletion, defect, theft or destruction or unauthorized access to, or alteration of, any user communication. Further, YES BANK & TERI BCSD does not assume any responsibility or liability for any loss or damage, including personal injury or death, resulting from use of this report or from any content for communications or materials available on this report. The contents are provided for your reference only.

The reader/ buyer understands that except for the information, products and services clearly identified as being supplied by YES BANK & TERI BCSD, it does not operate, control or endorse any information, products, or services appearing in the report in any way. All other information, products and services offered through the report are offered by third parties, which are not affiliated in any manner to YES BANK & TERI BCSD.

The reader/ buyer hereby disclaims and waives any right and/ or claim, they may have against YES BANK & TERI BCSD with respect to third party products and services.

All materials provided in the report is provided on “As is” basis and YES BANK & TERI BCSD makes no representation or warranty, express or implied, including, but not limited to, warranties of merchantability, fitness for a particular purpose, title or non – infringement. As to documents, content, graphics published in the report, YES BANK & TERI BCSD makes no representation or warranty that the contents of such documents, articles are free from error or suitable for any purpose; nor that the implementation of such contents will not infringe any third party patents, copyrights, trademarks or other rights.

In no event shall YES BANK & TERI BCSD or its content providers be liable for any damages whatsoever, whether direct, indirect, special, consequential and/or incidental, including without limitation, damages arising from loss of data or information, loss of profits, business interruption, or arising from the access and/or use or inability to access and/or use content and/or any service available in this report, even if YES BANK & TERI BCSD is advised of the possibility of such loss.

The traditional approach of the banking sector to sustainability is often regarded as lacking in proactive

initiatives. However, several banks have recently adopted innovative and forward looking strategies to deal

with opportunities associated with sustainability. They have developed new products such as ethical funds

or loans specifically designed for environmental businesses to capture new market opportunities associated

with sustainability. This very joint endeavor between TERI BCSD and YES BANK to explore Electric Vehicles

as an option of sustainable mobility that has the capability to significantly lower emission levels including

carbon dioxide emissions which is an encouraging beginning.

Rapid urbanization, rising per capita incomes, growing aspirations of an expanding population and sprawling

cities have resulted in transport demand increasing at a rate much faster than the rate of growth of transport

infrastructure. Indian cities are witnessing an exponential increase in the use of personal transport and a

steady decline in the modal share of both public transport and non-motorized transport. There is a growing

realization, both internationally and nationally, that the current trends in urban transport are unsustainable

and should be arrested. Urban transport should move along a low carbon and sustainable pathway. Several

international initiatives like the SLOCAT (The Partnership on Sustainable, Low Carbon Transport), and major

events like the United Nations Conference on Sustainable Development, 2012 (Rio+20), etc. have

highlighted the challenges associated with meeting urban mobility demand in a sustainable manner. In India,

the National Urban Transport Policy, 2006 aims to move future transport development in Indian cities

towards a sustainable and low carbon trajectory. Current policy promotes investments in public transport

and non-motorized transport infrastructure so as to advance the agenda of sustainable mobility. While it

becomes important to plan for systems of public transport, and non-motorized transport for promoting

sustainable mobility, it is also critical to ensure that personal modes of transport i.e. cars and two wheelers

embody energy efficiency and low-carbon intensity. This is important because we are going to witness an

explosive increase in the number of personal vehicles in our country. It is therefore crucial that the new

vehicular fleet in the country produces low environmental impacts.

Electric vehicles, though not yet popular in India, are an important solution to addressing the issue of

vehicular pollution. The country has recently witnessed the unveiling of the National Electric Mobility

Mission Plan 2020 by the Hon'ble Prime Minister, Dr Manmohan Singh. This move is significant at this

juncture considering the country cannot continue its heavy dependence on personal modes, which run on

petroleum products (petrol and diesel) with implications for India's energy security and CO2 emissions. It is

important that we diversify our fuel mix in favour of clean fuels. Electrification of vehicles certainly offers

such potential provided the electricity is generated from clean sources of energy. Going forward, it is very

important that any plan for electric vehicles is implemented in an integrated manner in consonance with our

plans for electricity generation and distribution and urban infrastructure planning. Major R&D initiatives are

needed to ensure that the penetration of electric vehicles is accelerated. All key stakeholders including

industry, government, and financial institutions will have to work together in this endeavour.

I compliment YES BANK for undertaking this study and for publication of this Knowledge Paper.

MESSAGE

Dr R K Pachauri

Director-General, TERI

This well-researched knowledge paper advocates the incremental transition of private

transportation in India - from being driven by the internal combustion engine to electric drive

trains.

YES BANK and TERI BCSD are of the strong view that this revolution in Indian personal

transportation will open up significant business avenues, and corresponding financing

opportunities. It will also address the critical issues of India's long term energy security and

reduce the environmental impact of fossil fuel driven vehicles, though only at the tailpipe.

However, there are some ground realities in India and globally that will remain long term

challenges for the widespread uptake in electric vehicles (EV). The technology which makes

complete electric mobility possible and financially viable, from an Original Equipment

Manufacturers (OEMs) perspective, already exists in the Indian scenario. Technology

improvements in battery capacity, fast charging facilities and vehicle range are rapid and dynamic,

with many OEMS and other companies in the EV value chain already investing significant amounts

in research and development (R&D), and scaling manufacturing capacities. EVs have arrived

globally and most certainly in India with companies like Mahindra REVA championing the EV four

wheeler (4W) space and Hero Group dominating the EV two wheeler (2W) segment.

The rising price of crude in the international market has become an energy security concern for

the country. Are EVs the silver bullet to securing India's energy future and reducing carbon

emissions of its transportation sector? This is a difficult question to explicitly answer. While on one

hand, the mainstreaming of EVs will dramatically reduce India's reliance on imported crude oil, on

the other hand, EVs, if disruptively introduced, will be charged by India's crumbling and inefficient

electricity grid which is predominantly powered by imported coal. Therefore, whether EVs will

strengthen India's energy and climate security is a catch 22 question, in case the status quo

remains. The question then is - How do we change the status quo? For this, there is a need for a

comprehensive policy roadmap towards private vehicle electrification wherein the financial sector

and Government of India (GoI) play interdependent roles to develop critical and enabling EV

infrastructure and incentivize OEMs and organisations along the value chain, to innovate and

collectively work towards introducing EV 4W & 2W EV variants, thereby giving the consumer a

choice.

I firmly believe that the contents of this knowledge paper will provide important insights to policy

makers in achieving a smooth and incremental transition to EV's, thus ensuring India's long term

energy security.

FOREWORD

Thank You.

Sincerely,

Rana KapoorFounder, Managing Director & CEO

The findings of this paper will be of particular interest to 3 key stakeholders: The financial sector, policy

makers and the automobile industry.

The premise of this paper is that the financial sector will not fund companies that fall in a value chain

whose risks and business models are not fully understood. Therefore the key objective of the paper is

to clearly outline the EV value chain, the perceived risks along the value chain and highlight some

financial tools and business solutions that could be modified specifically for de-risking and therefore

facilitate the financing of EV growth in India.

Our key insight emanating from this report is that the Indian customer does not need to be directly

incentivized by the Government of India (GoI) and State Governments to buy EVs, as is currently the

case. The Indian consumer is price, fuel economy and style conscious and will therefore appreciate the

long term savings of EV versus Internal Combustion Engine (ICE). In which case, growth of the EV

value chain must be fuelled by organic consumer demand, and not pushed by unsustainable

Government subsidies for consumers, to drive EV purchases. This would defeat the purpose of

reducing strains on India's Balance of Payments. Organic consumer demand can only be fostered by

the Government, working in collaboration with the private sector to invest in an economically enabling

environment for rapid EV adoption, which entails the following:

Consumers will not buy EVs if

they are unable to charge them whilst in urban transit. Range anxiety inhibits the consumer's

decision making process and this is well documented by numerous reports. Therefore, the

Government must invest in 'clean & energy efficient fast charging infrastructure' that will

perceptually give urban consumers the comfort in buying EVs. Clean & Energy efficient fast

charging infrastructure will comprise of, in a phased manner, smart grids and metering, renewable

energy (RE) feeds and fast charging ports. Smart grids will not only accommodate EV charging

point applications, but will also reduce energy wastage by the grid in general. EVs will not

mainstream in India until and unless primary yet significant GoI led investments are made firstly in

smart grid adoption, followed by plug in applications like RE feeds & fast charging ports. Direct

GoI investments and public private partnership (PPP) models can be explored accordingly to hive

off the financial investment component to the private sector.

Launch a Government sponsored fund, inviting applications

from commercial banks, specifically for low interest forward lending, partial project risk

guarantees and co-equity investments.

PRUDENCE - Innovate and take incremental steps towards full automobile electrification. Competition

in the Indian EV and hybrid market will transform the Indian consumer's perception in the years to

come where foreign competitors and early bird Indian companies will grab dominant 4W EV & 2W EV

market shares.

