Embed Size (px)

Citation preview

ABOUT FRESH ARTSONLINE SERVICES

• The Culture Guide

Online event calendar

• The Houston Artist Registry

A warehouse of local artists and creatives

• Houston Artist Field Guide

A wealth of resources for artists and arts administrators

PHYSICAL PROGRAMMING

• Community Supported Art

A subscription for local art

• Workshops & Professional Development- Offered to assist arts administrators and artists

• Exhibitions - We work exclusively with local emerging artists

• Cultured Cocktails

Raises funds for local arts projects

• Winter Holiday Art Market

An annual holiday art market involving over 60 local artists (Last year we sold over $153,000 of local art!)

• M-Lab - Marketing incubator for small to mid-sized nonprofit organizations

ABOUT OUR GUEST experts TONIGHT:

Amy Lampi has 12 years of fundraising experience in the arts, education and

now health care. As a development generalist, she has done everything from gift

processing and database administration to major gift fundraising and

management of a department/team. Her current role as Senior Director of

Development Support Services at Memorial Hermann Foundation has her

overseeing database, prospect research, gift processing, finance and annual

fund for the Foundation. Her goal is to streamline processes and discover best

practices so fundraising operations remain smooth and efficient.

Joanna Torok’s first official paycheck came from the Houston Grand Opera

in 1989, after performing as a children’s chorus member in Carmen. Many years

later, after various professional experiences and obtaining an MBA in 2008,

Joanna decided to take the leap from corporate America back in to the arts

community. With a background in technical television operations, Joanna has

always had an interest in back-end technology, and developing systems for

seamless product distribution. Currently working as the Director of Advancement

Operations, Joanna specializes in automating processes and increasing

operational efficiency in the Development and Marketing departments of HGO.

Development Finance and Operation

Basics for the Jack-of-All Arts

Administrator

Gift Acceptance, Disclosure Rules & Basic Financial

ReportingAmy Lampi

Senior Director of Development Support Systems

Memorial Hermann Foundation

Joanna Torok

Director of Advancement Operations

Houston Grand Opera

We would like to acknowledge the contribution of the GWSCPA for some of the copyrighted content of this

presentation.

http://www.gwscpa.org/

Creating simple systems for fund development

management and operations

Timing, rules, and language for donor receipts

Common mistakes in communicating the tax benefits of

donations

How to determine Fair Market Values for special events,

etc.

Basic financial reports

Forecasting revenues

Reconciling fundraising activities with greater financial

goals

Daily ‘to-dos’ to stay on track (Amy)

Resources

The BIG ideas. What we will cover:

OPERATIONAL SYSTEMS

No matter your size, invest in healthy

operational systems:

Financial investment

• Hiring &/or training qualified staff

• Implementing new Software/Programs

Resource investment

• Time researching needs

• Creating & updating Policies & Procedures

• Developing effective system

OPERATIONAL SYSTEMS

Researching Needs: Data ManagementCloud based v. Installed v. Consortium

1. Reach out, ask questions– What are others using? Good vs. Bad

– Is a free system sufficient for your needs?

2. Think Long-term– Before committing: Scalable/strategic forward thinking

– After commitment: Set-up/ Structure

Already set up with a system?

• Analysis

• Possible realignment/restructure

Researching Needs: Reporting

Q: When do your stakeholders need information?

• What info and when?

• Develop and stick to a reporting schedule

• Automate reports where you can / create templates– Daily transaction log: see example on next slide

– Mail Merges- create and use template letters for:

• acknowledgements, receipts, invoices

– Gift acknowledgments sent within 72 hours (if at all possible)

– If 72 hr. formal acknowledgment isn’t possible, a phone call or email acknowledgment will build important trust with your donor