For the Financial Sector:

For the Indian Government and Policy Makers:

• Develop 'Clean & Energy Efficient fast charging infrastructure' –

• Financially incentivise Indian Banks to fund India EV OEM manufacturers, Battery R&D, Fast

charging R&D & Smart grid projects –

For Indian Automobile companies:

Preface

C O N T E N T S1 Introduction: The Case for Sustainable Personal Transport in India 1

2 Sustainable Personal Transportation 13

3 The Electric Vehicle Value Chain 23

4 Policies Promoting Electric Vehicles in India 31

1.1 Energy Security 3

1.2 Climate Change 5

1.3 Road Transport Emissions in India 6

1.4 Trends in Personal Road Transport in India 71.5 Modal Shifts 9

2.1 Technological Innovations in Low-Carbon Transport 14

2.2 Pathway to Zero-Emission Vehicles 20

3.1 Raw Material Suppliers 24

3.2 Traditional Component Suppliers 25

3.3 Battery Manufactures & Suppliers 25

3.4 Original Equipment Manufacturers (OEMs) 26

3.5 Utilities 26

3.6 The Electric Vehicle Ecosystem 27

4.1 Initiatives by the Ministry of New and Renewable Energy 32

4.2 Initiatives in the 2011-2012 Budget 33

4.3 Initiatives by the Ministry of Heavy Industries 33and Public Enterprises

4.4 Government Agencies to take up EV Mobility in India 34

C O N T E N T S5 Development of EV Charging Infrastructure in India 37

6 Emerging Business Models 45

7 Analysis and Thought 51

5.1 EV Charging Infrastructure: Past Efforts 38

5.2 Comparison with Compressed Natural Gas (CNG) 39

Infrastructure

5.3 India's Power Sector 39

5.4 Smart Grids 41

5.5 Requirements for Smart Grid Deployment 43

6.1 Direct Vehicle Sales 46

6.2 EV Leasing 47

6.3 Battery Leasing and Swap Schemes 47

6.4 Infrastructure Service Models 48

7.1 Short Term Horizon 52

7.2 Long Term Horizon 52

7.3 Concluding Thoughts 54

Introduction: The Case for

Sustainable Personal Transport in India

“The mobility model we have today will not work tomorrow”

- Bill Ford, great-grandson of Henry Ford and Executive Chairman of the Ford Motor Company

India's population is expected to surpass that of China's in 2030, making it the most

populous county in the world. High economic growth rates and the impacts of

globalization have concentrated prosperity in urban centers resulting in sprawl and

auto-mobilization. Within 15 years the population residing in urban areas is expected

to double to over 700 million [1] due to distressed rural to urban migration and other

factors. This will place additional pressures on urban infrastructure, which is already

overburdened. Projections indicate that by 2021 India will have the largest

concentration of megacities in the world with a population exceeding 10 million. Out

of a total of 88 cities, with a population of more than half a million in 2011, only 28

have any formal public transportation system. In most cases, the existing public

transport systems are ageing and stretched beyond capacity, as the demand for public

transport services outstrips supply, both qualitatively and quantitatively.

As disposable income increases, a result of economic growth, those entering the

middle-class are able to afford and prefer personal vehicles, as it is a symbol of

upward social mobility, and also provides greater comfort, flexibility and convenience.

In the absence of proper planning measures, the dynamics between increasing

numbers of vehicles as well as a growing population wanting to use private vehicles

for transport are likely to pressurize transport infrastructure, leading to inefficiencies as

a result of infrastructural bottlenecks such as traffic congestion, gridlocks and slower

train speeds. This would result in higher traffic management costs and greater energy

consumption, therefore significantly increasing carbon emissions from transportation.

The growth in motor vehicles is much faster than the population and faster than the

GDP with 5% annual growth in motorcycles/scooter and 14% annual growth in cars

[2].

Introduction: The Case for Sustainable Personal Transport in India

Electric Vehicles in India: Challenges and Opportunities2

If current ICE uptake trends continue, developing countries like India are faced with unsustainable

futures that are likely to have negative triple bottom line impacts. Considering the stage of

economic development in India, the country has a unique opportunity to develop sustainably by

managing emissions growth, enhancing energy security and by supporting the creation of a world

class clean-technology industry. The time is ripe to explore a range of potentially promising

solutions to redirect the economy towards a path which is sustainable and secure.

Beginning with economic liberalization in 1991, the consistent growth and globalization of the

Indian economy thereafter, energy consumption in India has grown exponentially. Increasing

urbanization, infrastructural development and concentration of economic activities in certain load

centers have resulted in higher mobility fuelled by a rapid increase in number of vehicles and

distances travelled. The growing demand for energy is being addressed largely though oil imports, thwhere India is currently the 5 largest oil importer in the world. India simply does not possess

adequate oil reserves to meet current and future demand. 72% of the oil consumed in India in

2007 was imported and this is projected to rise sharply to over 90% by 2030 [3]. High oil prices

result in negative feedback loops that weaken stock prices and tighten fiscal conditions, thereby

depressing economic growth in the long term.

The growth of the Indian economy is impacted by the price of oil imports, which tends to be

extremely volatile and sensitive to economic and political shifts. As a result of the global

recession, oil prices rose to a record peak of INR 7,830 per barrel (USD 145) in July 2008 (Exhibit

1) and the Brent Crude oil price hit INR 5,400 (USD 100) on 31st January, 2011 due to

the political upheaval in Egypt [4]. The growth in demand for oil from BRICS (Brazil, Russia, India,

China & South Africa) nations and other emerging economies coupled with a decrease in the

discovery of new exploitable oil fields will push up oil prices up over the next few decades. This

would further exacerbate the budget deficit, dampening economic growth.

1.1 Energy Security

per barrel

Electric Vehicles in India: Challenges and Opportunities 3

Exhibit 1: Oil price fluctuations (USD), 1987 – 2011 [19]

Source: IEA (International Energy Agency), (2009), Key World Statistics

May

1987

Jan

198

8

Jan

198

9

Jan

199

0

Jan

199

1

Jan

199

2

Jan

199

3

Jan

199

4

Jan

199

5

Jan

199

6

Jan

199

7

Jan

199

8

Jan

199

9

Jan

20

00

Jan 2

001

Jan

20

02

Jan

20

03

Jan 2

004

Jan 2

005

Jan 2

006

Jan 2

007

Jan 2

008

Jan 2

009

Jan

201

0

Jan 2

011

0

20

40

60

80

100

120

140Nominal Real (April 2011 US dollars)

May 1987-April 2011 monthly average Brent spot prices

Conversion to April 2011 dollars uses US CPI for AII Urban Consumers (CPI-U)

Electric Vehicles in India: Challenges and Opportunities4

The transport sector is a key consumer of oil and oil products. More than 50% of the oil

consumption in India occurs on account of transport-related activities [85]. The World Energy

Outlook has estimated that most of the increase in oil consumption by 2030 in India will be driven

by light-duty vehicles, mainly passenger cars – growing at an annual rate of approximately 10%

(Exhibit 2) [5].

Exhibit 2: Energy usage worldwide, industry break up and light duty vehicle depictions [19]

Source: IEA (International Energy Agency), (2009), Key World Statistics

A significant question to ask at this juncture is whether the world can continue generating a

sufficient supply of oil in the coming decades to accommodate the rise in demand from emerging

economies like India and China, without hampering environmental quality?

Until recently Governments and businesses have ignored the phenomenon of 'peak oil'. Peak oil

refers to the 'point at which the maximum rate of global oil extraction is reached'. However, there

has been growing acceptance of peak oil in the public domain, where both Governments and

businesses have been exploring alternative sources of energy supply, primarily renewable sources

like solar, wind, hydro, geo-thermal and nuclear energy. The oil industry is beginning to realize that

we have crossed “the era of easy oil, (and) in the future oil will be dirtier, deeper and far more

challenging (to extract)”[5]. Technologies that have the potential to phase-out oil dependent forms

of transportation should be actively pursued to gauge their feasibility.

PROJECTED INCREMENTAL OIL

DEMAND BY SECTOR, 2006-30 (MTI)

TOTAL STOCK OF LIGHT-DUTY

VEHICLES BY REGION (bn)

-200

0

200

400

600 Africa

Latin AmericaMiddle EastIndia

2.0

2.5

x3

Rest of world Other Asia India

China OECD

OtherNon-energy USE

IndustryTransport

Other Asia1.5 x2

ChinaEastern EuropeEECCAOECD Pacific

OECD Europe

OECD N. America

205020402030202020102000

0.5

0

1.0

1880 1900 1920 1940 1960 20001980-0.6

-0.4

-0.2

0.2

0

0.4

0.6

Global Temperature Anomalies

Year

Electric Vehicles in India: Challenges and Opportunities 5

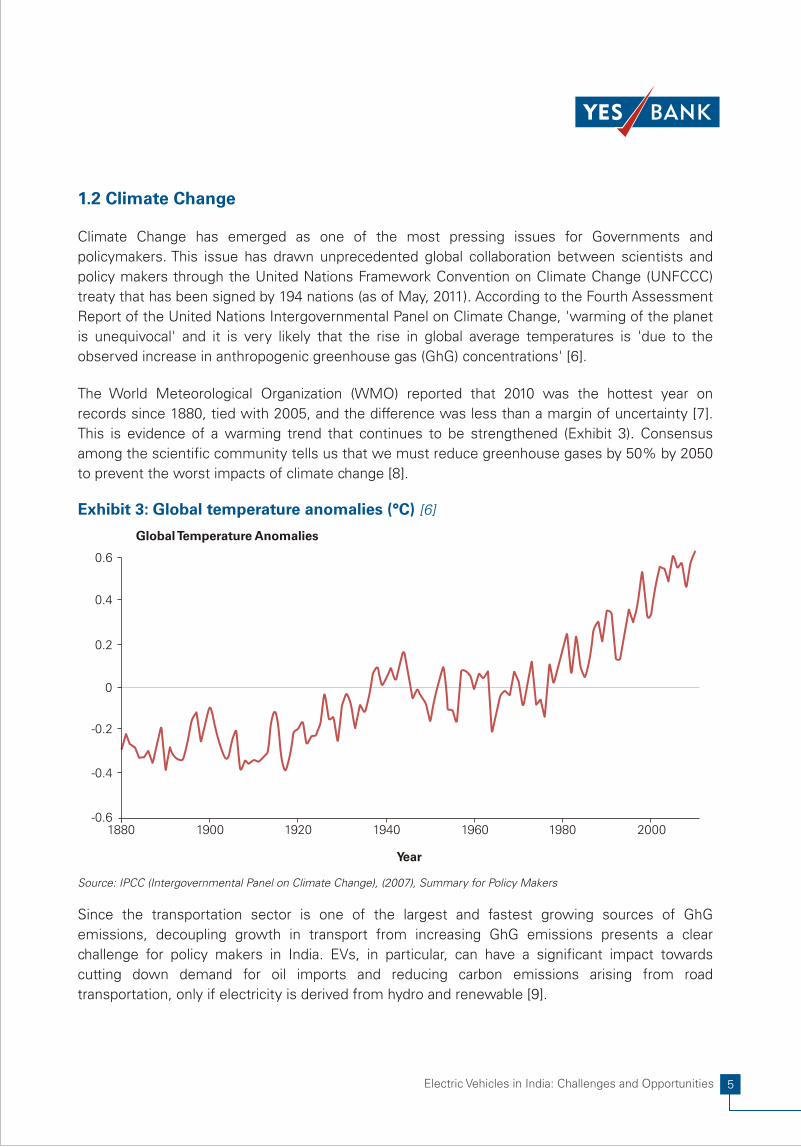

1.2 Climate Change

Climate Change has emerged as one of the most pressing issues for Governments and

policymakers. This issue has drawn unprecedented global collaboration between scientists and

policy makers through the United Nations Framework Convention on Climate Change (UNFCCC)

treaty that has been signed by 194 nations (as of May, 2011). According to the Fourth Assessment

Report of the United Nations Intergovernmental Panel on Climate Change, 'warming of the planet

is unequivocal' and it is very likely that the rise in global average temperatures is 'due to the

observed increase in anthropogenic greenhouse gas (GhG) concentrations' [6].

The World Meteorological Organization (WMO) reported that 2010 was the hottest year on

records since 1880, tied with 2005, and the difference was less than a margin of uncertainty [7].

This is evidence of a warming trend that continues to be strengthened (Exhibit 3). Consensus

among the scientific community tells us that we must reduce greenhouse gases by 50% by 2050

to prevent the worst impacts of climate change [8].

Since the transportation sector is one of the largest and fastest growing sources of GhG

emissions, decoupling growth in transport from increasing GhG emissions presents a clear

challenge for policy makers in India. EVs, in particular, can have a significant impact towards

cutting down demand for oil imports and reducing carbon emissions arising from road

transportation, only if electricity is derived from hydro and renewable [9].

Exhibit 3: Global temperature anomalies [6](°C)

Source: IPCC (Intergovernmental Panel on Climate Change), (2007), Summary for Policy Makers

Electric Vehicles in India: Challenges and Opportunities6

1.3 Road Transport Emissions in India

India is the fourth largest GhG emitter in the world. The transport sector is the fourth largest

contributor of greenhouse gases in India with a share of 7.5% of the emissions in the country

preceded by electricity generation (37.8%), agriculture (17.6%) and industry (8.7%) [11].

India has witnessed a 200-fold increase in vehicle numbers between 1951 and 2011. Road

transport is the largest contributor of GhG emissions and was responsible for 87% (123.5 Mt

CO e) of the total emissions arising from the transport sector in 2007. Currently passenger 2

vehicles that include two wheelers and four wheelers are responsible for about 30% to 35% of

the total road transport emissions (Exhibit 4).

Over the next decade, the number of passenger vehicles on the road is expected to rise sharply,

approximately 14% y-o-y. According to the IEA/SMP transportation model reference case (using

2003-04 as the base year), emissions from passenger cars are likely to grow at 5% per annum in

India [13]. Even if engine efficiencies improve, the sheer growth in the number of vehicles on the

road would lead to an absolute increase in GhG emissions from road transport.

Exhibit 4: Road Transport: CO e emissions by Fuel type – 2007 [12]2

Source: Transport Sector: Greenhouse Gas Emissions 2007, Central Road Research Institute, New Delhi, INCCA

2% 15%

28%

55%

Buses/Cars/Taxi/3W (CNG+LPG)

2W/3W (Petrol)

Cars/Taxi/Jeep (Petrol+Diesel)

Commercial Vehicles: Trucks/Buses/LCV (Diesel)

Electric Vehicles in India: Challenges and Opportunities 7

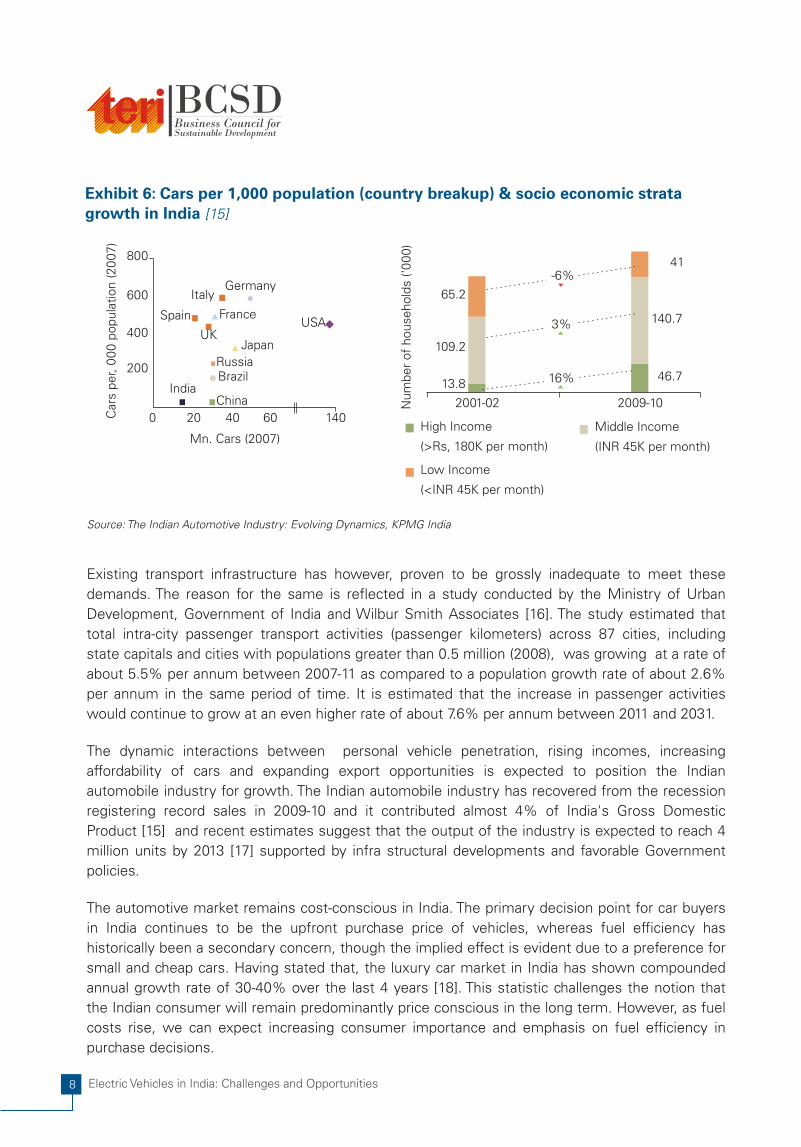

1.4 Trends in Personal Road Transport in India

The Indian road network is the second largest in the world, covering 3.34 million kilometers where

as much as 80% of passenger traffic is carried by the roads [14].

The high growth rates of the Indian economy have resulted in an unprecedented rise in disposable

incomes and this has contributed towards a burgeoning automotive industry. With the Indian

economy projected to grow at an average of 8-9% per annum over the middle term, the

percentage of Indian consumers that are able to afford vehicles is likely to increase. Yet, India's car

per capita ratio (i.e. number of cars per 1000 persons) is the lowest among the world's five largest

automobile markets (Exhibit 6), pegged at 18 cars per 1000 people. The share of public transport

has been declining slowly as a result of the growth in private vehicle ownership, fuelled by

expanding urbanization and affluence.

Exhibit 5: Expected growth in CO emissions in India from different transport 2

modes [13]

Source: Mobility at What Cost?,InfoChange Agenda

2005 0

201

2015

2020 5

202

2030

2035

2040

2045

2050

2000

0

100

200

300

400

500

600

700

800

Water

Frieght rail

Freight trucks

Air

Pass rail

Buses

3-wheelers

2-wheelers

Pass cars

Meg

ato

nn

es

C O

2

Electric Vehicles in India: Challenges and Opportunities8

Existing transport infrastructure has however, proven to be grossly inadequate to meet these

demands. The reason for the same is reflected in a study conducted by the Ministry of Urban

Development, Government of India and Wilbur Smith Associates [16]. The study estimated that

total intra-city passenger transport activities (passenger kilometers) across 87 cities, including

state capitals and cities with populations greater than 0.5 million (2008), was growing at a rate of

about 5.5% per annum between 2007-11 as compared to a population growth rate of about 2.6%

per annum in the same period of time. It is estimated that the increase in passenger activities

would continue to grow at an even higher rate of about 7.6% per annum between 2011 and 2031.