– Sample acknowledgment will be included in follow up materials

– Report templates

• Excel sheets, email text, .pdf

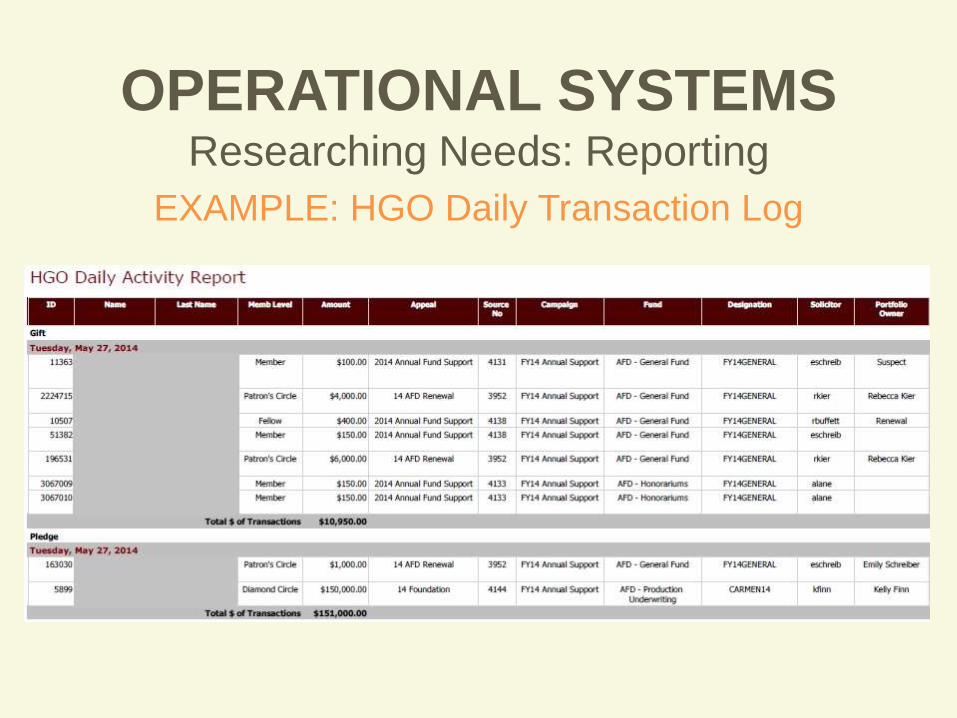

OPERATIONAL SYSTEMS

Researching Needs: Reporting

EXAMPLE: HGO Daily Transaction Log

OPERATIONAL SYSTEMS

Researching Needs: Roles &

Responsibilities

Define up front, who is responsible for what

• Create written workflows, accessible to all staff

• Delegate and Define, no matter the size

– Important in the scheduling of reports/duties

– Ownership of quality

– No questions

• ARC-Authorization, Record-keeping & Custody

– Best practice: have three separate people responsible for

recording different aspects of any financial transactions

• Add info to or start a Policy & Procedure document

OPERATIONAL SYSTEMS

Researching Needs: Policy & Procedures[ aka Operations Manual ]

• Clearly state the organization’s expectations for transparency and accountability

• Promote good internal controls

• Backed by / approved by Board & Senior Management

• Updated regularly: This is an organic document that will grow with your organization.

• Good to start by documenting major annual events

OPERATIONAL SYSTEMS

&

• After all research is done, build timelines and

workflows

– Think smart, efficient

• Use all information collected in research and build optimal

system around your needs

– Prioritize by importance/weight

• Stakeholders, financial, legal

• Organic in nature

– Let it flow, it should feel right and not forced

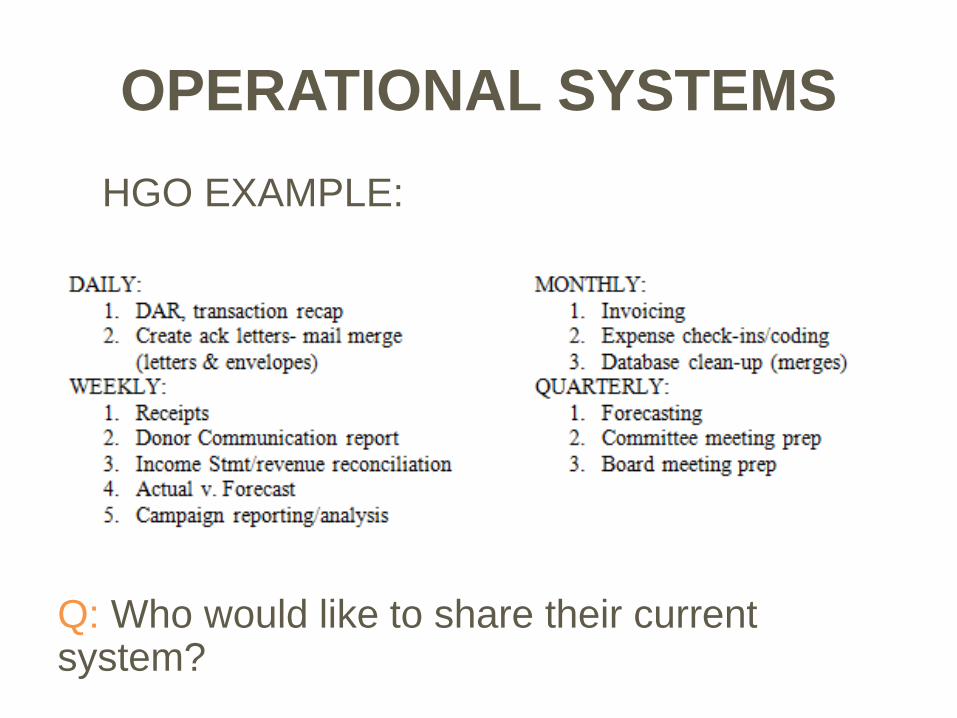

OPERATIONAL SYSTEMS

HGO EXAMPLE:

Q: Who would like to share their current system?

OPERATIONAL SYSTEMS

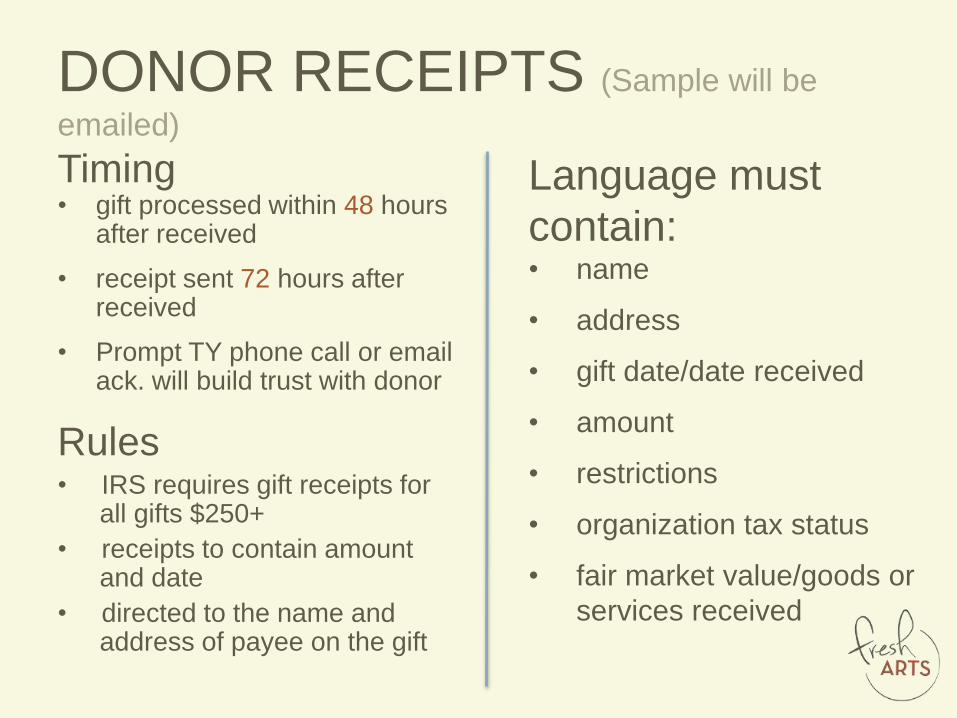

DONOR RECEIPTS (Sample will be

emailed)