The dynamic interactions between personal vehicle penetration, rising incomes, increasing

affordability of cars and expanding export opportunities is expected to position the Indian

automobile industry for growth. The Indian automobile industry has recovered from the recession

registering record sales in 2009-10 and it contributed almost 4% of India's Gross Domestic

Product [15] and recent estimates suggest that the output of the industry is expected to reach 4

million units by 2013 [17] supported by infra structural developments and favorable Government

policies.

The automotive market remains cost-conscious in India. The primary decision point for car buyers

in India continues to be the upfront purchase price of vehicles, whereas fuel efficiency has

historically been a secondary concern, though the implied effect is evident due to a preference for

small and cheap cars. Having stated that, the luxury car market in India has shown compounded

annual growth rate of 30-40% over the last 4 years [18]. This statistic challenges the notion that

the Indian consumer will remain predominantly price conscious in the long term. However, as fuel

costs rise, we can expect increasing consumer importance and emphasis on fuel efficiency in

purchase decisions.

Exhibit 6: Cars per 1,000 population (country breakup) & socio economic strata growth in India [15]

Source: The Indian Automotive Industry: Evolving Dynamics, KPMG India

ItalyGermany

USAFranceSpain

UKJapan

RussiaBrazil

IndiaChina

0 20 40 60 140

200

400

600

800

Mn. Cars (2007)

Cars

per, 0

00 p

opula

tion (20

07)

Num

ber

of

household

s ('0

00)

65.2

13.8

109.2

-6%

3%

16%

41

140.7

46.7

2009-102001-02

High Income

(>Rs, 180K per month)

Low Income

(<INR 45K per month)

Middle Income

(INR 45K per month)

Electric Vehicles in India: Challenges and Opportunities 9

1.5 Modal Shifts

The rapid growth of demand for passenger mobility in Indian cities has not been matched by an

equal increase in supply of transport infrastructure and services. This has resulted in the increased

use of private vehicles across most urban centres accompanied by declining share of public

transport systems. In addition, with expanding cities, the share of pedestrians, cyclists and non-

motorized transport users has also fallen, as seen in Exhibit 7, 8 and 9.

Exhibit 7: Growth in passenger vehicles in India (mn) from 1981 to 2009

Exhibit 8: Change in public transport shares between 1994 to 2007 [16]

Exhibit 9: Changing shares of walk trips between 1994 and 2007 [16]

In India, the transportation sector is responsible for nearly 20% of the total energy consumption

and is the second largest consumer of energy in the country after industry [19]. A significant

amount of road based passenger transport activities in the country are concentrated in cities. The

on-road passenger transport activities in urban India are responsible for nearly 40% of the total

energy consumption in road passenger transport sector [20].

Source: MoRTH Yearbooks

0

10

20

30

40

50

60

70

80

90

Growth of registered motor vehicles in India

Two-wheelersCars, jeeps, taxisBuses

1981 1991 2001 2009

0

10

20

30

40

50

60

70

80

<0.5 0.5 to 1 1 to 2 2 to 4 4 to 8 > 8

City population size (in million)

Share of public transport in India

1994 2007

PT

sh

are

(%

)

0

20

40

60

<.5 .5-1 1-2 2-4 4-8 Above 8

1994 2007

City population size (in mn)

% S

ha

re o

f w

alk

trip

s

Source: WSA (Wilbur Smith Associates) & MoUD (Ministry of Urban Development), (2008), Study on Traffic & Transportation Policies and Strategies in Urban Areas in India, as cited in TERI, (2012)

Source: WSA (Wilbur Smith Associates) & MoUD (Ministry of Urban Development), (2008), Study on Traffic & Transportation Policies and Strategies in Urban Areas in India, as cited in TERI, (2012)

Electric Vehicles in India: Challenges and Opportunities10

The current trends in urban transport, which are primarily a result of the inability of Indian cities to

meet the increasing transport demand in a planned manner, have resulted in local problems

related to congestion, deterioration of air quality, increase in number of road fatalities and

accidents and loss in economic productivity. The congestion levels in many Indian cities have

reached unmanageable proportions, the average vehicle speeds dropping down to as low as 10

km/hour in many cities. This leads to higher fuel consumption due to low speeds and vehicle

idling [21].

Considering an oil constrained future and the high emission levels associated with the

transport sector, it is therefore important to reduce the use of petroleum dependent private

vehicles in the country.

In the 1950's and early 1960's, private vehicles were less in number and road transport served as

a mode complimentary to public transportation. By the late 1990's the share of road transport in

cities was as much as 80% in passenger traffic [21]. The modal split has shifted in favor of road

transport, away from energy efficient modes like railways and buses that have a lower carbon

footprint. For example, in Delhi the modal share of public transport has dropped from 60% in 2000

to 43% in 2008 [22]. This is a likely trend not only in most megacities but also Tier II and Tier III

cities that are characterized by poor transport services and infrastructure. Only 20 cities in the

country have an organized public bus service [23], which in most cases are inadequate leading to

an increased dependence on personal modes of transport.

Exhibit 10: Comparison of Vehicular Growth with Population Growth

Source: Indiastats.com

140000

2001 2002 2003 2004 2005 2006 2007 2008 2009

Population** 102874 102761 104353 106002 108900 110600 112200 113800 115400

Public Buses* 114.9 114.6 115.2 115.7 113.2 112.1 107.8 113.6 117.6

Cars/Taxis/Jeeps* 7058 7613 8599 9451 10320 11526 12649 13950 15313

2W* 38556 41581 47525 51922 58799 64743 69129 75336 82402

PCI 40678 42375 45337 49004 54505 60951 70238 78790 88420

0

20000

40000

60000

80000

100000

120000

Electric Vehicles in India: Challenges and Opportunities 11

The growth in personal vehicle ownership will continue to accelerate with increasing incomes,

greater availability, as well as access to credit and decreasing vehicle cost, case in point being the

Tata Nano which has enjoyed an increase in sales, 5.8%, over 2011-2012 [24].

Exhibit 10 indicates a growing reliance on personal modes of transport (cars and two-wheelers)

and intermediate modes of transport (taxis and auto-rickshaws) driven by the doubling of per-

capita incomes from 2001 to 2009. Over the same period the number of public buses has

remained relatively constant considering a rise in population of approximately 125 million. This

data suggests a growing trend towards a reliance on personal modes of transport due to the

burgeoning middle class, a lack of urban planning and minimal investments by the Government

towards improving public transportation.

Bus services in particular have deteriorated because public transport service providers are unable

to expand services, both in terms of number of buses and number of routes plying. The share of

buses is negligible when compared to private/personalized vehicles in most Indian cities.

Overcrowding of the public transportation system is particularly evident in large cities, where

buses and trains carry more than twice their optimal capacity. As a result we have seen a massive

shift towards personalized transport, particularly two-wheelers, and the growing use of

intermediate modes such as taxis and three-wheeler auto-rickshaws [25].

At this juncture, it should be noted that the Government has drawn plans to improve local rail

networks in urban cities by improving access and expanding existing capacity. Other urban

transport planning initiatives include bus-rapid-transport-systems (BRTS), pedestrian zones,

skywalks and cycling paths. Delhi, Mumbai, Kolkata, Chennai and Hyderabad are in different

phases of planning or implementing light-duty metro rail services to complement existing modes

of public transport. It is envisaged that these plans will have some impact on increasing the share

of public transport. However given India's low motorization index and the lack of adequate

investments in public transport, the country is further expected to exhibit growth in light duty

personal vehicles.

India will be faced with the complex problem of convincing people not to use their vehicles

because this would increase the demand for oil imports - adding to the budget deficit while

contributing to the country's growing carbon footprint. Therefore, the only way to really shift

population mindsets is by making public transportation networks extensive, accessible and safer.

In the interim, alternative modes of sustainable personal transportation must be explored to

tackle the immediate socio-environmental impacts of the Internal Combustion Engine.

Sustainable Personal Transportation

Sustainable transport systems aim to reduce emissions, fossil fuel

consumption and minimize the land area requirements, while providing easy

access to people to enable efficient mobility [25]. Vehicles that run on

alternative sources of energy such as solar, bio-fuels, fuel cells and batteries

have been developed, demonstrated and in some cases they have entered

markets and are already on the roads.

2.1 Technological Innovations in Low-Carbon Transport

A brief overview of key innovations in low-carbon vehicles that are being

actively pursued in India:

1. Electric Vehicles (EV)

EV's utilize electric motors to induce propulsion. The key differentiator between

EV's and conventional ICE vehicles is that the electricity that they consume can

be derived from different sources or a combination of energy sources,

particularly renewables such as solar and wind energy. Electric vehicles are only

as 'green' as the energy sources used to charge them. Charging EV's in India

remains a challenge, where 60% of electricity is generated from fossil fuels

fired coal power plants [26].

Electricity can be transmitted to EV's wirelessly through induction or directly

using an electrical cable. EV's utilize on-board batteries to store electricity.

Unlike ICE's, EV's are capable of regenerative braking whereby they are able to

recover the energy that is lost during braking as electricity that is then stored

back into the on-board battery. They do not have any tail-pipe or evaporative

emissions and are virtually maintenance free. There has been a renewed

Sustainable Personal Transportation

Electric Vehicles in India: Challenges and Opportunities14

interest in EVs as a solution to address the emerging concerns around energy security and

climate change. There are almost 40 new production ready electric vehicles and hybrid vehicles

launching by 2013.

Bio-fuels are broadly defined as “fuels that are produced directly or indirectly from organic

material – biomass – including plant materials and animal waste” [27]. Efficiency improvements in

conversion technology now permit the extraction of bio-fuels from a wide variety of sources,

particularly, wood, crops and waste materials. Bioethanol and biodiesel are the two most

commonly available types of biofuels. Biofuels have been around since the invention of the

automobile but were largely displaced by the discovery of huge deposits of oil that kept petrol

and diesel prices cheap for decades.

Bio-fuels are a renewable resource as more plants can be grown for conversion into fuel, with the

added advantage that the plants sequester carbon as they grow. Over the last decade there has

been much debate about the relative pros and cons of focusing on biofuels as a viable solution

based on a range of economic, social, environmental and technical issues. The large scale

production of bio-fuel for transportation would require large land areas; as a result its potential to

replace fossil fuels is limited. However, innovative approaches like using seaweed to produce

biofuels might address the 'food vs. fuel' debate and lead to breakthroughs.

The current world production of biofuels is less than 1% of world transport fuel demand and India

contributed about 0.6% of global biofuels production in 2009 [28]. In India, bio-fuels have an

assured market as the Government, through the 'National Biofuel Policy', aims to meet 20% of

diesel with fuel derived from plants. In 2009, the Government of India mandated 5% blending of

ethanol with petrol across India, which is projected to annually save 80 million liters of petrol [29].

Vehicles are increasingly using compressed natural gas (CNG), or less commonly liquefied natural

gas (LNG), as an alternative to conventional fuels as it is cheaper and cleaner. In 2010, there were th~12.6 million CNG/LNG vehicles plying the roads worldwide with India ranked 5 , with a total

fleet of approximately 1.08 million vehicles [30]. Existing petrol or diesel vehicles can be easily

modified to run on CNG at an average cost of INR 20,000 [31] for petrol vehicles and about INR

50,000 for diesel vehicles. CNG is one of the more promising alternative fuels due to its

abundance and zero emissions. The strongest driver of CNG development has been its favorable

economics i.e. the price advantage of CNG over conventional fuels.

CNG as a transport fuel has been actively promoted by the Government of India through

mandates and targets. The CNG programs in Delhi and Mumbai are the oldest and well matured,

driven by public policy mandates and a strong commercial interest of large taxi fleets in fuel/cost

savings. The Ministry of Environment and Forests recently stated that approximately 70% of intra-

2. Bio-fuels

3. Compressed Natural Gas (CNG)

Electric Vehicles in India: Challenges and Opportunities 15

Electric Vehicles in India: Challenges and Opportunities16

city public buses use CNG as fuel [32]. Rising petrol and diesel prices have stimulated demand for

CNG vehicles and many auto majors like Maruti-Suzuki, Tata Motors, Chevrolet, Toyota, Hyundai,

among others, have introduced factory fitted CNG vehicles of their popular models in the Indian

market.

Hydrogen vehicles internally convert the chemical energy from hydrogen to mechanical energy for

propulsion either through burning hydrogen in an internal combustion engine or through reactions

between hydrogen and oxygen in fuel cells that run electric motors.

Hydrogen vehicles are divided by two different technological approaches, namely -

i. Hydrogen-ICE: Existing cars that run on petrol and diesel can be modified to use hydrogen as

a fuel in their internal engines.

ii. Hydrogen Fuel Cell: Hydrogen fuel cell cars are essentially electric vehicles that use hydrogen

fuel cells instead of battery packs for power.

Hydrogen has proved to be an attractive fuel as it has excellent electro-chemical reactivity,

adequate power density to enable automobile propulsion and zero tail-pipe emissions [33].

Hydrogen can be produced using a wide variety of sources such as natural gas, coal, biomass,

geothermal, solar and wind, which makes it an important energy carrier from an energy-security

stand point. Most automobile majors have invested in developing prototypes and are at various

stages of testing commercial feasibility of HFV.

Though HFVs are considered to be zero emission vehicles, they do have 'well to wheel' (total

lifecycle) emissions, as most of the hydrogen used is produced from natural gas. Though HFCV's

tend to outperform battery electric vehicles in terms of range and refueling time, they yet face

significant technical and economic hurdles that critics, like Nobel laureates Steven Chu and Burt

Richter, say would not be overcome in the near future [34]. Most research tends to support a

hydrogen economy as a long term option as the hydrogen option suffers from several

uncertainties around system and infrastructure costs and is not likely to be available en-mass in

the foreseeable future, i.e. before 2020.

In India, the Planning Commission has constituted working groups to look at hydrogen as a viable

fuel. The Ministry of Petroleum and Natural Gas created a INR 100 cr. (USD 18.5mn) fund for

research and development of hydrogen technologies. Other efforts include - The Green Initiative

for Future Transport (GIFT), which aims to research, develop and demonstrate hydrogen fuel cell

vehicles, with goals and targets up to 2020. India is also one for the 16 founding members of the

International Partnership on Hydrogen Economy set up in Washington D.C., on November 2003

and has also prepared a National Hydrogen Energy Road Map and Programme (2006) focusing on

two and three-wheelers [35]. Few Indian vehicles manufactures like Mahindra and Tata Motors, in

4. Hydrogen Fuel Vehicles (HFV)

Electric Vehicles in India: Challenges and Opportunities 17

partnership with research institutes have developed prototypes of hydrogen vehicles to test their

feasibility in the Indian market.

Hybrid/Dual Fuel Vehicles are defined as vehicles that use two or more distinct fuel sources, or a

mixture of fuels, for power and propulsion. HFVs are viewed as a transition technology to bridge

the gap towards zero-emission vehicles because they provide consumers with flexibility in terms

of fuel costs, refueling time, driving distances and emission reductions [37]. They tend to be

cleaner and are more fuel-efficient than conventional vehicles that use an ICE, the extent of which

depends on the combination of fuel sources used. Many different combinations of fuel sources

have been developed and tested for vehicles.

Hybrid vehicles typically ensure savings in terms of fuel economy and emissions due to the

following:

i. Relying on both engines and electric motors for their power needs, as this reduces the size

and weight of engines resulting in less internal losses.

ii. The tank-to-wheel efficiency of electric motors is also significantly higher than ICEs.

iii. Batteries have the capacity to efficiently store, reuse and recapture energy, through

technologies like regenerative breaking that save energy normally wasted as heat during

braking.

iv. Vehicles use blended fuels, like ethanol added to petrol or hydrogen mixed with CNG, as the

addition of low emission fuels to conventional fuels reduces the total fuel emission factor.

5. Hybrid/Dual Fuel Vehicles (HFV)

Exhibit 11: Various fuel combinations being pursued through Government initiatives

and by automobile manufactures

Source: YES BANK Analysis

Blended Fuels

Biofuel +GasolineHydrogen +CNG

(Hy-thane)

Dual Fuels

CNG +

Gasoline

Electric +

Gasoline

GaseousLiquid

Hybrid and Dual Fuel Vehicles

Electric Vehicles in India: Challenges and Opportunities18

The Government of India, in partnership with automobile manufacturers and research institutes,

has been exploring the feasibility of blended fuels and dual fuel vehicles. The future will most likely

see a combination of solutions being used for different purposes based on their relative suitability.

For example, while dual fuel vehicles might be promoted in densely populated urban environment

that have the required recharging/refueling infrastructure, vehicles running on a mix of gasoline

and ethanol might be suited to inter-city mobility or long distance journeys where recharging

infrastructure for electric vehicles or CNG refueling facilities are absent. The Ministry of New and

Renewable Energy, along with SIAM, IOCL, Tata Motors, Ashok Leyland, Eicher Motors, Mahindra

and Mahindra and Bajaj Auto, have supported a unique project for demonstrating a hybrid Hythane

(H-CNG) model, using up to 30% of hydrogen and CNG, in cars, buses and three-wheelers[35].

Vehicles that utilize new technologies to improve the overall engine efficiency and reduce

emissions of internal combustion engine vehicles are collectively called Advanced Internal

Combustion Engine (AICE) vehicles. Automobile manufacturers constantly strive to improve the

efficiency of ICE vehicles to reduce energy loss, improve mileage, reduce tail-pipe emissions and

ultimately lower the cost of operation. The Government of India has also driven engine efficiency

improvements by imposing the Bharat Stage (BS) emissions standards, which are progressively

updated. They stipulate emissions limits for different vehicles categories. Automobile

manufacturers must meet the stipulated criteria as they are mandatory.

In cost-conscious markets like India, a key decision point for consumers is the total cost of

ownership of vehicles – which includes the price of the vehicles, the cost of fuel, and

maintenance costs. Cars that have a higher efficiency require comparatively less fuel to travel a

particular distance. As a result their fuel consumption and running costs are less. However, it is

important to consider the 'rebound effect', formally referred to as the Khazzoom-Brookes

postulate [37], that has been confirmed by a wide range of studies and indicates that when energy

prices are constant, cost effective efficiency improvements will increase economy-wide energy

consumption above what it would have been without those improvements or in simpler terms -

“greater the efficiency of a process, the greater the energy use” [5]. The Kazzoom-Brookes

postulate clearly suggests that energy efficiency improvements in the automobile sector would

not suffice to meet future transportation goals (i.e. de-carbonization of the transport sector), as

they would invariably lead to an absolute increase in energy/fuel consumption and thus carbon

emissions [37].