Timing• gift processed within 48 hours

after received

• receipt sent 72 hours after received

• Prompt TY phone call or email ack. will build trust with donor

Rules• IRS requires gift receipts for

all gifts $250+

• receipts to contain amount and date

• directed to the name and address of payee on the gift

Language must

contain: • name

• address

• gift date/date received

• amount

• restrictions

• organization tax status

• fair market value/goods or

services received

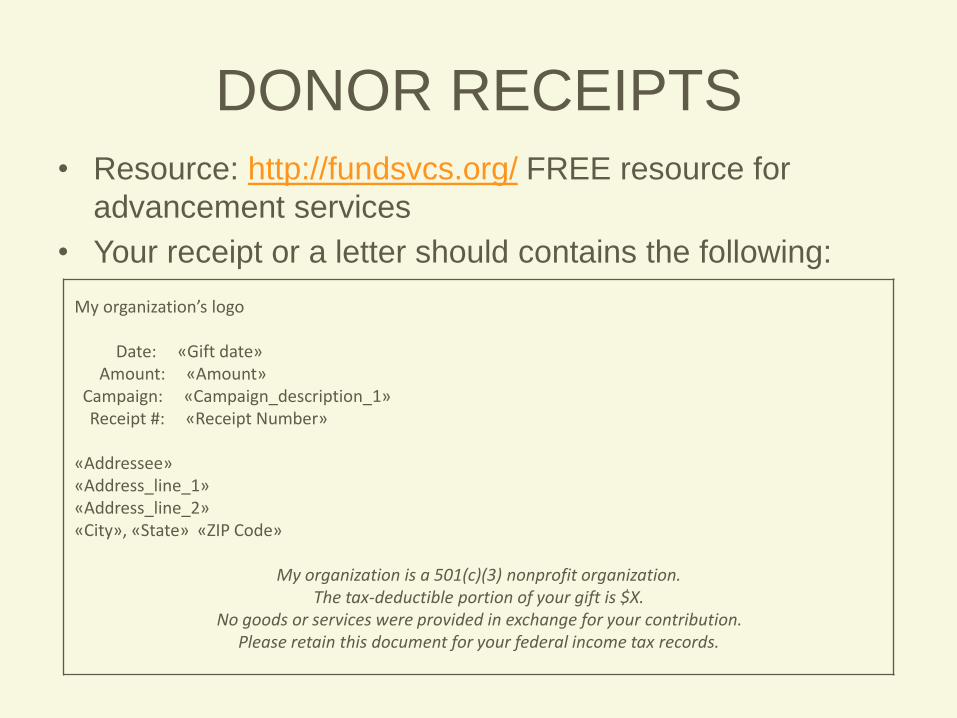

DONOR RECEIPTS

• Resource: http://fundsvcs.org/ FREE resource for

advancement services

• Your receipt or a letter should contains the following:

My organization’s logo

Date: «Gift date» Amount: «Amount»

Campaign: «Campaign_description_1»Receipt #: «Receipt Number»

«Addressee»«Address_line_1»«Address_line_2»«City», «State» «ZIP Code»

My organization is a 501(c)(3) nonprofit organization. The tax-deductible portion of your gift is $X.

No goods or services were provided in exchange for your contribution. Please retain this document for your federal income tax records.

TAX BENEFITSCOMMON MISTAKES IN COMMUNICATING TAX BENEFITS:

• Raffle tickets

• In Kind Goods

• In Kind Services

• Membership benefits

• Special events

• Donated “Services" are not tax deductible

• Donations are only 100% tax deductible if absolutely no goods or services are received

• Fundraising events are not fully tax deductible (unless the donor does not attend)

• Stewardship events are usually tax deductible

• Giving away stuff to donors with your orgs logo can be tax deductible, but know the IRS limits

TAX BENEFITS

RESOURCES:

IRS Publication 526

IRS Publication 561

“Quid Pro Quo”

Contributions

http://www.irs.gov

FAIR MARKET VALUE• Fair market value (FMV): is good faith estimate of any goods or

services received in exchange for a contribution

• Basically, if you were to walk off the street to an event, what is the value of what you consume or receive in exchange for your donation at the event

• Good faith estimates can be a grey area

• Some organizations are more conservative than others

• Bottom line, you could get fined if audited by the IRS $1,000 per underestimated FMV receipt

• This includes any gifts donated to guests at the event (unless your logo is on them, see quid pro quo)

• Do not count taxes

• Do not count catering charges

• Do not count entertainment value (may be considered in-kind donation)