Advanced ICE's are not an end solution but they will play an important role as an intermediate

wedge until other low-carbon alternatives like EVs and HFV's achieve scale and market

penetration.

6. Advanced Internal Combustion Engine (AICE)

Electric Vehicles in India: Challenges and Opportunities 19

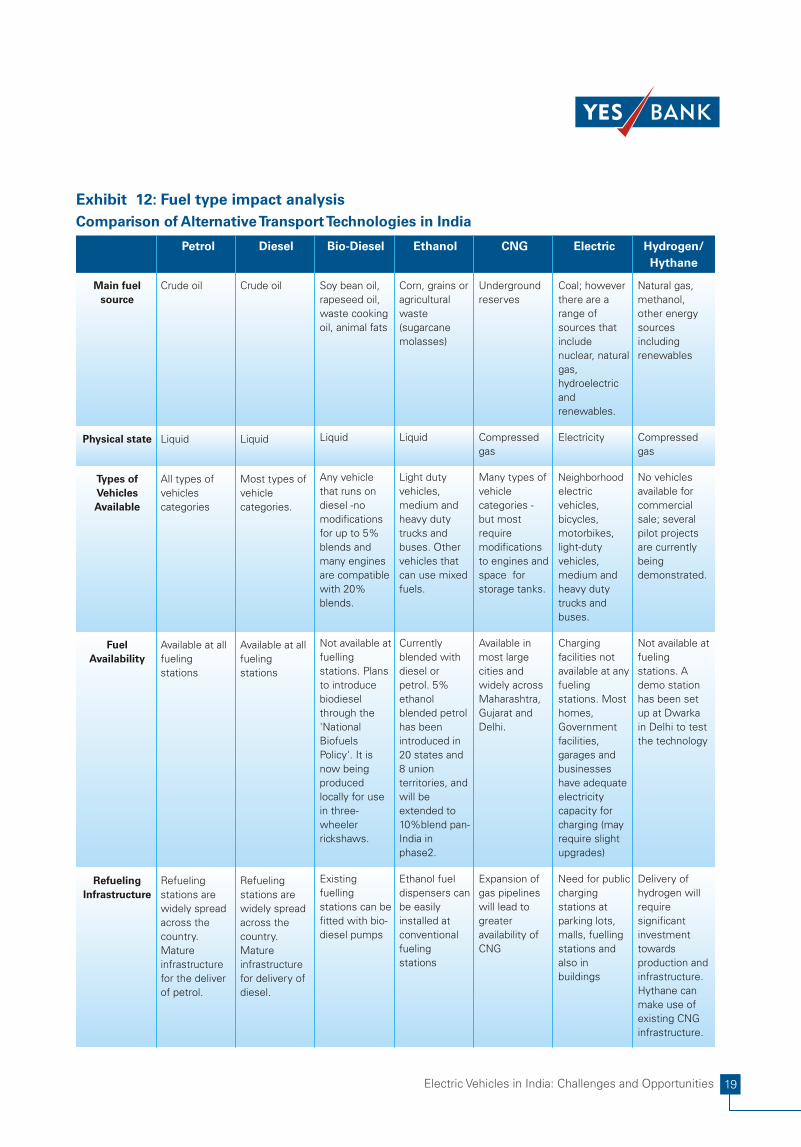

Exhibit 12: Fuel type impact analysis

Petrol Diesel Bio-Diesel Ethanol CNG Electric Hydrogen/

Hythane

Main fuel

source

Physical state

Types of

Vehicles

Available

Fuel

Availability

Refueling

Infrastructure

Crude oil

Liquid

All types of

vehicles

categories

Available at all

fueling

stations

Refueling

stations are

widely spread

across the

country.

Mature

infrastructure

for the deliver

of petrol.

Crude oil

Liquid

Most types of

vehicle

categories.

Available at all

fueling

stations

Refueling

stations are

widely spread

across the

country.

Mature

infrastructure

for delivery of

diesel.

Soy bean oil,

rapeseed oil,

waste cooking

oil, animal fats

Liquid

Any vehicle

that runs on

diesel -no

modifications

for up to 5%

blends and

many engines

are compatible

with 20%

blends.

Not available at

fuelling

stations. Plans

to introduce

biodiesel

through the

'National

Biofuels

Policy'. It is

now being

produced

locally for use

in three-

wheeler

rickshaws.

Existing

fuelling

stations can be

fitted with bio-

diesel pumps

Corn, grains or

agricultural

waste

(sugarcane

molasses)

Liquid

Light duty

vehicles,

medium and

heavy duty

trucks and

buses. Other

vehicles that

can use mixed

fuels.

Currently

blended with

diesel or

petrol. 5%

ethanol

blended petrol

has been

introduced in

20 states and

8 union

territories, and

will be

extended to

10%blend pan-

India in

phase2.

Ethanol fuel

dispensers can

be easily

installed at

conventional

fueling

stations

Underground

reserves

Compressed

gas

Many types of

vehicle

categories -

but most

require

modifications

to engines and

space for

storage tanks.

Available in

most large

cities and

widely across

Maharashtra,

Gujarat and

Delhi.

Expansion of

gas pipelines

will lead to

greater

availability of

CNG

Coal; however

there are a

range of

sources that

include

nuclear, natural

gas,

hydroelectric

and

renewables.

Electricity

Neighborhood

electric

vehicles,

bicycles,

motorbikes,

light-duty

vehicles,

medium and

heavy duty

trucks and

buses.

Charging

facilities not

available at any

fueling

stations. Most

homes,

Government

facilities,

garages and

businesses

have adequate

electricity

capacity for

charging (may

require slight

upgrades)

Need for public

charging

stations at

parking lots,

malls, fuelling

stations and

also in

buildings

Natural gas,

methanol,

other energy

sources

including

renewables

Compressed

gas

No vehicles

available for

commercial

sale; several

pilot projects

are currently

being

demonstrated.

Not available at

fueling

stations. A

demo station

has been set

up at Dwarka

in Delhi to test

the technology

Delivery of

hydrogen will

require

significant

investment

towards

production and

infrastructure.

Hythane can

make use of

existing CNG

infrastructure.

Comparison of Alternative Transport Technologies in India

Electric Vehicles in India: Challenges and Opportunities20

Petrol Diesel Bio-Diesel Ethanol CNG Electric Hydrogen/

Hythane

Maintenance

Fuel Costs

(as on Sept

2012)

Environment

Impacts

Energy

Security

Impacts

Require regular

pollution

checks,

servicing,

tune-ups, oil

changes,

lubrication

INR 71/liter

Produces

harmful

emissions.

Gasoline

vehicles are

improving and

as a result

emissions are

being

progressively

reduced.

Manufactured

using mostly

imported oil

which is not a

secure option

Require regular

pollution

checks,

servicing,

tune-ups, oil

changes,

lubrication

INR 42/liter

Produces

harmful

emissions and

particulate

matter.

Emissions are

being reduced

with after-

treatment

devices.

Manufactured

using mostly

imported oil

which is not a

secure option

Hoses and

seal may be

affected with

higher-percent

blends.

Lubricity is

improved over

that of

conventional

diesel

NA

Reduces

emissions and

particulate

matter when

compared to

conventional

diesel.

However NOx

emissions may

increase.

Bio-diesel is

domestically

produced and

has a fossil

energy ratio of

3.3 to 1 which

means that its

impacts are

slightly less

but similar to

petrol

Special

lubricants may

be required.

Practices are

similar to

conventional

vehicles

INR 27/liter

Can

demonstrate

up to 25%

reduction in

ozone-forming

emissions

when

compared to

petrol.

Ethanol is

domestically

produced and

is renewable.

High pressure

tanks require

periodic

inspection and

certification

INR 32/kg

Significant

reduction in

tail pipe and

ozone forming

emissions

though HC

emissions may

increase.

CNG is

domestically

produced but

is limited. India

is currently

exploring

options of

importing

natural gas

from Iran and

Myanmar.

Minimal

servicing

needed. No

tune-ups, oil

changes,

timing belts,

water pumps,

radiators or

fuel injectors.

Batteries need

to be replaced

after 3-6 years

INR 4/kWh

Zero tail-pipe

emissions.

Some

emissions can

be attributed

to power

source/

generation.

Electricity is

generated

through coal

fired power

plants as it is

available in

plenty. It is the

most

economical

and price

stable fuel.

In fuel cell

applications

maintenance

in minimal.

Hydrogen-

ICE's would

require regular

servicing.

NA

Zero regulated

emission for

fuel cell

vehicles and

only NOx

emissions

possible with

Hydrogen ICE

vehicles.

Hydrogen can

help reduce

India's

dependence

on foreign oil

by being

produced from

renewable

resources

2.2 Pathway to Zero-Emission Vehicles

The path towards Zero-Emission Vehicles (ZEVs) begins with technological modifications and

enhancements to existing engines and drive-trains that improve the tank-to-wheel efficiency of

vehicles. Vehicles that run on low-carbon alternative fuels such as biodiesel, ethanol, synthfuels

and natural gas are categorized collectively with high efficiency ICEs as A-ICE vehicles, and they

can reduce emissions by up to 10-15% [39].

(Source: YES BANK research, SIAM, Ministry of Petrolium,

US Department of Energy –Alternate Fuels and Advanced Vehicle Data Center)

Electric Vehicles in India: Challenges and Opportunities 21

The next step towards ZEVs involves the electrification of vehicles. There are a wide range of EV

technologies being explored at the moment, that include:

üMild-Hybrid – It is the first real step towards electrification and ZEVs, and contains a small

electric motor that enables a start-stop system, facilitates regenerative braking energy to

charge the battery and offers acceleration assistance. Mild-hybrid vehicles achieve small

reductions in emissions, between 10 to 15% at relatively high costs [39]. It is viewed as an

intermediate development step towards a fully-hybrid system.

üFully-Hybrid – Features a larger motor and battery pack that provides the vehicle with electric

launching, acceleration assistance and electric driving at low speeds. It can achieve a

maximum of 25-30% in GhG emission reductions. Though fully-hybrids currently cost

between INR 2.5 to 3.5 lacs (USD 4629 – USD 6481) more than conventional ICE cars, the

cost of hybrid components is expected to fall by 5% per year [39].

üPlug-in Hybrid (PHEV) – It is a hybrid vehicle with a larger battery that can be recharged by

connecting a plug to an electric power source or grid. The ability to connect to the grid gives

the PHEV an range of 30-60 kilometers of all electric driving. PHEVs feature smaller ICE that

takes over from the all electric drive to provide a longer range. The carbon reduction potential

of a PHEV is between 30-40%.

Exhibit 13: The path to electrification

Source: YES BANK Analysis

Advanced Internal

Combustion

Natural Gas and Biofuels

Hybrid Fuel + Electric

Fully Electric

Hydrogen

Electrification

10- 30%Up to 15% 50 -100 %30-40% 50 -100 %

Tech

nolo

gic

al A

dva

nce

men

t

Carbon Reduction Potential

Electric Vehicles in India: Challenges and Opportunities22

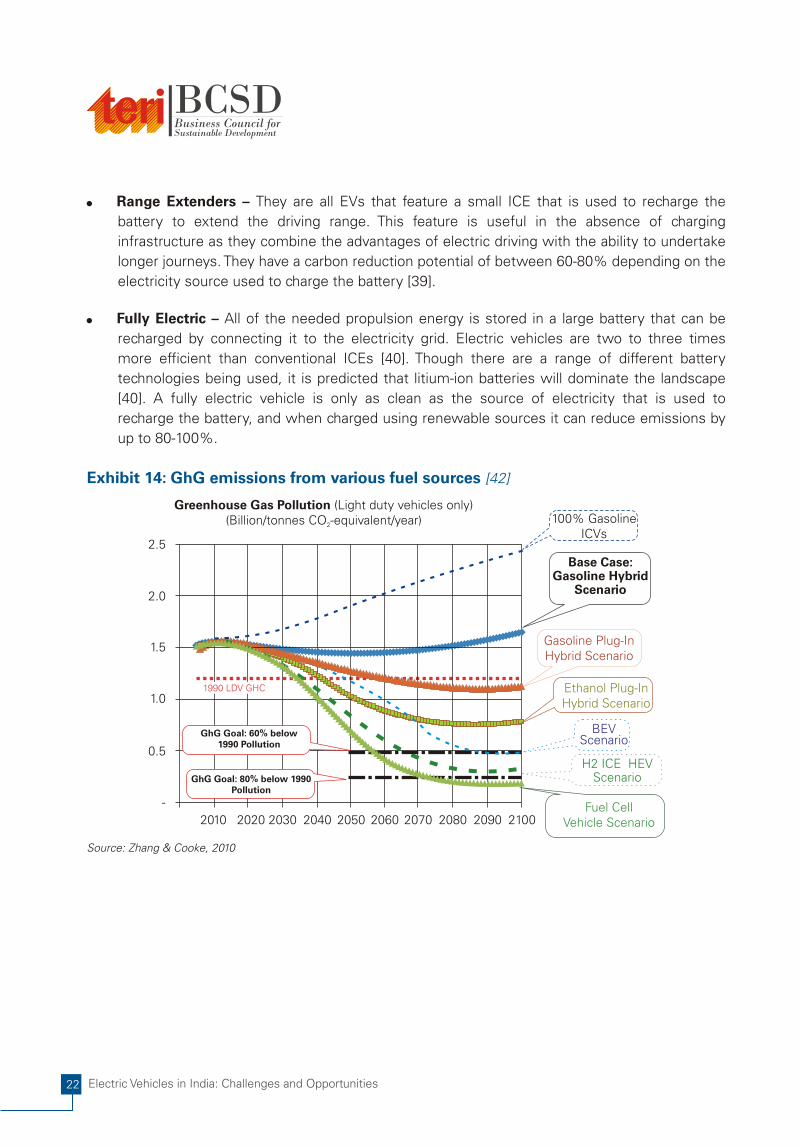

üRange Extenders – They are all EVs that feature a small ICE that is used to recharge the

battery to extend the driving range. This feature is useful in the absence of charging

infrastructure as they combine the advantages of electric driving with the ability to undertake

longer journeys. They have a carbon reduction potential of between 60-80% depending on the

electricity source used to charge the battery [39].

üFully Electric – All of the needed propulsion energy is stored in a large battery that can be

recharged by connecting it to the electricity grid. Electric vehicles are two to three times

more efficient than conventional ICEs [40]. Though there are a range of different battery

technologies being used, it is predicted that litium-ion batteries will dominate the landscape

[40]. A fully electric vehicle is only as clean as the source of electricity that is used to

recharge the battery, and when charged using renewable sources it can reduce emissions by

up to 80-100%.

Exhibit 14: GhG emissions from various fuel sources [42]

Source: Zhang & Cooke, 2010

0.5

2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

GhG Goal: 80% below 1990 Pollution

GhG Goal: 60% below 1990 Pollution

1990 LDV GHC1.0

1.5

2.0

2.5

Fuel CellVehicle Scenario

H2 ICE HEV Scenario

BEV Scenario

Ethanol Plug-In Hybrid Scenario

Gasoline Plug-In Hybrid Scenario

Base Case: Gasoline Hybrid

Scenario

100% Gasoline ICVs

-

Greenhouse Gas Pollution (Light duty vehicles only)(Billion/tonnes CO -equivalent/year)2

The Electric Vehicle Value Chain

The stimulus for a technological shift towards electric vehicles in India, as is the

case among most comparable markets, depends on improved battery

technologies, longer ranges, better charging infrastructure, lower prices,

Government incentives and progressive regulation. While electric vehicles offer

a great opportunity to diversify across the value chain, they also pose significant

risks as the technology could change the dynamics of the industry and cede

large parts of the value chain that has evolved over several decades obsolete

[43].

In order to grasp the changing landscape of the EV sector it is important to

understand the different actors across its value chain and the relationships they

share –

3.1 Raw Material Suppliers

Raw materials have a high impact on cost structures of the automobile sector.

Raw material suppliers face a host of challenges that include rising prices,

fluctuating prices, discriminatory pricing by foreign vendors of Indian

component manufacturers/exporters and custom free import of finished goods

from ASEAN countries under various free trade agreements [44]. Steel is one

The Electric Vehicle Value Chain

Electric Vehicles in India: Challenges and Opportunities24

Exhibit 15: The EV value chain

Source:YES BANK Analysis

Raw Material Suppliers

Traditional Component Suppliers

Battery Suppliers OEMS

Utilities /Infrastructure

of the primary raw materials used in the manufacture of automobiles and its price has risen

between 25% to 40% for specific products like flat, long and pig iron which are commonly used

by vehicle manufacturers. Ironically, even though India is one of the cheapest sources of iron ore,

steel prices are high when compared to international standards. The Government of India must

consider enforcing competitive policies that contain the price of steel against global steel prices

by regulating the export of steel, monitoring steel price and lowering import duty to widen access

to cheap steel sources outside India (IDC, 2008) [45]. Other raw materials like plastics and lithium

(for batteries), a rare earth metal, are also plagued by global price fluctuations. Given the growth

in demand for lithium batteries, that are used in common electronics and appliances like mobile

phones and laptops, the price of lithium is expected to rise as lithium reserves are scare and

geographically sparse. This is of particular concern to Indian battery manufacturers, considering

China is the closest source of lithium, having the largest proven lithium reserves in the world.

Also, the battery component has the highest weightage in the overall cost structure of an EV.

The auto component industry in India is expected to grow at a rate of 13-15%, having the

potential to become one of the top five auto component economies by 2025 [45]. Over the last

decade there has been a marked improvement in the quality of auto components manufactured in

India. Most of the standard components required by the Indian automotive sector are

domestically manufactured with an import dependance estimate of about 13.5% of domestic

demand. Due to growing economies of scale of the Indian auto component industry,

manufacturers of EV are likely to depend on traditional component manufacturers for all

standardized parts that go into an EV and that are common to ICE vehicles such as tyres, seats,

doors, windows etc. India exports a wide range of auto components and chassis. The auto

component industry's exports are expected to grow by about 24% during 2010-2015 [46], and can

be further bolstered by investing in technology collaborations and joint R&D. Traditional

component manufacturers can diversify their product offerings by tying up with makers of EVs,

leveraging their technological expertise, to develop specialized parts for hybrid and EV, both for

domestic and export markets. India has a relatively strong auto component base for electrical and

electronic components that can be leveraged to tap into the emerging EV sector.