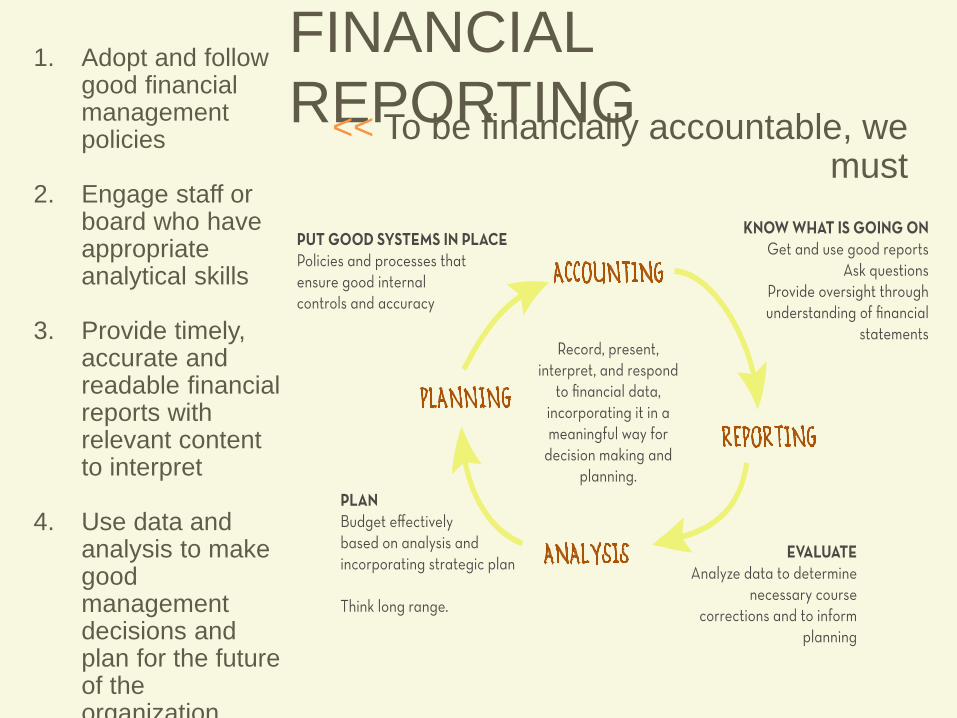

FINANCIAL

REPORTING<< To be financially accountable, we must

1. Adopt and follow good financial management policies

2. Engage staff or board who have appropriate analytical skills

3. Provide timely, accurate and readable financial reports with relevant content to interpret

4. Use data and analysis to make good management decisions and plan for the future of the organization

FINANCIAL REPORTING

Ties back to Research phase:WHAT INFO DO WE NEED > When do we need the

report?

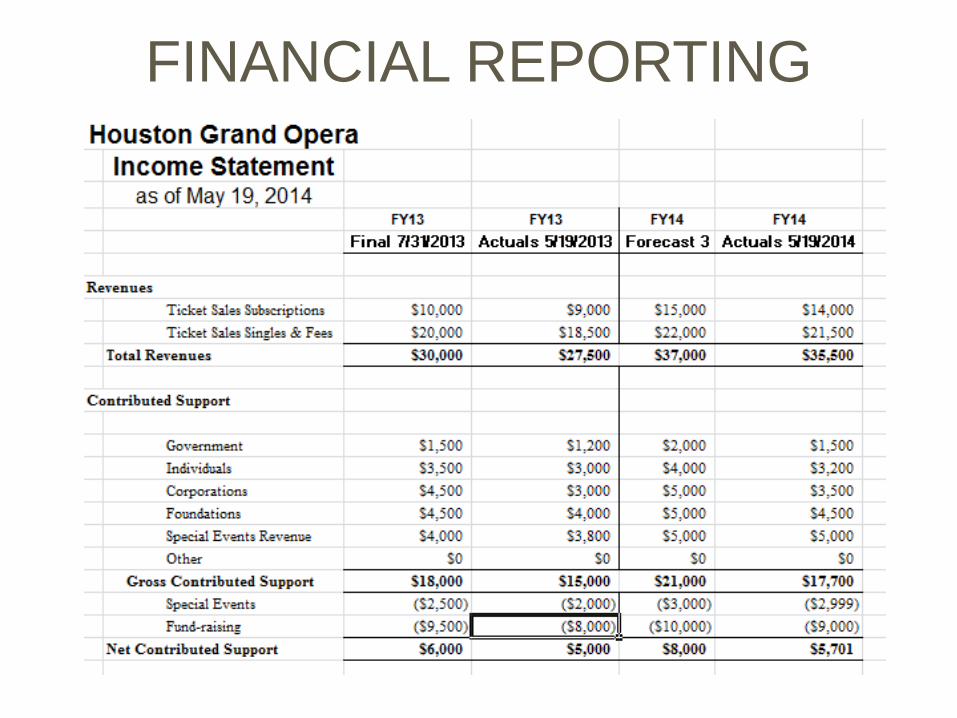

Standard Reports

Primary: Income Statement, Balance Sheet

Secondary: Revenue detail (contributed & earned),

Expense detail, Actual v. Forecast, Current v. Prior year

Income Statement

Reflects the changes to an organization’s net assets resulting from income and expenses that occur during the current fiscal year.

• What was last year’s total?

• What is the annual budget for this year and what percentage of the budget is represented by the year-to-date amounts?

• How do we expect to end the year and how does that compare to the approved budget?