A key concern in the EV sector has been the advancement of battery technology, which has

benefitted from recent breakthroughs in lithium-Ion batteries due to their application in computers

and mobile devices. There has been substantial growth in the number of lithium-ion patents in

China, USA, Japan and Western Europe [40] and batteries available today can store energy to

enable driving ranges that exceed 100 kms. Battery manufacturers have been working with

OEM's to develop batteries for EVs and many of them have been increasing production capacity

to achieve the required volume to drive down prices. The growth in the battery market for EVs will

spur investments in R&D making batteries more reliable and affordable while providing longer

driving ranges. It is likely that existing battery suppliers for mobile devices will dominate the

3.2 Traditional Component Suppliers

3.3 Battery Manufacturers & Suppliers

Electric Vehicles in India: Challenges and Opportunities 25

Electric Vehicles in India: Challenges and Opportunities26

market, though new players are quickly emerging. Battery manufacturers and suppliers will also

have to consider pro-environmental means to dispose depleted batteries as they comprise

hazardous chemicals. While some battery suppliers are forging new partnerships with automobile

manufacturers to reduce risks (e.g. Toyota and Panasonic), others continue to traditionally buy

batteries from Tier 1 suppliers (e.g. Johnson Control and Saft)

Looking ahead, OEM's face daunting challenges towards the allocation of investments in new

technologies as a result of the current financial slowdown, and yet they must adapt their

businesses to capitalize on emerging opportunities in new markets, specifically the EV sector. The

automobile industry seems to be preparing for a major shift towards powertrain technology. There

are a range of different types of EVs (see 'Pathway to ZEVs) and OEM's will have to assess

options based on their ability to leverage different actors across the value chain. Since established

OEM's have plants that are built around mass production, they offer very few cost advantages for

new powertrain configurations. OEM's could develop a competitive advantage through

partnerships with technology companies (that have know-how on electric drive-trains), battery

manufactures and traditional component suppliers to reduce risks and leapfrog the development

of EVs. In turn, they could also partner with other OEM's to share and spread associated risk, by

standardizing EV components. Manufacturers in emerging economies, India and China in

particular, are exposed to much wider business opportunities from the shift towards EVs.

“Indian cities and towns are plagued by frequent outages and the basic requirement for electric

cars is electricity…” [47]. A growth in demand for EVs will have a sizable impact on electricity

generators and suppliers. This additional demand for electricity will have to be addressed through

increased generating capacity and essentially through better grid management. Driven by reforms

beginning with 'The Electricity Act, 2003', followed by de-licensing, the power generation sector

has transformed from being a slow moving industry to a space where there lie vast growth

opportunities. By repairing or upgrading distribution equipment, efforts are being made to reduce

transmission and distribution losses, which currently stands at 28%. Covered in a later section,

we will explore the possibility of introducing smart grids in major metropolitan cities, from a

technical perspective. India's power sector has increased generation capacity by record numbers

this year, and it is expected to double from the current 177 gigawatts (2011) to 300 gigawatts by

2015 [48]. India also has plans to generate 15% of the electricity mix through renewable sources

such as solar, wind, biomass, geothermal and hydro energy [49]. Solar energy is expected to grow

to the tune of 2 GW by 2013, gradually scaling up to 20 GW by 2020 [50], and wind energy

generation capacity which has experienced phenomenal growth, stands at 13 GW (Dec, 2010) and

is expected to grow to about 50 GW by 2020 [49]. According to a number of studies, electricity

demand from EVs can 'increase the penetration of wind as a baseload resource' [51], since the

generating profile of wind energy matches the load profile of a night-time charging regime.

Increasing the renewable energy mix would reduce the emission factor of the total electricity

3.4 Original Equipment Manufacturers (OEMs)

3.5 Utilities

Electric Vehicles in India: Challenges and Opportunities 27

generation mix, rendering EV's cleaner and greener. Since EVs are only as clean as the electricity

used to charge them, adding renewable energy to the mix would only boost their green

credentials. EV manufacturers must liaise with utility providers in order to develop innovative

solutions for charging of public and private, including option of using renewable energy sources.

3.6 The Electric Vehicle Ecosystem

Exhibit 16: The EV Ecosystem

Source: Mahindra - Reva

Insurance

e DT ch R&

Climate Change

Policy

Smart Charging

V2G

Building/VehicleInteraction (V2B)

Grid Storage

Smart Grid

Firming Renewables

Renewable Power

Li-ion Battery

Vehicle Electrification

Consumers

Data Flow

Finance

Information

Money

Electricity

Major trendsKey system players

Electric Vehicles in India: Challenges and Opportunities28

Exhibit 17: EV risks, challenges & solutions

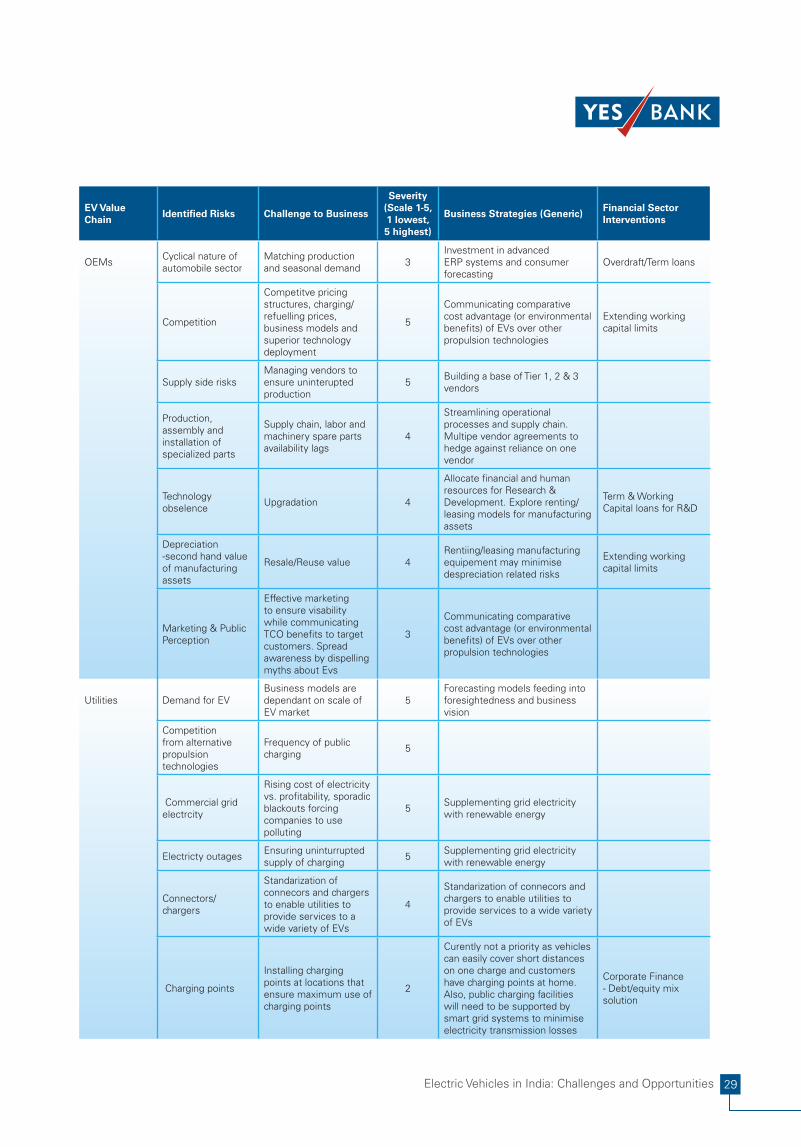

Electric Vehicles in India: Challenges and Opportunities 29

Electric Vehicles in India: Challenges and Opportunities30

EV

Safety chassissafety

Source: YES BANK Analysis

Policies Promoting Electric Vehicles

in India

Policies Promoting Electric Vehicles in India

Electric Vehicles in India: Challenges and Opportunities32

The Government of India, along with several State Governments, have

supported many initiatives promoting environmentally friendly technologies.

Over the last few years several steps have been taken in this direction by using

regulation as the primary driver. The following section highlights some of the

major initiatives that have been taken by the Government to support the cause

of electric mobility in India.

4.1 Initiatives by the Ministry of New and Renewable Energy (MNRE)

The Ministry of New and Renewable Energy (MNRE) in November 2010

decided to offer incentives to EV manufacturers during the remaining period of

Exhibit 18: Green Transport in India

Source: KPMG, YES BANK Analysis

CNG conversion of buses, taxis and auto-rickshaws introduced in

Mumbai

India’s first CNG bus launched

Supreme Court orders to convert

all city bus fleets, taxis and

auto-rickshaws in Delhi to CNG

First electric car commercialized in India (Reva)

India’s first MUV-‘Omni

Cargo’ launched by Maruti-Suzuki

Reva exported to European markets and branded as

G-wiz

All buses in Delhi

converted to CNG

India’s first dual fuel (petrol + LNG)

passenger car ’Wagon R Duo’

launched by Maruti-Suzuki

–

India’s first electric two wheeler

launched –‘Yo Byke’ by Indus Elec-trans

Hero Electric launches

electric two wheeler

First hybrid car launched in India-Honda Civic Hybrid

1,10,000 electric vehicles sold -

97-98% of which were

two wheelers

Full exemption from central excise duty

provided to EVs

Delhi is the first city in India to introduce

a hybrid electric-CNG public bus manufactured by

Tata Motors

GOI sets up the National Mission

for Hybrid and Electric Vehicles

Karnataka is the first state to utilize bio-fuels

and ethanol-blended fuels in public buses

in Bangalore

First section of the Delhi Metro Rail–the

red line-opened

1998 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011