FINANCIAL REPORTING

FINANCIAL REPORTING

The Reporting ProcessDefine constituents Gather needs Build & Test

Evolve

Example: HGO Finance Committee

1. Set schedule/agenda in advance

2. Develop standard reports

3. Gather feedback, refine

FINANCIAL REPORTING

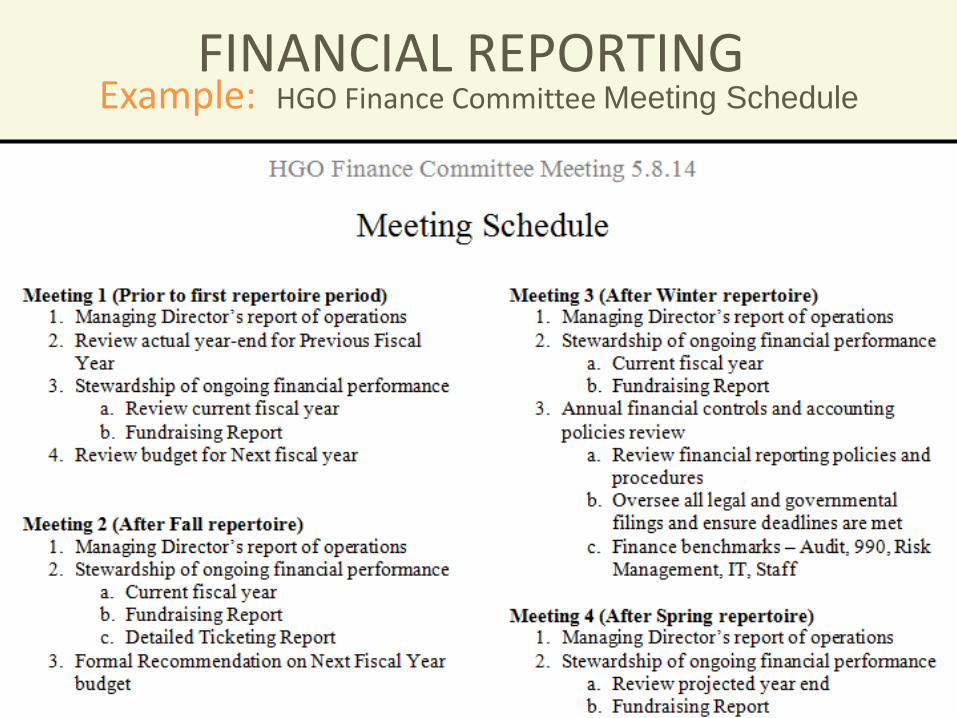

Example: HGO Finance Committee Meeting ScheduleFINANCIAL REPORTING

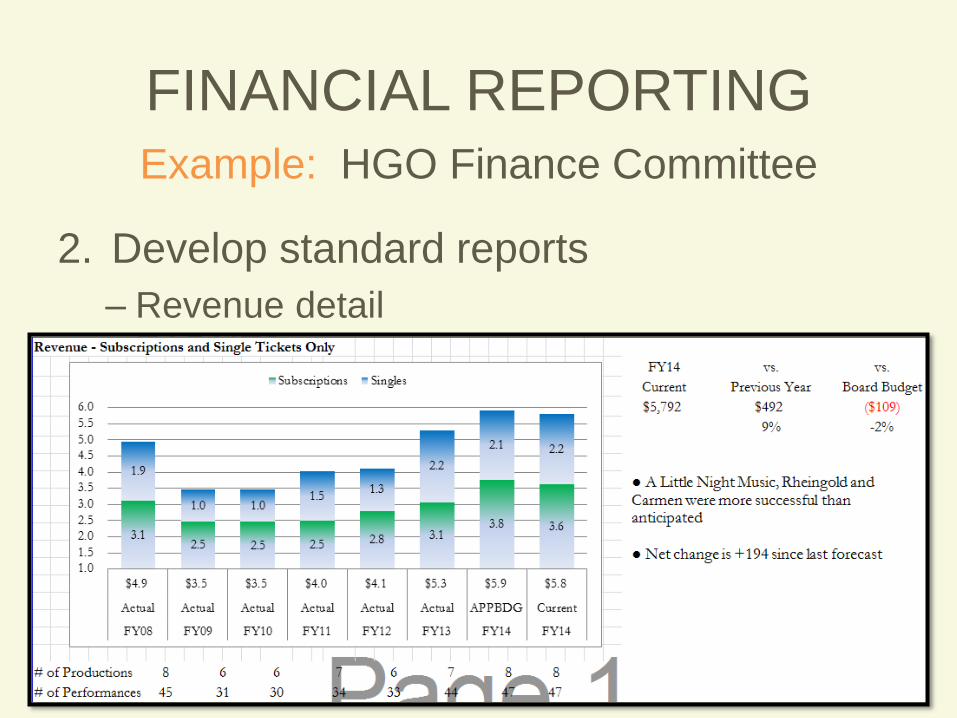

Example: HGO Finance Committee

2. Develop standard reports

– Revenue detail

CONTRIBUTED

FINANCIAL REPORTING

Example: HGO Finance Committee

2. Develop standard reports

– Revenue detail

EARNED

FINANCIAL REPORTING

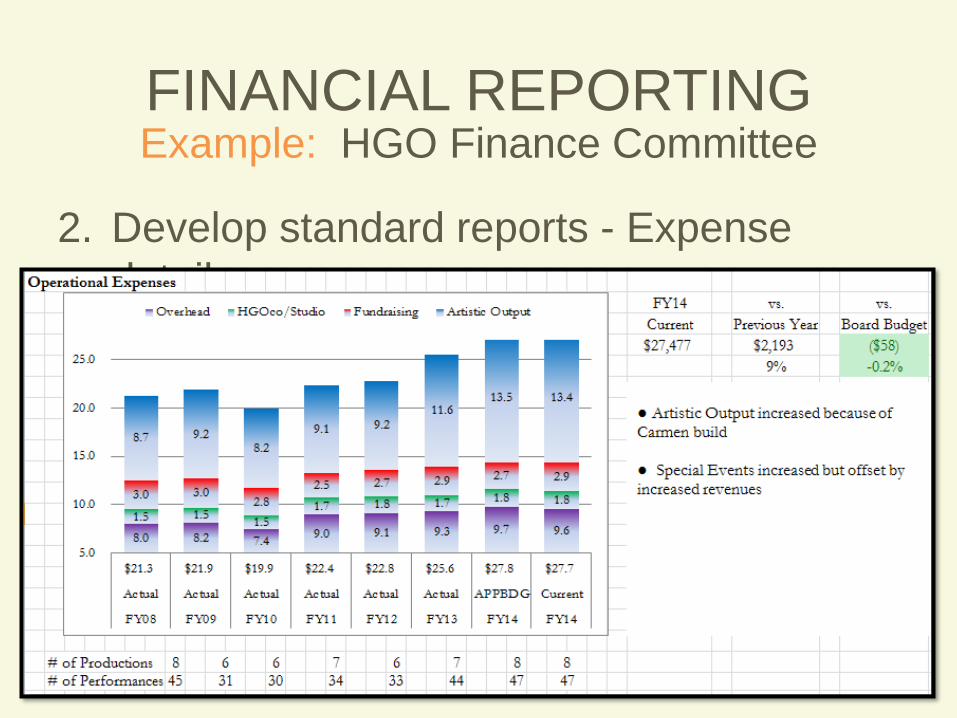

Example: HGO Finance Committee

2. Develop standard reports - Expense

detail

FINANCIAL REPORTING

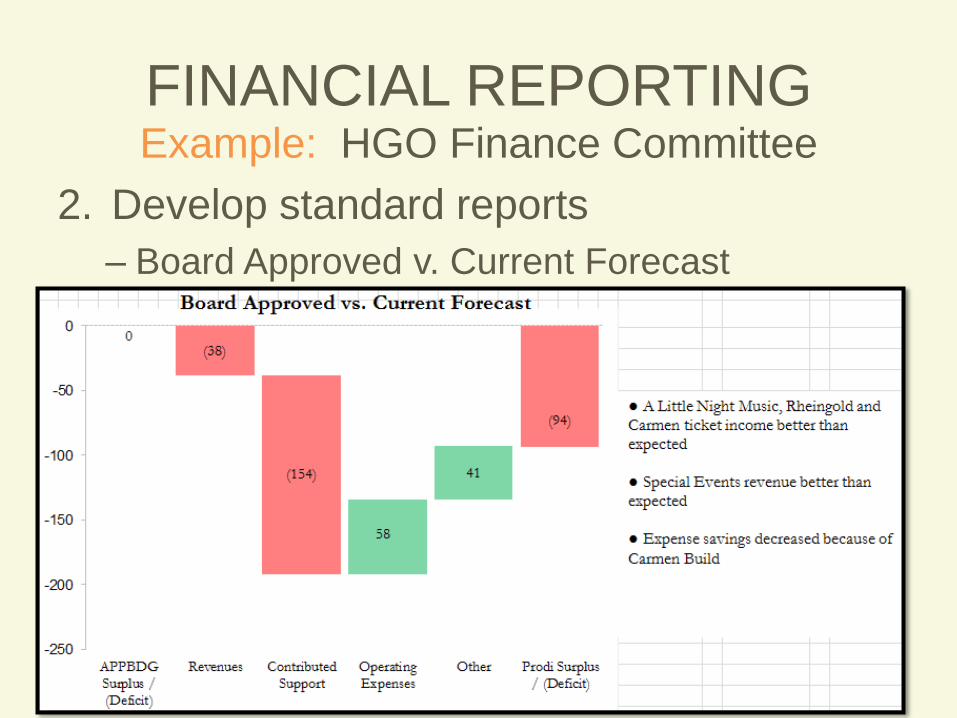

Example: HGO Finance Committee

2. Develop standard reports

– Board Approved v. Current Forecast

FINANCIAL REPORTING

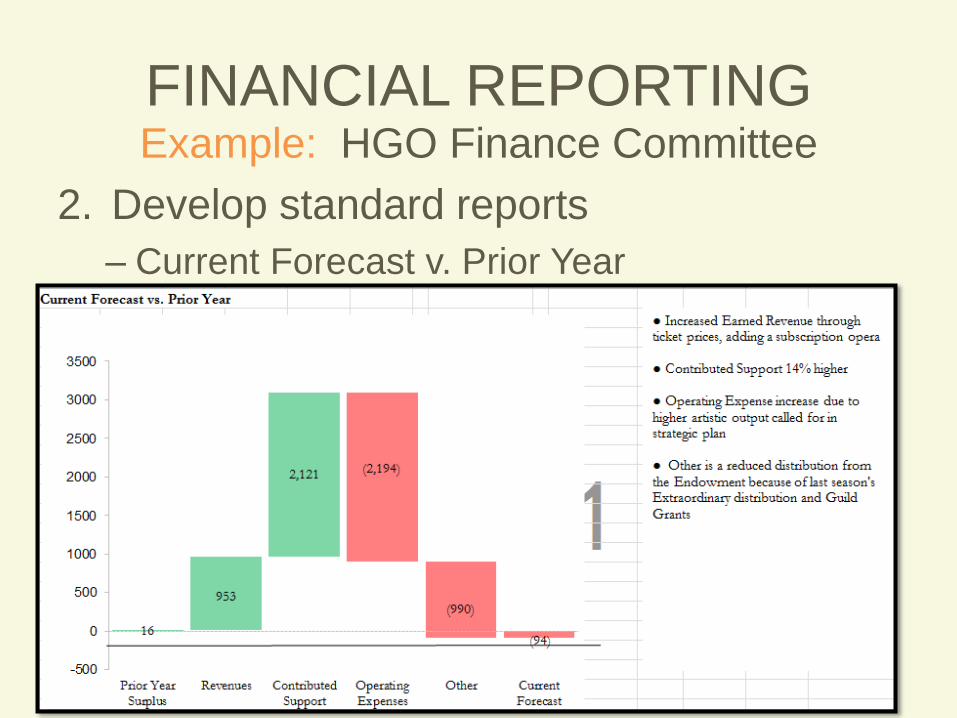

Example: HGO Finance Committee

2. Develop standard reports

– Current Forecast v. Prior Year

FINANCIAL REPORTING

Example: HGO Finance Committee

3. Gather feedback, refine

– Missing data/stories

– Visual displays

– Personal preferences

– Group discussion or one-offs?

FINANCIAL REPORTING

To develop a good budgeting process:

FORECASTING REVENUES

Document- Write it down!

Decide who’s involved and when

• List specific tasks with specific responsibility assignments

Create annual timeline

• In line with important meetings for approvals/review

Adopt policies for adhering to budgets, handling variances, approval authority, etc.

On-going checks & balances

Contributed Revenue

• Revenue is generally the starting point in a budget

planning process

– forecast level determines program delivery

• Incredibly important to accurately predict, AND to

closely track progress of approved goals

Q: How do you currently forecast your

revenue?

% increase? Individualized?

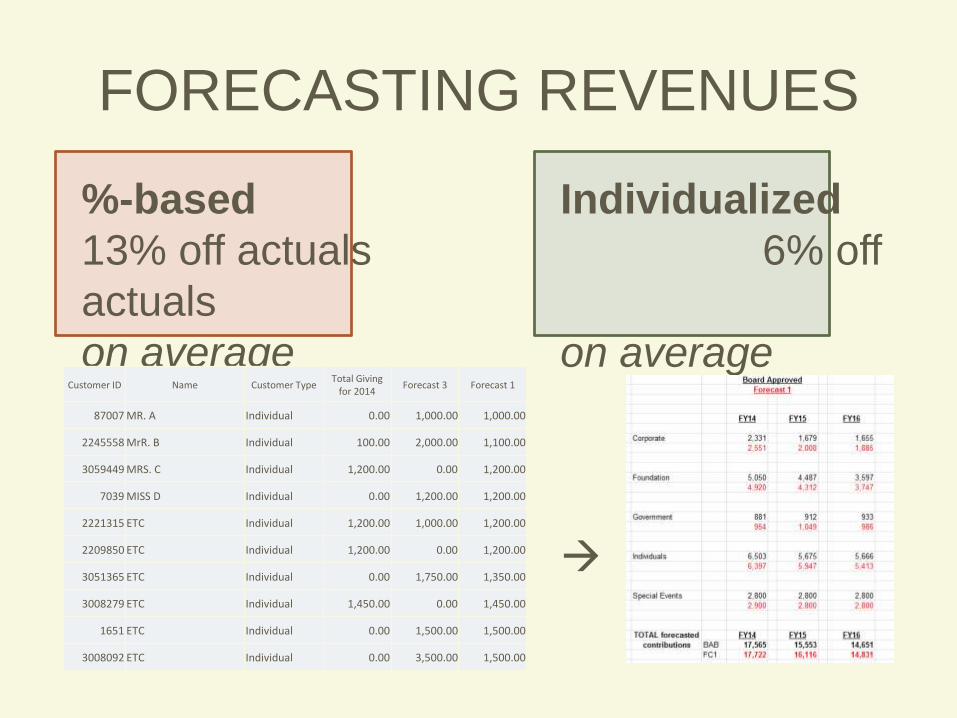

FORECASTING REVENUES

%-based Individualized

13% off actuals 6% off

actuals

on average on average

FORECASTING REVENUES

Customer ID Name Customer TypeTotal Giving

for 2014Forecast 3 Forecast 1

87007 MR. A Individual 0.00 1,000.00 1,000.00

2245558 MrR. B Individual 100.00 2,000.00 1,100.00

3059449 MRS. C Individual 1,200.00 0.00 1,200.00

7039 MISS D Individual 0.00 1,200.00 1,200.00

2221315 ETC Individual 1,200.00 1,000.00 1,200.00

2209850 ETC Individual 1,200.00 0.00 1,200.00

3051365 ETC Individual 0.00 1,750.00 1,350.00

3008279 ETC Individual 1,450.00 0.00 1,450.00

1651 ETC Individual 0.00 1,500.00 1,500.00

3008092 ETC Individual 0.00 3,500.00 1,500.00

Tracking Goals

Q: How do you track progress once goals are

set?

Forecast data needs to link to contributions:

Can show actuals v. budget (in detail) and

top ‘outstanding’ forecasts

HGO’s Top 10/100/1000:

FORECASTING REVENUES

customer no Name cust type Total Giving Forecast 1 balance

185175 MR. A Individual - 4,000.00 4,000.00

234869 MRS. B Individual 6,000.00 10,000.00 4,000.00

246768 MISS C Individual 1,200.00 5,200.00 4,000.00

2224715 MISTER D Individual - 4,000.00 4,000.00

2238532 ETC Individual - 4,000.00 4,000.00

2259744 ETC Individual 1,166.69 5,000.00 3,833.31

200949 ETC Individual - 2,000.00 2,000.00

3022557 ETC Individual - 2,000.00 2,000.00

17474 ETC Individual - 2,000.00 2,000.00

2250513 ETC Family Foundation

- 1,000.00 1,000.00

2260945 ETC Individual 6,500.00 7,000.00 500.00

19036 ETC Individual 1,750.00 2,000.00 250.00

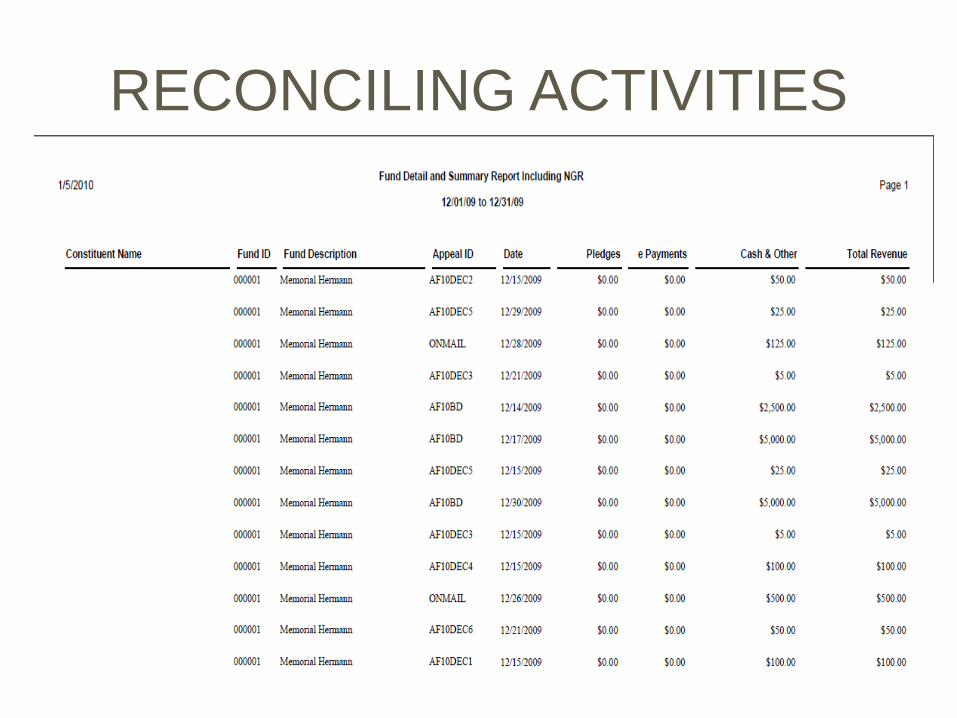

RECONCILING ACTIVITIES• Each month, all donations received that month need to be

reconciled with “Finance"

• Donations are batched for deposit and then each month's batches are balanced

• Pledge, payment and cash reports need to be generated and reconciled with your organization's bank statements

• This also gives you the opportunities to clean donation data

• After a month is "closed", gift dates and amounts should never be adjusted. Restrictions can be adjusted.

• If reconciling each month, the end of your fiscal year reconciliation should be much easier.

• Result? Clean and beautiful audit and IRS 990 filing

• Each month, all donations received that month need to be reconciled with

“Finance"

• Donations are batched for deposit and then each month's batches are

balanced

• Pledge, payment and cash reports need to be generated and reconciled with

your organization's bank statements

• This also gives you the opportunities to clean donation data

• After a month is "closed", gift dates and amounts should never be adjusted.

Restrictions can be adjusted.

• If reconciling each month, the end of your fiscal year reconciliation should be

much easier.

• Result? Clean and beautiful audit and IRS 990 filing

RECONCILING ACTIVITIES

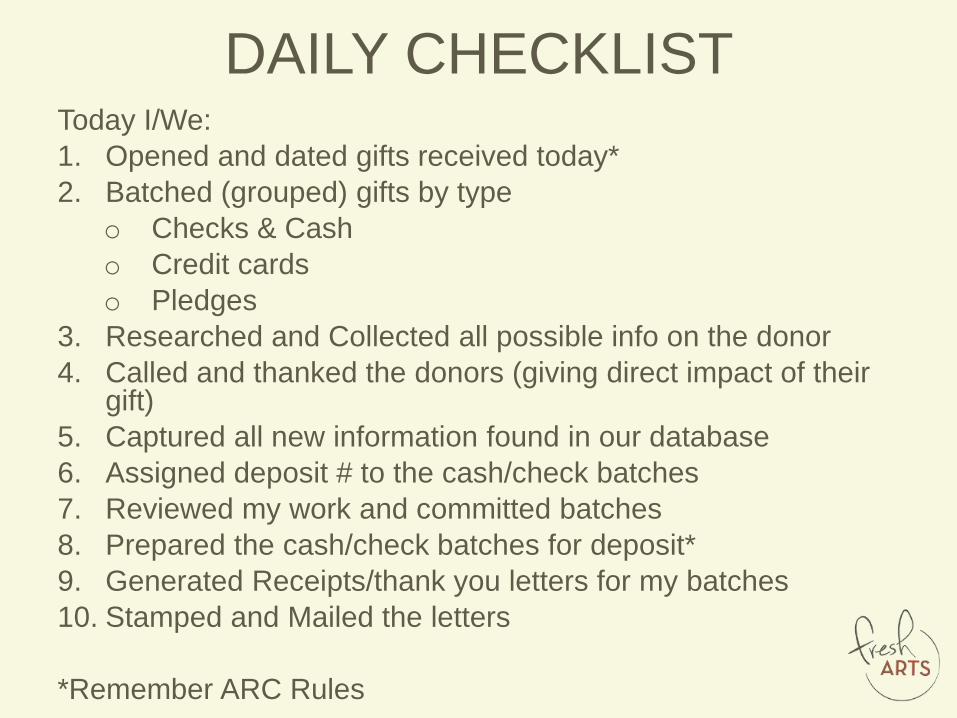

DAILY CHECKLISTToday I/We:

1. Opened and dated gifts received today*

2. Batched (grouped) gifts by type

o Checks & Cash

o Credit cards

o Pledges

3. Researched and Collected all possible info on the donor

4. Called and thanked the donors (giving direct impact of their gift)

5. Captured all new information found in our database

6. Assigned deposit # to the cash/check batches

7. Reviewed my work and committed batches

8. Prepared the cash/check batches for deposit*

9. Generated Receipts/thank you letters for my batches

10. Stamped and Mailed the letters

*Remember ARC Rules

RESOURCESNonprofit Accounting Basics:

http://www.nonprofitaccountingbasics.org/

Fund Services:

FundSvcs.org

IRS: http://www.irs.gov/Charities-&-Non-Profits/Frequently-

Asked-Questions-about-Tax-Exempt-Organizations

GWSCPA:

http://www.gwscpa.org/

IN YOUR INBOX TOMORROW

This PowerPoint

List of example docs and resources

Info about upcoming workshops including

– MEET YOUR MEDIA: With Joel Luks, Molly

Glentzer, Bill Davenport

June 8, 6-8 p.m. @ Diverseworks Artspace

Link to a post-workshop survey